PFF - PTA: Some Improvements But Shares Are Not As Attractively Priced

2023-12-04 22:00:00 ET

Summary

- Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has an 8.65% current yield, but other fixed-income closed-end funds offer higher yields.

- The fund's shares have outperformed the fund's portfolio in recent months, but it is still trading at a discount.

- The fund failed to cover its distribution in the most recent reporting period, but it appears to be overcoming this problem lately.

- The fund appears to have increased its allocation to bonds at the expense of preferred stocks, which may not be the best idea.

- The fund's discount is much smaller than it was a few months ago.

The Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund ( PTA ) is a closed-end fund that investors can employ in order to generate a high level of income from the assets in their portfolios. The fund has an 8.65% current yield, so it certainly does this job reasonably well, although this yield is nowhere near as attractive as some other fixed-income closed-end funds are able to offer. We can see that here:

| Fund |

| Current Yield |

| Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund |

| 8.65% |

| John Hancock Preferred Income Fund ( HPI ) |

| 9.74% |

| First Trust Intermediate Duration Preferred & Income Fund ( FPF ) |

| 10.33% |

| John Hancock Preferred Income Fund II ( HPF ) |

| 9.56% |

| John Hancock Preferred Income Fund III ( HPS ) |

| 9.84% |

With that said, there are several other preferred stock funds with yields in the 6% to 8% range, which seems strange even with long-term interest rates coming down. After all, bonds are generally considered to be less risky assets than preferred stocks, so they should have higher yields The iShares Preferred and Income Securities ETF ( PFF ) does have higher yields than the Bloomberg U.S. Aggregate Bond Index ETF ( AGG ) so it does seem to be the case that preferred stocks generally have higher yields. The fact that bond funds are yielding above 11% right now makes it very difficult to make the case for any preferred stock fund to income-focused investors right now.

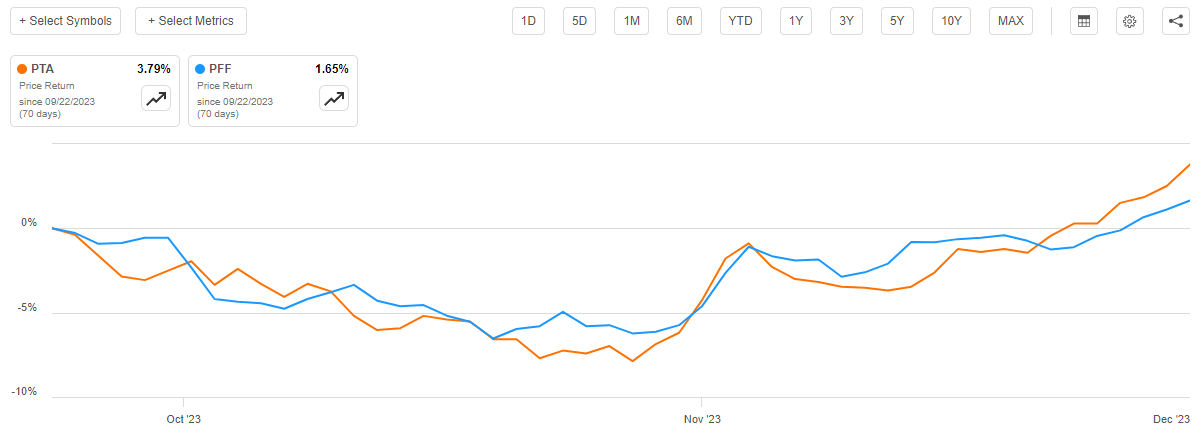

As regular readers can no doubt recall, we last discussed the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund around the end of September. As has been the case with many leveraged fixed-income funds, this one has seen its price increase significantly over the past month or so as the market has started to price in a fairly large interest rate cut next year:

{kind=link}

As we can clearly see, the fund’s shares are up 3.79% since September 22, 2023 (the date that my prior article on this fund was published). This is significantly more than the 1.65% gain of the iShares Preferred and Income Securities ETF, which claims to track the price of preferred stocks throughout the domestic market. This gain was well above the 1.46% that the fund’s net asset value increased over the same period though, which could suggest that the shares of this fund have gotten ahead of themselves. As such, we will want to take a close look at this fund’s current valuation before purchasing shares of it.

