NORW - Prepare For Fed Easing And A Market Rally By Year-End

Summary

- The Federal Reserve is suffering massive operating losses.

- When politicians wake up, Fed losses will draw their fire.

- Faced with recession, the Fed will likely slash short term interest rates by year end.

- This could spark a short term rally, but stocks may struggle afterward.

- I own NORW, C, CMA, lithium stocks, emerging market stocks, and I am short HYG.

Every year I construct a “Most Likely” forecast for the stock market. This forecast is based on all the variables I can possibly envision, with each assigned a (highly subjective) probability weighting. My forecast is necessarily clouded in uncertainty, but at least it gives me a starting point for my portfolio. I modify this forecast throughout the year as new facts roll in to confirm or refute my “predicates.”

As a fan of Nassim Taleb, I take special care to identify as many potential “tail risks” as I possibly can. They are called “tail risks” because are highly unlikely but have the potential to sneak up and bite us on the tail. My main objective is not to predict the future but to identify events that might occur, try in advance to tease out their stock market repercussions and anticipate how a prudent investor might respond.

While my forecasts are not predictions per se, in recent years they have panned out pretty well: Here is my initial 2021 forecast and my 2022 forecast.

As in all past years, the 2023 outlook includes innumerable moving parts, both economic and political.

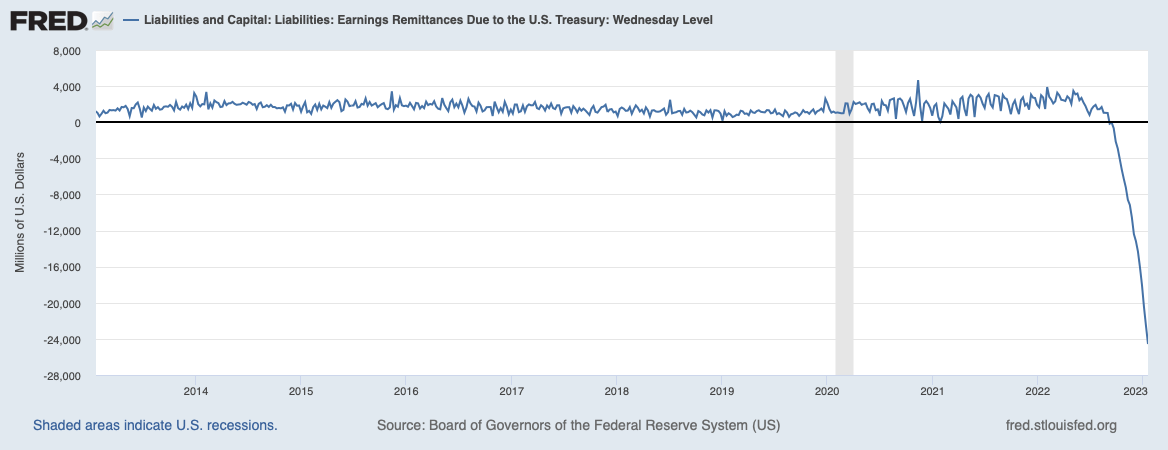

But the more I thought about it, the more convinced I became that stock market performance in 2023 will boil down to one critical issue that can be distilled into this one gob-smacking graph.

Federal Reserve Remittances to Treasury (St. Louis Federal Reserve)

{kind=link}

Followers of SA authors Wolf Rich ter and Alan Longbon and Paul Kupiec at the American Enterprise Institute will be familiar with this chart. I commend their work for background, corroboration, and insight

Question: What is going on here?

Answer: every week the Federal Reserve is paying banks billions of dollars in interest on bank reserve assets and also for Reverse RP. In doing so, it is creating tens of billions of dollars of obligations. At current rates, the Fed could end up owing as much as $100 billion in 2023. Technically, I suppose, the Fed is not losing money because it is simply creating the money it is paying out, which, in turn, adds to bank reserves. But it is an obligation that must ultimately be paid by us taxpayers – one way or another. For the sake of simplicity, let’s call it an “operating loss.”

For my part, I am not convinced that the Fed’s burgeoning obligation necessarily represents an existential threat to the Fed or to the economy. Yes, it reflects misguided monetary policy. Yes, it is injecting reserves into the banking system even as QT is draining reserves. Yes, it is deeply unfair since in essence it represents a subsidy to bank shareholders. But I’m not sure that the Fed's obligations do anything worse than add incrementally to our national debt. That’s plenty bad enough.

Unless I am missing something, there can be no need for a Fed “Bail Out” because the Fed can always create as much cash as it wants. For its part, the Fed projects its operating losses to abate in 2024 and for the cumulative loss to disappear by 2026 as QT reduces bank reserves and, presumably, interest payments on reserves decline.

