PINC - Premier: SaaS Healthcare Products And M&A Imply Undervaluation

2024-01-17 16:53:21 ET

Summary

- Premier Inc. offers healthcare solutions through a collaborative business model and SaaS-based software, with potential for significant financial improvement.

- The company is experiencing growth through inorganic means and is expected to see double-digit net sales growth.

- Premier Inc. has a significant amount of goodwill but a small amount of financial debt, indicating potential for further acquisitions and business growth.

Premier, Inc. ( PINC ) brings a collaborative business model with SaaS-based clinical and financial software as well as an aggressive M&A strategy. I also believe that the recent strategic initiatives, restructuring efforts, and recent acquisitions could bring significant financial performance improvement in the coming years. There are several risks out there from goodwill impairments or lower than expected growth for SaaS-based products, however, I think that PINC trades cheaply.

Premier

Premier offers healthcare by uniting hospitals and health systems in the U.S. The company partners with diverse healthcare players in order to innovate in clinical, financial, and operational areas, adapting to the evolution of the industry. Through comprehensive services, such as supply chain as well as SaaS-based clinical and financial software, Premier empowers providers to deliver quality care at a lower cost.

Premier Inc. offers two types of solutions, supply chain services, and performance services. In the supply chain, it addresses areas such as group purchasing, co-management, and direct sourcing. In performance, its sub-brands offer advanced services in clinical intelligence, margin improvement, and value-based care. The model was designed to optimize costs, mitigate risks, and facilitate effective transformation in healthcare. As shown in the image below, in the recent quarter, the company noted a significant amount of net revenue from software licenses and SaaS-based products among other services. The performance services business segment, which includes SaaS-based products subscriptions, appears to be growing faster than supply chain services.

Source: 10-Q

The growth expected for the healthcare software as a service market in the coming years is close to 18%. Besides, Premier Inc. is growing significantly through inorganic growth. Hence, I would not be surprised if we see double-digit net sales growth in the coming years. The following lines were obtained from the Healthcare Software As A Service Market Report.

The healthcare software as a service market size is expected to see rapid growth in the next few years. It will grow to $48.78 billion in 2028 at a compound annual growth rate of 18.8%. Source: Healthcare Software As A Service Market

Recent Earnings Release, Market Reaction, And Market Expectations

In the last quarterly report, Premier Inc. reported lower than expected quarterly net sales, but better than expected EPS GAAP. EPS GAAP stood at close to $0.37 per share, with quarterly revenue close to $318 million. EPS revisions in the last 90 days included six different analysts lowering their EPS expectations. Premier Inc. is currently trading at price marks not seen even in 2014.

Source: SA Source: SA

If we also have a look at the quarterly adjusted EBITDA and quarterly net sales as compared to the figures reported in Q1 2023, Premier Inc. does look improving. Quarterly net sales increased by close to 2%, and quarterly net sales were 5% larger than that in Q1 2023. More in particular, I believe that the most relevant was the revenue growth reported by the performance services segment, which stood at close to 15%. The following is a slide from a recent presentation.

Source: IR Presentation

I believe that market expectations for 2024, 2025, and 2026 are also beneficial. Analysts are expecting net sales growth, net income growth, and FCF growth. 2026 Net income stands at close to $195 million, with 2026 EPS of about $1.59, 2026 free cash flow of $375 million, and FCF margin close to 26%. We would be talking about 2026 EBITDA of $422 million and 2026 EBITDA margin of 29%.

Source: S&P Source: S&P

Significant Amount Of Goodwill, But A Small Amount Of Financial Debt

The most remarkable thing about Premier Inc. is the total amount of goodwill, which increased significantly in the last seven years. It means that Premier appears to know well how to acquire other targets. With this in mind, I believe that we could expect significant business growth due to inorganic growth in the coming years.

Source: Ycharts

The acquisitions are financed using notes payables besides liabilities related to the sale of future revenues and revenue share obligations. Financial debt/EBITDA stands at less than 1.2x, and the total amount of financial leverage does not seem significant. I believe that management could execute new acquisitions in the future.

Source: Ycharts

More in particular, in the last quarter, the company noted cash worth $453 million, accounts receivable of about $102 million, and contract assets worth $311 million. Besides, with inventory of $69 million, total current assets stand at close to $1002 million. I do not see liquidity risks because the current ratio appears to be over 1x.

Other assets include property and equipment worth $210 million, intangible assets of $417 million, and goodwill close to $1012 million. Finally, with deferred income tax assets close to $797 million, total assets stand at $3.849 billion. The asset/liability ratio is larger than 2x, so I would say that the balance sheet appears quite stable.

