PROSF - Prosus: The Lack Of Upside Is Clear To Me Here

2023-10-27 07:32:16 ET

Summary

- Prosus is not a bad company, but its success in the past does not guarantee future success.

- The company is set to increase its adjusted earnings, but that doesn't automatically make it more attractive.

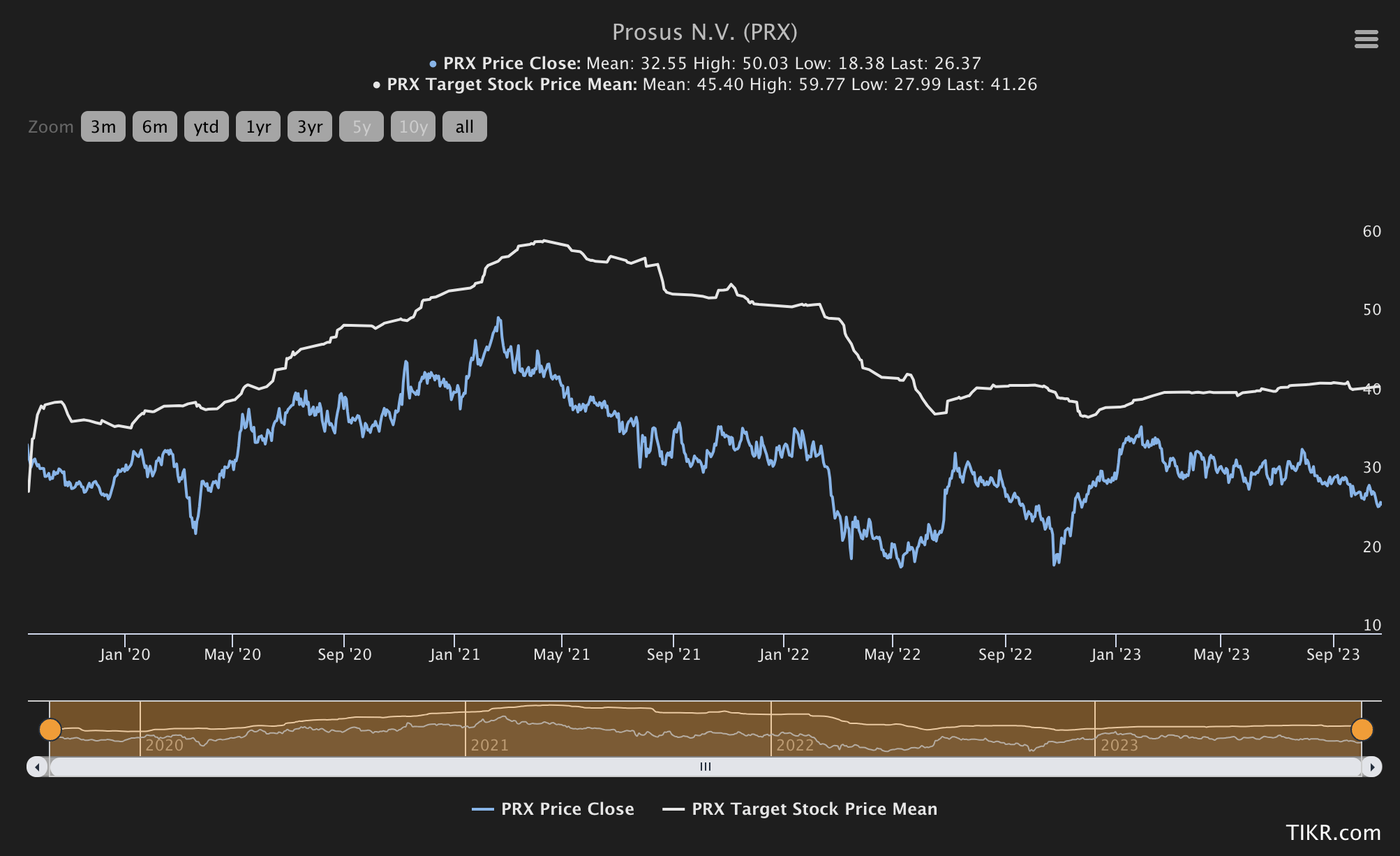

- Prosus has not achieved net profitability in any of its current investments, its appeal lies in legacy - and this is not enough for me. I say "HOLD".

