PRYMF - Prysmian: Positive Megatrends And Supportive Capital Allocation Priorities

2023-10-24 09:23:30 ET

Summary

- The company is set to capitalize on its long-term investment and seize new opportunities within the industry.

- Prysmian is a well-run company with a supportive track record and aims to increase DPS by double digits by 2027.

- The company sold out its self-funded higher production capacity. Margins recovery post Russia-Ukraine conflict and a new reporting to understand the current megatrends better. Prysmian is a clear buy.

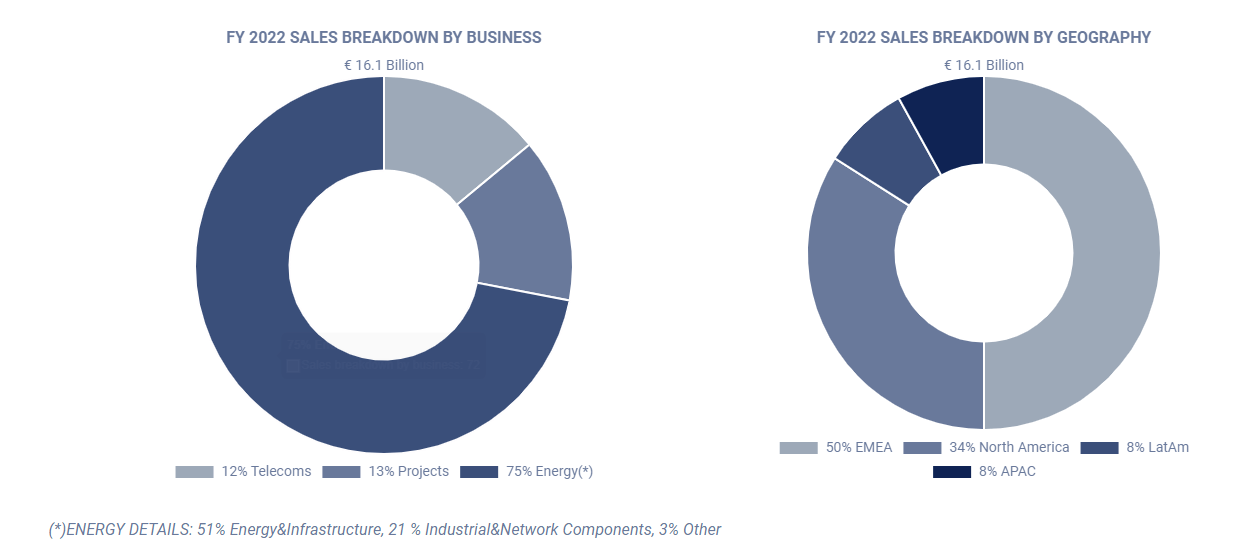

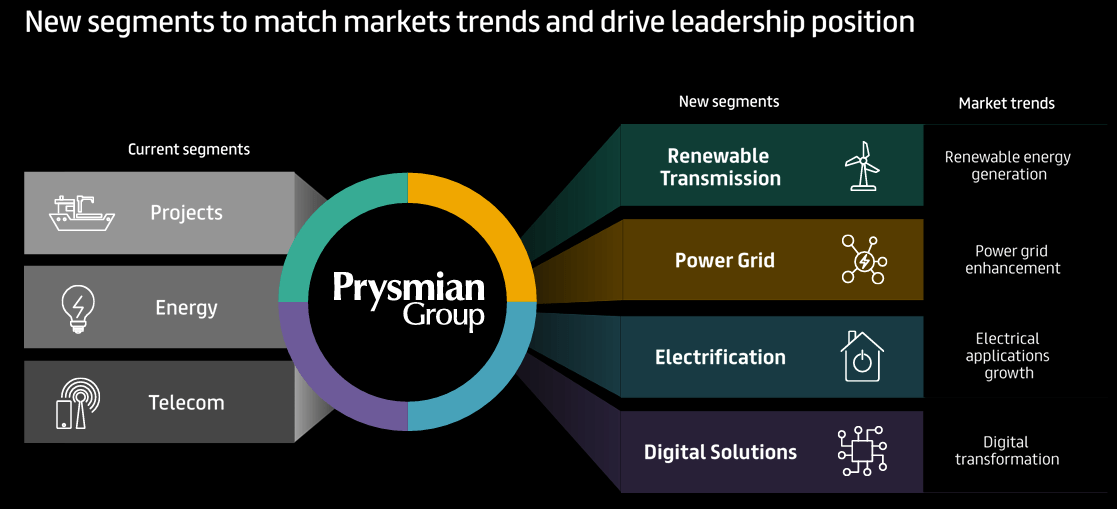

Following our detailed Eni analysis with a decade of underinvestment in oil investment and Saipem follow-up notes , today we look at Prysmian S.p.A. (PRYMF). The company is an Italian corporation active in developing, producing, and installing cables. Even if it is a well-known sector within our team, this is our initiation of coverage, so we report that Prysmian's business activities were divided into three segments (Fig 1): Energy (including oil), Projects, and Telecom. The Energy division includes infrastructure comprised of power transmission systems and cables with submarine distribution systems. Regarding the telecom division, we see cable and connectivity products used in networks, including optical and fiber cables. Following the release of the Capital Market Day presentation, Prysmian will now