About The Fund

According to the fund’s website , the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has the primary objective of providing its investors with a high level of current income. The fund also has a secondary objective of capital appreciation. For the most part, this objective makes a great deal of sense since this fund is investing its assets in preferred stocks and bonds. As we can see here, 56.51% of the fund’s assets are invested in preferred stock, 37.34% of its assets are invested in corporate bonds, and 5.59% of the fund’s assets are invested in convertible bonds:

CEF Connect

As I pointed out in my previous article on this fund, both preferred stocks and bonds are by their nature income vehicles:

The fund’s objective of providing its investors with a high level of current income makes a great deal of sense when we consider this. After all, that is how both preferred stock and bonds deliver their returns. In both cases, there are no net capital gains because neither type of security has any inherent link with the growth and prosperity of the underlying company. A company will not increase the amount that it pays its creditors just because its profits go up. In the case of both bonds and preferred stock, the securities are issued and redeemed at face value so there will be no capital gains for an investor who holds over their entire lifetime. With that said, preferred stock normally does not have a maturity date so in some cases that lifetime can be forever. In such cases, the only way for the investor to recover their money is to sell the security.

While the prices of both preferred stocks and bonds will fluctuate with interest rates, there are no net capital gains over their lifetimes. There are also limits to how far interest rates can decline, so there is a limit as to how valuable these securities can become. As such, the generation of current income certainly makes a great deal of sense for a fund like this.

The presence of the large allocation to convertible securities does add an interesting twist, however. As these securities can be converted into shares of common stock, the potential capital gains here can be quite high. This is especially true when we consider that convertible securities are frequently issued by start-ups or financially distressed companies, the potential capital gains can be quite high if the company recovers or becomes a home-run stock. For example, Tesla ( TSLA ) issued some of these securities when it was in its early days. Obviously, investors who purchased those convertibles are happy with their purchase. The presence of these securities in the fund’s portfolio contributes to the secondary objective of providing capital appreciation, since we cannot really expect much appreciation from the bonds or the preferred stock.

One thing that we noticed is that the fund’s asset allocation has changed somewhat since the last time that we discussed it. In particular, the fund’s allocation to both bonds and convertible securities has increased and the allocation to preferred stock has gone down over the same period:

| Asset Type |

| Previous Allocation |

| Current Allocation |

| Preferred Stock |

| 57.21% |

| 56.51% |

| Bonds |

| 36.81% |

| 37.34% |

| Convertible Securities |

| 4.74% |

| 5.59% |

The fund’s annual turnover is 41.00%, which is higher than most other fixed-income funds so that could explain some of the changes here. Indeed, it almost certainly explains the changes. The asset allocation chart from the previous article was dated June 30, 2023. The chart shown above is dated September 30, 2023. Over that period, preferred stock actually outperformed bonds:

{kind=link}

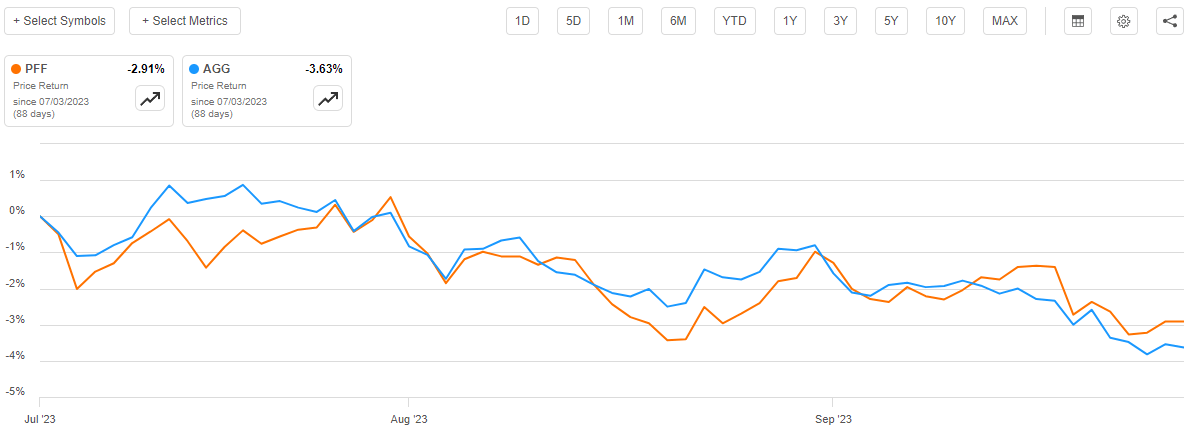

As such, if the fund had simply kept its asset allocations static, the preferred stock weighting would have increased relative to bonds. However, we see the exact opposite. As such, it appears that the fund actively increased its weighting to bonds during the third quarter. This makes sense since bonds should outperform preferred stocks when interest rates are increasing. This comes from the fact that bonds usually have a lower duration. I discussed this in a few previous articles. However, that is clearly not what we saw in the third quarter of this year, which is somewhat difficult to explain unless preferred stocks were benefiting from the same investor desire to lock in high yields on their money over the long term that benefited junk bonds during that period. Regardless, we can see that the fund’s managers apparently believe that bonds will outperform preferred stock going forward as that is the only reason to increase this fund’s allocation to bonds.

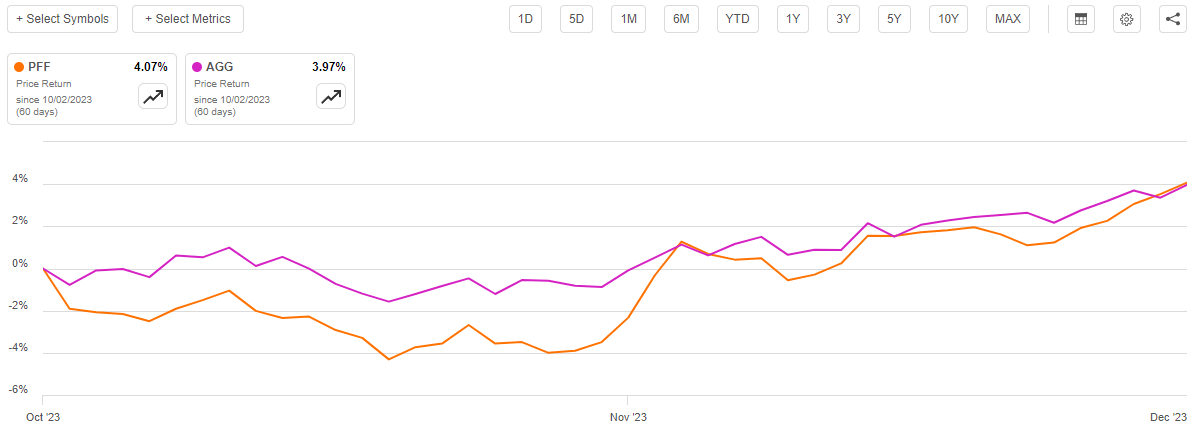

Unfortunately, that has not been the case recently. As we can see here, preferred stock has outperformed bonds since October 1, 2023:

{kind=link}

This is exactly what we would expect during a period of falling long-term interest rates. Once again, this is due to preferred stocks typically having a higher duration than bonds. Thus, it appears that the fund may have done exactly the wrong thing (although the decision to shift assets from preferred stock to bonds did make sense while interest rates were rising).