Dear readers/followers,

Prosus (PROSY) is a company I've been actively reviewing for over a year at this point. My coverage hasn't always been popular - similar to my coverage of PayPal (PYPL) - but this is something I expect when the company is, according to many of its investors, a tech darling. I got a request to re-review the company fairly recently. Prosus has moved double digits in a relatively short time frame, begging the questions by some investors if now could be the time to invest in the business, or if I am updating my price target for the company.

In this article, I'll aim to answer that question, and see if the company is worth investing in - but if you're aware of my coverage here to any degree, you probably know the answer to that question, at least as far as my own stance goes.

Prosus is not a bad company. You can't call a company with this business history a bad company. However, the company having one success does not equate to it having more successes of the same caliber going forward.

I'll clarify here that the company is actually set to increase its adjusted earnings by a significant amount on a forward basis.

This does not mean the company is automatically more attractive here though - let's take a look.

My last article on Prosus can be found here. I was neutral, and this rating obviously turned out to be exactly correct.

Seeking Alpha Prosus (Seeking Alpha Prosus)

Prosus - A lot to like, but only at a steep discount, given its status as a Tencent proxy.

I will state with clarity here that my coverage on Prosus for the past 1+ year and the associated ratings with this coverage have been absolutely unerring looking at the share price and valuation today. I'm not shy about when my ratings, even in the short term, are wrong, but I'm also clear about when I see my ratings as "correct" overall.

Despite tech seeing good trends, we're not seeing significant outperformance from Prosus here. Since very early on, I've held my discount thesis for Prosus. At this time, the discount I want to see for Prosus in order to invest in the business is over 50%. However, at one time during the coverage spectrum, the company was actually buyable to my share price target. If you had followed that and bought a sub-€55, you would have been at positive RoR now. Please note that €55/share is not my PT at this time, however.

The only positive set of news, as I see it, for the latest 12 or so months, is the unwinding of the cross-holding structure for the company, which will have result of simplification, while maintaining the interest split in a more traditional manner. This is little more than a slight improvement of something that should have been clear or done from the get-go though.

As before, none of Prosus' current investments are GAAP-profitable or net profitable, unless you start significantly adjusting those results. The company continues to beat the drum for "strong performance" from its food delivery, classified, payment/fintech, and edtech vectors, and while streamlining and improvements are indeed being done, there is no implication of near-term GAAP or net profitability in any of these businesses.

This environment is a testing ground for businesses, especially businesses in the tech sector which have been some of the clear beneficiaries of the ZIRP environment we've been in for many years.

When I say no clear indications of near-term profitability, I mean that the closest potential profitability estimate is during 1H25. I also want to be very clear about the fact that Prosus is terrible at hitting any sort of analyst estimate. For FactSet analyst estimates, the company misses 100% of the time even with a 20% margin of error for the past few years (Source: FactSet).

So when this company gives an estimate or guidance, I would be inclined to take that with a fair bit of salt. Since early 2021, none of these things has managed net profitability or a positive trading result.

Prosus IR (Prosus IR)

The improvement here, if it can even be believably called that, is only a lower rate of loss compared to the 1H23 period, which is here called the high point of the company's overall losses.

And the company's recent trends and sales don't exactly inspire confidence in the company's business acumen. I only say that because any divestments made by the company have come at a negative profit relative to what was invested when it was purchased, the definition of a loss or a negative. On a high-level perspective, the only thing Prosus has going for it is the Tencent investment, which is a hundred-point-buck sort of investment.

Instead of improving fundamentals, Prosus uses its impressive war chest to perform financial alchemy, which is what I like to call buybacks. This might enhance the company's NAV, and the company obviously believes it is buying back equity for less than it's actually worth, but as I've stated before, this is something that I question with regard to the valuation of that equity.

AI has come into the mix of course, as it seems to have come into play for most companies and businesses even remotely connected to IT or information here. But this continued focus on what I would call softer values and KPIs shows me that a focus on net profitability is not Prosus' main concern or target at this time. And to those that still argue, years after tech mania, that "net profitability isn't the point", I say that net profitability is the point for any company that wants to survive.

As interest rates climb higher and this starts impacting the company's financing - or even just the cost of capital, as any business should consider, we will , as I see it, witness this impact on the valuation.

