PTA - PTA: This 8.3% Yielding Preferred CEF Remains Our Favorite Sector Pick

Summary

- We refresh our previous constructive analysis of PTA in light of its recently issued shareholder report.

- PTA continues to benefit from a number of structural features unique to Cohen CEFs such as leverage resilience, low cost of leverage and modest duration.

- These factors are the primary drivers of the fund's strong performance since our last update.

- Apart from its strong performance, PTA is the only fund in the sector that has managed to raise its distribution in a difficult market environment.

- PTA remains our favorite pick in the sector, with LDP a potential rotation option during periods of discount convergence.

This article was first released to Systematic Income subscribers and free trials on Jan. 24 .

Preferred stocks remain key components of investor portfolios due to their high-quality, attractive yields and modest duration profile. In this article, we catch up on the Cohen and Steers Tax-Advantaged Preferred Securities and Income Fund (PTA) - a CEF we highlighted mid last year and one that remains our favorite preferreds CEF. The fund has recently issued a shareholder report that requires some parsing and we take this opportunity to update the analysis.

Our key takeaway is that the fund remains an attractive way to allocate to the preferred sector given the resilience of its leverage profile, modest duration, cheap valuation and low cost of leverage. These characteristics are not found in the funds of other issuers within the sector, which is why PTA offers a unique proposition in our view.

Fund Snapshot

PTA is one of three Cohen & Steers preferreds CEFs, all of which have a very similar profile.

PTA holds primarily financial preferreds, specifically Bank and Insurance stocks. This is not unusual as the sector is dominated by financial issuers with smaller pockets of energy, utilities and REITs issuers.

Cohen & Steers

PTA also has a relatively high quality allocation within the corporate credit space, with nearly 70% of stocks rated BB+ and above (BB+ being the highest non-investment-grade rating).

Cohen & Steers

Performance Review

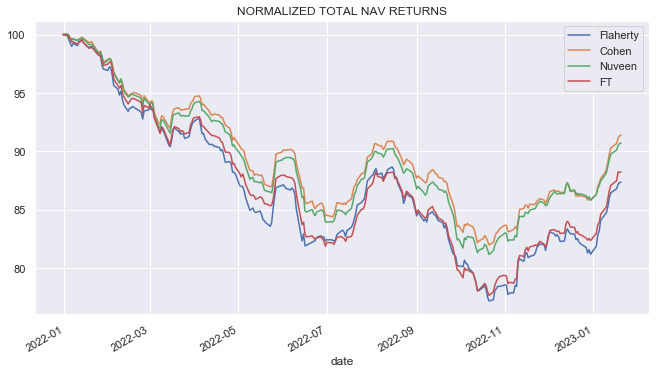

Since our previous recommendation of PTA in June of last year, the fund has performed well with the third highest return in the sector. The only funds that have outperformed it are ( JPI ) and ( LDP ).

Systematic Income

JPI is a Nuveen preferred CEF which is the only non-Cohen preferred CEF that we have held in our Income Portfolios. It's a fund that we like due to its term structure which provides both discount stability and a likely tailwind due to discount compression to zero in 2024. We don't expect the fund to terminate, but we do expect Nuveen to set up a tender offer where investors can tender shares back at NAV, which is what happened with another Nuveen preferred CEF ( JPT ), which has since turned into a perpetual CEF.

