PSMT - PriceSmart: Cooling Inflation Growing E-Commerce And Retail Sales Will Support Future Growth

2024-01-03 22:49:59 ET

Summary

- PriceSmart has shown strong historical revenue growth and stable margins, with a strong performance in 4Q23.

- Inflation cooling in Latin America is expected to boost retail spending, providing opportunities for revenue growth.

- The e-commerce market in the region is experiencing strong growth, and PriceSmart is investing in its digital capabilities to capture this growth.

- My valuation model reflects a double-digit upside potential, thus leading to a buy recommendation.

Synopsis

PriceSmart ( PSMT ) runs membership warehouse clubs, offering a wide range of high-quality goods and services at low prices to its members. They operate mostly in Central America, the Caribbean, and Colombia.

PSMT's historical revenue has shown robust revenue growth driven by COVID pandemic easing. In addition, margins over the years have remained robust as well. As a result, it managed to grow its diluted EPS annually. For 4Q23, revenue continues to show strong growth. While 4Q23 margins came under slight pressure, it was mainly due to tax litigation. On a FY2023 basis, it was in line with FY2022. Thus, I expect it to continue maintaining its robust margins in the quarters ahead.

Moving ahead, as inflation cools, I anticipate it will boost retail spending, which will create tailwinds for PSMT's revenue growth. In addition, Latin America's total retail sales and e-commerce are expected to grow for the foreseeable years ahead. As such, it provides PSMT with the room and opportunity for revenue growth. With double-digit upside potential, I am recommending a buy rating for PSMT.

Historical Financial Analysis

Over the last four years , its revenue growth has been increasing from 2020's 3.33% to 2023's 8.58%. However, I do notice a slight slowdown in 2023 revenue growth, but it is still strong given that it is above its 5-year revenue CAGR of ~6.7%. Overall, on the top line, its revenue growth is looking strong and robust.

Author's Chart

Apart from its robust revenue growth, its margins have been robust and stable over the years. In 2020, gross profit margin [GPM] was 16.65%. In 2023, it expanded to 17.21%. In terms of operating income margin [OIM], it was 3.69% in 2020, and it has expanded to 4.66% in 2023. Lastly, its 2020 net income margin [NIM] was 2.32%. In 2023, it expanded to 2.45%.

Author's Chart

As a result of strong revenue growth and robust margins, it managed to grow its diluted EPS annually from 2020's $2.55 to 2023's $3.50. This represents a growth rate of ~37%. With growing EPS, it was able to increase dividend payments over the last 5 years. In 2019, the total dividend declared for the year was $0.70 per share. In 2023, it grew to $0.92 per share. This represents a growth rate of ~31%.

Author's Chart

4Q23 Financial Results

For 4Q23 , it reported robust quarter performance. Revenue for the quarter grew 9.5% year-over-year to $1.12 billion, up from the previous period of $1.02 billion. Net merchandise sales grew 10% to $1.09 billion, up from the previous period of ~$989 million. Net merchandise sales are crucial when analyzing PSMT, as they form the largest share of its total revenue. Based on its 4Q23 results, it accounts for ~97% of its total revenue. The remaining ~3% is distributed among its export sales and membership income segments.

For the quarter, its GPM remained robust year-over-year. However, both its OIM and NIM contracted during the quarter. Management attributed these contractions to a $9.2 million charge for tax litigation and a $5.7 million asset impairment charge and closure costs. These are extraordinary events that are not expected to have a long-term impact on its future margins, and the contraction does not stem from core business operational issues. Therefore, looking ahead, I expect its margins to remain strong. Furthermore, as discussed in the 'Historical Financial Analysis' section, its FY2023 margins are still robust compared to 2022, further supporting my thesis that it will maintain its margins in the upcoming quarters.