report on four new segments (Fig 2): Renewable Transmission, Power Grid, Electrification, and Digital Solutions. Here at the Lab, we have good coverage within the business, and in the EU area, we cover Enel , Iberdrola , E-ON , Snam , Enagas , Red Eletrica , and Schneider Electric . Prysmian is a diversified business focused on EU sales. All the above-listed companies have essential CAPEX requirements to decarbonize the EU and drive the energy transition. The cable industry is a strategic asset with key long-term trends to ensure independence and sustainability.

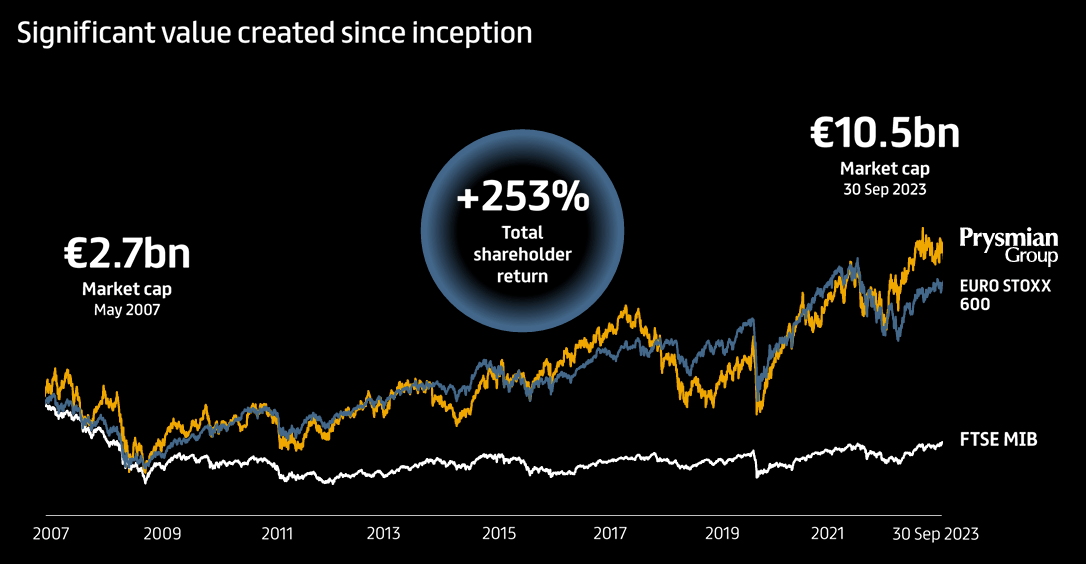

Higher renewable energy generation, growing electricity demand supported by population growth, technological advancement, and a more efficient power grid are upsides that cannot go unnoticed. With this vital backdrop, Prysmian could lead the sector thanks to 1) a solid balance sheet that supports organic and inorganic growth, 2) technological innovation to support its leadership position, 3) a higher dividend per share in the forecasted visible period, and 4) a strong management team with a solid track record (Fig 3). Here at the Lab, we have a positive macro view after the Russia-Ukraine conflict; indeed, 65% of the company's sales are from the markets that might boost growth. In addition, construction is not a sector that drives Prysmian performance and is also the business with the lowest EBITDA margin in the portfolio.

