PSTX - Poseida Therapeutics: Intriguing Buy And Hold Opportunity Thanks To Big Pharma Backers

Summary

- Poseida is emerging as a leader in the allogeneic cell therapy field.

- A deal struck with Swiss Pharma giant Roche last year involved a $110m upfront payment plus as much as $6bn in development and commercial milestone payments.

- The 2 companies will develop allogeneic cell therapies targeting hematological cancers - the first candidate has shown some early promise.

- Novartis has also invested heavily in Poseida, and a third large Pharma, Takeda, has a co-development agreement for preclinical gene therapy programmes.

- After its first autologous candidate failed to show efficacy in the clinic, Poseida's share price fell from $16, to <$2. Now it is back on the rise - this could be one of the better cell therapy opportunities to back.

Investment Overview

San Diego based Poseida Therapeutics ( PSTX ) opted to abandon plans to launch its initial public offering back in April 2019, instead completing a Series C financing worth $142m, which was led by a $75m equity investment from Danish Pharma giant Novartis ( NVS ).

Poseida is a cell therapy specialist that was spun out of Transposagen Biopharmaceuticals in 2015. Transposagen is a genetic engineering platform technology specialist whose CEO and President of 13 years Dr. Eric Ostertag became CEO of Poseida, serving in the role until 2022, when he became Executive Chairman.

18 months later, Poseida did complete an IPO - after raising a further $110m via a Series D financing - raising ~$224m via the issuance of 14m shares at $16 per share. It's lead candidate throughout this period was a B-cell maturation antigen ("BCMA") CAR-T therapy, P-BCMA-101 indicated for multiple myeloma.

P-BCMA-101 was an autologous CAR-T candidate that had shown early promise, but despite the progress made in this drug class (there are now 6 FDA approved autologous on the market, including Bristol Myers Squibb's ( BMY ) Abecma and Breyanzi, Legend Biotech's ( LEGN ) / Johnson & Johnson's ( JNJ ) Carvykti, Gilead Sciences' ( GILD ) Yescarta and Tecartus, and Novartis' ( NVS ) Kymriah) - in Q4 2021 Poseida opted to discontinue development of this asset.

As disappointing as that may sound, given the funding raised was primarily aimed at preparing P-BCMA-101 for an approval shot, Poseida's CEO (at the time) Ostertag argued that the future of cell therapy lies in allogeneic, as opposed to autologous therapies.

Autologous therapies work by genetically engineering a patients' own cells ex-vivo to enhance their cancer cell-killing properties, and reintroducing them back into the patient. The genetically modified T-cells help to restore bone marrow cells that may have been damaged by chemotherapy, whilst seeking and destroying cancer cells.

Allogeneic therapies act in a similar fashion, but using blood cells from a donor, as opposed to the patients themselves. The obvious advantage is that these therapies can be created and made available "off the shelf", meaning they are more readily available and can be administered to a patient faster.

The drawback is the higher risk that a patient's immune system will reject the donor cells, leading to potentially fatal conditions such as cytokine release syndrome or graft vs host disease, and immune effector cell-associated neurotoxicity syndrome ("ICANS") or that patient's cells begin to develop resistance to the new cells over time, reducing their effectiveness.

Today, Poseida has a single wholly owned allogeneic CAR-T therapy in the clinic targeting solid tumors, plus 2 wholly-owned preclinical programs. Solid tumors is a field that has proven resistant to cell therapy - all of the approved cell therapies to date are indicated for hematological ("blood based") cancers.

The company has also entered a co-development partnership with the Swiss Pharma giant Roche ( OTCQX:RHHBY ) - in August 2022 - by the terms of which - according to Poseida's Q322 10-Q submission - Roche will:

develop, manufacture and commercialize allogeneic CAR-T cell therapy products from each of the Company’s existing P-BCMA-ALLO1 and P-CD19CD20-ALLO1 programs (each a “Tier 1 Program”) and develop, manufacture and commercialize allogeneic CAR-T cell therapy products from each of the Company’s existing P-BCMACD19-ALLO1 and P-CD70-ALLO1 programs (each, a “Tier 2 Program”). The parties will conduct an initial two-year research program to explore and preclinically test a specified number of agreed-upon next generation therapeutic concepts relating to allogeneic CAR-T cell therapies.