Author's Chart

Cooling Inflation Serving As A Growth Catalyst

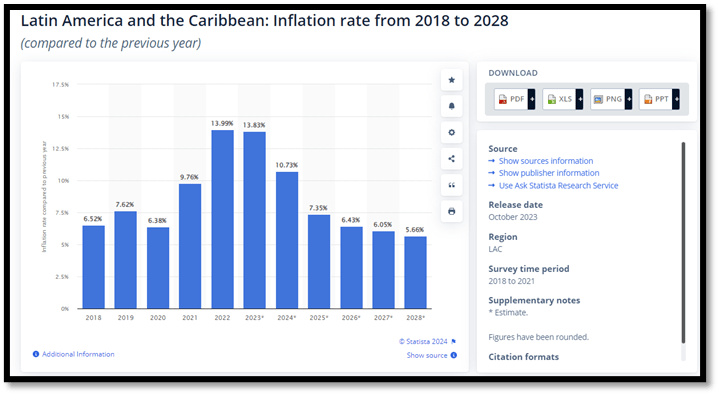

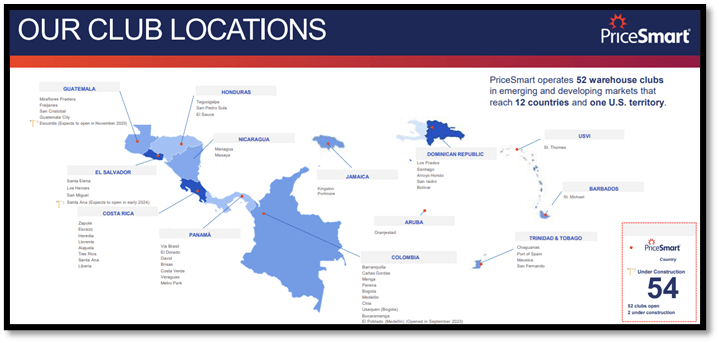

For the next few years, inflation in Latin America and the Caribbean [LAC] is expected to decrease. In 2022, it peaked at 13.99%, and by 2028, it is expected to decrease to 5.66%. Based on its club location diagram, it's clear that PSMT operates mainly in LAC regions. Therefore, it is more accurate to look at inflation in this region of the world.

Cooling inflation tends to spur economic growth as it induces more consumer spending and also interest rate cuts. According to the World Bank economic review for LAC, they estimated that the region's GDP will grow by 2% in 2023, which is above the previously estimated growth of 1.4%. For 2024 and 2025, LAC's GDP is anticipated to grow at 2.3% and 2.6%, respectively.

{kind=link}

{kind=link}

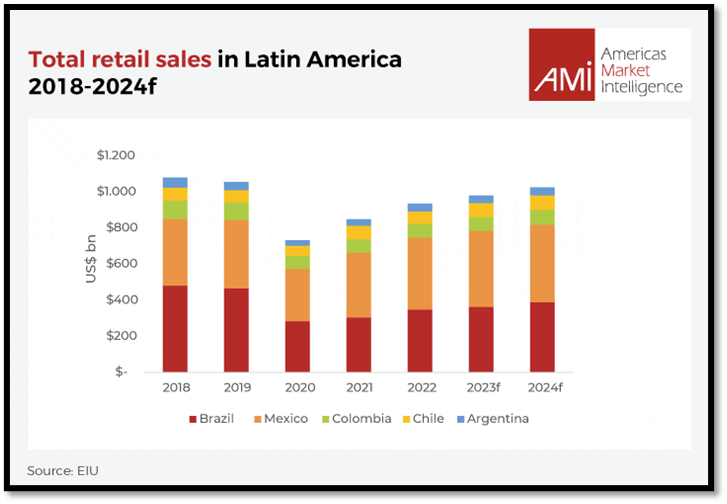

Based on the following chart by AMI , total retail sales in 2022 were valued at ~$900 billion. For the next two years, it is anticipated to continue growing, reaching ~$1 trillion by 2024. However, I note that 2024's level is still below pre-pandemic levels due to the current high inflation rate. However, as inflation cools down for the years ahead, I expect the total sales to gradually increase in tandem and gradually reach and surpass pre-pandemic levels.