{kind=link}

Source: Prysmian corporate website - Fig 1

Prysmian new reporting segment

{kind=link}

Source: Prysmian Capital Market Day presentation - Fig 2

{kind=link}

Fig 3

CMD Update

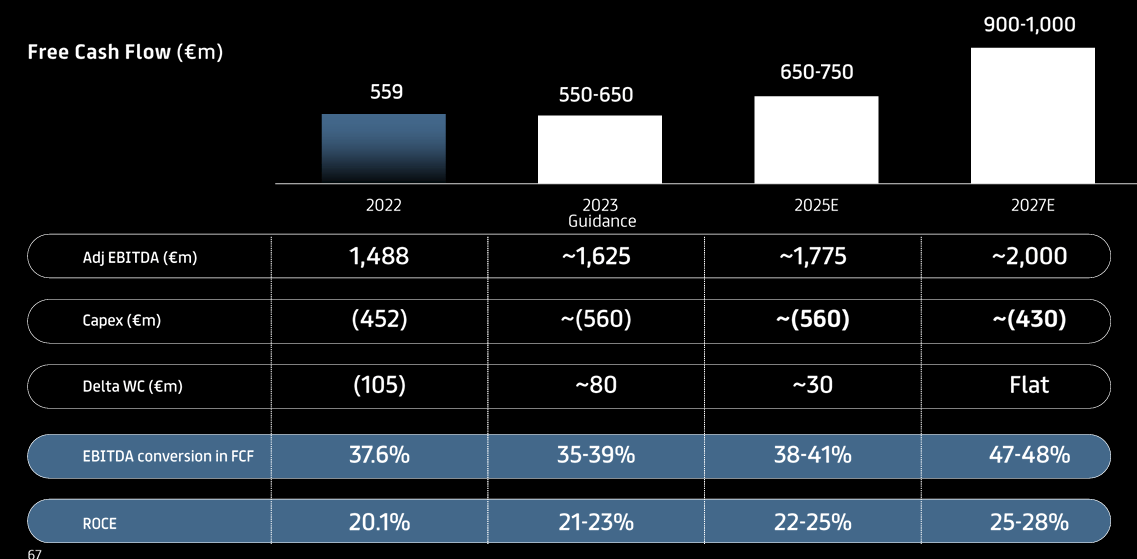

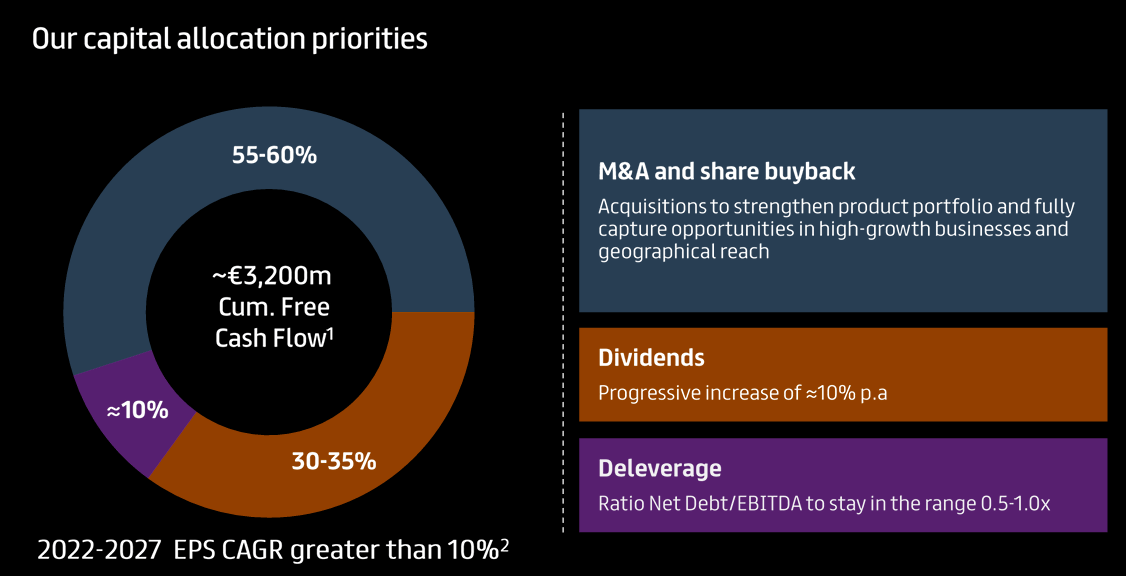

Looking at the CDM numbers, Prysmian lifts the veil on its 2027 strategy and, as anticipated, divides the business into four areas to be able to better capitalize on the current megatrends and improve the financial visibility of its cyclical businesses. This choice will allow Prysmian to invest more - approximately €2.7 billion - and increase margins, from €1.49 billion achieved in 2022 to an adjusted EBITDA target of €2 billion in 2027 (Fig 4). The plan will increase the coupon from €0.6 per share in 2022 with an expected total DPS hike of 10% annually from 2024 to 2027 (Fig 5). During the presentation, the order book reached €20 billion, of which €9.7 billion in backlog and €10.3 billion in orders with a strong commitment.