Poseida received an upfront cash payment of $110m under the agreement, plus research funding of $75m, and there are development and commercial milestones in place that could see Roche eventually pay >$6bn to Poseida. The Roche candidates are all aimed at hematological cancers, and a candidate P-BCMA-ALLO1 has already entered a Phase 1 clinical trial.

That is not all. Poseida has also initiated a strategic partnership - in October 2021 - with another Pharma giant in Takeda ( TAK ), this time in gene therapy, for 6 initial disease targets, including a preclinical program targeting hemophilia, with up to $3.6bn of potential development and commercial milestone payments on the table.

Takeda has already made a $45m upfront payment. No assets have entered the clinic as yet.

{kind=link}

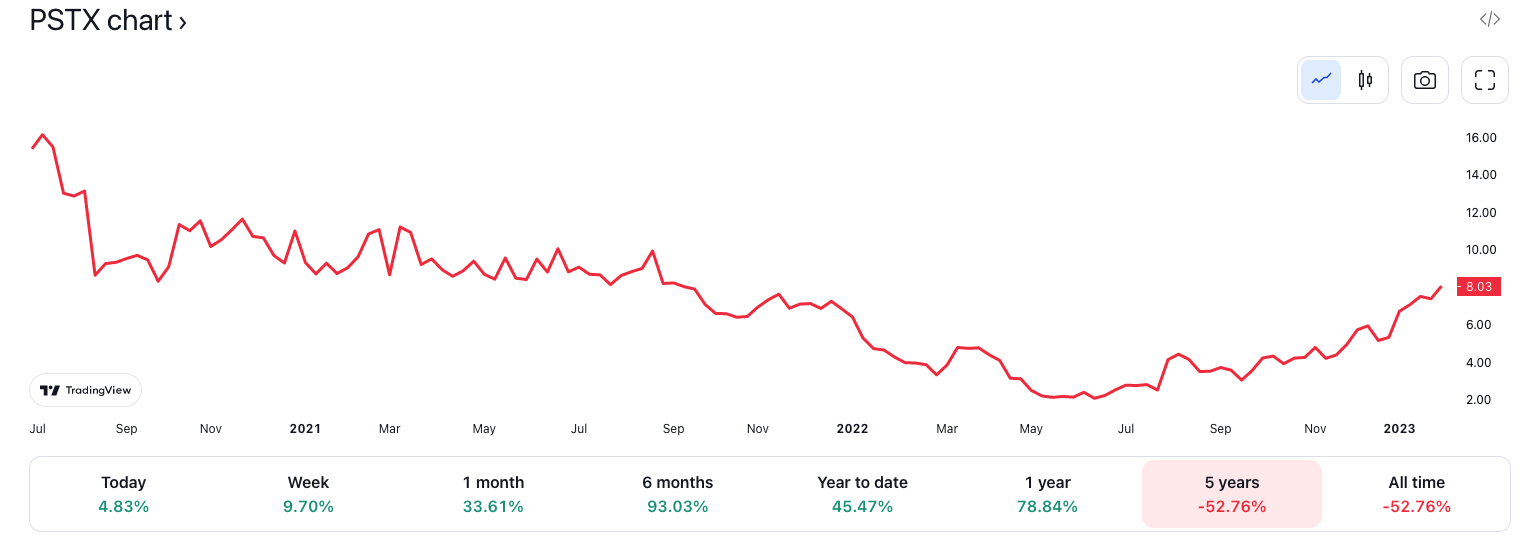

As we can see above, Poseida shares initially performed poorly post-IPO, probably due to the abandonment of its lead autologous asset P-BCMA-101, with shares hitting a low of <$2.5 in late July last year, before the Roche deal was announced, after which point Poseida stock has been steadily climbing, reaching a market cap valuation of $658m at the time of writing.

