BNO - Praetorian Capital Fund Q4 2022 Investor Letter

Summary

- Praetorian Capital is a “global-micro” hedge fund managed by Harris “Kuppy” Kupperman. The fund is dedicated to seeking non-correlated, asymmetric returns.

- During the fourth quarter of 2022, the fund appreciated by 15.26% net of fees.

- Currently, Central Bankers are trying to control the damage from decades of excessive money printing. Ultimately, they will not be able to take the pain that they are inflicting, and they will pivot—we are anxiously waiting for that pivot.

During the fourth quarter of 2022, the fund appreciated by 15.26% net of fees. For 2022, the fund appreciated by 11.95% net of fees. Given the fund’s concentrated portfolio structure and focus on asymmetric opportunities, I anticipate that the fund will be rather volatile from quarter to quarter. During the fourth quarter, many of our core portfolio positions appreciated moderately while the Event-Driven book produced a small positive return.

| Praetorian Capital Fund LLC |

| Gross Return |

| Net Return* |

| Q1 2022 |

| 19.79% |

| 15.55% |

| Q2 2022 |

| -18.16% |

| -15.69% |

| Q3 2022 |

| 0.01% |

| -0.30% |

| Q4 2022 |

| 18.69% |

| 15.26% |

| YTD 2022 |

| 16.38% |

| 11.95% |

| 2021 |

| 181.80% |

| 142.87% |

| 2020 |

| 161.87% |

| 129.49% |

| 2019 |

| 18.71% |

| 14.97% |

| Since Inception (1/1/19) |

| 919.49% |

| 617.39% |

| * Unaudited net return data is estimated, net of all fees and expenses (using the expense structure in place at the time, which was: a maximum of 2% expenses from Inception through December 2020, and a 1.25% Management fee since January 2021). |

As this fund has now completed its fourth consecutive year of positive returns, I thought it would be helpful to review my performance expectations for this fund. To start with, the first four years were roughly in-line with how I anticipated that the fund’s performance profile would look. As a fund that focuses on inflection investing, we will experience some years where we participate in strongly inflecting trends, potentially earning triple-digit net returns (like during 2020 and 2021). Offsetting this, there will also be some years where our core themes do not trend, or even fail. During those years, I’d expect our performance to cluster around unchanged (like during 2019 and 2022) with our Event-Driven book likely adding to the overall net outcome.

As 2022 is now complete, I’d like to focus on the five core trends that we were invested in during the year, zeroing in on the fact that not a single one of them worked—which is something of a rarity during my career.

To start with, our “Russian Adventure” (for lack of a better term) has been a disaster, costing us approximately 770 basis points net of fees. While I’m hopeful that this may be reversed at some future date, there is zero clarity on when or if we will ever have this capital returned to us.

Our exposure to legacy media (primarily print and radio) transitioning to the digital space was also rather disappointing. While these businesses made considerable progress in terms of growing their digital businesses, declines in their legacy businesses accelerated in some cases. Meanwhile, fears of an advertising recession during 2023 hurt the share prices of our investments. Our four current positions have declined between 24% to 46% during the course of 2022—though we did not own two of them at the start of the year. Clearly this performance was far from ideal—despite the strong underlying trends toward a digital transformation remaining intact.

Moving on, I was quite bullish on US housing, yet housing doesn’t really “work” with mortgages rates moving into the 7% range like they did during the year. Our largest housing position, St. Joe ( JOE ) declined by approximately 26% during the year, while our housing materials businesses saw their end markets vaporize during the fourth quarter. Fortunately, we were able to exit our housing materials exposure for a small net gain, as we purchased them quite cheaply and traded around them adroitly. As an inflection investor, I know that I’ll frequently get the thesis wrong. Therefore, discipline on valuation and speed on the exit when the macro turns is paramount. I’m particularly proud that we were able to earn a small return on what turned out to be a mistaken investment thesis. When employed correctly, inflection investing works, and the slight positive performance of our materials names, despite getting the thesis wrong, is proof of it. At the same time, the trend towards net migration to Florida picked up steam during the year, with Florida becoming the state with the most net migration in the nation. Clearly this is a long-term positive for JOE, even if interest rates remain a short-term headwind. As a result, we used weakness in the share price to dramatically increase the size of our position in JOE, mostly at prices below where the shares ended the year.