{kind=link}

Fig 4

The new strategy envisages a selective acceleration of investments to meet growing demand, particularly in the Renewable Transmission and Power Grid segments. In 2023-2027, investments will grow 1.7 times compared to the previous five years. According to the management team, free cash flow will also increase, reaching between €900 million and €1 billion in 2027, i.e., almost double the €559 million recorded in 2022. The ROCE (return on invested capital) is expected to increase to 25-28 % in 2027, confirming the high returns on expected strategic investments.

{kind=link}

Fig 5

Our Take

Prysmian management provided many details about the segment and related sub-sectors. We believe the company is moving on with a conservative plan, particularly looking at the Power Grid and Renewable Transmission growth rate. On the downside scenario, the CEO confirmed that there is no material impact from lower investment in the offshore wind market, and the Prysmian high voltage business is entirely capped by 2027. In detail, from the Q&A call, we understood that only 10% of the sub-sea cable market is linked to offshore wind, and the company's order backlog is estimated at €400 million vs a total commission of almost €20 billion. Q3 results are expected in mid-November, and we anticipate a solid performance. In our analysis, we forecast an adjusted EBITDA margin of €390 million with a 9.6% margin compared to the results of €432 million one year ago. Looking at the FCF, we expect a breakeven position with a rebound in Q4, in line with the Prysmian historical average. We are aligned with the company's guidance with an ad on the yearly guidance. EBITDA of €1.62 billion and an FCF between €550 and €650 million.

According to our estimates and backed by management comments, Prysmian appears to be signaling that short-cycle prices are normalizing, and any decline should be temporary thanks to structural growth. Even if our long-term targets are well set, we have more skepticism for 2024. No detailed objectives for 2024 have been released, which could represent an element of concern for the Wall Street sell-side and current investors. In the context of the recent economic slowdown, we expect that 2024 will be mainly a transition year, keeping the equity story intact. For 2024, we believe that the group will maintain an adj. EBITDA of €1.65 billion, while the consensus points to a slight decline. Any further comments from management on this front could support market confidence. On the EBITDA level, we support Prysmian EBITDA thanks to expected synergies. The company has a diversified portfolio and a clear advantage of being a ' One Stop Shop ' cable corporation. US distributors favor single suppliers, and Prysmian might scale its advantage in large infrastructure projects. Looking at the EU, Prysmian clients are within our coverage, and Renewable Transmission companies are the same as Power Grid. On the R&D level, we understood that there is a shared platform which leads to increasing operating leverage. In our new estimates, Prysmian adj. EBITDA margin is above 10%, and looking down to the P&L, management estimates D&A rising to €470 million levels in 2027 vs. €387 million reported last year.

Conclusion and Valuation

Given the order backlog, the company entirely sold out its planned higher capacity through 2027. Even if we expect a lower EBITDA margin, the company recover from 2022 levels, which were impacted by higher inflation. Regionally, we see support from margin in the future with opportunity in the US compared to Europe, thanks to scale, infrastructure aging, and less fragmentation. Prysmian's history of long-term value creation cannot go unnoticed. The company is positioning itself as one of the primary beneficiaries of the energy transition, and the digitalization process and other secular growth trends combined with still undemanding valuations reinforce our positive view of the stock. A diversified product portfolio also allows the company to hedge against the cyclicality of geographies and businesses. Looking at the valuation, we decided to use a 2025 EV/EBIT of 11x to account for CAPEX (D&A) growth. In our estimates, we arrive at an adj. EBIT of €1.1, €1.08, and €1.2 billion in 2023, 2024, and 2025 respectively. Our 2023 net debt, given the solid FCF, is estimated at €1.2 billion. Our EV/EBIT multiple is based on a reverse discount cash flow considering capital and tax rate costs. The multiple implies an FCF yield of 5% despite the growth capex plan and fully covering the ongoing hike in DPS. In numbers, we initiate coverage with a buy rating of €40 per share ($19 in ADR). Downside risks included in our target price are project delays, compliance (the industry was accused of cartels in the past), execution risks, higher comps from Chinese producers, and metal commodity price volatility, particularly copper and aluminum.

For further details see:

Prysmian: Positive Megatrends And Supportive Capital Allocation Priorities