PTRA - Proterra: Attractive Price With Potential Margin Expansion

2023-05-30 15:25:42 ET

Summary

- Proterra was oversold in March as profitability and growth weakened. Our finding suggests that it remains well-positioned to capture the long-term demand for heavy commercial EVs in the US and globally.

- Cost efficiencies through staff cuts and consolidation of bus and battery manufacturing may drive gross margin expansion in Q4 2023 and then FY 2024.

- At ~$1.1 per share, I believe this is an attractive entry point. Proterra appears undervalued even under my relatively conservative bull case target price.

Proterra (PTRA) is a market leader in the design and manufacture of heavy commercial electric vehicles / EVs. It generates revenue by manufacturing and selling transit electric buses (“Proterra Transit” revenue stream) as well as proprietary battery systems and charging infrastructure services (“Proterra Powered and Energy” revenue stream).

Proterra went public through an IPO at around $26 per share. However, the stock has fallen significantly. It is currently trading at approximately $1 per share, reflecting a significant drop of ~96%. Concerns about breaching financial covenants in Q4 last year as well as significant increases in cost of sales due to recent supply chain disruptions and parts shortages have impacted share performance.

As Proterra works through these challenges, I continue to expect strong demand for heavy commercial EVs in North America by 2030, supported by initiatives like the Inflation Reduction Act. As it stands, Proterra remains well-positioned to capture this secular demand.

Operational efficiency measures have been taking places. As of Q1 2023, Proterra has been working on improving major cost efficiencies as it made a major staff cut at the beginning of the year and aims to consolidate bus and battery manufacturing in its Greer and Greenville facilities to reduce overhead.

Based on the current situation, I rate the stock as a buy. The current price seems attractive to initiate a buy position and is undervalued based on my modeled target price, which already assumes a relatively conservative bull-case FY 2023 outlook.

Risk

It seems that suggesting that gross profit will turn positive in the second half of FY 2023 still remains overly optimistic. I feel that negative gross margin may remain longer than the management's suggestion in Q1 earnings call since it depends on the ramp-up capability at Powered 1. While Proterra displayed a decent capability to do cost optimization in the past pre-IPO , it just seems that Proterra has a lot more things going at the moment between making successful deliveries, finishing battery production at the City of Industry until Q3, and production consolidation at both Greer and Greenville facilities, which may add another layer of complexity. I feel that it is probably more realistic to expect a gross profit break even in the first half of FY 2024, rather than in Q3 or Q4 2023, as a result.