The real danger is how our policymakers in Washington might react to the Fed’s losses, and what the Fed might do in response.

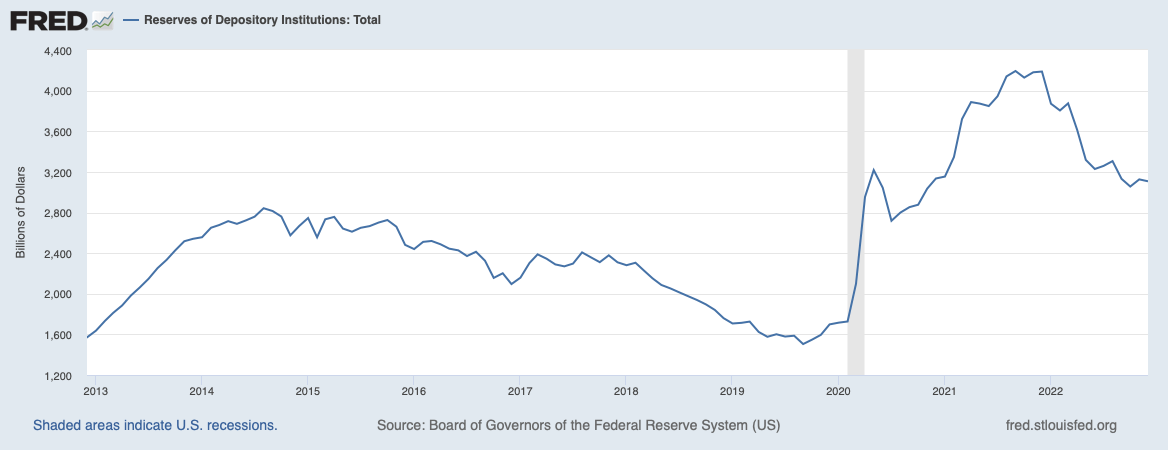

The Fed’s current dilemma stems from a 2020 change in monetary strategy at the Federal Reserve. Prior to 2020, the Fed’s primary monetary tool was “open market operations.” The Fed would buy and sell securities to increase or decrease bank reserves. This enabled them to stabilize the targeted Fed Funds rate.

Commercial Bank Reserves at Fed (St. Louis Federal Reserve)

{kind=link}

But by the summer of 2020, the “Quantitative Easing” fire hose had forced such a surfeit of reserves into the banking system that open market operations became ineffective. In response, the Fed changed its monetary policy focus from open market operations to the management of the interest rate it pays banks for reserves.

Shortly thereafter, the Fed instituted a “Reverse Repo” program to support interest rates for Money Market Funds (MMF’s) and other non-bank financial institutions. The initial impetus for this decision, I think, was to keep short term interest rates from going negative.

“Open Market Operations” had at least two advantages over current methods. First, and most important, fed funds interest payments went from bank to bank, not from the Federal Reserve to banks.

Second, Fed Funds was at least a quasi-market interest rate, driven by the economy’s underlying demand for and supply of credit. The policy mechanism was not the setting of interest rates per se, but the setting the quantity of bank reserves. Banks with insufficient reserves at the end of the reporting period could borrow reserves from those with excess reserves. If banks needed to bid above the target Fed Funds rate for reserves, the Fed could buy securities, thereby introducing more reserves into the system and tamping down the Fed Funds rate. In contrast, today’s interest rate targets are purely arbitrary shots in the dark.

As the Fed raised its policy rate in 2022 to tighten monetary conditions, the payments it made to banks grew commensurately. Since revenues (mainly Treasury and MBS interest payments) did not increase as interest payments rose, the Fed started losing money. And that’s how we got the graph pictured above

Fed Losses Will Draw Congressional Fire

My overriding assumption for 2023 is that our congressmen and women will soon wake up to the Fed’s operating losses and will take action to quash them. They will not be happy to realize that Jay Powell is enriching the likes of Jamie Dimon and Larry Fink (and, indeed, all bank shareholders) at the expense of the average working stiff.

Many legislators on both sides of the political divide already are implacable Fed foes, notably Elizabeth Warren and Rand Paul. They will relish an opportunity to attack and, if possible, shackle the Fed. Rhetoric will be heated, and the Fed’s independence could be tested. This would not be good for investors.

Anti-Fed sentiment is likely to be amplified by the national debt ceiling battle. While I am confident that the US will not default on its debt, this could be an extended and rancorous fight. Even though the Federal Government is evidently not legally obligated to backstop the Fed, its burgeoning losses are likely to draw legislator’s attention.

