PTA - Preferred CEF Update: Global Bank Crisis Takes A Toll On The Sector

2023-04-03 11:13:37 ET

Summary

- Bank failures in the U.S. and elsewhere have caused air pockets in parts of the preferreds market.

- We take a look at the impact of recent developments on the sector, including the price action in AT1s.

- Despite recent underperformance, preferred CEFs have performed fairly well over the longer term, suggesting that the sector carries a sufficient risk premium for investors.

- We continue to focus on the Cohen & Steers preferred CEFs as well as JPI in the sector.

- We have not added additional capital to preferred CEFs through this drawdown, focusing instead on individual preferreds, however, further price drops will make us reconsider.

This article was first released to Systematic Income subscribers and free trials on Mar. 23.

The ongoing global bank crisis has upended the preferreds market, which allocates primarily to the bank and financial sector securities. From the initial wobble in U.S. regional banks, the sector was hit a second time because of the Credit Suisse Group AG (CS) AT1 fallout - a topic we address in more detail below. Overall, while recent performance across preferred CEFs (closed-end funds) has been tough, its historic returns are comparable to the broader credit CEF space. This suggests that there is sufficient risk premium in the sector to generate solid returns going forward. Within the sector, we continue to focus on the Cohen & Steers funds due to their extremely low level of interest expense as well as the term CEF Nuveen Preferred & Income Term Fund ( JPI ).

Let's Talk About CoCos

CoCos, i.e., contingent convertible securities, i.e., Additional Tier 1 bonds, i.e., AT1s have been in the news recently.

The action in the Credit Suisse AT1 bonds was particularly notable for preferreds funds holders. The bonds were written down to zero, despite equity holders getting $3.25bn. Conceptually, this is odd, as bonds are ahead of stocks in the capital structure. This is all true, however, AT1s can't really be described as bonds. Rather, they're bonds that contractually can go to zero to support equity - that was the entire point of their design, after all. When phrased this way, what happened makes sense. AT1 bonds were written down to zero in order to support the equity capital of the bank. Of course, the way it happened was not great - CS capital never really breached the required triggers - it was all done by regulator fiat.

However, even that is allowed if the regulator views the bank as unviable, whatever that means. AT1 are hybrid (having flavors of debt or equity) securities much like preferreds and are often held by preferred funds. If we look across the true preferreds CEF fund families (i.e., excluding the John Hancock CEFs which are a mix of corporate bonds and preferreds), we get numbers like the following for AT1 holdings as a percentage of total assets: Flaherty (FLC 21%), Cohen (PTA 18%), Nuveen (JPS 34%), First Trust (FPF 29%). The NAV moves on the Monday after the CS AT1 write-down were roughly in line with these figures as Nuveen CEFs underperformed, with FPF not far behind.

Systematic Income

The point here is that while everyone rushed out to check CS holdings across funds, the key information was in the overall AT1 allocation instead. Yes, in some sense, the losses due to CS AT1 holdings were more "real." However, arguably, losses from broader AT1 holdings are as real since the sector has repriced to a higher risk premium levels and the pull-to-par investors normally expect in the wake of losses from bonds are less likely here as AT1s are perpetual instruments. They can be called by the banks, but refinancing them at now higher AT1 yields is not very appealing. In fact, some banks have pulled their AT1 issuance given ongoing concerns in the sector.

What are the consequences here? One is that we will probably not see a quick recovery in this sector, as it's clear that some investors will have to reassess their risk tolerance to AT1s, and AT1s everywhere have already repriced lower.

That said, we probably won't see a total turning away from the sector for two reasons. When Banco Popular saw AT1s written down to zero, lots of people complained, but then happily forgot about it and went back to buying the bonds. Plus, regulators from countries other than Switzerland quickly chimed in that, yes, bonds are ahead of stocks in the capital structure (though naturally they didn't say they wouldn't do the same when push came to shove).

Every time we hear about investors taking their toys and going home, we are reminded of the fact that Argentina has defaulted twice this century and nine times since its independence and has never really struggled to find buyers for its debt after each default. In fact, it managed to issue a 100-year bond in between its two most recent defaults, only three years after its last penultimate one. Investors are an optimistic bunch.

That said, we shouldn't expect the preferred CEFs to quickly retrace their losses, since the AT1 bonds will now carry a higher risk premium. While painful from a mark-to-market perspective, this is actually good from a yield perspective going forward, as preferred CEF distributions can be reinvested at higher yields.

Are Preferred CEFs Uninvestable?

Banks had a rough ride in the past month. Preferred CEFs, which are majority invested in bank preferreds, not through any choice of their own but because banks dominate the preferreds sector, have underperformed since the start of the recent debacle. Preferred CEF NAVs are down around 11% - roughly an order of magnitude worse than the median sector.

Systematic Income

Such a sudden air pocket of performance raises an important question of whether bank preferreds, and by extension preferred CEFs, are actually uninvestable.

Banks are clearly an oddball sector. We want banks to give us our deposits back at a moment's notice while, at the same time, we want them to make risky long-term loans to growing businesses. These two asks are obviously in conflict, which is what causes a lot of the occasional problems in the sector. Apart from this internal conflict, banks are highly leveraged institutions - much more than "normal" businesses.

Moreover, a bank can be quickly brought down by a loss of confidence of the depositors. What's particularly interesting is that a bank that would be correctly described as liquid and solvent can quickly fail if enough of its depositors decide to take the money and run. Another unique aspect of the sector is that a bad bank can cause good banks to fail through a general loss of confidence in the sector. That is the opposite of what happens in other sectors, where a failure by one company normally immediately improves the prospects of other sector companies.

