POWL - Powell: Great Opportunities But Minimal Upside For Now

2024-06-29 10:00:00 ET

Summary

- The higher oil/ gas spot prices have contributed to higher industry-wide capex, triggering POWL's double-digit revenue growth and triple digit EPS growth in FY2023.

- There are great opportunities in the data center market as well, with the generative AI boom triggering increased electrical power demands and expanded utility/ data center projects.

- While the data center market remains nascent to POWL, we believe that the intensified sampling and capacity expansion may allow the company to capture incremental growth prospects.

- The stock is also relatively cheap compared to its peers, with the market expecting accelerated top/ bottom-line growth prospects through FY2025.

- Nonetheless, with POWL charting a head and shoulder pattern while being highly shorted, we believe that there is a minimal margin of safety here.

POWL's Investment Thesis Remains Promising, Assuming Successful Data Center Monetization

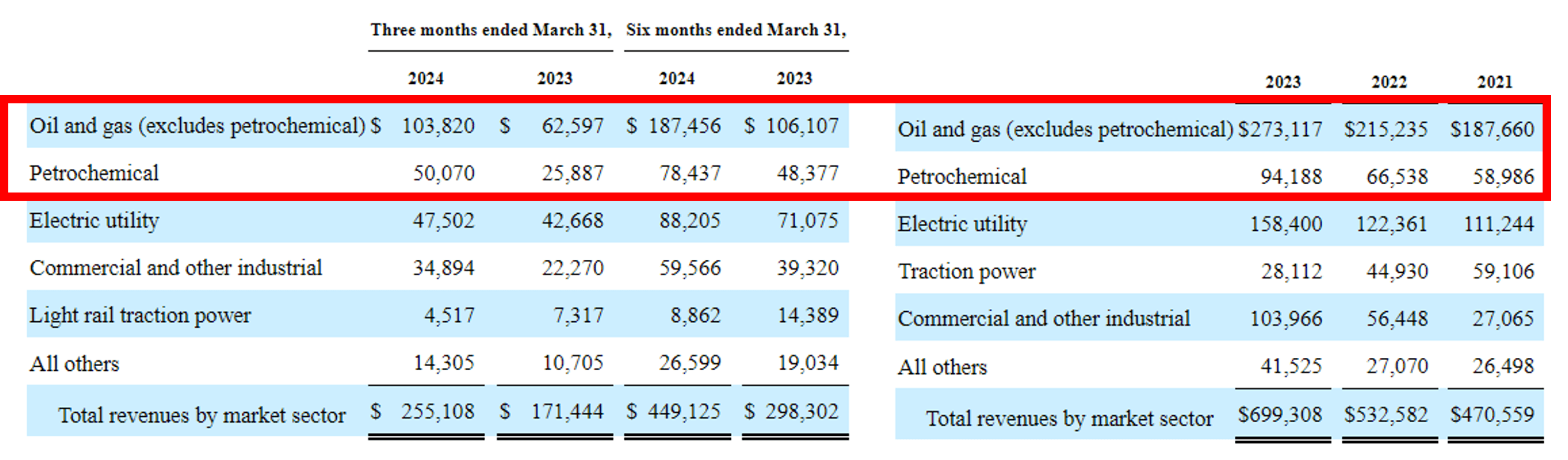

POWL's Revenue Segments

{kind=link}

Powell Industries, Inc. (NASDAQ: POWL ) is a company that develops, manufactures, and sells custom-engineered electronic equipment and systems for multiple end markets, most notably the Oil and Gas and Petrochemical industry, which comprises 52.5% (-0.4 points YoY) of its FY2023 revenues and 60.3% in FQ2'24 ( +2.6 points QoQ / +8.7 YoY)....

Powell: Great Opportunities But Minimal Upside For Now