That is a reasonably high valuation for a biotech with only 2 Phase 1 assets, that recently abandoned its lead program, although former CEO Ostertag, who is now Executive Chairman of Poseida - has claimed that:

The initiation of our P-BCMA-ALLO1 clinical trial represents the beginning of a long-planned strategic transition to what we believe is the ‘holy grail’ of cell therapy for oncology, a fully allogeneic CAR-T with a fully-humanized heavy chain BCMA binder and a high percentage of T SCM cells, which we believe are the key to success.

In the remainder of this post I'll dive into Poseida, its science and pipeline and early clinical performance in the allogeneic space in a little more detail to try to come to a conclusion about whether Poseida truly merits its current valuation, and what the share price may look like 1-3 years from now.

Poseida's quest for the "Holy Grail" - An Allogeneic, Solid Tumor Targeting Cell Therapy

{kind=link}

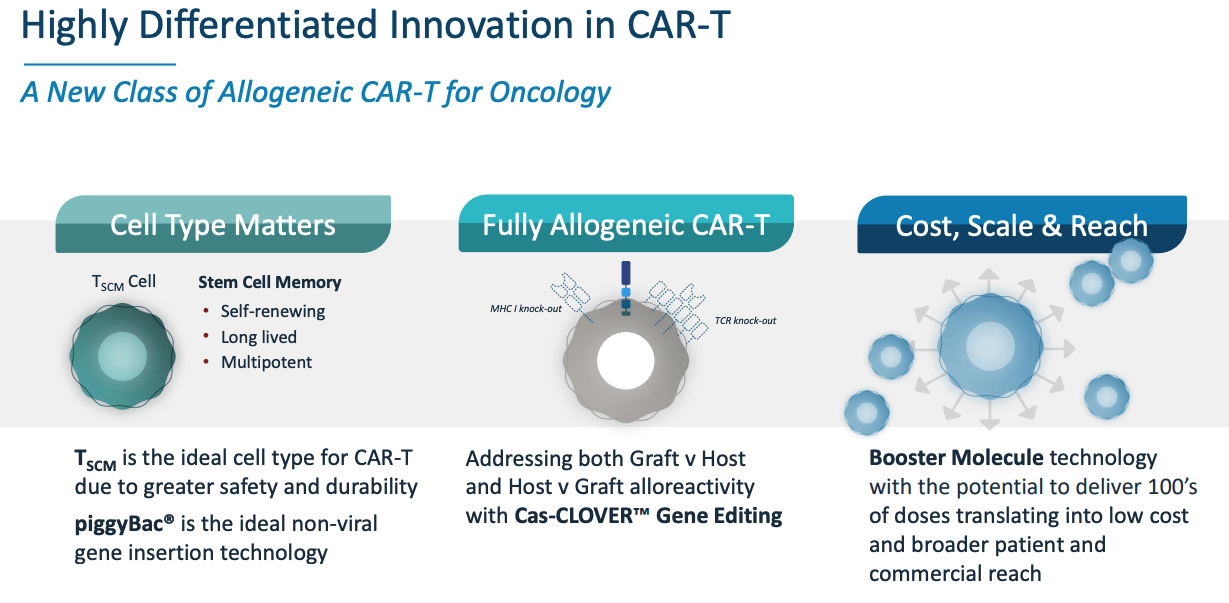

Essentially there are 3 ways in which Poseida believes it can create "a new class" of allogeneic therapies in CAR-T, targeting both solid tumors via its wholly owned programs - which would represent a revolutionary breakthrough if achieved - and hematological malignancies alongside Roche - an extremely lucrative opportunity thanks to the structure of the Roche deal.

