PRYMF - Prysmian: A Leader In Submarine Cables At Just 8x EBITDA

2023-04-14 10:30:00 ET

Summary

- Prysmian is an Italian company focusing on cables with submarine cables as a specialty.

- The company's free cash flow result remains strong, despite investments in a new production plant and a new cable-laying vessel.

- The company is trading at just under 8x EBITDA for 2023 and at less than 7x the anticipated 2025 EBITDA.

Introduction

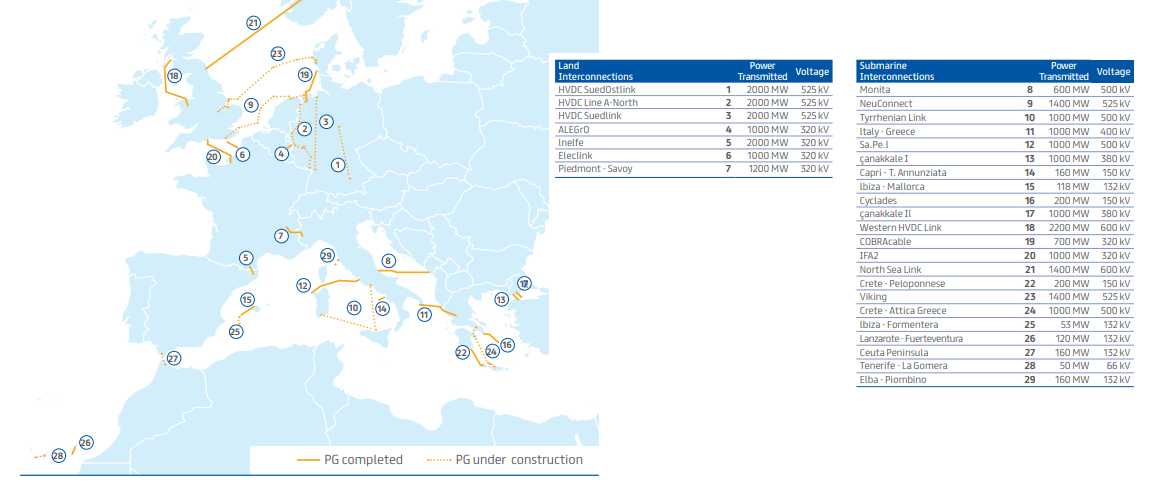

Prysmian (PRYMY) (PRYMF) is active in three divisions ( energy, projects and telecom ), of which the energy division is by far the most important as it represents almost 75% of the total revenue (but generating the lowest margins with an EBITDA margin of just 8.1% in 2022 ). Prysmian is one of the specialists to connect offshore wind farms to existing power grids and to connect cities and countries with submarine cables for telecommunications. As more submarine powerlines are under construction in Europe, Prysmian should be able to benefit as well as a leader in the sector.

{kind=link}

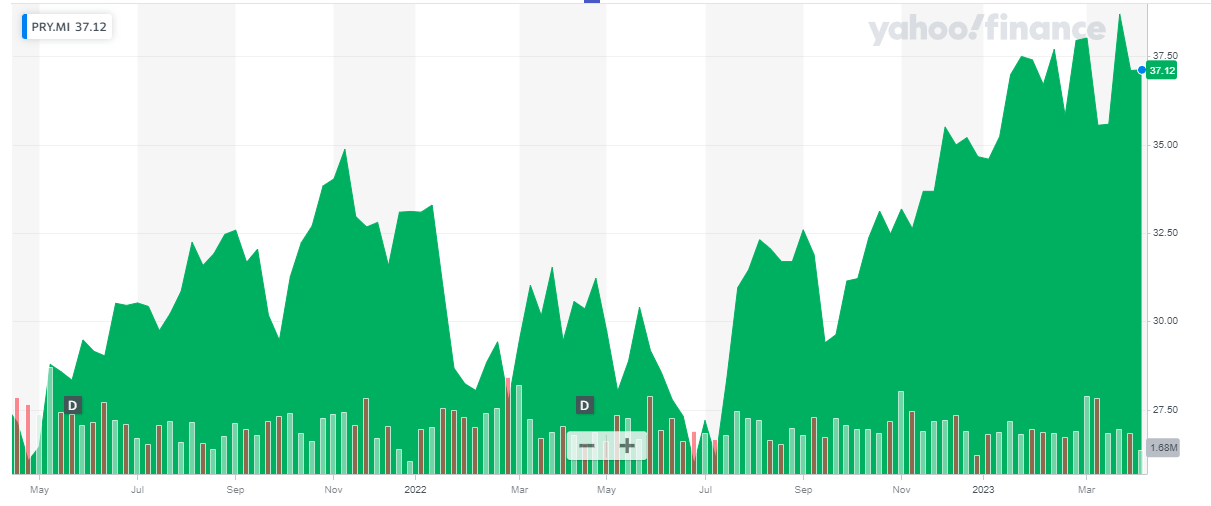

Prysmian has its primary listing in Italy where it's trading on the Milan Stock Exchange with PRY as its ticker symbol. The average daily volume in Italy is approximately 700,000 shares per day. Investors should clearly try to use the company's primary listing to trade in its shares. Prysmian currently has approximately 264M shares outstanding (this has been pretty stable over the past few years) and the current market capitalization is approximately 9.8B EUR.