Now, let’s go to our largest exposures at the start of the year, oil and uranium. Oil effectively roundtripped during the year, with Brent Oil increasing from $78 to $86 during the year, after peaking out at $139. Our oil exposure has mostly consisted of two core investment genres—long-dated oil futures and futures call options, and oilfield service providers. In the case of oil, despite a lot of movement, the price ended only 10% higher than where it started, and we experienced minimal net movement on our long-dated oil positions. Fortunately, our oilfield services positions appreciated dramatically, becoming one of the few victories in the portfolio during 2022. While I’m proud of the performance of the services names, it’s worth being intellectually honest here. I thought that oil would end the year much higher than it did. However, as I’ll discuss shortly, I think this performance has simply been deferred into 2023.

Finally, spot uranium prices appreciated moderately from $42 to $49. Yet, once again, we suffered in this thesis. Kazakhstan is slowly being dragged into the Russian and Chinese orbit, which has not been a positive for Kazakh asset valuations, mostly priced amongst Western investors. This was further compounded by a rather messy power change during January, as long-time strong-man, Nazarbayev, was replaced with Russian help. As you can imagine, this was a negative for our sizable position in Kazatomprom (KAP – LI), and it declined from $36.75 to $28.14 during 2022. However, Sprott Physical Uranium Trust ( SRUUF ) did appreciate by 6% in US Dollar terms during the year. Once again, I had a thesis on uranium, and it didn’t quite work out as I had expected. Even worse, our only producer got caught up in unexpected geopolitical turmoil, leaving our portfolio with a black eye.

In summary, this was a rather miserable performance for our portfolio’s core positions, made worse by how concentrated the portfolio has been over the past few quarters. When I think back on 2022, quite honestly, nothing worked—four out my of our five core themes went nowhere, while our Russian positions completely detonated. That said, we still made it through the year with a small net gain and I want to focus on this gain to explain why I remain such a strong believer in the power of inflection investing.

How did we show a positive result when our core themes failed us? To start with, outside of our “Russian Adventure,” we did not suffer any catastrophic losses. Losses are the bane of an inflection investor as you must first overcome losses before showing gains. In this regard, my rigorous focus on balance sheet strength, cash flow generation, and most importantly valuation, helped to ensure that when we got a theme wrong, we suffered only slightly—or in the case of housing materials, earned a small positive return. Secondly, I successfully traded around positions to mitigate losses, earn some yield on short option positions and work to constantly lower our cost basis when possible. Thirdly, I was fast to exit inflecting themes when the strength of the macro faded. Inflection investing, at its core, utilizes the strength of a macro tailwind, overlaid upon deeply distressed valuations. Value stocks can stay cheap or even become cheaper. It is the macro tailwind which serves to unlock the valuation. Hence, when the tailwind turns downward, the speed of the exit is critical. Finally, our Event-Driven book was the gift that kept on giving. Even during 2022 when Event-Driven returns were sedate, they were still rather consistent, allowing us to generate cash that was deployed for de-levering or adding to positions when appropriate.

Warren Buffett has famously merged an insurance business with a securities portfolio. During most years, this has allowed him to generate consistent underwriting gains and continue to add to his portfolio, without having to use portfolio leverage in the form of broker margin. As a result, he can ignore market conditions, harvest cashflow, and frequently make large purchases during distressed periods in the markets. Instead of insurance, I prefer to use Event-Driven strategies to generate this cash, also adding to our positions during moments of stress.

While insurance is frequently not correlated with stock market cycles, our Event-Driven book’s returns tend to be inversely correlated with the markets. During periods of increased volatility, the EventDriven book tends to do better, whereas during periods of benign market activity, the Event-Driven book tends to produce minimal returns. This effect frequently offsets the depreciation of the core portfolio, becoming something of a hedge to overall volatility, while offering a tool for me to take advantage of market dislocations.