How our policymakers might attempt to address the Fed’s losses is anyone’s guess. It is always possible that legislators could respond with a rational, productive solution, but I wouldn’t bet on it.

Given the uncertainty surrounding future government actions, I believe it is prudent for investors to prepare for a “worst case” -- or at least an extreme -- scenario and try to anticipate where the chips might fall.

Following is my attempt at a “worst feasible case” for how these Fed issues might play out. This is mainly a thought experiment, but I think that if one prepares for an extreme scenario such as this, one will be better positioned to respond to a less severe outcome.

My “Forecast”: The Fed Pivots, Short Rates Slashed

I suspect that by midyear the Fed could be seeking pretext for abandoning its high-rate policy. For one thing, it may feel browbeaten by politicos and threatened with legislation.

More importantly, by midyear the country may well be staring recession in the face. My concern about recession centers principally on three economic trends. First, the index of leading indicators has declined for two months in a row and is down sharply from its peak in June.

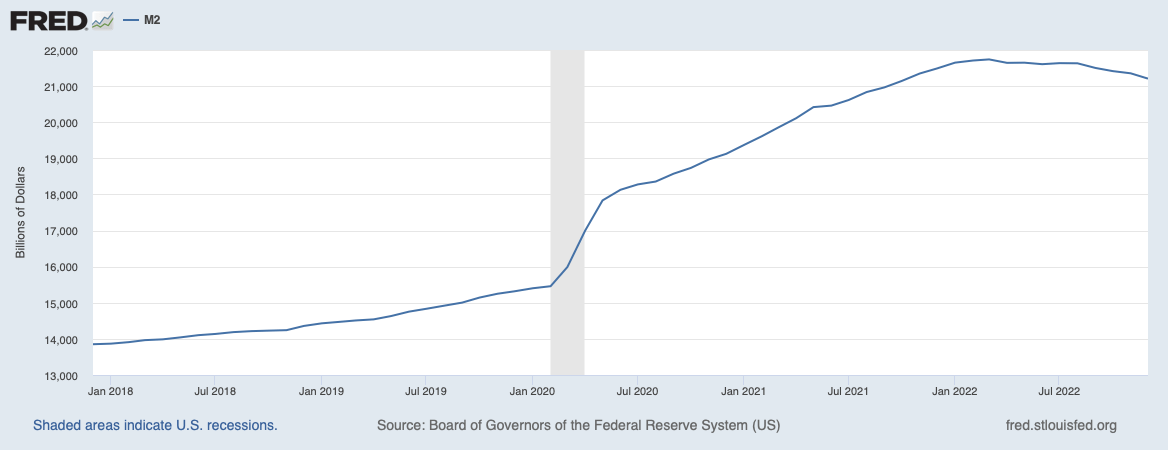

Second, M2 has declined for three consecutive months and has declined more than 2% from its March high. Consecutive monthly declines in M2 are extremely rare. Even under Paul Volcker’s famously frugal monetary policy I could not find a single instance of this.

M2 Money Supply (St. Louis Federal Reserve)

{kind=link}

Third, I suspect that corporate margins will compress as pricing power declines and inflation (mainly labor) continues to take a toll. This will bring further layoffs. Plus, COVID-related savings are dwindling.

Bank balance sheets will be a critical factor. As I cautioned in my October 18, 2022 SA article , the combination of QT and onerous bank regulation severely limit the capacity of banks to supply financing to the economy. This could trigger a liquidity crisis which might, in turn, spark an economic downturn and give the Fed with cover to cut rates.

The inverted yield curve is another portent of recession, but I don't assign it much importance. While longer-term rates are at this point largely market-determined, the short end is arbitrarily manufactured by the Fed. Thus, I don't think it has much information content.

For all these reasons, my “worst feasible case” forecast assumes that sometime around mid-year the Fed will slash the rate it pays on reserves and Reverse Repo to, say, 1-2%. This will be low enough to ensure a positive carry on its bond portfolio.

A steeply positive yield curve immediately will ensue. Banks, hedge funds and other entities will capitalize on the positive yield curve to establish bond positions. Depending on where Repo rates actually settle, the Fed’s Reverse Repo facility could disappear.

The race to establish positions will tend to drive long term rates lower. But if the Fed pursues QT as advertised, selling $95 billion in securities every month the Fed presumably will sell into any rally. This, along with continued huge Treasury borrowing, will support longer term interest rates and keep the yield curve steep. Rates could easily move higher.

My guess is that the banking system’s capacity to add even low risk or risk-free assets is decidedly limited. Liquidity regulations will make bank purchases of longer-term bonds especially problematic.

I am assuming that bank reserves no longer impose a significant constraint on bank balance sheets. As mentioned earlier, reserve requirements are no longer a focal point for Fed policy. Total reserves of the banking system are $3 trillion which by historical standards would seem adequate to support $18 trillion in deposits.