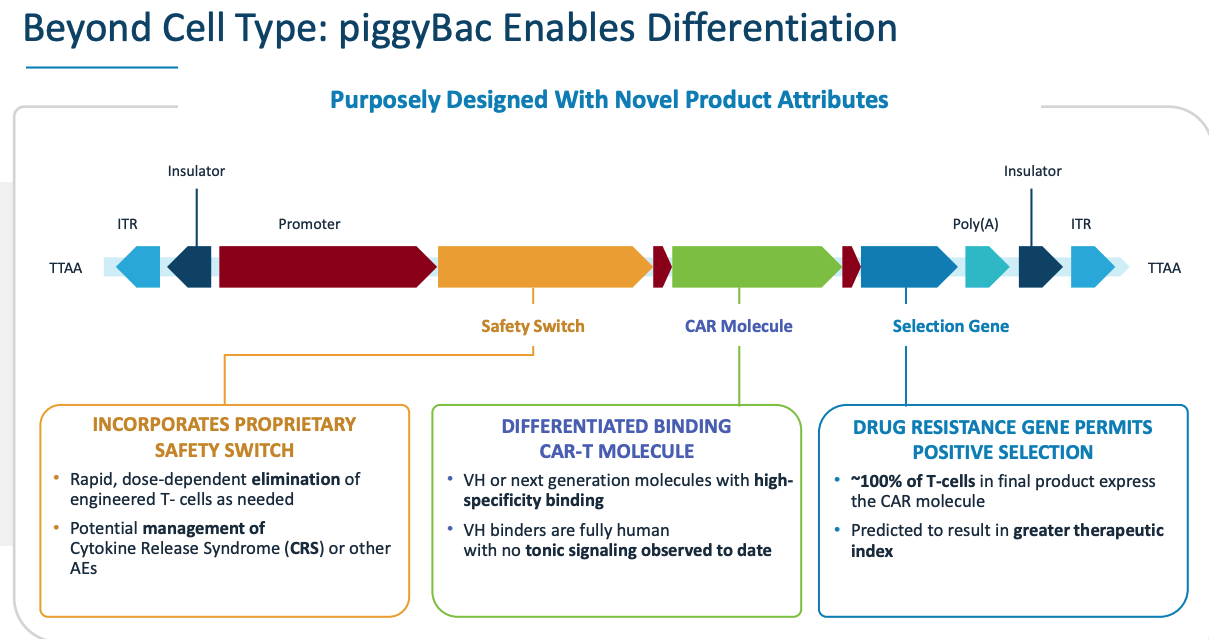

The first is by targeting what are known as "Stem Cell Memory T-cells - Poseida says these cells are ideal for allogeneic CAR-T because they are "self-renewing, long lived, and multipotent" - and then using its custom non-viral, gene insertion technology "piggyBac" to ensure safety and high specificity of binding, with 100% of the engineered cells expressing the CAR molecule, resulting in a "greater therapeutic index", as shown below.

{kind=link}

The second is to employ state-of-the-art Cas-CLOVER gene editing - borrowing from the Nobel prize winning CRISPR-Cas9 technology employed by the likes of CRISPR Therapeutics, and Intellia Therapeutics ( NTLA ) - and applying it to ex-vivo gene editing as these companies are also doing, alongside in vivo therapeutics - to achieve the cleanest possible editing and avoid off-target toxicity.

Finally Poseida is using "booster molecule" technology to drive "cost, scale and reach", and by this, I believe Poseida is referring to the use of delivery methods such as lipid nanoparticles - again, not necessarily new or proprietary technology, but used by most gene and cell therapy drug developers as well as messenger-RNA drug developers such as the vaccine giants Moderna ( MRNA ) and BioNTech ( BNTX ) - to achieve non-viral delivery.

Early Signs Of Promise

Poseida has been able to show some signs of efficacy in the clinic with its wholly owned solid tumor candidate P-MUC1C-ALLO1, presenting clinical data at ESMO last year, and reporting, from a safety perspective:

No dose-limiting toxicities ("DLTs"), cytokine release syndrome ("CRS"), graft vs host disease ("GVHD") or immune effector cell-associated neurotoxicity syndrome ("ICANS").