Positives for Prosus do exist, and they are not few. Prosus is incredibly well-capitalized. It has zero liquidity issues and I don't believe it is overstated to say that it can live off its Tencent "nest egg" for a decade before it would be in any trouble. Many of the company's investments actually seem like very good businesses.

prosus IR (prosus IR)

And not just in one vector, but in several. To be very clear, I do not mind these sorts of businesses - what I am looking for are simply profitable businesses with an upside, and I want the businesses that I invest in to focus on very fundamental KPIs. That's why I have such problems with many of the businesses that rose to prominence during ZIRP - because I felt that their focus, outside of that "free money" environment, was wrong or flawed.

Prosus can certainly be congratulated for managing to streamline operations as much as we're seeing here. However, none of the businesses that we see here are of yet seeing bottom-line profitability.

The bullish thesis for Prosus remains focused on the eventual profitability of it segments while using the Tencent stake as a sort of Rock of Gibraltar-type safety in terms of the company's economy. This is not a bad thesis or expectation, provided that profitability is not too far off. Recent management guidance does point to an earlier breakeven in terms of its "Managed companies" than expected, with no selling or shutdown of further assets to bring about this goal - but this, again, is not "good enough" for me.

Its move into AI is actually more of a worry than it is a positive for me.

The bearish thesis, which I am obviously more closely adhering to, is continuing devaluation on the basis of interest rates/risk-free rates, cost of capital, and continued potential underperformance in a rising cost environment from Prosus, which I consider likely.

Let's look at the recent valuation results now that we're down more than 10% in less than 2 months.

Prosus Valuation - Still not the greatest, despite going lower.

My latest PT for this company was €35/share. Obviously, I do not regret going this low for the company given the latest trends in valuation. I remain very dubious about how a company should be valued which is essentially Tencent and a collection of currently unprofitable companies.

With the sale of Avito, I believe the company has posted very clearly just how bad things can go.

As you may notice, the company's current share price is actually significantly lower than my PT.

Should this not be a cause for celebration or a rating change?

No.

Because the reason is simply issuance. The NAV is different. At the overall NAV discount that I consider relevant with a discount rate of 60-70% to NAV, a Sub-€30/share price is entirely possible for Prosus - but that was pre-dilution.

The current NAV per share is now €43.7. A 60-70% discount range for Prosus now comes to an implied EPS of €13/share on the low-end side of things - I'll end up here at €15/share for the updated share price target for the company, but that still means that Prosus is significantly overvalued - if you believe my rate of discount for this business.

Most analysts do not.

The average analyst target for Prosus here is €41/share, from a range of €32 to €50/share on the high side. However, I want to point out that these 16 analysts following the company have typically held a 35-60% premium or upside to the share price, and the company has not moved to these levels for years.

{kind=link}

What you need to ask yourself is if you think it is likely that the company is going to trade at closer to a 100% NAV now that rates are increasing and money is getting more expensive.

I say "No".

You may view my targets as being extreme - and indeed, would say that given the other PTs here, my €15/share PT is extreme. However, it also represents the realistic earliest time that I would "BUY" Prosus given what's available on the market today. Therefore, it's my new PT.

Here is my thesis for the company.

Thesis

My thesis on Prosus is as follows:

- Prosus stock remains a somewhat unattractive investment due to the specifics of how the company operates and what it has. This lack of appeal has increased, as I see it, as we've moved into a higher interest rate environment where the demand for the company's investments in terms of profitability - which rely on cheap capital and being able to operate at a loss for some time - has increased. This view has not changed in June of 2022.

- The shareholder structure is unappealing and inherently disadvantageous to Prosus investors. While the company is fundamentally sound and has a good track record due to the Tencent investment, there are too many fundamental question marks to really make this an option for me.

- I would be interested in Prosus if the market decided to discount it more than 70% to its current NAV.

- I consider it a "HOLD" here. My PT is €15/share. This is not a change, it's only an update accounting for the recent dilution of shares compared to the new NAV of the company.

Remember, I'm all about

1. Buying undervalued companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime. Even if that undervaluation is slight and not mind-numbingly massive.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can't call this anything except a "HOLD".

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Prosus: The Lack Of Upside Is Clear To Me Here