PSTNY - PostNL: Not The Greatest Q4 Results Weak 2023 Guidance

Summary

- Competition is increasing and PostNL is losing market share.

- Cost savings initiatives will not mitigate cost inflationary pressure.

- 2023 guidance is even worse than we had expected.

It was a good call to initiate PostNL ( OTCPK:TNTFF ) ( OTCPK:PSTNY ) with a neutral rating and six negative points. Looking back to our analysis, here at the Lab, we anticipated some of the outcomes just released in the Fiscal Year 2022 account, and we also emphasized the negative company's evolution by publishing two reports in the half year and Q3 respectively called Not Our Cup Of Tea and Another Negative Quarter . Our PostNL main concerns were due to the structural change that’s happening in the Netherlands. Competition is picking up, and this is not only coming from traditional peers such as Deutsche Post AG (DPSTF), but also from new entrants such as Budbee (that already invested in green CAPEX facilities and have a fleet fueled by r enewable diesel).

During the COVID-19 outbreaks, PostNL competitors and last-mile logistics players have exponentially increased capacity. This has created an oversupply which – in an operationally geared environment – leads to price competition in order to secure volumes.

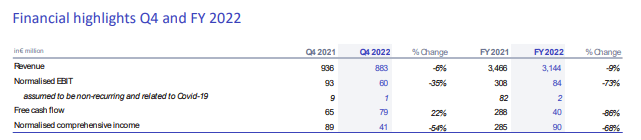

Q4 and FY 2022 results

In FY22, the Dutch postal operator incu rred higher-than-expected cost inflation pressure. Cross-checking the company's previous estimates, they were forecasting a higher cost of €65 million and this resulted to be € 135 million. C ontract prices are usually fixed once a year (mostly at the very beginning of the calendar year), and for PostNL was impossible to pass on these higher costs to cl ients. Despite the fact that the company managed to realize €45 million in gross savings initiatives, PostNL had to absorb the higher expenses itself. If we are adding Parcels development with the drop in volumes, this explained the €100 million negative impact on the core EBIT.

The company CEO explained that “ 2022 turned out to be a turbulent year. The global macroeconomic and geopolitical environment was extremely challenging, with record-high inflation and consumer confidence at an all-time low. This impacted our performance, as we saw a sharp increase in labor and fuel costs". However, during the analyst call, PostNL management spent more time engaging investors’ attention on e-commerce growth rather than analyzing fundamental questions about revenues and margin development. The company forgot to mention the growing competition and the market changes (i.e. insourcing and growth in out-of-home) and how PostNL is facing a loss in market share penetration. According to market regulator ACM , in 2016, the Dutch postal player used to have a 60-65% volume share in its domestic market. In 2021, this dropped to a level of between 50-55%, and adding the last year’s numbers, there is a further 2%-point drop.

{kind=link}

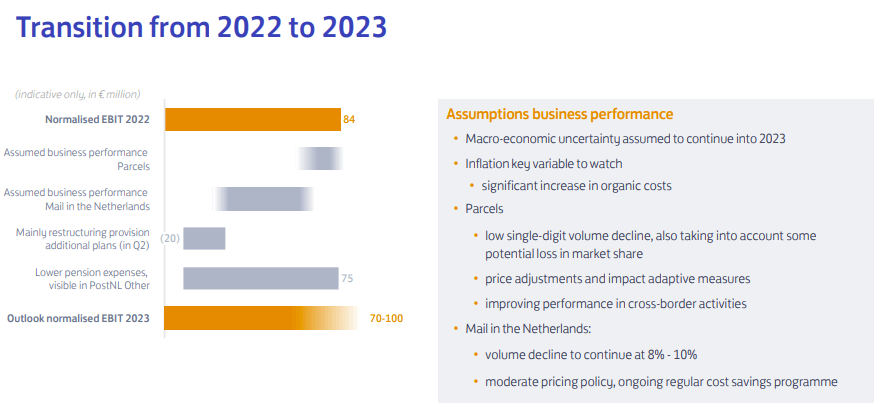

The slide below shows that our 2022 fears have turned into reality (Fig 1). Higher tariffs won't be enough to offset the 2022/2023 cost inflation pressure. PostNL is expecting to reduce this gap by approximately €35 million. As already mentioned, in 2022, the negative pricing delta was circa €135 million, including also the cost-saving plan at €45 million, hence, last year’s net raw material price increase was even higher than what we had estimated. The company is trying to look safer than they really are. However, it is important to emphasize that the company will not close the pricing/costs gap and will be widening further in the Fiscal Year 2023.

{kind=link}

So, we are not surprised that PostNL will reduce its total workforce by 200-300 FTEs and already announced a provision for a total amount of €20 million mainly for restructuring. Aside from the €30 in cost savings, the company disclosed an additional run rate savings plan of €25 million in 2024 and 2025. Despite that, parcel volume will again decrease and PostNL estimates a further decline in the ‘ low -single- digit ’ percentage in a market that is expected to be ‘ flat to growing at a low-single- digit rate ’. And as already mentioned, this translates into another market share loss.

PostNL 2023 outlook

Conclusion and Valuation

PostNL aims to have a leverage ratio not exceeding 2.0x and with the latest numbers, the company reached 1.9x. There is a €10 million capex dedicated to innovation to add, and without surprise, the second buy-back tranche was postponed until further recovery of the core activity business performance. 2022 results and the guidance for the current year clearly reflect the company's stock price performance. Continuing to value PostNL with a P/E of 8x, we reiterate our neutral rating at €2 per share ($2.12 in ADR).

For further details see:

PostNL: Not The Greatest Q4 Results, Weak 2023 Guidance