Additionally there were some signs of efficacy too - a partial response ("PR") from 1 patient with breast cancer, and stable disease in 2 patients with pancreatic and colorectal cancers respectively, out of 7 dosed patients overall.

These results - achieved in patients with treatment resistant cancers - are encouraging, particularly from a safety perspective although there is clearly much more work to be done - going forward Poseida will increase dose levels and it will be interesting to see what effect that has on both safety and efficacy, and whether the responses are durable - a key factor in the success of cell therapies. Although these drugs will likely only be used as third or fourth line therapies, the market opportunity is substantial, Poseida believes.

Meanwhile, the likes of Moderna and BioNTech are developing "personalised cancer vaccines" ("PCVs") that work by injecting mRNA into a patients' tumor, containing instructions to help the immune system recognise types of circulating tumor DNA and use this knowledge to attack cancer cells. These PCVs are at a similar stage of development but have been shown to be successful, when used alongside Immune Checkpoint Inhibitors ("ICIs") such as Merck's Keytruda - the current standard of care in a wide range of solid tumor cancers.

Poseida argues that the likes of breast and ovarian cancers are fields where ICIs are less effective and PCV's untested, and that is true, at least for the time being. Any kind of breakthrough by a cell therapy treating a solid tumor cancer is likely to be greeted with a hysterical reaction in the markets, and result in a substantial rise in Poseida's share price.

The issue I would point to here is that Poseida's track record is not good, having withdrawn its lead autologous asset, plus the efficacy and safety need to be durable for the therapy to work.

In short, Poseida is taking on a massive challenge the difficulty of which should not be underestimated, where the chances of success are very slim.

The Roche Partnership - Solid Early Progress

It's instructive to me that Roche has not shown an interest in targeting solid tumors with Poseida's cell therapies, instead focusing on hematological cancers.

Poseida also reported data concerning the Roche partnered lead asset P-BCMA-ALLO1 at ESMO last year, and again the results seem encouraging. Out of 6 evaluable patients with relapsed / refractory multiple myeloma ("MM") receiving the lowest dose level:

As of the cutoff date, P-BCMA-ALLO1 achieved a 50% (3/6) overall response rate, with a 66% (2/3) ORR in patients who had previously received BCMA-targeted therapy and a 50% (2/4) ORR in patients with high-risk cytogenetics.

These results look strong although the bar for cell therapies in MM has been set high , with approved Abecma having achieved an Overall Response Rate ("ORR") of 72%, and a Complete Response "CR") rate of 28% in its pivotal trial, and Carvykti achieving an ORR of 98%, and CR of 78%, with an acceptable safety profile.

Of course, Roche's therapy is Allogeneic and its safety profile also looks strong, with no dose limiting toxicities, CRS, GVHD or iCANS detected in the study to date.

If these results can be repeated in later stage trials, at higher dosages, then Roche and Poseida could target a first ever approval for an allogeneic CAR-T, which would be a historic moment, and trigger a high triple-digit- million, or possibly over $1bn milestone payment to Poseida plus a small share of net sales of the drug.

Gene Therapy - Intriguing Targets But Too Early To Assess Progress

Poseida's approach to gene therapy and its deal with Takeda quite closely mirrors what the company is doing with Roche in allogeneic cell therapy. Once again, Poseida's piggyBac gene insertion technology, Cas-Clover gene editing capabilities, and non-viral delivery form the basis of its work.

Hemophilia is the first major target - the disease is caused by deficiency in functional coagulation factor VIII and Poseida is pursuing an in-vivo approach where lipid nanoparticles are used to safely deliver the gene correction materials. This approach could result in the permanent curing of patients who currently have to endure a lifetime of regular blood transfusions.

Poseida also has a wholly-owned candidate targeting liver disease Ornithine Transcarbamylase, or OTC, deficiency, this time using AAV and nanoparticles.

By the terms of the Takeda agreement, Takeda has the opportunity to develop up to six in vivo gene therapy programs, with an additional option to add two more programs to the collaboration.

