SAT - Preferreds Weekly Review: What To Watch Out For As The Fed Approaches Rate Cuts

2023-04-30 23:55:46 ET

Summary

- We take a look at the action in preferreds and baby bonds through the third week of April and highlight some of the key themes we are watching.

- Preferreds had another decent week as credit spreads continued to tighten. Sector yield remains attractive at around 7%.

- We discuss what to watch out for as the Fed nears a reversal of its previous rate hikes.

This article was first released to Systematic Income subscribers and free trials on Apr. 24

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the third week of April.

Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the closed-end fund ("CEF") markets for perspectives across the broader income space.

Market Action

Preferred continued to rally over April despite slightly higher Treasury yields. Banks and Financials outperformed as investors took comfort from strong earnings and fairly subdued deposit outflows.

Preferreds yields remain attractive near 7% despite a retracement of near 0.5% from the recent peak.

Systematic Income Preferreds Tool

Market Themes

Since 2022 interest rates have mostly marched upward, supported by high and persistent inflation and the Fed that turned increasingly hawkish through last year. Now that the market consensus is for the Fed to start to reverse the hikes, an important question is what impact will this coming rate pivot have on the preferreds market.

Chatham

The obvious thing to do is to see what happened in 2020 when interest rates fell. However, that comparison is not a great one. For one, to put it mildly, there was a lot more going on in 2020 than a drop in interest rates. For example, credit spreads blew up (rising by a lot more than the drop in rates) and this introduced a lot of noise into the data. We don't expect a similar type of credit blowup this time around. Two, there were few if any floating-rate preferreds in 2020 (and many of those that were floating-rate had rate floors, making them fixed-rate).

So what we do instead is check what happened since 2022 when both short-term and longer-term rates rose. Many investors talk about "interest rates" however it's important to understand that interest rates across the curve rarely move in lockstep. Although rates across the entire curve rose since 2022 they rose by very different amounts. For example, while short-term Treasury yields rose by around 4.5% over 2022, longer-term rates rose by about half that. Moreover since the start of the bank tantrum, 10Y yields fell by 0.54% while short-term rates were flat or rose slightly.

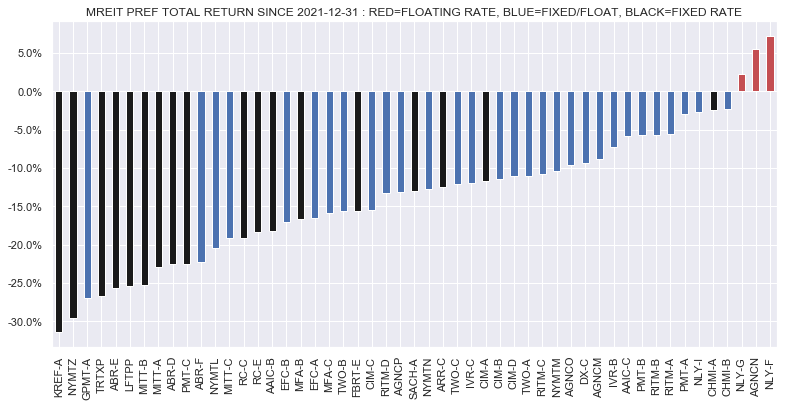

Changes in short-term rates will disproportionately impact preferreds with different coupon types. For example, the chart below of mortgage REIT preferreds shows that since the end of 2021, when interest rates started to climb, preferreds that underperformed tended to be fixed-rate ones (black lines). Fix/Float preferreds (blue lines) did better on average and floating-rate preferreds did the best. This illustrates the, fairly obvious, point that floating-rate preferreds will do well during a period of short-term rate hikes and vice-versa.

{kind=link}

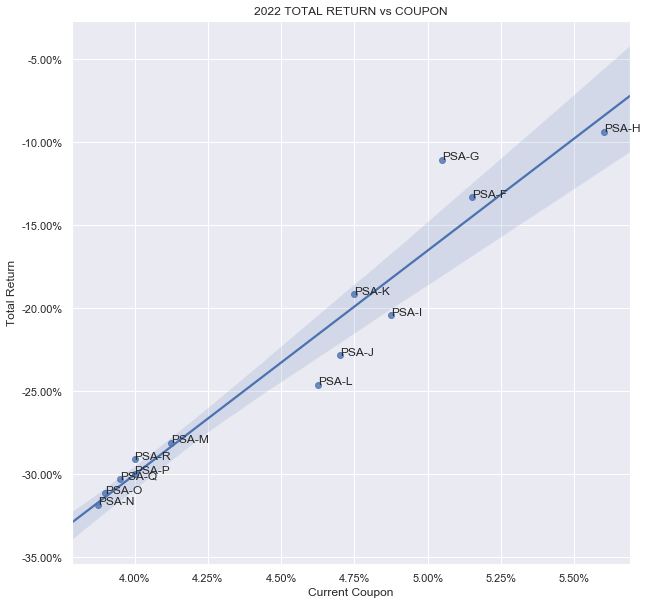

If we turn our attention to longer-term rates we can see that what investors need to pay attention to is the coupon level of the relevant fixed-rate or Fix/Float preferred. Intuitively, the lower the coupon level the more work the price has to do to adjust the yield of the stock to an appropriate level. The chart below shows how 2022 played out across fixed-rate Public Storage preferreds. We can see that lower-coupon stocks fell more than higher-coupon ones. The key takeaway here is that lower-coupon stocks tend to have a longer duration.

{kind=link}

One key takeaway here is that floating-rate stocks (and by extension Fix/Float stocks with shorter first call periods) are more vulnerable to the drop in short-term rates. And two, higher-coupon stocks will benefit less from the drop in longer-term rates.

There are some clear risks here but there are also mitigants as well, particularly for floating-rate preferreds which we continue to hold. One, there is still a significant coupon cushion which will keep the yield attractive on many of these stocks even after a number of Fed cuts. Two, as the first chart above shows, the Fed doesn't expect to cut as soon as the market so we are likely to live through a big chunk of this year without cuts. Three, few people expect the Fed to take rates back to zero so the underperformance by floating-rate stocks should be more muted than the gain since 2022. All in all, investors should review their preferred holdings to make sure they are not surprised by price moves once the Fed starts to take rates lower.

Stance and Takeaways

In this article we discussed how different preferreds react to changes in short-term and long-term rates. However, one challenge with allocating based on a view on the direction of rates is that if you're wrong, your portfolio returns will likely suffer as well.

This is why it's useful to remember that investors don't have to take views on the direction of rates and can happily allocate to securities that will be largely immune to whether rates move up or down.

There are few preferreds outside of a handful of CEF term preferreds that will be broadly unaffected by changes in rates. However, there are quite a few baby bonds that can fit the bill. These include bonds like the mortgage REIT Arlington Asset Investment Corp 6.75% 2025 bonds ( AIC ) with a yield well north of 9% and BDC baby bonds from Saratoga ( SAY ) and Oxford Square ( OXSQL ) trading at yields north of 8%. These bonds allow investors to earn attractive yields without trying to be a hero on the direction of rates. We continue to hold these bonds in our Income Portfolios as high-yield ballast that can perform regardless of what happens to rates.

For further details see:

Preferreds Weekly Review: What To Watch Out For As The Fed Approaches Rate Cuts