I naturally believe that Warren Buffet’s model is superior to simply owning a static portfolio of CUSIPS, waiting for them to appreciate. Having an active business tucked inside of a portfolio, earning cash flow, is an amazingly powerful tool. We’ve emulated that approach, with great success thus far, in the Event-Driven arena. Of course, just as with insurance underwriting, we will occasionally suffer large losses on the Event-Driven book. As a result, I tend to size the positions in a manner that is intended to ensure that no one position can cost us much more than 1% of our capital under normal circumstances. Should we ever experience a larger loss, it would be the result of multiple Event-Driven positions becoming correlated. While this is quite possible, it tends to be a rare occurrence. It is notable that even during the peak turmoil of the March 2020 Covid collapse, the Event-Driven book produced astonishingly strong short-term returns for us, allowing us to continue averaging down when other funds had fully utilized their capital reserves long before the markets had bottomed.

While the Event-Driven book will remain somewhat unpredictable in terms of the rate of return, it has thus far been a great boon to our overall returns. My expectation is that this will continue. However, there will be periods like during 2022 where results are tame and made worse by a conscious decision on my part to reduce exposure in the Event-Driven book as I await periods of heightened volatility.

Finally, it goes without saying that we will have years where the portfolio declines in value. This is inevitable. However, my goal is to ensure that these declines are not due to permanent losses of capital—rather they are due simply to short-term volatility within the markets. In that regard, we have yet to experience a down year at the portfolio level—despite highly volatile and varied market conditions over the past four years. I am hopeful that we can continue to build upon this record.

Market Views

For most of the past decade, unusually easy monetary conditions allowed a bevy of Ponzi Schemes to expand to near biblical proportions. While the finance industry has always experienced waves of small stock promotes that retail investors would briefly fixate on, never before have so many of these Schemes grown to such a size and taken on such a relevance to the global economy. Over the past few years, millions of US citizens were employed by Ponzis that had no chance of ever showing economic profits. Fake currencies, backed (at best) by monkey JPEGs, grew to values in the hundreds of billions. Companies owned by venture capitalists, many of which did not even pretend to do anything productive, were supposedly valued into the tens of billions, despite the fact that a handful of insiders set the prices of each financing. The prevalence, size, and longevity of many of these Schemes warped investors’ minds, and investors came to believe that metrics other than cash flow ultimately mattered. That world is now changing, and fast.

I’ve always said that Ponzi Schemes are inherently unstable. They are either expanding or collapsing; they rarely exist in a state of equilibrium. Once they begin to collapse, they rarely reinflate, and the rate of collapse tends to accelerate due to leverage and cash demands. While we’ve seen the values of various SPACs and green energy frauds rapidly collapse, the victims were mostly cloistered amongst the speculators and retail investors that often transfer their capital to professional grifters during bubbles. The next phase of collapse tends to focus on larger businesses, frauds that have become oddly respected due to their prolonged existence—we’re now midway through this phase. If history is a guide, there will soon be a period of introspection, followed by new waves of collapse. I wouldn’t be surprised if many prominent PE and VC funds show epic losses in the coming years. Their very existence has mostly been a house of cards, built on quicksand, fused together by low rates. Inflation and interest rate increases will rupture these unstable edifices—only compounded by the fact that so many of these businesses do sham transactions with each other.

The past few decades have experienced a pronounced wealth effect, and this feedback loop has driven much of the consumption boom that we’ve come to think of as a normal state of affairs. As this all goes in reverse, I expect a lot of pain. 2023 will be a bad year for risk assets. It will be a bad year for many financial products. It will simply be a bad year—that is, until the Federal Reserve cannot take the pain. At some point, they’ll choose inflation over an economic collapse. That will be our signal to get long—very, very long inflationary risk assets. To date, we are exposed, but I intend to really press it when the time is right. That time isn’t today, but it is coming soon. I hope to be prepared, yet patient, in terms of when to gross up our exposure.

Returning to our portfolio, having been critical of Ponzi Schemes for much of the past decade, I boldly chose not to invest in Ponzi Schemes during 2022. That decision saved us from a lot of grief. I realize that refusing to invest in fraud is rarely mentioned as a positive attribute of someone’s investing process, but for most of the past decade, such a refusal would have led to dramatic underperformance, as low interest rates and money printing turned much of the globe into a Ponzi economy.