{kind=link}

Investment in Growing E-commerce Market

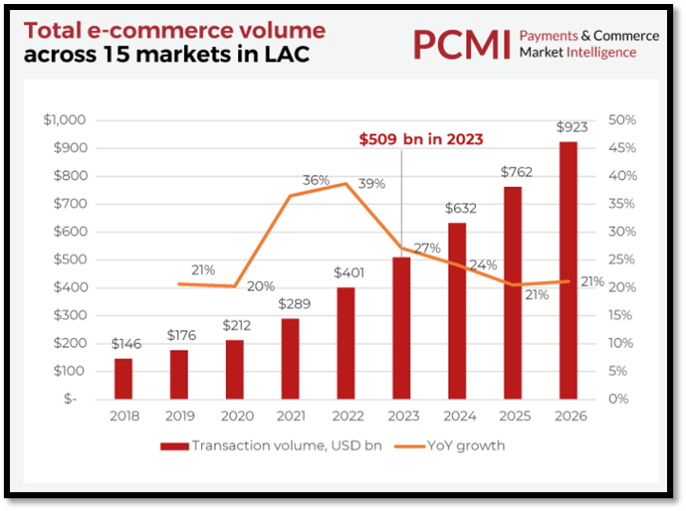

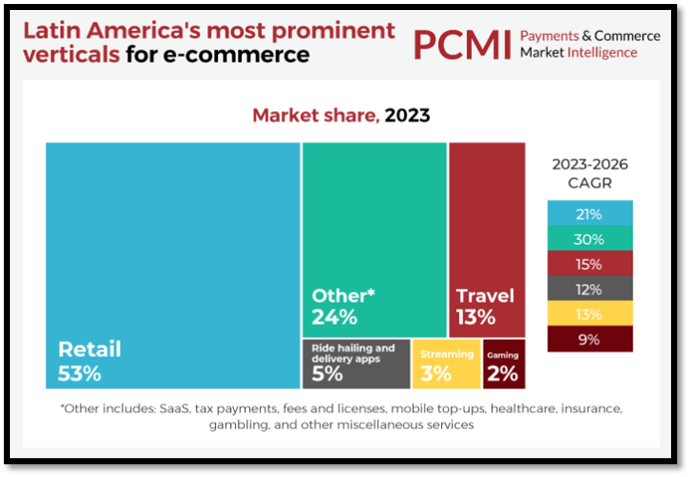

Based on the following chart , the e-commerce market in the LAC region is experiencing strong growth, and this growth is expected to continue growing strongly until 2026. As of 2022, it was valued at $401 billion, and it is expected to reach $923 billion in 2026. The e-commerce market is expected to continue growing at above 20% for the next few years. In the second chart, it is clear that retail forms the largest share of the e-commerce sector at 53%. Therefore, e-commerce is an important aspect of PSMT's business.

During the earnings call , management reported that 60.9% of members did create their online profiles, and 15.4% of membership base members made purchases on its website. Therefore, management believes that there is still room for growth in its e-commerce segment, and they are actively investing in this area to capture growth.

One move PSMT made to drive growth in its digital segment was appointing Wayne Sadin as its new CIO. Wayne has years of experience and success in the IT industry and this shows PSMT's commitment to improve and enhance its IT capabilities. Together, the fast-growing e-commerce market, PSMT's strategic initiatives to enhance its digital capabilities, and Wayne's experience will drive their future revenue higher.

{kind=link}

{kind=link}

Comparable Valuation Model

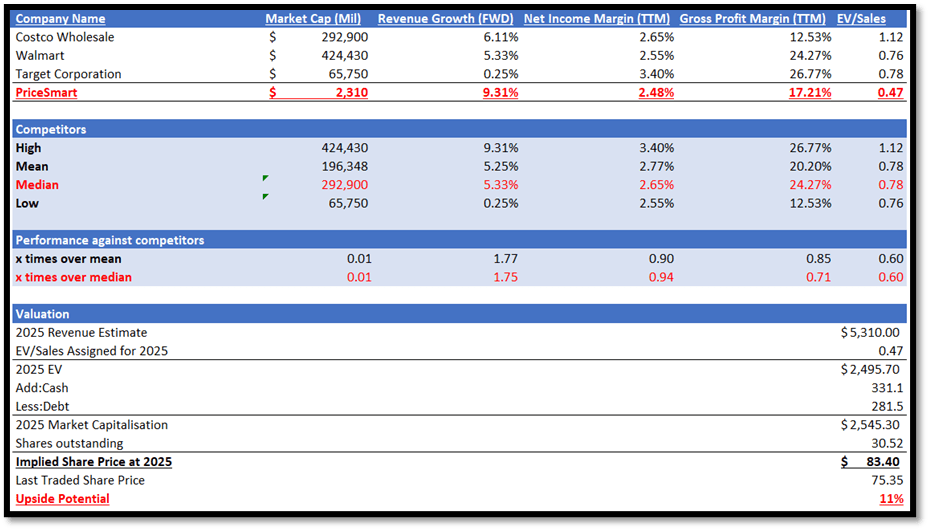

In my valuation model, I will be comparing PSMT with its competitors in terms of forward revenue growth outlook and profitability. The three competitors I listed in my model operate in the same industry as PSMT, which is consumer staples merchandise retail.