{kind=link}

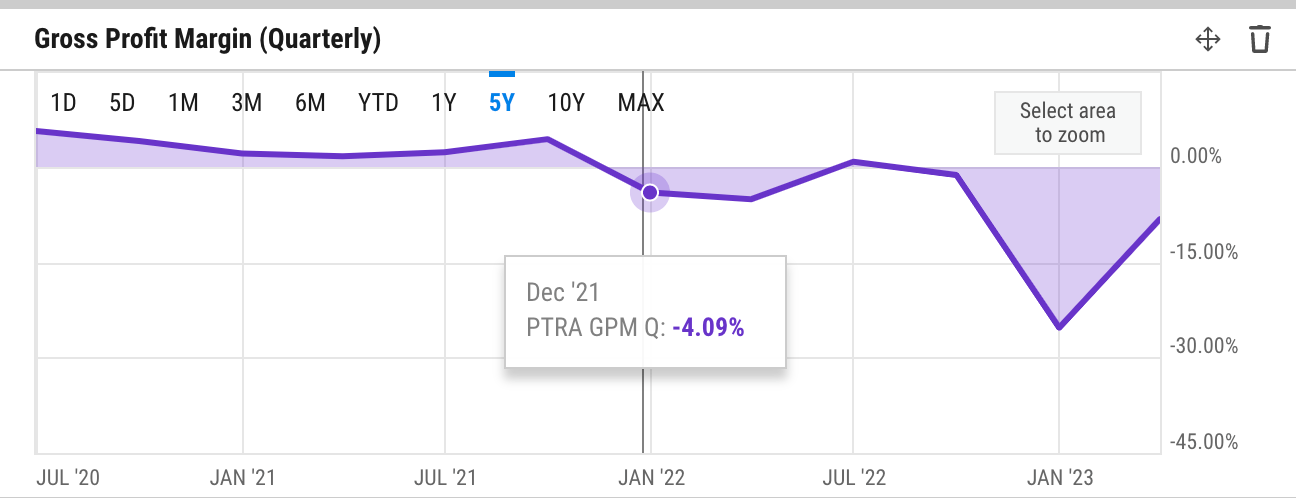

Proterra had a negative ~8% gross margin as of Q1, which means that it will need to expand quite meaningfully throughout the rest of the year to see a breakeven. If any, it will likely be driven by the profitability outlook for Q3 and Q4, considering that Proterra historically has reported higher sales in those two quarters. For instance, in FY 2021, a negative ~4% gross margin in Q4 pretty much offset a consecutive low single-digit, yet positive gross margin performance in the first three quarters to bring down the overall annual FY 2021 gross margin to ~0.84%.

Additionally, I also feel that there is a bit of execution-related procurement risk that needs to be accounted for, especially if Proterra is diversifying the supplier base to reduce the impact of future component shortages. Finding and working with more suppliers and building new sourcing relationships could present a new challenge for Proterra. Furthermore, as per its 10-K, Proterra has also been working with only one supplier - possibly South Korea's LG Chem (KRX: 051910) - to source lithium-ion cells, which is the most critical component of its battery technology.

In general, heavy-duty commercial EV companies like Proterra produce at a much lower volume than companies producing passenger EVs like Tesla (TSLA), and as such would probably benefit from higher supplier concentration to optimize purchasing volume and reduce unit cost per supplier. Proterra’s potentially high supply-base concentration is probably also well evidenced by the fact that the parts shortages were of things like wiring harnesses and resin for connectors - components that are more widely available than semiconductors and chips, which have been undersupplied since the last two years due to the COVID-19 impact on South Korea and Taiwan, two major producers of such components.

As such, while some supply chain issues might have been alleviated with the post-COVID reopening of China, the outlook of parts shortages remains uncertain in the near term despite the company announcing an intention to improve its supply chain capability, which may refer to supply base diversification.

Catalyst

All in all, I believe that Proterra's profitability headwind should be temporary, and I would probably project gross-profit breakeven to happen sometime in the first half of FY 2024. This will be facilitated by the ramping up of production at their Greer and Greenville facilities. By consolidating bus and battery manufacturing in these two locations, they can achieve better labor and overhead efficiencies, as well as cost savings in freight expenses. The proximity of the facilities, being just a 20 minute drive from each other, further supports this optimization.