We rented some Ponzis at times during 2022, but we never invested. I remain mesmerized and befuddled by how many prominent and well-respected investors, after struggling with cash flowbased investing during the Ponzi bubble, moved to the dark side and fully-embraced Ponzis. 2022 was the year when they all wished that they’d stayed disciplined. Fortunately, we do not confuse Ponzis with real businesses. While our performance was rather tame during 2022, we also managed to sidestep the carnage in Ponzis. While 2022 was a bad year for fraud investing, I think that 2023 will be lights-out for many of these entities as they are forced to liquidate their Schemes and terminate their employees. The pain has just begun.

On the flip side, I remain unusually bullish on energy and believe that it will be the core market theme over the next few years. We’ve covered the reasons for my bullishness in prior letters. Rather than rehash old material, I’d like to focus on why my thesis has not panned out thus far. To start with, oil is a global commodity that is governed by supply and demand. During the second half of the year, that supply increased as the US and other OECD countries released hundreds of millions of barrels of oil onto the commercial markets. On the demand side, China continued to try to control the spread of germs through arbitrary lockdowns. These two factors now appear to be reversing. On the supply side, not only are strategic petroleum reserves depleted, but Russia along with some OPEC countries appear to be experiencing production declines. Meanwhile, on the demand side, China is now reopening at a time when many other countries are experiencing explosive demand growth caused by their populations entering their respective S-Curves, compounded by an acceleration of gas to liquids switching for electricity generation.

In broad numbers, I believe that while the oil market was slightly oversupplied during the second half of 2022, it will swing to a substantial deficit by the end of 2023. In rough numbers, that swing will be comprised of: 2-3 million of increased Chinese demand, 1 - 1.5 million of SPR release abatements, 1 million of Russian energy production declines, and 1 - 2 million of other global demand increases, all offset by roughly 1 million in further global supply growth, mainly from US shale. Overall, this tallies to a swing of between 4 and 6.5 million bbl/d. Of course, such a swing would be massive by any historic measure and likely lead to an energy crisis like we have not witnessed in many decades. Just to be clear, my expectation is that the deficit will not end up being 4 to 6.5 million bbl/d, but that is only because the price will spin out of control and the demand side will suffer.

Such a scenario likely only accelerates the collapse of non-energy risk assets, particularly as Central Bankers panic to raise rates and quell inflation. In summary, 2023 will be a maelstrom, but I like to think we’re positioned as well as we can be for what’s coming.

Position Review (top 5 position weightings at quarter end from largest to smallest)

Uranium Basket (Entities holding physical uranium along with production companies)

It may take some time still, but I believe that society will eventually settle on nuclear power as a compromise solution for baseload power generation. This will come at a time when there is a deficit of uranium production, compared with growing demand. As aboveground stocks are consumed, uranium prices should appreciate towards the marginal cost of production. Additionally, there is currently an entity named Sprott Physical Uranium Trust (U-U – Canada) that is aggressively issuing shares through an At-The-Market offering, or ATM, in order to purchase uranium (we are long this entity). I believe that these uranium purchases will accelerate the price realization function by sequestering much of the available above-ground stockpile at a time when utilities have run down their inventories and need substantial purchases to re-stock. The combination of these factors ought to lead to a dramatic increase in the price of uranium as it will take multiple years for sufficient incremental supply to come online—even if the re-start decision were made today.

Ironically, I believe uranium will be a prime beneficiary of sanctions on Russia as Russia is one of the world’s largest enrichers of uranium. As the West is forced to enrich more of the uranium that ultimately goes into reactors, underfeeding of tails will flip to an overfeeding of tails. In my opinion, the net effect could be anywhere between 10% and 30% of the global supply of uranium disappearing—which may dramatically accelerate the timing of my thesis while increasing the ultimate magnitude of the upward swing in uranium prices.

Oil Futures, Futures, and ETF Options and Call Spreads

I believe that years of reduced capital expenditures, along with ESG restricting capital access, combined with Western governments that are openly hostile to fossil fuels, have created an environment for dramatically higher oil prices. While we could purchase oil producers, I feel it is far more conservative to simply own the physical commodity itself.

