PRYMY - Prysmian: A Call Option On Offshore Energy Trading At An 8% FCF Yield

2023-08-01 11:30:00 ET

Summary

- Prysmian is a leader in submarine cables and a leader in connecting offshore windmills to the power grid.

- The first semester was much better than I had expected.

- This results in a full-year free cash flow guidance increase of 20%.

- The anticipated 600M EUR in free cash flow includes investments in growth like a new plant and a new vessel.

Introduction

Back in April, I was quite charmed by Prysmian’s ( OTCPK:PRYMY ) ( OTCPK:PRYMF ) financial performance. Although the company is a world leader in submarine cables, its valuation was very reasonable as the stock was trading at just around 8 times EBITDA . That’s relatively low, especially knowing Prysmian has been scoring multiple new contracts in the energy division.

{kind=link}

Prysmian has its primary listing in Italy where it's trading on the Milan Stock Exchange with PRY as its ticker symbol. The average daily volume in Italy is approximately 860,000 shares per day and there are options available in Italy. Prysmian currently has approximately 272.6M shares outstanding and the current market capitalization is approximately 9.88B EUR and that’s pretty flat compared to where the company was trading at about four months ago.

A look under the hood after the H1 results

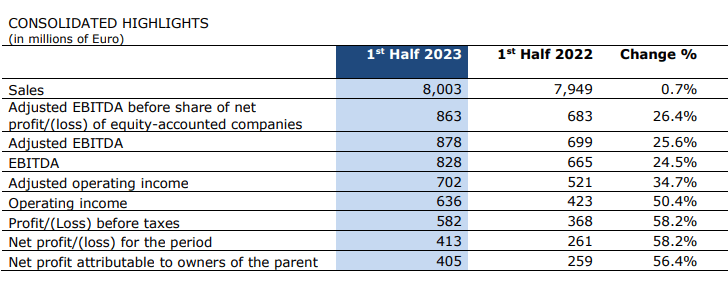

And Prysmian performed quite well in the first semester. It reported a total revenue of 8B EUR, thanks to an organic revenue growth rate of just under 5%. And perhaps the margin expansion is even more important (and impressive) as the adjusted EBITDA result increased by a whopping 25.6%. As you can see below, the EBITDA margin increased from 8.8% in H1 2022 to almost 11% on an adjusted basis.

{kind=link}

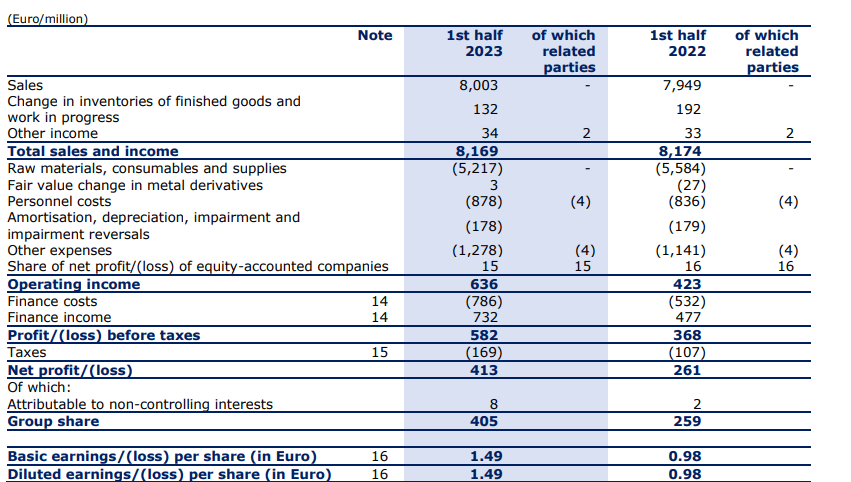

That EBITDA boost was mainly generated thanks to lower operating costs. As you can see below on the income statement, the total amount spent on raw materials and consumables decreased by almost 350M EUR. And although the personnel expenses increased and the ‘other’ expenses increased as well, the cost savings on the raw materials were sufficient to push the operating income substantially higher. With an increase of in excess of 50%, Prysmian’s first semester was a pleasant surprise.

{kind=link}

This all resulted in a pre-tax income of 582M EUR and a net profit of 413M EUR of which 405M EUR was attributable to the shareholders of Prysmian. This results in an EPS of approximately 1.49 EUR per share.

That’s an excellent result and definitely better than I had expected. But as explained in my previous article , I’m also very interested in the cash flow profile of a company.

In Prysmian’s case, it is important to take the working capital changes into consideration. You traditionally see a build-up in working capital items in the first semester and the majority of those investments gets released in the second half of the year. While managing the working capital is an essential element of managing a business, it also makes sense to look at how the ‘core’ activities of a company are performing. If there’s not additional growth, no investments will be required in additional working capital elements and calculating the free cash flow result before these working capital elements provides a closer look that’s more fair.

{kind=link}

As you can see above, the reported operating cash flow was a negative 134M EUR. This includes about 24M EUR in taxes paid that were not owed based on the H1 income statement (193M EUR versus 169M EUR) while you also very clearly see a net investment of 756M EUR in working capital. We should also deduct the 32M EUR in net finance income from the equation and this means the adjusted operating cash flow in the first half of the year was a positive 614M EUR. And with about 164M EUR in capex, the net free cash flow was 450M EUR of which about 445M EUR was attributable to Prysmian’s shareholders. This means the H1 free cash flow result was approximately 1.63 EUR per share.