In terms of market size, PSMT is way smaller than its competitors, as it has a market capitalization of ~$2.3 billion, while the median market capitalization is $292 billion. This means that PSMT is only about ~1% of their size.

Despite its smaller size, it outperformed competitors in terms of forward revenue growth outlook, as PSMT's forward revenue growth rate is 9.31%, 1.75x higher than the median of 5.33%. Due to its smaller size, its GPM of 17.21% is lower than the median of 24.27% due to a lack of economies of scale. Even though it has a lower GPM, it is impressive that it performed in line with competitors in terms of NIM trailing twelve months [TTM]. PSMT's NIM TTM is 2.48% vs. the median of 2.65%.

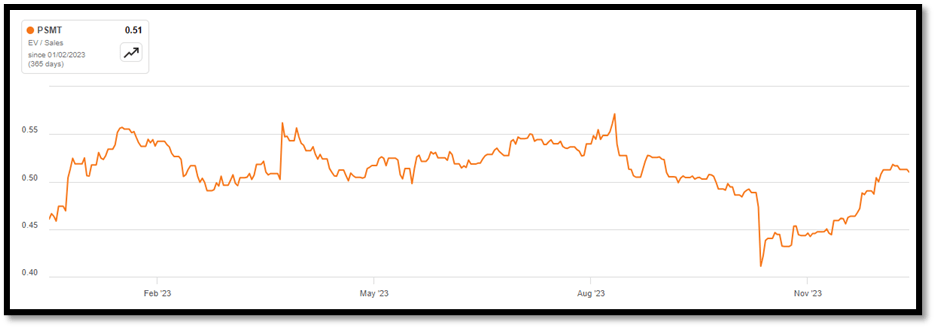

Currently, PSMT's EV/Sales trades at 0.47x, which is lower than the median of 0.78x. However, I argue that this valuation is fair for PSMT as it is much smaller in size and operates mainly in the LAC region, which carries and commands a higher risk return due to country risk. In addition, its current valuation is in line with its 1-year average, further supporting its current valuation.

The market revenue estimate for 2025 is ~$5.31 billion. Given the growth outlook and its financial strength that I have discussed in depth above, it supports this estimate. By using 0.47x on its 2025 revenue estimate, my target price for PSMT is $83.40, which represents an implied upside potential of 11%. With these, I am recommending a buy rating for PSMT.

{kind=link}

{kind=link}

Risk

One downside risk of buying PSMT would be regarding the market it operates. It operates in emerging markets, and these markets introduce additional risks such as economic and political instability. Such instability can lead to forex fluctuation, which will affect COGS or government interventions and policies to combat it. These factors can disrupt PSMT's operations and financial performance. Furthermore, less developed infrastructure in these markets, including transportation and distribution networks, can pose challenges for improving operational efficiency.

Conclusion

In conclusion, PSMT's past four years have demonstrated strong revenue growth. In addition, its margins over the years have remained stable. The combination of these two factors allowed PSMT to grow its diluted EPS annually. In its 4Q23, revenue growth continues to be strong, with net merchandise growing 10% year-over-year. Although margins for the quarter contracted slightly, it was mainly due to tax litigation costs, which are a one-off event. On a yearly basis, FY2023's margins are in line with the previous year.

As we move into 2024 and beyond, the anticipated cooling inflation in the LAC region will bolster PSMT's future growth as it will encourage retail sales. In addition, both retail sales and the e-commerce market in Latin America are anticipated to continue growing for the next few years, which will further support PSMT's revenue growth.

As PSMT operates in emerging markets, investors would demand an additional return in the form of a country risk premium. Therefore, it is justified for PSMT to be trading at a lower forward EV/Sales. With my target share price indicating double-digit upside potential, I am recommending a buy rating for PSMT.

For further details see:

PriceSmart: Cooling Inflation, Growing E-Commerce And Retail Sales Will Support Future Growth