During the fourth quarter, I swapped out our December WTI 2025 futures for the Brent Oil ETF ( BNO ) as I wanted to diversify our oil exposure from WTI and into a global commodity that is less likely to be manipulated by the US government. I also believe that over time, BNO should earn a roll yield, much like it did for most of 2022. Finally, I wanted more exposure to the front of the oil curve, as that is likely to be where the action will be. This position swap was done at a time when the spread between Brent Oil and our futures had compressed by a decent amount, allowing us to avoid paying up substantially for the above-mentioned benefits. We also purchased some shorter-dated futures at around the same time.

I believe that this leveraged play on oil gives us the most upside to oil and ultimately inflation, while exposing us to reduced risk when compared to producers.

Energy Services Basket (Positions Not Currently Disclosed)

In 2020 when oil traded below zero, drilling activity ground to a halt and many energy service providers declared bankruptcy. Many of these businesses had teetered on the verge of bankruptcy for years due to reduced demand and over-leveraged balance sheets. The bankruptcies led to consolidation and reduced future industry capacity, removing future competition in the recovery.

With oil prices now recovering, I believe that demand for drilling and other services will increase from subdued levels. While producers have been slow to increase spending on exploration despite recoveries in energy prices, I believe that this only extends the timing on the thesis. In the end, the only way to reduce future energy prices is to see a dramatic increase in global oilfield services spending. Any postponement of this spending only leads to higher prices and more wealth transfer from the global economy to the oil producers, which will likely end up resulting in an increase in spending on exploration and production.

We purchased many of these positions at fractions of the equipment’s replacement cost, despite restored balance sheets and positive operating cash flow. As spending in the sector recovers, I believe that the potential for cash flow will become more apparent and this equipment will trade up to valuations closer to replacement cost.

St. Joe ( JOE )

JOE owns approximately 175,000 acres in the Florida Panhandle. It has been widely known that JOE traded for a tiny fraction of its liquidation value for years, but without a catalyst, it was always perceived to be “dead money.”

Over the past few years, the population of the Panhandle has hit a critical mass where the Panhandle now has a center of gravity that is attracting people who want to live in one of the prettiest places in the country, with zero state income taxes and few of the problems of large cities.

The oddity of the current disdain for so-called “value investments” is that many of them are growing quite fast. I believe that JOE will grow revenue at 30% to 50% each year for the foreseeable future, with earnings growing at a much faster clip. Meanwhile, I believe the shares trade at a single-digit multiple on Adjusted Funds from Operations (AFFO) looking out to 2024, while substantial asset value is tossed in for free.

Besides the valuation, growth, and high Return on Invested Capital ( ROIC ) of the business, why else do I like JOE? For starters, land tends to appreciate rapidly during periods of high inflation— particularly an inflationary period where interest rates are likely to remain suppressed by the Federal Reserve. More importantly, I believe we are about to witness a massive population migration as people with means choose to flee big cities for somewhere peaceful.

I suspect that every convulsion of urban chaos and/or tax-the-rich scheming will launch JOE shares higher, and it will ultimately be seen as the way to “play” the stream of very wealthy refugees fleeing for somewhere better.

Legacy to Digital Transformation Securities Basket (Various Positions)

Most global print newspapers have seen their readership decline for decades as subscribers seek out alternative digital sources of information. In response to this, newspapers have tried to build up their digital presence. Historically, this digital revenue stream was always rather negligible as it was coming from a small base, especially when compared to steep declines from the print side.

Over the past few years, digital revenue growth has accelerated to the point where I expect that the newspaper companies in our basket are within a few years of their digital revenue overtaking their print revenue—assuming recent trends hold. Digital revenue represents a higher margin and higher return on capital business when compared to the capital and manpower intensity of printing and distributing physical newspapers. My belief is that, as these digital businesses come to dominate the revenue stream, newspaper company valuations will re-rate—particularly as many of them trade as if they are dying businesses, when in reality, the digital side of their businesses is growing quite rapidly.