{kind=link}

2022 was a satisfying year

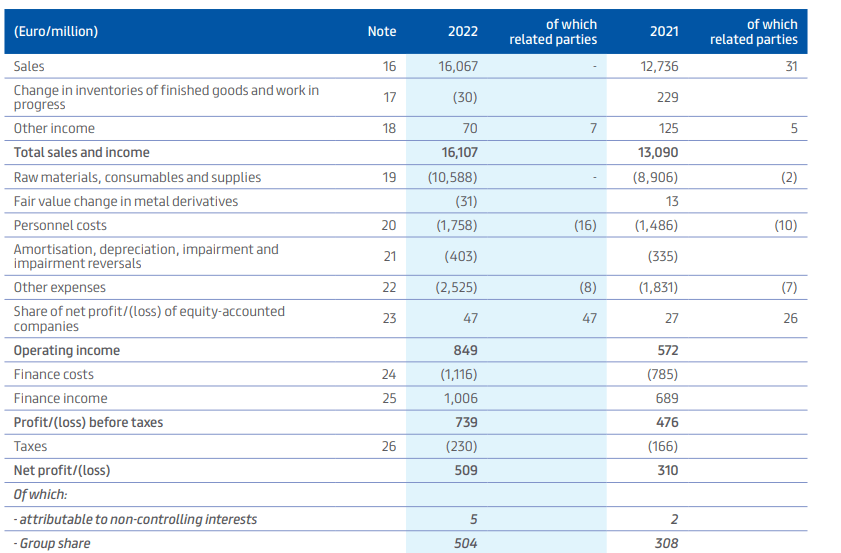

As expected, Prysmian was able to report a substantial revenue boost as it saw its total revenue increase from 13.1B EUR in 2021 to 16.1B EUR in 2022 . And although the other expenses also increased, the company's operating income jumped by almost 50% to 849M EUR.

{kind=link}

That's despite seeing the "other expenses" increase by over a third (these other expenses include maintenance expenses, utilities, project execution-related items and the provision for risks). Thanks to Prysmian's strong balance sheet and its preference to have fixed rate debt, the net finance expenses (including FX changes) came in at just 110M EUR resulting in a pre-tax income of 739M EUR and a net income of 509M EUR of which 504M EUR was attributable to the shareholders of Prysmian. Based on the current share count of approximately 264M shares, the EPS came in at 1.91 EUR which is a 63% increase compared to the EPS reported in 2021. A very strong improvement indeed.

But as I explained in my 2021 article , I was mainly interested in Prysmian from a cash flow perspective.

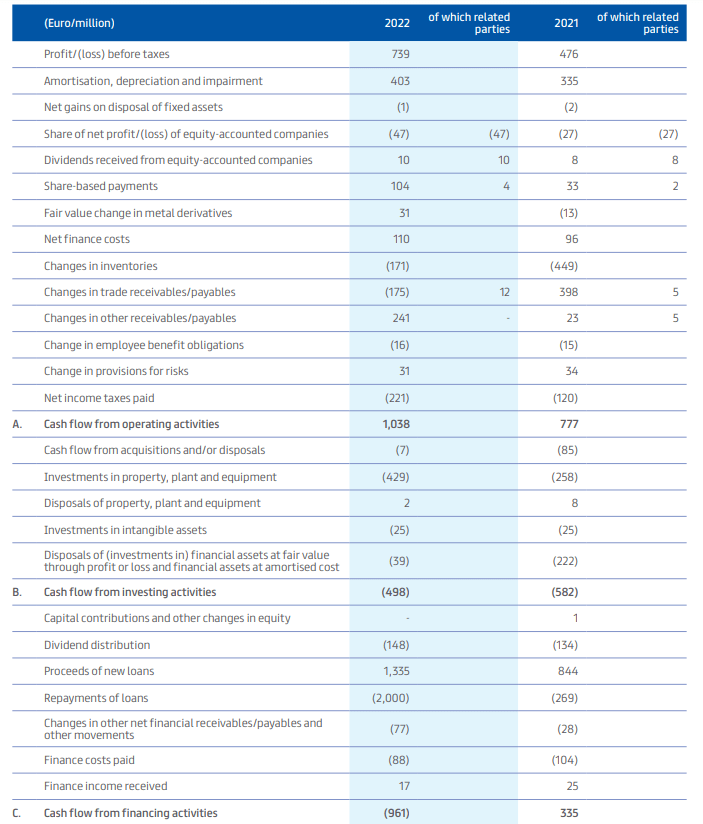

The reported operating cash flow in 2022 was 1.04B EUR but this includes a net investment in the working capital position of approximately 121M EUR compared to just 43M EUR in 2021. This means the adjusted operating cash flow was approximately 1.16B EU compared to approximately 820M EUR in 2021.