{kind=link}

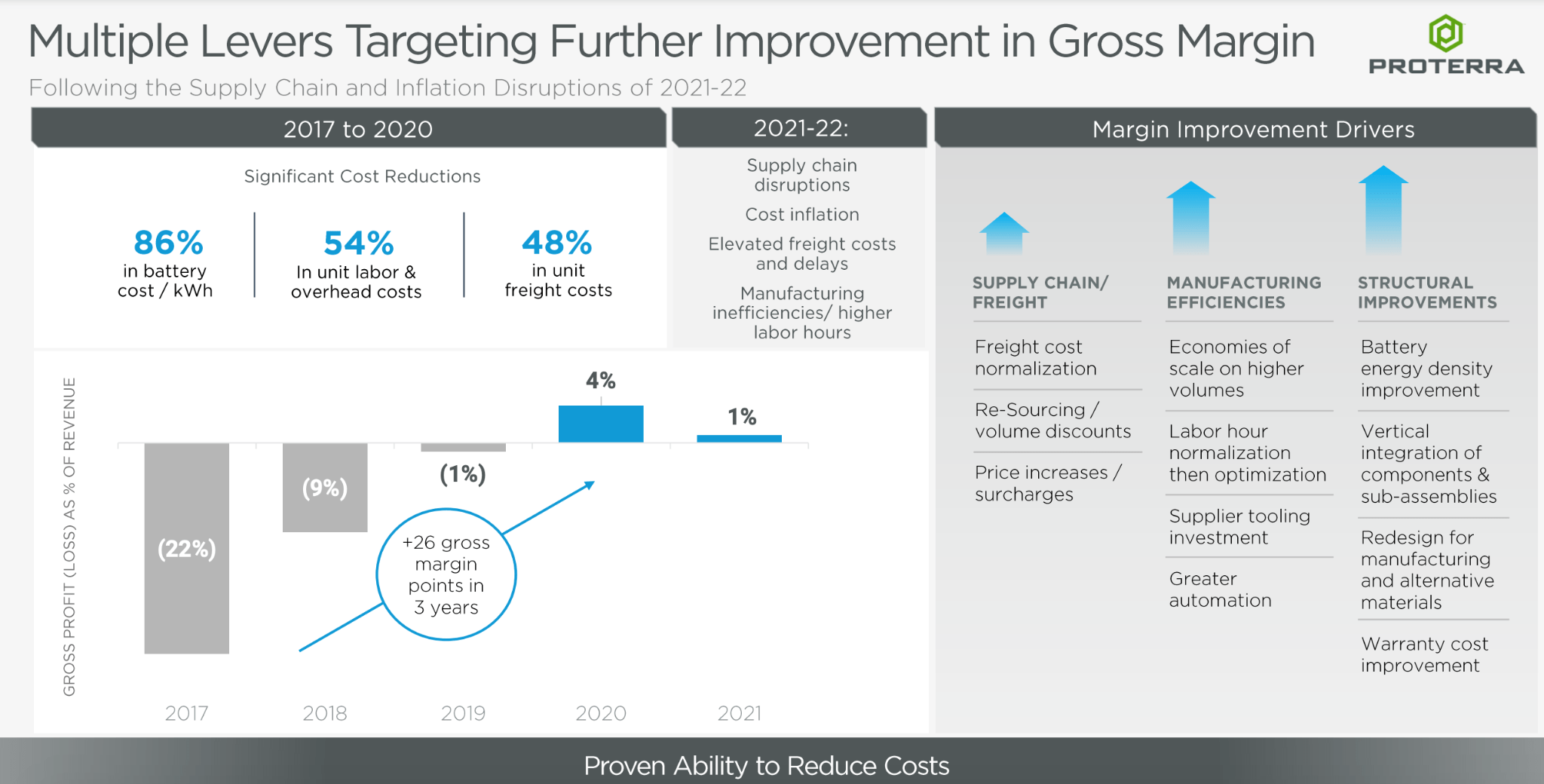

Historically, Proterra had also made a good achievement in optimizing its gross margin pre-IPO. However, since then, the gross margin has fallen and reached a negative 7.75% in FY 2022. It was a level previously seen between 2018 and 2019 when Proterra was in the middle of preparing a major launch of its Proterra Energy business unit, which seems like a comparable situation to today's major ramp-up of the Powered 1 facility, though with the added complexity of the supply chain disruption and inflation at present.