While many well-known global newspapers have successfully made this digital transition and seen earnings growth for a number of years, many smaller papers have continued to see earnings decline. I believe that these smaller papers are now on the cusp of an inflection to earnings growth as digital growth overtakes print declines. Should this happen, I anticipate it will dramatically change the narratives for these companies, along with their valuations, much like what occurred at more wellknown papers. The fund owns a global basket of these smaller newspaper companies.

Operations Update

2022 was something of a transition year for us from an operational standpoint as we staffed up, moved to permanent offices, and finally completed our transition from a start-up hedge fund into one that is far more institutional and robust in every way.

While we don’t intend to get bureaucratic, growth requires people and systems. In that regard, we have put in place an amazingly high-quality team to manage the back office. This process took time, but I am really excited about where we sit today, as I can now focus far more of my time on the thing that I enjoy doing, which is investing capital. In furthering that goal, we’ve hired a team of four analysts to help me dive deeper into various investment themes and companies, while also offering us much improved coverage of our Event-Driven universe of opportunities. We are in a war for knowledge, and I’m convinced that our team can solve the puzzles faster than our competitors.

In January of 2023, Praetorian PR LLC, a Registered Investment Adviser (RIA), became the investment manager of the fund after we transitioned the investment management of this fund from Praetorian Capital Management LLC to this Puerto Rico entity. We are now managing just shy of $200 million in assets, and my goal remains focused on this fund’s performance, not its size, with a soft close planned for the near future.

In summary, we’ve been growing up fast around here, and 2022 was the year that our management company made the big leaps necessary for the next phase of our investing success.

Summary

Returning to the markets, during 2022, the fund experienced a slight net positive return. While the result was rather anemic, it was well within my range of expectations for the fund’s performance— particularly during a year that was difficult for many risk assets.

The strategies employed by this fund are designed to create high-torque returns during periods when our themes are positively inflecting—however and most importantly, during years when our themes aren’t inflecting (2019 and 2022), I endeavor to avoid down years. If we can continue to produce slightly positive returns during the difficult periods, while compounding aggressively during the easier periods when our trends have tailwinds, I believe that this fund can continue with its return profile since inception—producing very attractive rolling three-year returns, which is our internal goal here.

I remain focused on opportunities to seek out multi-bagger returns while avoiding permanent losses of our capital. While I may not always succeed at this, thus far we’ve done quite well during our first four years in existence.

Our fund is currently a bit more concentrated than normal, with a focus on energy, uranium, and other inflation beneficiaries. I believe that the global economy is currently experiencing a speed-bump on the path to an inflationary crack-up boom. Currently, Central Bankers are trying to control the damage from decades of excessive money printing. Ultimately, they will not be able to take the pain that they are inflicting, and they will pivot—we are anxiously waiting for that pivot. In the interim, there will be sizable volatility going forward, mostly caused by energy prices recovering now that China is reopening. Fortunately, I believe that we are positioned well for what is coming.

Sincerely,

Harris Kupperman

APPENDIX

Praetorian Capital Fund LLC Quarterly Returns |

| Gross Return |

| Net Return* |

| Q1 2022 |

| 19.79% |

| 15.55% |

| Q2 2022 |

| -18.16% |

| -15.69% |

| Q3 2022 |

| 0.01% |

| -0.30% |

| Q4 2022 |

| 18.69% |

| 15.26% |

| YTD 2022 |

| 16.38% |

| 11.95% |

| Q1 2021 |

| 57.50% |

| 45.66% |

| Q2 2021 |

| 28.14% |

| 23.96% |

| Q3 2021 |

| 11.42% |

| 9.85% |

| Q4 2021 |

| 25.32% |

| 22.44% |

| 2021 |

| 181.80% |

| 142.87% |

| Q1 2020 |

| -41.22% |

| -41.22% |

| Q2 2020 |

| 54.32% |

| 54.32% |

| Q3 2020 |

| 34.09% |

| 29.32% |

| Q4 2020 |

| 115.28% |

| 95.63% |

| 2020 |

| 161.87% |

| 129.49% |

| Q1 2019 |

| 6.10% |

| 4.88% |

| Q2 2019 |

| 7.96% |

| 6.44% |

| Q3 2019 |

| -10.23% |

| -8.40% |

| Q4 2019 |

| 15.44% |

| 12.42% |

| 2019 |

| 18.71% |

| 14.97% |

| * Unaudited net return data is estimated, net of all fees and expenses (using the expense structure in place at the time, which was: a maximum of 2% expenses from Inception through December 2020, and a 1.25% Management fee since January 2021). |