Overall, the collaboration looks intriguing, and additionally exciting because it is looking at in-vivo opportunities, which ought to be easier on patients than ex-vivo cell therapy, which requires days of patient pre-conditioning and comes with additional risks of an adverse immune response.

Until one or two candidates have been approved for in-human studies by the FDA, it is difficult to assess how successful this partnership can be, but once again, the fact that Poseida has been able to enlist the support of a major Pharma speaks to the competency of the management team and the company's technology.

Conclusion - 3 Major Pharmas Are Backing Poseida To Succeed With An "Evolution Not Revolution" Platform - A Decent Buy and Hold Opportunity

When it comes to the cell therapy landscape, there are a number of oncology focused biotechs developing allogeneic therapies to be aware of, including Adicet Bio ( ACET ), Adaptimmune ( ADAP ), Allogene Therapeutics ( ALLO ), Astellas Pharma (ALPMF) (ALPMY), Athenex ( ATNX ), Atara ( ATRA ) - partnering with Pharma giant Merck ( MRK ), Beam Therapeutics ( BEAM ), bluebird bio ( BLUE ), Cellectis ( CLLS ), CRISPR Therapeutics ( CRSP ), CTI Biopharma ( CTIC ), Celyad Oncology ( CYAD ), Fate Therapeutics ( FATE ), Gamida Cell Ltd ( GMDA ), IN8Bio ( INAB ), MiNK Therapeutics ( INKT ), Jasper Therapeutics ( JSPR ), Kiromic BioPharma ( KRBP ), Lineage ( LCTX ), Legend Biotech ( LEGN ), Senti Biosciences ( SNTI ), and TCR2 Therapeutics ( TCRR ).

Framed in the context of so much competition and having little more than Phase 1 study data - at the lowest does - in a handful of patients, it's difficult to argue that Poseida is a front-runner to win the race for a first ever approved allogeneic CAR-T therapy, let alone win out in the race to deliver a first ever approved in vivo gene editing therapy.

That helps to explain why Poseida's valuation declined to the extent it did throughout 2022, but the Roche deal has made Poseida's share price the best performing of all of the above mentioned companies over the past 12 months.

What I like about Poseida is that its approach appears to be based on "evolution not revolution". Its technology platform is not necessarily breaking new ground, but employing several of the most important scientific approaches to in vivo and ex vivo therapies developed to date, including e.g. Cas-Clover gene editing, nanoparticle delivery technology, and perhaps most significantly, stem cell memory cells - as close to a Unique Selling Point as Poseida has.

The failure of its autologous candidate is disappointing - especially for investors in the company who bought stock in Poseida in the hopes of seeing it quickly progress into late stage trials - but if we take the management team at their word, then autologous therapies have always been the long-term goal.

Thanks to Roche, Poseida has plenty of funds available for developing not just Roche-partnered assets targeting hematological malignancies, but also its own solid tumor candidates - and what a coup it would be if Poseida made a breakthrough in that field.

Moderna's market cap valuation increased by ~$10bn after its PCV candidate showed efficacy in combo with Merck's Keytruda as an adjuvant therapy in melanoma, so imagine the gains Poseida might be capable of if it succeeds with an allogeneic therapy in breast or colorectal cancer.

That is why I think Poseida will be worth keeping a close eye in 2023. There will be more data from its clinical candidates arriving this year, plus an IND for another Roche partnered asset targeting CD19/CD20, recognised targets for blood cancers.

Roche is in a position where it cannot really lose on the deal, and Takeda also - a data readout of note in 2023 that highlights durability of response, safety, and efficacy of either a Roche or Takeda partnered asset, or indeed one of its wholly owned assets could create a genuine sense of excitement about where Poseida is headed. Poseida is an intriguing buy and hold position for a risk-on biotech investor, in my view.

For further details see:

Poseida Therapeutics: Intriguing Buy And Hold Opportunity Thanks To Big Pharma Backers