ESVIF - Precision Drilling: Bullish On Canadian Oilfield Services Stocks Going Into 2024

2023-11-19 23:43:37 ET

Summary

- Echoing the events from this past spring, land drillers have sold off again and have possibly created another buying opportunity.

- The Canadian players Precision Drilling and Ensign Energy appear particularly undervalued, given that oilfield activity in Canada stands at multi-year highs.

- Precision Drilling can be bought at 3x next year's EBITDA or 5x next year's earnings; Wall Street expects 60% upside.

- I rate Precision Drilling a "buy"; I am bullish on premium drilling and completion services providers, particularly those with Canadian exposure.

Note: Precision Drilling is a Canadian company; the article distinguishes between Canadian dollars (C$) and US dollars (US$).

Investment thesis

Precision Drilling ( PDS ) is one of the 5 big providers of land drilling services to the oil and gas industry in the US and Canada; the other 4 are:

- Nabors Industries ( NBR );

- Helmerich & Payne ( HP );

- Patterson-UTI Energy ( PTEN );

- Ensign Energy Services ( ESI:CA ).

NBR, HP, and PTEN are US companies whereas Precision and Ensign are Canadian-based although both Canadian peers also run US rigs. Generally, these drillers segment their operations among the US, Canada, and "international", the latter capturing anything outside North America.

Canadian Precision ( PD:CA ) and Ensign ( OTCPK:ESVIF ) both maintain dual US-Canada listings; however, while PDS is an NYSE listing, ESVIF is over-the-counter and carries some liquidity risk.

Similar to its peers, Precision Drilling's stock has taken a hit over the last couple months and is now re-testing the lows from this past spring:

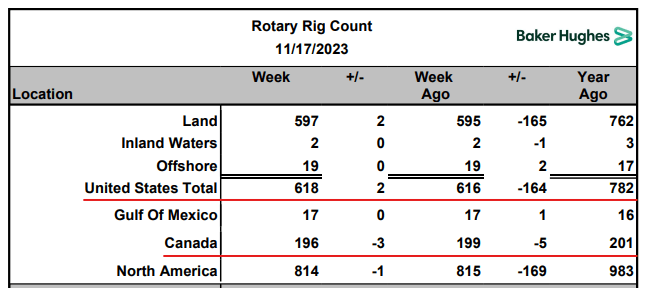

This has been due to the disappointing (from a services provider's perspective) US rig counts that have been sliding down for most of the year.

However, the focus on the headline US rig count report from Baker Hughes ( BKR ) every Friday misses a few important nuances:

- Canadian rig counts aren't falling; in fact, Canada is preparing for a record surge in oilfield services activity in 2024 Q1; Precision and Ensign stand to benefit the most from this;

- Outside of North America, rig counts are also flat or increasing;

- Even within the US, the evolving technical needs of US oil & gas operators ( XOP ) drive a preference for "super-spec" rigs which hands the advantage to PDS and its large peers at the expense of smaller or private drilling services providers.

The blanket selloff in the market has therefore opened up a decent buying opportunity and Precision Drilling can now be purchased for 3.2x enterprise value (or EV) to forecast 2024 EBITDA or 5.0x price to earnings.

Wall Street heavyweight James West of Evercore issued recently a C$142 target - compare it to Friday's C$82 close.

Lay of the land for drilling services

I talked about this in my recent Nabors article, but the industry dynamics aren't as simple as "falling rig count bad." First, we get much coverage that focuses only on the headline US number:

{kind=link}

Looks quite scary, right? Yet, if you bother to check out Baker Hughes' full rig count report , you may note that, while US rigs are down 20% year-on-year, Canada is essentially flat:

{kind=link}

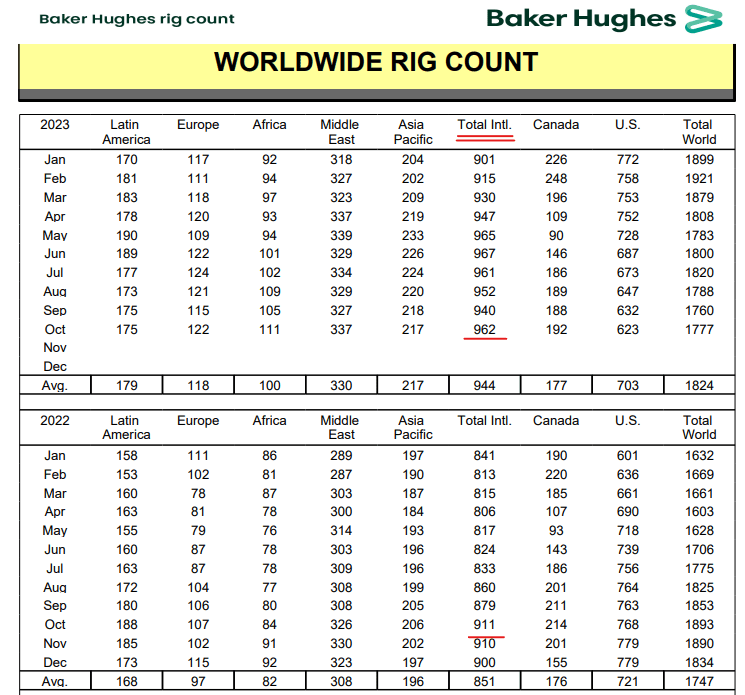

International rigs are actually up YoY:

{kind=link}

The "two-speed" view of the world (softness in the US, firing on all cylinders in Canada and internationally) was shared at the earnings calls of oilfield services bellwethers SLB ( SLB ), Halliburton ( HAL ) and Baker Hughes ( BKR ).

The reasons behind these trends are also interesting in themselves and have to do with the resurgence of the so-called "long-cycle" capex; I talk more about this in my macro-focused articles:

Oilfield Services Update: Offshore And International Make Up For North America Weakness

3 Things To Consider Before Buying Oil Stocks

As it comes to Precision and its drilling peers though, the relevance is that these companies derive much of their revenue from Canada and internationally. A slowdown in the US is worse for Independence Contract Drilling ( ICD ), as an example of a pure domestic US-focused driller.

Even within the US oilfield services market, Precision and the rest of the "Big 5" are advantaged because the large E&P operators (who have the most steady capex budgets) are drilling longer horizontal wells that require higher-performance rigs.

Nabors talked about this trend during their earnings call :

You've actually seen some of the big guys talk about that increasing lateral length as much as five miles and that kind of stuff benefits Nabors, because we've pre-invested in that move.

We built the M 1000 rig, which was the successors to the X-ray a couple years ago, has a million-pound hook load that's perfectly designed for these longer lateral lengths. We also introduced to the market a new top drive that has the pious torque available that can actually handle a five-mile lateral. So, the company's positioned itself to capture that moment.

Precision Drilling has made similar comments. Here is an exchange from Precision's earnings call between management and ATB Capital's Waqar Syed:

Waqar Syed

[It] was mentioned in one case that they would be looking at these for mile type laterals and some other companies have talked about those as well...

What type of rig would be required to drill that? I imagine not every Super Triple rig can do that...

Kevin Neveu

[We've] drilled some 3-mile laterals. We've actually drilled a couple of mile laterals they've been in shallower plays, not the deeper plays. But any time you extend the length of the well or the vertical depth of the well, either one, you're increasing the required hope load capacity for the rigs...

And then because you're drilling farther and you're adding more pipe in the ground, you hydraulic horsepower. So we're typically going from two pumps to three pumps or going from 1,600 to 2,000 horsepower mud pumps. So most of these rigs that -- in our fleet, all of these changes for us are kind of bolt-ons...

Precision Drilling and the likes have the requisite equipment to meet the increasing requirements of their E&P customers - or can get there with limited capex. Smaller players don't and may lose market share to the big guys.

Also from Precision's earnings call comments:

During the third quarter, we continued to experience strong customer interest in our Alpha Super Triple rigs. Since the beginning of the year, we've added 5 public E&Ps to our customer list, and increased our share with two others as we transition to more oil-based work and less private company exposure.

Now Super Spec rig supply remains in tight availability. During the third quarter, we secured a paid upgrade commitment from a customer to cover the cost of increasing the horizontal depth capability of Precision Super Triple. And during the year, we've executed 12 other similar upgrades.