{kind=link}

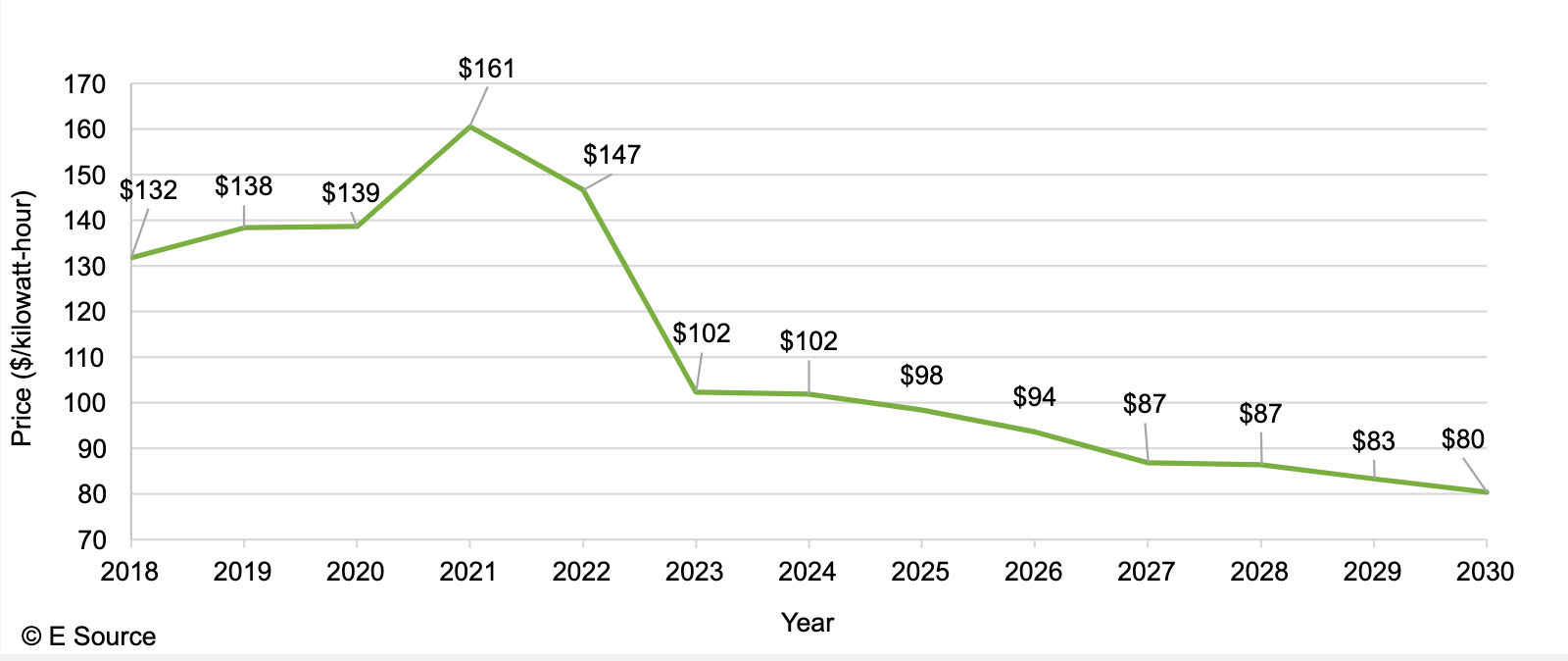

My view is that given that Proterra was able to improve gross margin by ~800 bps then, it is probably realistic to expect the same type of expansion over the next five or six quarters, driven by lower freight costs, higher manufacturing hours efficiency ( 250 hours less to produce a bus on average compared to in City of Industry), and continuing decline of battery cost / KWh , leaving Proterra with possibly a negative low single-digit gross margin in FY 2023, and 1% to 4% gross margin at the end of FY 2024.