Post-Pivot, a Short-Term Rally, Then . . . ?

Bottom line, in the aftermath of a Fed pivot, I think that overnight rates would drop to 1.0% to 2.0%. I assume that the 10-year bond rate would decline slightly, but not dramatically.

A policy reversal of this magnitude would be a shock for the stock market, but it’s not clear to me that the immediate impact would be negative. In fact, I suspect that the immediate stock market reaction would be a sharp rally. Fed easing almost always produces a market rally.

But I am extremely doubtful that any reflexive post-pivot bounce will be sustained. When the dust clears, what appears to be “loosening” by the Fed will prove to have been a mirage: if it continues to pursue QT, policy will be just as tight as before.

In fact, one could argue that rate hikes in the past year have been loosening, not tightening, monetary policy since these interest payments add reserves to the system. Thus, a “Pivot” that reduces short term rates might actually tighten financial conditions.

Alternatively, if the Fed abandons QT, it risks rekindling inflation.

At this point, I’m afraid my crystal ball for the stock market grows cloudy. I hope that our recovery from any recession will be rapid, but I'm afraid it could be a very tough slog.

The Fed's Shameful Double-Standard

To reiterate the point that I hammered on in October, our commercial banking industry is extraordinarily well positioned to be a source of strength in a recession. Balance sheets and credit quality are the strongest they have been in at least 50 years. But banks can only help if their draconian regulatory straight jacket is relaxed.

In fact, regulatory policy for US banks is thoroughly bankrupt, especially as regards the Federal Reserve. And I'm not just speaking metaphorically. Using a “fair value” benchmark, the Fed is deeply, deeply insolvent. The current “mark-to-market” loss on the Federal Reserve’s balance sheet may be as much as one trillion dollars. Yet no one has stepped in to shut them down. To my knowledge, the Fed has not even prepared a “living will” with which to guide its resolution.

Bank securities portfolios, too, have lost value as interest rates have risen. But bank accounting standards dictate that for banks, unlike for the Fed, these losses must immediately be marked down in bank equity accounts. Yet bank earnings continue to grow and franchise values that are expanding. This underscores the idiocy of mark-to-market accounting for banks.

There is one silver lining to our “worst feasible case.” It might get us one step closer to a fixed income market that is not manipulated by the Fed and allows genuine price discovery. That alone might reduce market uncertainty and benefit stock valuations.

Investment Implications

Here is how I am positioning my own portfolio for the economic environment I envision:

I am maintaining a larger than usual cash position – in the 20% neighborhood and I am selling calls where possible on my long positions. I think that we will have an opportunity to buy most stocks at lower prices later in the year. But even after their recent rally, most stocks are selling well below their highs.

My biggest positions include:

The Norway ETF (NORW)

This ETF, like Norway's economy, is very heavily weighted toward natural resources companies, which I think will continue to do well. The Norwegian energy companies are very serious about developing green energy. More importantly, I think the Norwegian Krone is the world’s most attractive currency. The country’s fiscal and trade balances are in very good shape. Plus, Norway has a sovereign fund that is larger than one year of GDP.

Bank Stocks

I own Citigroup ( C ) and Comerica (CMA.) Citi is selling at 60% of book value and – hopefully - will be allowed to buy back stock later this year. As expressed in this report, I am hopeful that Congress will do the right thing and loosen the reins on bank regulations. This would be extremely positive for the stocks, but I’m not counting on it.

Lithium producing stocks

Demand for lithium batteries will only grow. Also, the recently successful fusion process uses lithium. Admittedly, this is a bit of a pipe dream on my part, but if we get news that the fusion process is scalable, lithium will be a major beneficiary.

Emerging market stocks

These have lagged for US stocks for at least a decade, and I think many countries stand to benefit from supply chain shifts away from China. I am avoiding China, which recently hasn’t been very smart. I wish that the governments of these countries were becoming more responsible, but at least they are not regressing as we are.

Short the high-yield bond ETF (HYG.)

I am using put options, which seem reasonably priced. As mentioned in the body of the article, I am convinced that a recession is likely in 2023 which, along with higher interest rates, will pressure corporate cash flows. Moreover, junk bond spreads have narrowed to near all-time lows. If you short the HYG, you should also consider going long a shorter term Treasury ETF like the IEF (5-7 year average maturity) in case the short end of the yield curve does drop sharply. A widening high yield spread should work in your favor.

Other than these positions, my portfolio looks much like the S&P 500. I am lightening up on my tech positions, which have had a run that I think is a bit overdone.

For further details see:

Prepare For Fed Easing And A Market Rally By Year-End