Source: 10-Q

The most significant liabilities include accounts payable of about $48 million, with accrued expenses close to $46 million, revenue share obligations worth $265 million, and current portion of notes payable to former limited partners worth $100 million. With liability related to the sale of future revenues of close to $541 million and notes payable to former limited partners close to $76 million, total liabilities stand at close to $1.496 billion.

Source: 10-Q

I did have a look at the credit agreements signed by Premier and its subsidiaries in order to review the cost of capital. The company entered into an amended and restated senior credit facility on December 12, 2022. This unsecured credit facility, maturing in 2027 and with a capacity of up to $1.0 billion, replaced a prior agreement. It offers flexibility, allowing loans at the SOFR rate or base rate. According to the last quarterly report , the weighted average interest rate is not far from 6.47%. Given these figures, I assumed a WACC of 9% in my best case scenario and 12% in the worst case scenario.

Competition

Markets for supply chain services and performance services are highly competitive and fragmented, with rapid technological advances. The company competes with large GPOs like HealthTrust and providers like Cardinal Health. In performance services, it faces competition from information technology and consulting, such as Deloitte and Health Catalyst. Competition focuses on factors such as price, quality, clinical performance, and ability to integrate with existing technologies.

Assumptions Under My Best Case Scenario Include Successful Integration Of Recently Acquired Assets

Under the best conditions that I can imagine, Premier would successfully integrate the assets of Direct Pay and Devon Health to strengthen its Performance Services segment. Additionally, I assumed that we could see further acquisitions in cash, which I believe is quite appealing. Previous acquisitions were made in cash and funded by credit facilities. I believe that Premier Inc. does not intend to use equity, which, in my view, indicates that the current valuation is not at all expensive. The following lines were obtained from a recent quarterly report.

The purchase price paid by the Company to complete the TRPN acquisition consisted of cash of $177.5 million, funded with borrowings under the Company's Credit Facility (as defined in Note 8 - Debt and Notes Payable) and cash on hand, of which $17.8 million was placed in escrow to satisfy indemnification obligations of TRPN to Contigo Health and its affiliates and other parties related thereto under the purchase agreement governing the TRPN acquisition. Source: 10-Q

Given the recent increase in strategic initiatives and financial restructuring-related expenses, I also assumed that the company could successfully continue to innovate in improving access to healthcare and reducing costs.

Source: 10-Q

In addition, the sale of non-health-related group purchasing contracts to OMNIA Partners has been closed, generating significant resources in hand. We are talking about $750.0 million and $800.0 million, which will most likely improve Premier's financial health. In my view, as more investors have a look at this agreement, the company may receive more demand for the stock.

On July 25, 2023, we sold substantially all of our non-healthcare GPO member contracts pursuant to an equity purchase agreement with OMNIA Partners, LLC for a purchase price estimated between $750.0 million and $800.0 million, subject to certain adjustments. For a period of at least 10 years following the closing, the non-healthcare GPO members will continue to be able to make purchases through our group purchasing contracts. Source: 10-Q