Let's take a look at credit CEF sector returns over various longer-term periods to see how they stack up. What we see is that even with the recent shocker, the preferreds CEF sector compares well within this group. Its 0.9% and 4.4% CAGR total NAV returns over 5Y and 10Y periods are above the median credit sector.

Systematic Income

What this suggests is that this unattractive fundamental backdrop is well-matched by a decent risk premium, which allows longer-term returns for bank preferreds to be pretty good.

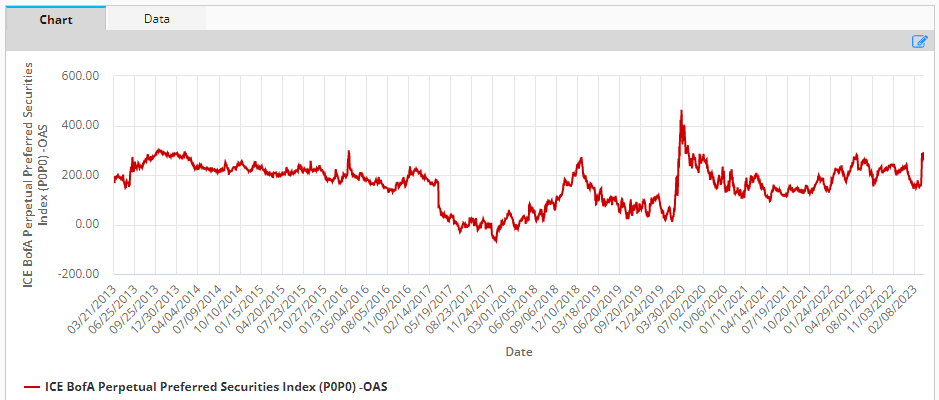

The chart below of perpetual preferreds option-adjusted spread is a good proxy for this premium. So long as it remains reasonably wide such as today, the sector should remain a reasonable destination for income investors.

{kind=link}

Our Sector Stance

We continue to focus on two types of funds in the preferreds CEF sector: The Cohen & Steers CEFs (PSF, LDP, and PTA) as well as the Nuveen Preferred & Income Term Fund.

The Cohen funds have three chief advantages - pretty good performance relative to the sector, resilient leverage profile, and an unusually low level of leverage. For example, PTA cost of leverage on 85% of its borrowings is around 1.2% versus around 5.5-6% for most other credit CEFs (its remaining 15% is in line with other credit CEFs).

At the moment, both LDP and PTA screens as attractive. PTA has a slightly lower cost of leverage but a slightly higher management fee. Overall, LDP will tend to trade at a slightly tighter discount than PTA. An LDP discount within 1% of the PTA discount would make us favor LDP over PTA.

Systematic Income CEF Tool

It's worth highlighting that a fund like PTA did not exactly distinguish itself during the current sell-off, having held CS AT1s as well as SVB (SIVBQ), Signature Bank (SBNY), and First Republic (FRC) securities.

That said, it has slightly outperformed the sector over the past month in total NAV terms, though not by much. A glance at the pre-crisis top issuers holdings (not the same as top holdings, given many instances of multiple holdings for one issuer) has CS at number 15 and SVB and Signature below that. 14 holdings before CS are ones that investors are not particularly concerned about. As a side note, CEFs should start to publish the largest issuer holdings rather than just the top 10 holdings, as the former can be highly unrepresentative of the risk to individual issuers.

Systematic Income

JPI also remains on our radar, primarily because of its term structure. Nuveen has consistently allowed investors an exit at the NAV for their term CEFs whether through termination (e.g., JEMD) or a tender offer at NAV (e.g., JPT).

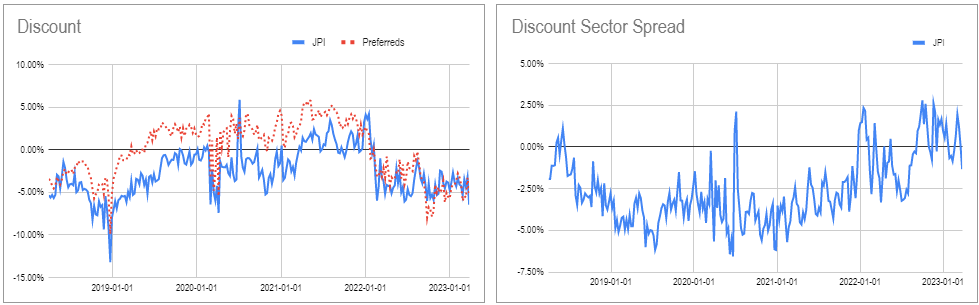

JPI is trading at an unusually wide discount for it of 6.5% as the left-hand chart shows. It's also trading at a slightly wider discount than the sector though this is less unusual.

{kind=link}

The fund's pull-to-NAV yield is at the highest level over the past 5 years of 4.5%. This metric is just the fund's discount (i.e., 6.5%) annualized to its expected termination date in Aug-2024. This is the additional tailwind its price is expected to enjoy over this period. Of course, if we see further volatility in the banking sector we could easily see a negative total price return even with this tailwind, but the additional performance will still help.

Systematic Income CEF Tool

Recent performance across these funds as well as the broader sector has clearly been painful, and we have not rushed to add new capital to these funds, focusing instead on individual preferreds. However, if we see further weakness from here, additional allocation to these funds will be a compelling proposition.

For further details see:

Preferred CEF Update: Global Bank Crisis Takes A Toll On The Sector