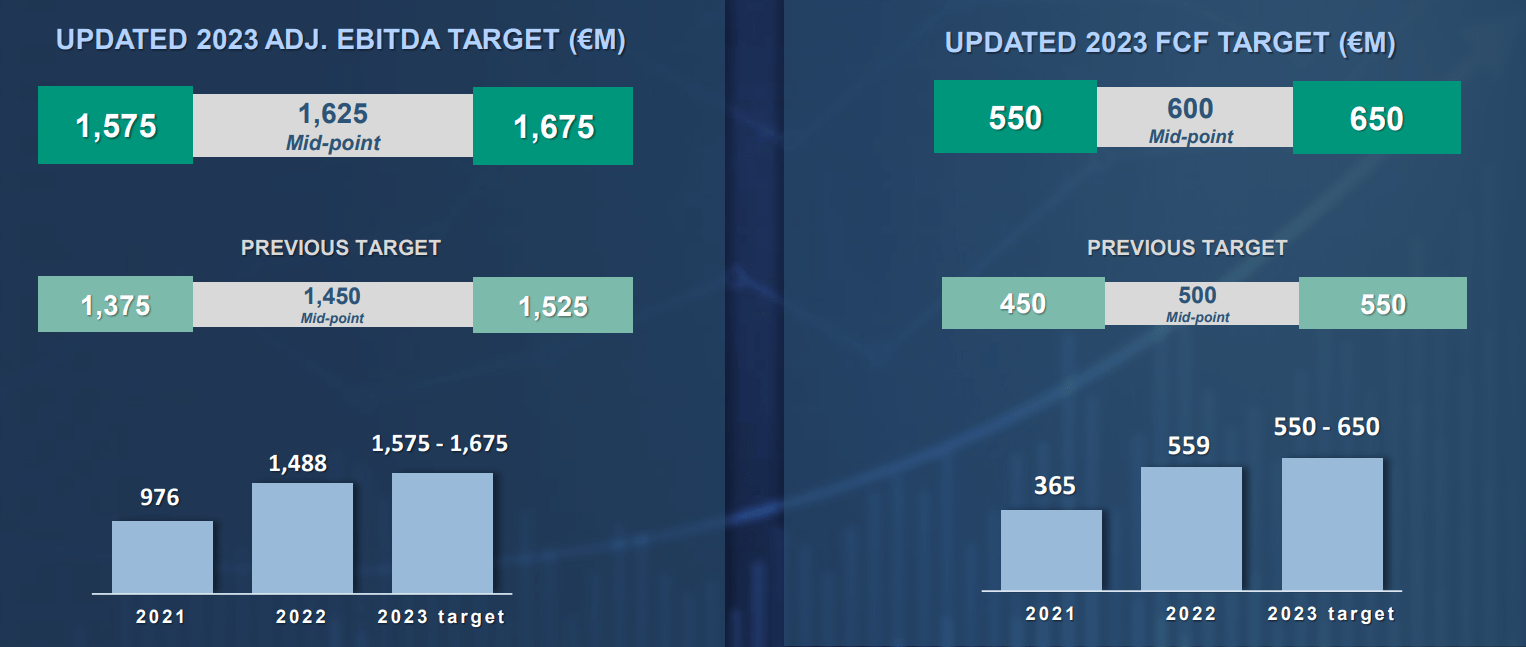

The adjusted EBITDA of 878M EUR is an excellent result and this immediately caused the company to hike its full-year guidance. As you can see below, Prysmian now expects to generate an adjusted EBITDA of 1.63B EUR (the midpoint between 1.58B EUR and 1.68B EUR) which is a 10% increase from the previous guidance. Meanwhile, the free cash flow result has been hiked by 20% from 500M EUR (midpoint) to 600M EUR. That would represent a full-year free cash flow result of approximately 2.20 EUR per share.

{kind=link}

The full-year free cash flow guidance appears disappointing considering the company already generated about 445-450M EUR in free cash flow in the first half of the year, but there’s a straightforward explanation for that. First of all, Prysmian includes working capital changes in its full-year guidance. While this will have an impact, the impact will be relatively small and the major ‘culprit’ for the low full-year free cash flow guidance is the fact the full-year capex is back-end loaded. Prysmian is investing in growth and as I explained in my previous article, the company is building a new cable plant in the USA and has ordered a new cable-laying vessel which will be delivered in 2025. This means the sustaining free cash flow yield (excluding the investments in growth) is likely closer to 8%.

The guidance hike comes on the back of the strong order book which improves the visibility. The backlog of firm orders currently stands at 9.1B EUR.

{kind=link}

Investment thesis

While the underlying free cash flow result in the first semester before taking any working capital changes into account was excellent, the full-year free cash flow guidance may sound a bit disappointing until you realize the full-year capex will likely be about 50% higher than the depreciation and amortization expenses. Even taking that into consideration, the 2.20 EUR per share in free cash flow still represents a free cash flow yield of in excess of 6%.

Meanwhile, the strong H1 result and updated EBITDA guidance means the current enterprise value (with the net debt defined as cash minus financial liabilities and not including other financial assets) is approximately 12.4B EUR which represents about 7.5 times the EBITDA guidance. And as the company will be able to convert working capital items into cash during the second semester, the net financial debt level should decrease towards the end of the year, resulting in an EV/EBITDA ratio of just 7%.

This makes Prysmian a ‘buy’ at the current share price. I still don’t have a long position but despite the low volatility ratio I am keeping an eye on the option premiums. A P33 for October for instance has an option premium of 0.60 EUR per share which would allow me to buy the stock at a 10% discount to today’s share price.

For further details see:

Prysmian: A Call Option On Offshore Energy, Trading At An 8% FCF Yield