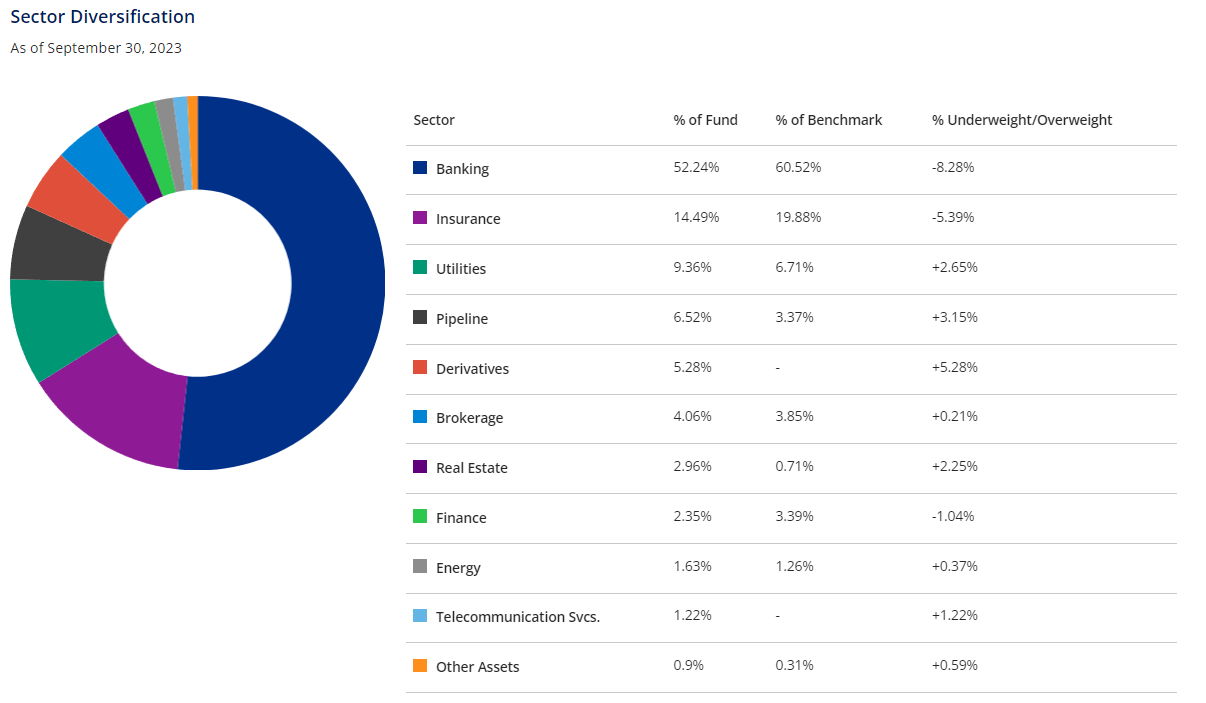

In the previous article on this fund, we saw that the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund was heavily invested in securities issued by banks and other financial institutions. This continues to be the case, as 52.24% of the fund’s assets are currently invested in the banking sector:

{kind=link}

This is not at all unusual for a preferred stock fund. As I pointed out previously:

In short, banks are required to back a certain percentage of their assets with Tier one capital. Tier one capital refers to that capital held by a bank that is the bank’s own money and not money that is a liability to somebody else, such as a depositor. There are two ways for a bank to increase its Tier one capital, which it is required to do if it takes on more deposits or regulations change. Its options to do this are issuing either common stock or preferred stock and most banks will opt to issue preferred stock in order to avoid diluting the common stockholders too much.

The fund’s allocation to the banking sector has increased somewhat since we last discussed it. Previously, the fund had 51.64% of its assets invested in this sector but today that is 52.24%. This is something that might be concerning to those investors who are somewhat risk-averse. After all, right now the banking sector is sitting on $684 billion of unrealized losses:

Zero Hedge/Data from FDIC

This is due to the rapid increase in interest rates that has taken place over the past two years. This pushed down long-dated bond and fixed-rate loan prices, which comprise a significant portion of most banks’ assets. However, as of right now, these losses are unrealized, and they may never be fully realized. After all, unless an event such as a bank run occurs, the bank will probably not be forced to sell its assets at fire sale prices in order to meet withdrawal demands. As long as confidence in the system remains, everything should be fine. The Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund is underweight bank preferred securities relative to its benchmark index too, so even in a worst-case scenario, this fund could be better positioned than its peers that have higher weightings to that sector.

Leverage

As is the case with many fixed-income closed-end funds, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund employs leverage as a method of boosting the effective yield of its portfolio. I explained how this works in my previous article:

In short, the fund borrows money and then uses this borrowed money to purchase preferred stock, bonds, and income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has leveraged assets comprising 38.99% of its assets. This is less than the 39.11% leverage ratio that the fund had the last time that we discussed it, which is certainly good to see. As we saw earlier, the fund’s net asset value has increased a bit over the past two months, which is the primary reason for this improvement. The fund is still above the one-third level that I would really like to see, but it is trending in the right direction and fixed-income funds can sustain a higher level of leverage than a common stock fund due to the less volatile nature of its assets. Overall, we probably do not need to worry too much about this fund’s leverage right now.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund is to provide its investors with a very high level of current income. In pursuance of this objective, the fund invests in a portfolio consisting of preferred stock, bonds, and other income-producing assets. These assets primarily deliver their total investment return in the form of direct payments to their investors, and in today’s environment, the yields on these securities tend to be quite respectable. The fund collects all the money that it receives from these securities and even borrows money to receive income from more securities than it could otherwise control with just its net assets. The fund adds any capital gains that it manages to realize by exploiting interest rates to this pool of capital. It then pays all of this money out to investors via distributions, net of its own expenses. We can probably expect that these activities will allow the fund’s shares to boast a fairly high yield.

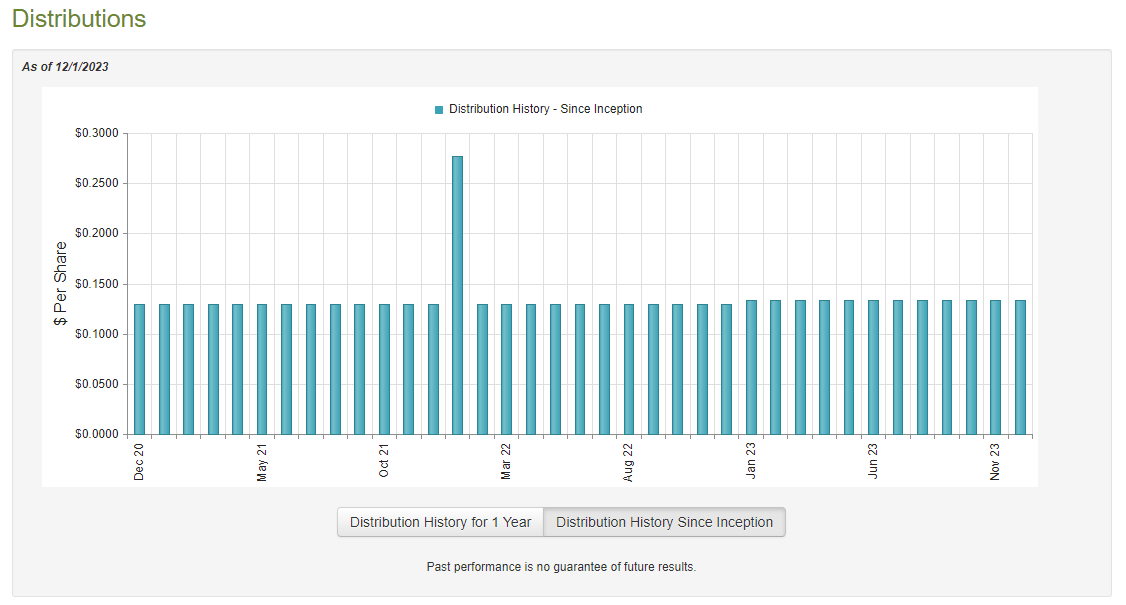

That is indeed the case. As of the time of writing, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund pays a monthly distribution of $0.1340 per share ($1.608 per share annually), which gives it an 8.65% yield at the current price. As mentioned earlier, this yield is not as attractive as it was a few years ago considering that it is not that difficult to find other fixed-income funds yielding well into the double-digits. This fund has been much more consistent with respect to its distribution than many of its peers, however. As we can see here, the fund increased the distribution in January and has never cut the payout:

{kind=link}

This is far better than the track record of most funds that are utilizing a similar strategy to this fund. Most fixed-income funds suffered severe asset declines in 2022 once the Federal Reserve started cutting interest rates and had to cut their payouts in order to avoid destroying their net asset values through the distributions. The fact that this one did not have to do that is curious, and it is something that we want to investigate further. It might be the case that the fund could not afford the distribution increase in January, but management increased it anyway to prop up the fund’s share price.

Unfortunately, we do not have an especially recent report that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. As such, this report will not provide any insight into the fund’s performance over the past seven months. This is quite disappointing, as the last seven months have certainly been interesting for a fund like this. In particular, the rising interest rate environment that existed from mid-July until mid-October almost certainly caused this fund to incur significant losses that will not be reflected in this report.