{kind=link}

We see the total capex was 454M EUR, including the 25M EUR spent on intangible assets. This means the underlying free cash flow result was approximately 610M EUR or 2.31 EUR per share after also deducting the 88M EUR in interest payments (which were recorded as a financing cash flow). That's a solid result despite seeing the total capex increase pretty dramatically from 283M EUR to 454M EUR. The 454M EUR spent in 2022 by Prysmian also exceeds the depreciation and amortization expenses which came in at 403M EUR.

The capex will likely remain relatively high in the next three years as Prysmian is guiding for an average capex level of 500M EUR per year in the 2023-2025 period . This will include investments in growth and capacity expansion as the company is building a new cable plant in the USA and has a new cable-laying vessel on order as well (this vessel will be delivered in 2025). This further strengthens the thesis that the sustaining capex is lower than the depreciation and amortization expenses while it should definitely be lower than the 454M EUR spent in 2022 (which included a 41M EUR deposit for the new vessel) and the average capex of 500M EUR over the next three years.

For this year, Prysmian expects to generate an EBITDA of 1.45B EUR which would be a relatively stable result compared to last year. The full-year free cash flow will come in around 500M EUR (the official range is 450-550M EUR) and Prysmian's free cash flow calculation includes working capital changes as well as the growth investments so the underlying sustaining capex will likely be lower than the 500M EUR the company is guiding for. Considering the EBITDA will remain pretty stable, I see no reason why we wouldn't be able to see a 600M EUR free cash flow on an underlying basis and likely closer to 700-725M EUR excluding growth capex.

{kind=link}

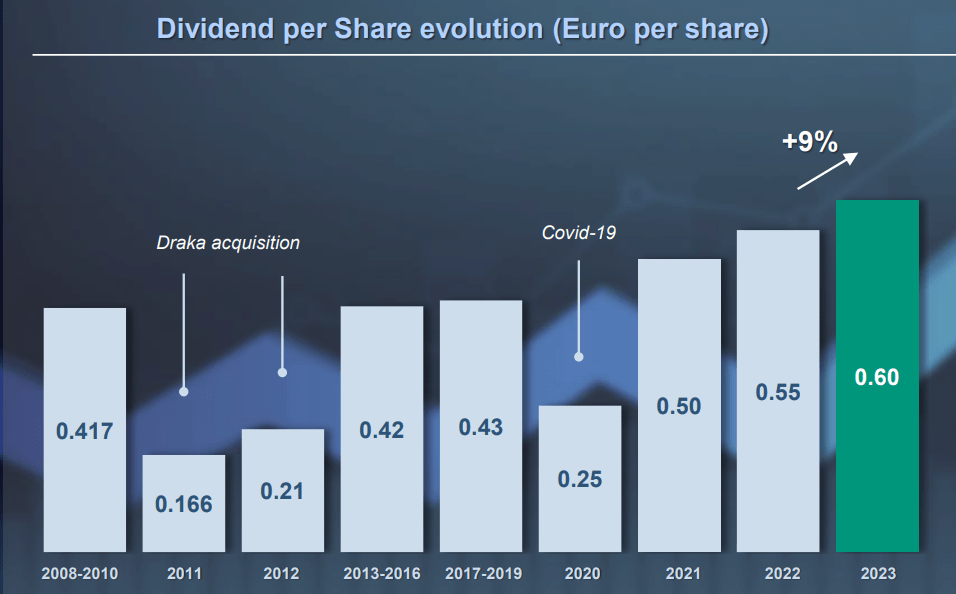

Prysmian will pay a dividend of 0.60 EUR per share based on its 2022 results, resulting in a cash outflow of just under 160M EUR. The anticipated ex-dividend date is April 23, and the dividend will be payable from April 25 onward.

{kind=link}

Investment thesis

Trading at an EV/EBITDA multiple of less than 8 (and decreasing as Prysmian should be able to continuously increase its EBITDA), Prysmian still isn't expensive. The company's operating cash flow will be sufficient to cover the growth capex, and the dividend and to reduce the net debt. In 2023 and 2024, the company will have to repay or refinance 200M EUR and 460M EUR of debt and it could easily do this using the current cash position of 1.5B EUR and/or the existing 1B EUR credit facility (which also will have to be extended).

I lost track of Prysmian and that's the sole reason why I currently don't have a long position. I may consider writing some out of the money put options as for instance the P34 for September currently has an option premium of 1.50 EUR which would allow me to either pick up the stock at around 7 times EBITDA or retain the option premium in case Prysmian's share price doesn't drop below the 34 EUR level. And any weakness in the company's share price could be an opportunity to pick up stock.

For further details see:

Prysmian: A Leader In Submarine Cables At Just 8x EBITDA