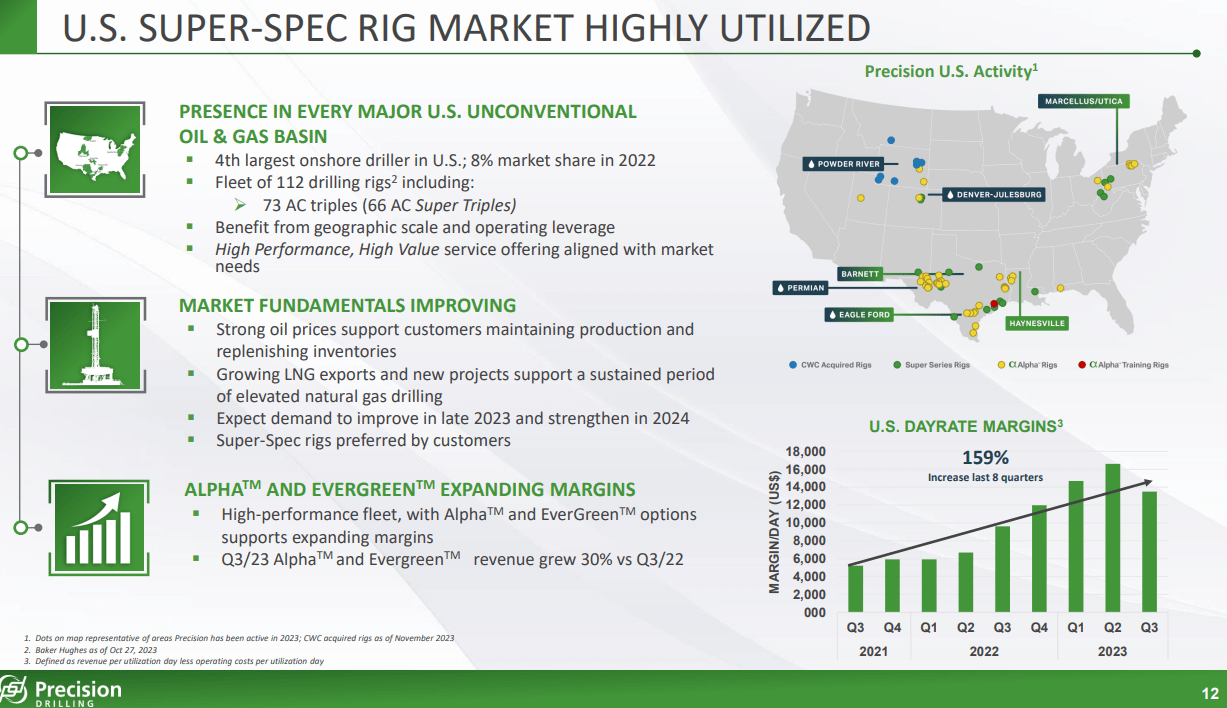

The utilization of these so-called "super spec" rigs doesn't mirror the overall rig count that Oilprice.com likes to talk about. The demand for higher-end equipment remains robust :