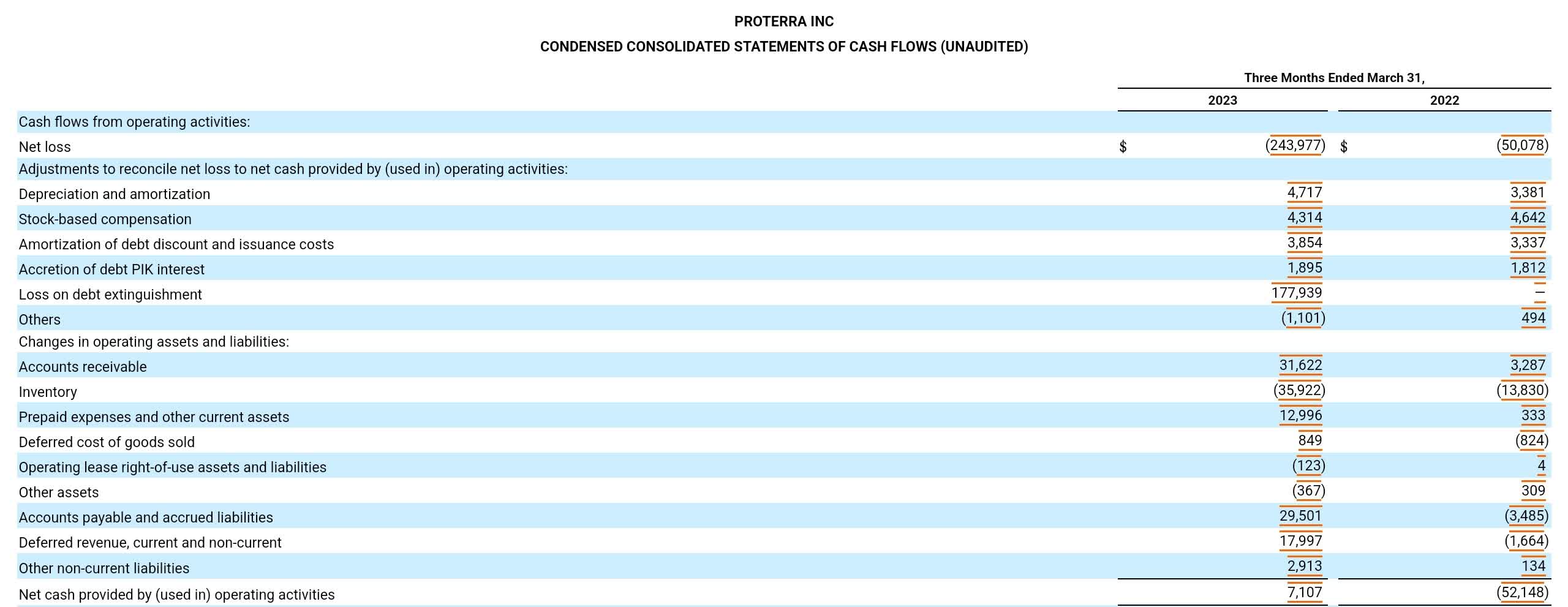

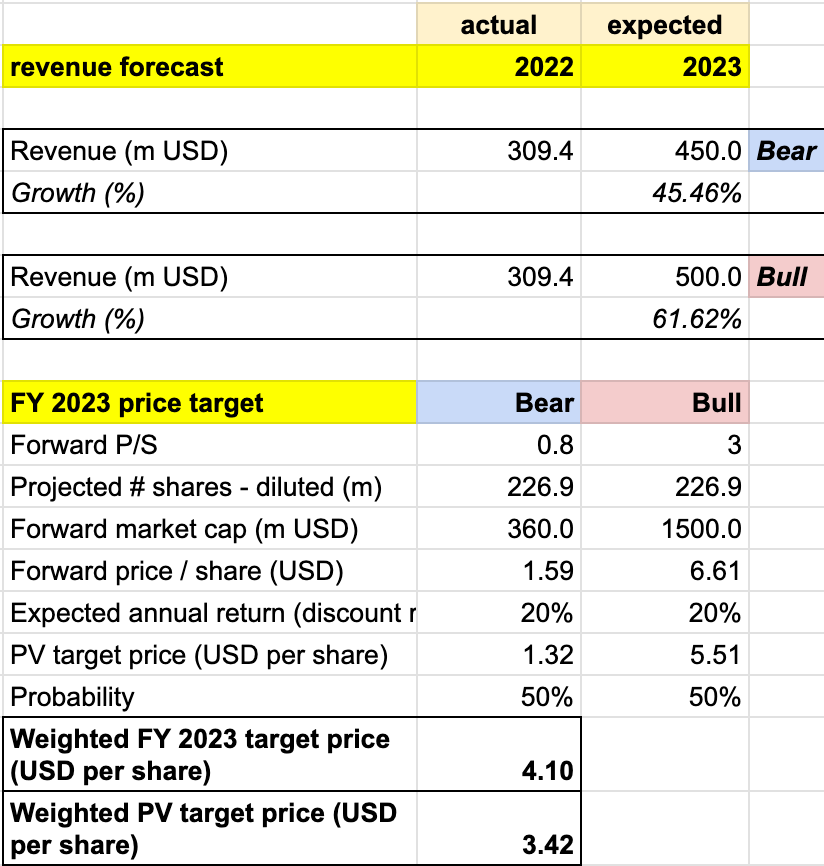

Looking ahead, Proterra's near-term growth outlook also remains solid as it guided to $450 - $500 million of revenue in FY 2023 (45% - 61% YoY), and with their cost optimization measures in place and a strong balance sheet. As of Q1, their total current debt and derivative liabilities were ~$314 million, while their current assets and cash positions were at ~$654 million and ~$296 million respectively. Furthermore, I also noted that Q1 operating cash flow / OCF was positive and on an uptrend, showcasing significant improvement compared to previous quarters.

{kind=link}

In Q1, OCF was ~$7 million, a big improvement from negative ~$52 million in Q1 2022. With negative $243 million, net loss also seems to widen by a lot in Q1, though if we account for the one-off +$177 million unrealized debt extinguishment loss, Q1 adjusted net loss was ~$66 million, a more similar level to last year's figure. As such, a lot of the OCF improvement was in fact driven by the operational improvements in operating assets and liabilities management through things like higher level of receivables collection and deferred revenue. With that in mind, I think that Proterra demonstrated that it has a good foundation to repeat that operational improvement as needed, alleviating concerns about a possibility of lowered cash flow outlook in Q2 due to a heavier cash usage for production growth in Powered 1.

Valuation/Pricing

My target price for Proterra is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 projection:

- Bull scenario (50% probability) assumptions - Proterra ends FY 2023 with $500 million of revenue and reaches positive gross margin in Q4, resulting in an overall FY 2023 gross margin of at best 1%. Nonetheless, the significant improvement in profitability would drive the premium on the valuation and reward Proterra a P/S of 3x, a level seen at the start of the year right before the earnings miss in March. This might be a bit conservative, since as a side note, Proterra generally had a high P/S in the past due to its higher growth rate. In FY 2021 where the company had a positive gross margin and +23% YoY growth, it reached a double-digit P/S, though it then normalized to 7x - 9x throughout the rest of the year.