During the six-month period, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund received $35,471,692 in interest and $14,422,099 in dividends from the assets in its portfolio. This gives the fund a total investment income of $49,893,791 during the period. The fund paid its expenses out of this amount, which left it with $23,291,768 available for shareholders. Unfortunately, this was nowhere near enough to cover the fund’s distributions. Over the period, the fund paid out total distributions of $43,997,692. At first glance, this is almost certainly going to be concerning as we typically would like a fixed-income fund to be able to fully fund its distributions out of net investment income.

However, net investment income is not the only source from which a fund can derive the income that it needs to cover its distribution. The fund might have been able to realize some capital gains from either the convertible securities in the portfolio or fluctuations in interest rates over the period. Unfortunately, this fund failed miserably at this task during the period, as it reported net realized losses of $74,404,336 but these were partially offset by $37,693,105 net unrealized gains. Overall, the fund’s net assets declined by $57,417,135 during the period after accounting for all inflows and outflows. As has been the case with most fixed-income funds, this one failed to fully cover its distributions during the period.

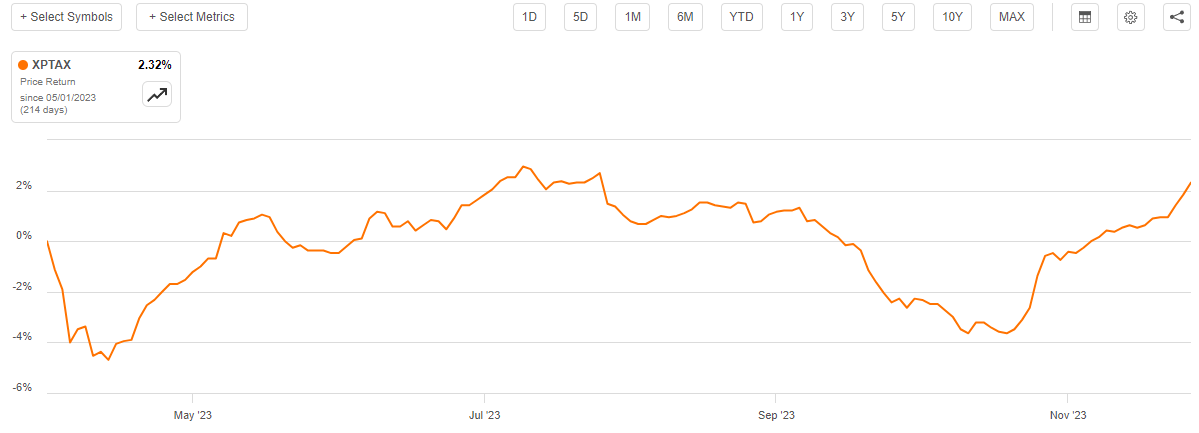

The fund does appear to have solved this problem since the time that the most recent report was released. As we can see here, the fund’s net asset value per share is up 2.32% since May 1, 2023:

{kind=link}

This suggests that the fund has been able to generate sufficient investment profits to cover its distribution over the past seven months. Obviously, it has been greatly helped by the recent optimism about the possibility of interest rate cuts in 2024. While it remains to be seen if the market is right about this, it is nice to see that this fund’s fortunes have reversed temporarily.

Valuation

As of November 30, 2023 (the most recent date for which data is currently available), the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has a net asset value of $19.33 per share but the fund’s shares currently trade for $18.60 each. That is a 3.78% discount on the net asset value at the current price. This is far worse than the 8.59% discount that the shares have averaged over the past month, so it may be possible to get a better price by sitting back and waiting a bit.

Conclusion

In conclusion, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has been delivering some fairly strong recent performance, but it appears that it has not been entirely justified. The fund’s shares have outperformed the portfolio for the past month or two, but fortunately, the fund is still trading at a discount. It has apparently reversed the problem of not being able to cover the distribution, at least temporarily, so there have been some real improvements here since the last time that we discussed the fund. However, given the relative uncertainty with respect to interest rates right now, it might be best to hedge your risk by holding some sort of floating-rate fund alongside a fund like this.

For further details see:

PTA: Some Improvements, But Shares Are Not As Attractively Priced