{kind=link}

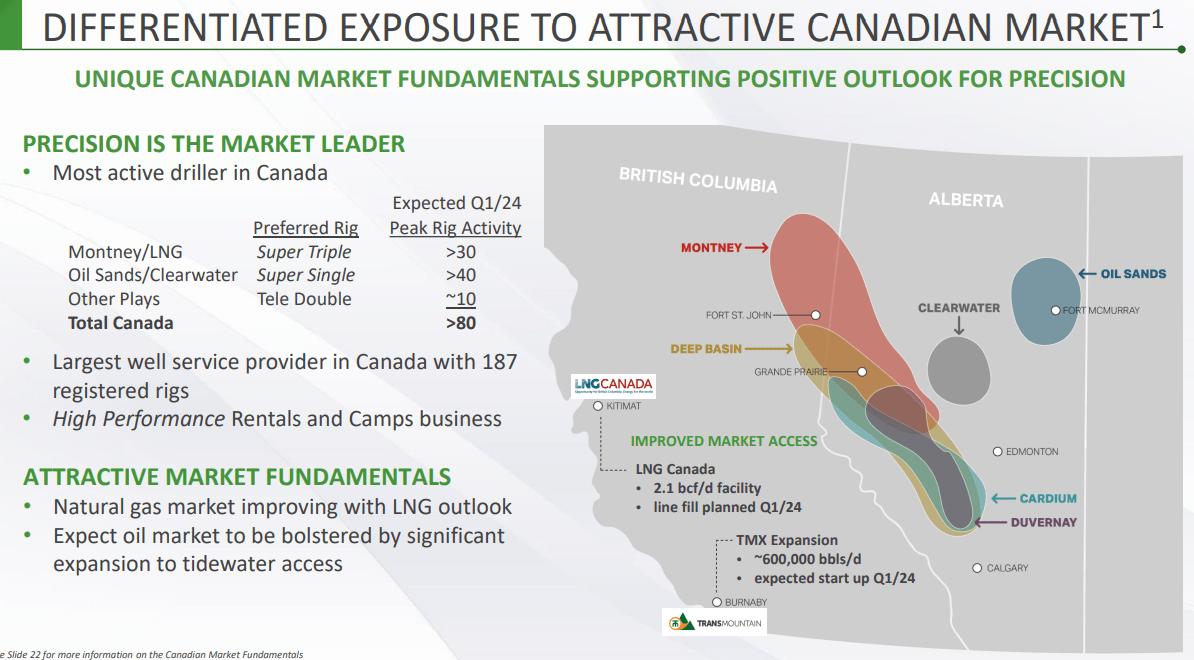

Canadian oilfield services demand is robust

Unlike the US, Canadian oilfield activity is on an upswing. Part of it is that Canada has better quality drilling prospects than what remains in the US, but there is also "pull" from the coming LNG Canada export facility, including the Coastal GasLine gas pipeline, as well as the TMX pipeline expansion that will unlock further Canadian oil export capacity.

Precision's management wasn't shy about calling out these midstream infrastructure projects as "game changers":

Our outlook for Canada remains uniquely strong. Early in 2024, two major hydrocarbon pipe projects will be started up. The Coastal GasLink pipe set to deliver natural gas to the LNG Canada project, and Trans Mountain expansion, adding almost 700,000 barrels per day of oil export capacity.

For Canada, these projects are absolute game changers resulting in significantly improved upstream commodity prices for our customers, debottlenecking production and providing global market access for Canadian energy...

[This] significantly improves the economics of the Montney gas producers who are ultimately focused on the LNG exports over the longer term.

Concurrently, the increased oil export capacity of TMX will serve to reduce the Western Canada Select price discount, significantly improving economics for our heavy oil customers. So for Precision, the result is that the natural gas drilling in the Montney is growing to meet the imminent needs of LNG Canada and heavy oil drilling has rebounded to levels not experienced since 2014. And all of this is evidenced in our record Super Triple demand and our strong Super Single demand.

This slide from Precision illustrates nicely the Canadian dynamics:

{kind=link}

I will also add here some comments from STEP Energy ( STEP:CA ), a Canadian provider of completion services (the completion work comes after the drilling, but the demand drivers are basically the same):

STEP will use the moderating of activity in Q4 2023 to complete more intensive maintenance on equipment to prepare it for the extremely intensive utilization anticipated for Q1 2024 ... Activity in 2024 is expected to increase, with multiple clients signaling that their 2024 capital budgets will be higher than 2023 . The discipline in global oil markets and anticipated completion of the Trans Mountain pipeline project and the Coastal Gas Link pipeline/LNG Canada projects are creating an opportunity for Canada to materially increase production in 2024.

The sentiment in Canada appears very strong and that is already resulting in 2024 Q1 getting sold out for services providers.

PDS benefits from the sector trends

Precision is well positioned because of the large Canada exposure, incremental international exposure, and the possession of coveted super spec rigs. This is filtering down to the bottom line.

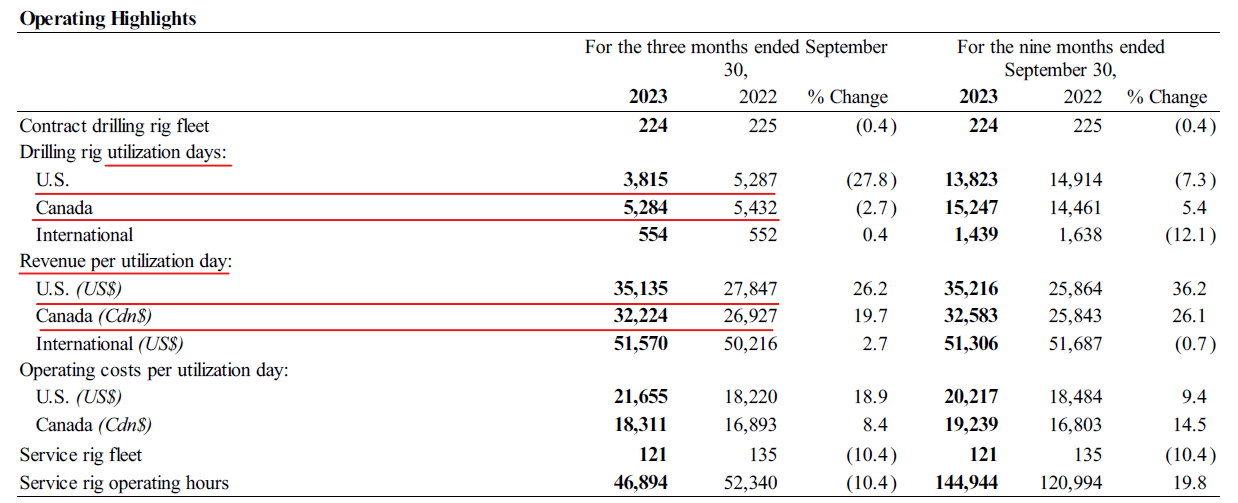

Overall utilization for PDS is down too but dayrates are up; note Canada is basically flat though:

{kind=link}

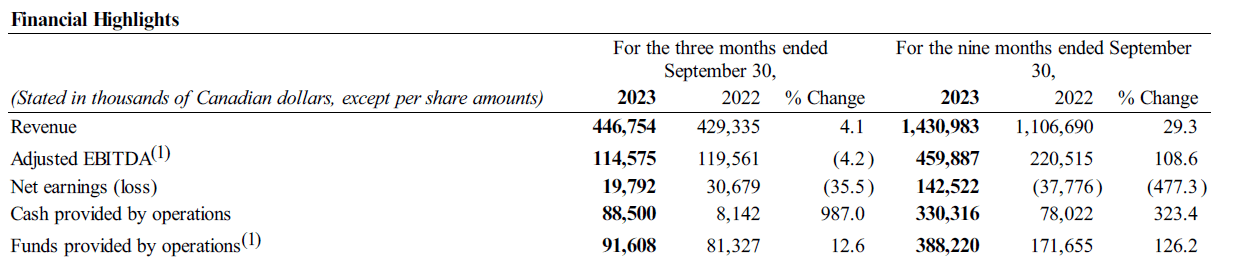

This yielded overall higher revenue although EBITDA was slightly down:

{kind=link}

Note also the steady count for rigs that were under a term contract:

{kind=link}

Most of the headline rig count variation is naturally due to rigs that work on spot contracts; however, premium providers as PDS also do a lot of work under term contracts and these are usually with the larger and more stable E&P operators.

Valuation and risks

PDS can be bought at 3.2x EV/EBITDA; here is a fuller comparison to the rest of the Big 5 plus Halliburton as additional reference point:

| Company |

| EV/ '24 EBITDA |

| P/ '24 E |

| Precision |

| 3.2x |

| 5.0x |

| Helmerich & Payne |

| 4.6x |

| 11.9x |

| Patterson-UTI |

| 3.8x |

| 9.1x |

| Nabors |

| 4.2x |

| 24.6x |

| Ensign |

| 3.2x |

| 5.4x |

| Halliburton |

| 7.1x |

| 10.9x |

Source: Analyst averages by Refinitiv

Precision and its Canadian peer Ensign are the cheapest valued among the group. As Canada leads on activity, it definitely looks like a market mispricing.

The Wall Street analysts covering Precision are bullish; compared to the C$82 current price:

| Analyst |

| Target |

| Date |

| Waqar Syed, ATB Capital |

| C$145 |

| 8-Sep-23 |

| James West, Evercore |

| C$142 |

| 11-Nov-23 |

| Cole Pereira, Stifel |

| C$135 |

| 7-Sep-23 |

Source: Analyst targets by Refinitiv

The Wall Street Average reported by Seeking Alpha sits at C$131:

Seeking Alpha

As risks to mind, please note that Precision Drilling is a very volatile stock. The beta of the US ticker PDS vs. the S&P 500 ( SPY ) is about 3 - this means that if the S&P 500 drops by 1% on a given day, you can expect Precision's stock to fall by 3% on average.

With regard to the usual disclaimer about the volatility of the energy sector, I actually see Precision Drilling's profit line as fairly robust due to the industry trends above. However, any across the board selloff in energy will likely drive PDS down too, at least temporarily.

Bottom line

I rate Precision Drilling a "buy." The multiples are quite discounted, especially given the strong expectations for Canadian oilfield activity. Wall Street's 60% upside sounds about right to me.

Please note that I personally don't own the stock because I already have highly correlated positions in Nabors and Ensign, as well as in the Canadian completions services provider Calfrac ( CFW:CA ).

Generally, I am bullish on all "Big 5" drillers to which PDS belongs, and I think the current selloff we're seeing across these stocks may be a buying opportunity similar to what the market handed us this past spring.

For further details see:

Precision Drilling: Bullish On Canadian Oilfield Services Stocks Going Into 2024