- Bear scenario (50% probability) assumptions - Proterra ends FY 2023 with $450 million of revenue and reports a negative ~9% gross margin, lower than that of FY 2022, but a similar level to FY 2018. Despite meeting the lowest end of the guidance, the lower profitability outlook creates concerns regarding the timeline to break even and the productivity level at Powered 1, adding difficulties in capital raising. P/S to remain at 0.8x, where it is today.

{kind=link}

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of +$4 per share. Discounting that target price with a 20% discount rate, I reached a Present Value/PV weighted target price of ~$3.4 per share. The 20% discount rate represents the expected annual return for holding Gogoro.

In summary, ~$3.4 per share is the highest price point at which investors can purchase the stock to realize a projected 20% annual return should my FY 2023 target price of +$4 be achieved. At ~$1.1 per share today, the stock trades at a massive ~67% discount to my target price, suggesting that it is undervalued.

Conclusion

Despite facing challenges that have impacted its stock price, Proterra is still poised to benefit from the anticipated long-term demand for heavy commercial EVs, primarily in North America, by 2030, supported by initiatives like the Inflation Reduction Act. The company remains well-positioned to capture this market demand.

To improve near-term cost efficiencies, Proterra has taken steps such as a major staff cut and plans to consolidate bus and battery manufacturing in its Greer and Greenville facilities, aiming to reduce overhead and streamline operations.

Nonetheless, it is still likely that the stock may also trade sideways in Q2 given the possibility of unchanged profitability outlook in the near term. I would advise investors to closely monitor the progress into Q3, when the management suggests that there is a possibility of gross profit turning positive, potentially driving a slight rebound in share price.

I rate the stock a buy. The current price appears attractive for initiating a buy position, as I believe it is undervalued based on my modeled target price, which already assumes a relatively conservative bull-case FY 2023 outlook.

For further details see:

Proterra: Attractive Price With Potential Margin Expansion