Cash Flow Expectations Under My Best Case Scenario

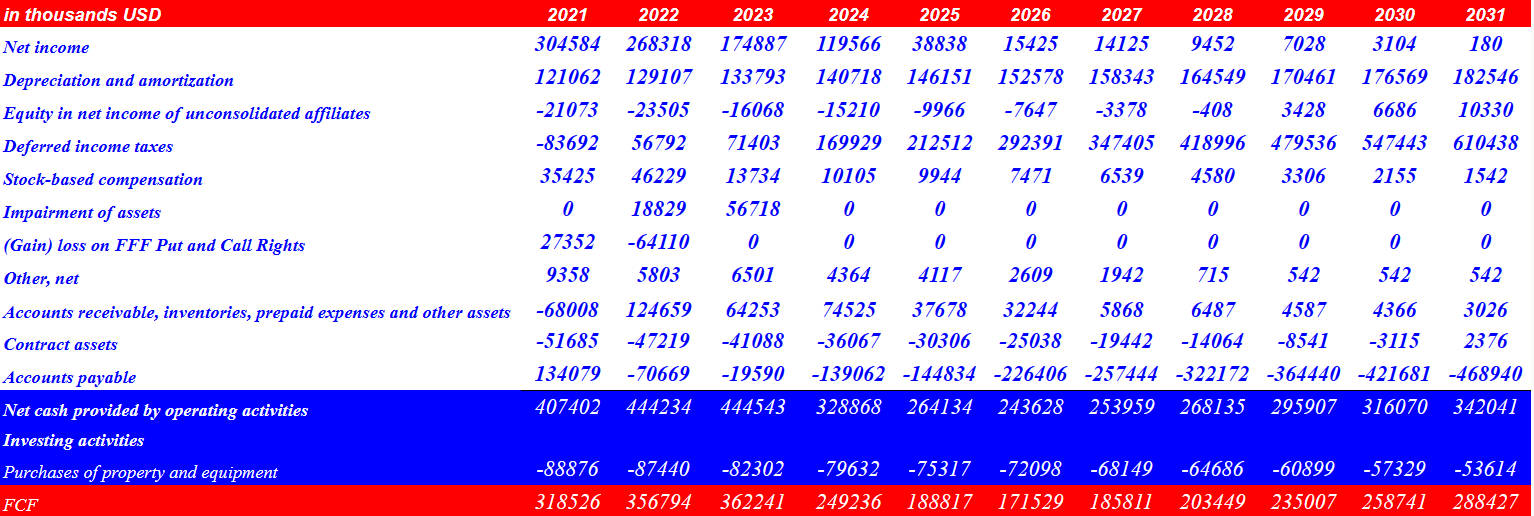

My best case scenario includes 2031 net income close to $70 million, 2031 depreciation and amortization worth $182 million, and stock-based compensation close to $1 million. I did not take into account impairment of assets or gains on put and call rights, because I believe that they do not represent recurrent items of the business model.

Besides, with changes in accounts receivable, inventories, prepaid expenses, and other assets close to $429 million, changes in contract assets of -$85 million, and changes in accounts payable of about -$43 million, I obtained CFO of $627 million. Finally, with purchases of property and equipment close to -$54 million, 2031 FCF would be close to $574 million.

{kind=link}

Peers in the same sector report a median EV/EBITDA of about 13x-14x and price/cash flow of 16x. Given these figures and the current trading multiples of Premier Inc., I believe that the company could report, under the best case scenario, an exit EV/FCF of 9x FCF. In my view, my figures are very conservative.

Source: SA Source: SA

Using a WACC of 9%, the NPV of future FCF projections would be worth $2.18 billion. Besides, with an exit EV/FCF of 9x, the implied enterprise value would be $4.7 billion. Finally, adding cash and subtracting debt, I obtained an intrinsic valuation of $42.23 per share and an IRR close to 12%.

Source: My DCF Model

Risks And Cash Flow Expectations Under My Worst Case Scenario

Premier's viability may be affected by the willingness of customers to adopt and expand the use of its SaaS or licensed products and services. Fluctuation in demand and licensing models could also lead to revenue volatility. Resistance to change from companies with investments in established software and security concerns could limit adoption in the coming future.

Reliance on private and government third-party payers for reimbursement, along with potential limitations on government spending, could adversely affect finances and demand for products and services, creating significant risks to the business. Under this case scenario, I assumed that some of these risks could lower future net sales growth expectations.

I also believe that Premier Inc. could suffer from goodwill impairments, which may only lower future net sales expectations, but also lower the book value per share and synergies expected. Given the total amount of goodwill, under this case scenario, I assumed that this risk would be significant.

Under this scenario, I included 2031 net income of close to $0.1 million, 2031 depreciation and amortization of close to $182 million, and stock-based compensation worth $1 million. Additionally, with accounts receivable, inventories, prepaid expenses, and other assets close to $3 million and changes in contract assets of $2 million, CFO would be close to $342 million. Finally, assuming 2031 purchases of property and equipment of about -$54 million, 2031 FCF would stand at close to $289 million.

{kind=link}

If we assume a WACC of 12%, the NPV of future free cash flow from 2024 to 2031 would stand at close to $1.07 billion. Additionally, with an exit multiple close to 7x, the total enterprise value would be close to $1.89 billion. If we add cash and subtract notes payables and lines of credit, the implied equity valuation would be $2.1 billion. The implied internal rate of return would be -2.8%.

Source: My DCF Model

My Conclusion

Premier's integrated and collaborative business model, focused on supply chain and performance services, has strengthened key partnerships, and will most likely enhance future FCF margin growth. Besides, I believe that the post-acquisition and contract sale strategy offers financial flexibility. Additionally, given recent efforts with regard to strategic initiatives and restructuring, we could expect further increase in profitability in the coming years. I did find risks from goodwill impairments and lower demand for SaaS or licensed products and services. With that, I think that Premier does trade a bit undervalued.

For further details see:

Premier: SaaS Healthcare Products And M&A Imply Undervaluation