| Year |

| Jan |

| Feb |

| Mar |

| Apr |

| May |

| Jun |

| Jul |

| Aug |

| Sep |

| Oct |

| Nov |

| Dec |

| Full Year |

| 2022 |

| 2.76% |

| 3.92% |

| 8.21% |

| -6.36% |

| 2.97% |

| -12.57% |

| 11.97% |

| -2.51% |

| -8.67% |

| 14.96% |

| -1.37% |

| 1.66% |

| 11.95% |

| 2021 |

| 13.76% |

| 18.12% |

| 8.40% |

| 5.82% |

| 10.54% |

| 5.98% |

| -1.58% |

| 3.00% |

| 8.36% |

| 15.19% |

| -0.01% |

| 6.30% |

| 142.87% |

| 2020 |

| -24.62% |

| -7.18% |

| -15.98% |

| 53.65% |

| -4.55% |

| 5.23% |

| 22.71% |

| 10.22% |

| -4.38% |

| 20.03% |

| 32.50% |

| 23.01% |

| 129.49% |

| 2019 |

| -1.31% |

| -1.33% |

| 7.71% |

| 8.82% |

| 0.63% |

| -2.81% |

| -3.18% |

| -8.08% |

| 2.93% |

| -13.10% |

| 4.26% |

| 24.09% |

| 14.97% |

{kind=link}

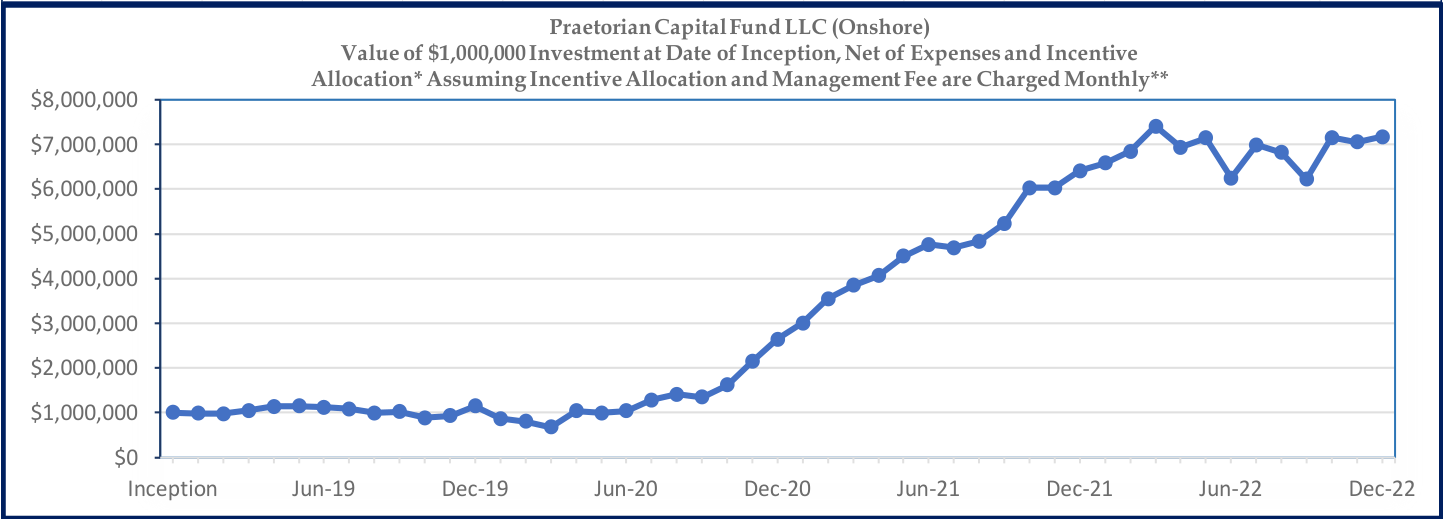

| * Unaudited net return data for Praetorian Capital Fund LLC ("PCF LLC") is estimated, net of all fees and expenses and 20% incentive allocation (using the expense structure in place at the time, which was: a maximum of 2% expenses from inception on January 1, 2019 through December 2020, and 1.25% management fee since January 2021). Praetorian Capital Offshore Ltd. ("PCO Ltd."), an affiliated feeder fund to the PCF LLC, has been subject to the 1.25% management fee and 20% incentive fee since its inception date of October 1, 2021. PCO Ltd.’s monthly performance results may have slight discrepancies, as compared to the results of PCF LLC, due to differences in fund-level expenses, and inception-to-date results will differ due to different inception dates. ** No investor has achieved these precise results. Chart is for illustrative purposes and is intended to provide a basis for further discussion. |

DisclaimerThis document is being provided to you on a confidential basis. Accordingly, this document may not be reproduced in whole or part, and may not be delivered to any person without the consent of Praetorian PR LLC (“PPR”). Note that effective January 1, 2023, PPR, a Registered Investment Adviser with the Securities and Exchange Commission, replaced Praetorian Capital Management LLC ((PCM)), a former investment manager to the funds, as an Investment Manager, as was fully disclosed in the amended confidential offering documents. Nothing set forth herein shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents for Praetorian Capital Fund LLC (the “Master Fund”) or Praetorian Capital Offshore Ltd. (collectively, the “Funds” or each a “Fund”), managed by PPR, which include, among others, a confidential offering memorandum, operating agreement and subscription agreement, as applicable. Such formal offering documents contain additional information not set forth herein, including information regarding certain risks of investing in a Fund, which are material to any decision to invest in a Fund. No information in this document is warranted by PPR or its affiliates or subsidiaries as to completeness or accuracy, express or implied, and is subject to change without notice. No party has an obligation to update any of the statements, including forward-looking statements, in this document. This document should be considered current only as of the date of publication without regard to the date on which you may receive or access the information. This document may contain opinions, estimates, and forward-looking statements, including observations about markets, industries, and regulatory trends as of the original date of this document which constitute opinions of PPR. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Actual results could differ materially from those in the forward-looking statements due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors, including those beyond PPR’s control. Statements made herein that are not attributed to a third-party source reflect the views and opinions of PPR. Opinions may be identified, among other things, by the use of words such as “in my opinion”, “I believe”, etc. Opinions, estimates, and forward-looking statements in this document constitute PPR’s judgment. PPR maintains the right to delete or modify information without prior notice. Investors are cautioned not to place undue reliance on such statements. Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Targeted returns reflect subjective determinations by PPR based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance. The past performance of a Fund, PCM, PPR, its principals, members, or employees is not indicative of future returns. The performance reflected herein and the performance for any given investor may differ due to various factors including, without limitation, the timing of subscriptions and withdrawals, applicable management fees and incentive allocations, and the investor’s ability to participate in new issues. There is no guarantee that PPR will be successful in achieving the Funds’ investment objectives. An investment in a Fund contains risks, including the risk of complete loss. The investments discussed herein are not meant to be indicative or reflective of the portfolio of the Master Fund. Rather, such examples are meant to exemplify PPR’s analysis for the Master Fund and the execution of the Master Fund’s investment strategy. While these examples may reflect successful trading, not all trades are successful and profitable. As such, the examples contained herein should not be viewed as representative of all trades made by PPR. All references to “net return” or return “net of fees” within this letter are for a return of an investor in Praetorian Capital Fund LLC (“PCF”) that would be subject to all standard fees and accrued incentive allocation, if any, during the period presented, as provided for in the PCF’s offering documents at the time, and has been an investor in the PCF since the beginning of the period or year presented. Certain information contained herein has been obtained from third-party sources. Although PPR believes the information from such sources to be reliable, it makes no representation as to its accuracy or completeness. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Praetorian Capital Fund Q4 2022 Investor Letter