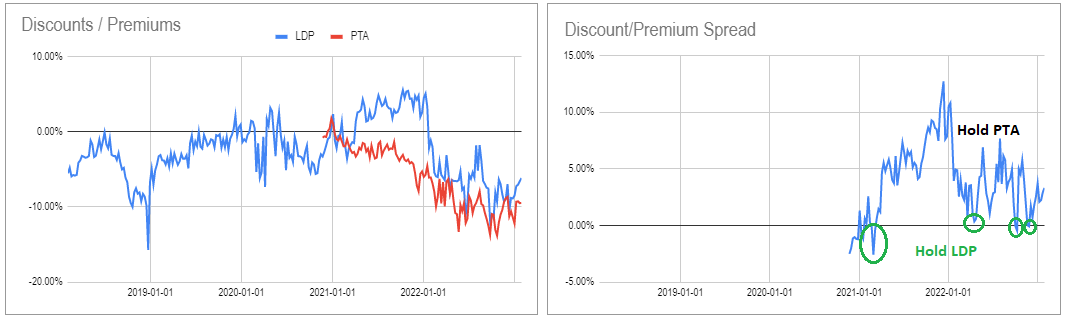

The best performer since our PTA analysis is LDP which is a Cohen & Steers sister fund of PTA that we have recommended a number of times as switch ideas for PTA. Specifically, when the discount differential between the two funds moves close to zero, we recommend rotating to LDP and when the discount differential moves back in favor of PTA, we recommend rotating back to PTA. The reason LDP tends not to trade at a wider discount than PTA has to do with its lower management fee.

{kind=link}

It's worth restating the key points behind our original PTA view and why they have allowed the fund to perform very well.

Cohen & Steers preferred CEFs like PTA as well as the Flaherty sector CEFs exhibit what we call leverage resilience . By leverage resilience, we mean that a given fund does not deleverage as quickly as other funds in the sector. Because fixed-income markets tend to be fairly mean-reverting (over varying timeframes), funds that deleverage more readily tend to lock in economic losses for investors, in effect, selling low and buying back high. This topic is one we documented a number of times in the preferreds sector. The short of it is that the Nuveen and First Trust funds tend to deleverage fairly quickly while the Flaherty and Cohen funds try to avoid deleveraging.

The main reason for this is simple - Nuveen and First Trust funds have leverage caps (38% and 40%, respectively) while Flaherty and Cohen funds don't. What tends to happen is that over a drawdown-and-reversal period, Nuveen and First Trust funds tend to lag as they deleverage (i.e. sell assets) on the way down and try to catch up (i.e. buy back) on the way up.

The second reason we like the Cohen funds here is due to their hedging profile . Specifically, the Cohen along with Nuveen funds partially hedge their duration (i.e. interest rate sensitivity) and partially hedge leverage costs (a pay-fixed interest rate swap does both at the same time). This relatively modest duration profile of Cohen and Nuveen funds in relation to Flaherty funds has allowed Cohen funds to outperform last year.

{kind=link}

And the reason a partial hedge of leverage costs is so important is because funds without hedges in place such as the Flaherty funds are paying around 5.5% on their leverage facilities, meaning that, after management fees, they are not actually earning much income on their leveraged assets (leveraged assets make up around a third of total fund assets). By contrast, PTA is paying closer to 2% on its leverage rather than the 5.5%, allowing it to generate more income for investors.

Overall, the way we would summarize this section is to say that Flaherty and Cohen funds give you leverage resilience while Nuveen and Cohen funds give you leverage cost hedging. In short, only the Cohen funds give you leverage resilience and leverage cost hedging. This is why the Cohen funds remain attractive holdings in the sector.

Income Review

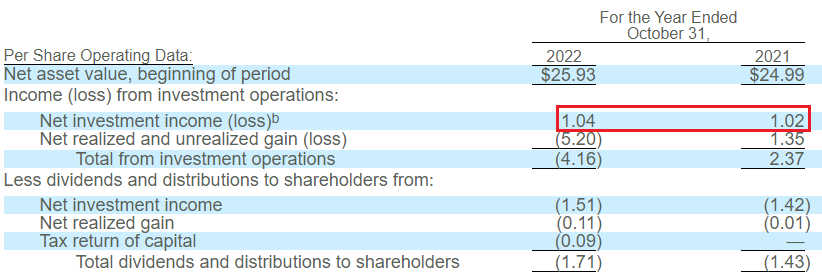

An important metric we like to check is how the fund's net investment income looks over time. A quick glance at the recently released shareholder report shows that its annual net income increased slightly from $1.02 to $1.04.

{kind=link}

On first glance, this looks fantastic since net income of most credit CEFs has gotten crushed in the last year, under pressure from rising short-term rates and the knock-on impact of higher leverage costs.

However, we also know that the fund has mostly fixed-rate assets and floating-rate liabilities and that short-term rates have increased sharply over 2021, which should have compressed net income for 2021 over 2020 (recall that the leverage cost hedge does not cover 100% of the credit facility). A rise in net income for a preferred CEF in a period of rising short-term rates just doesn't pass the smell test. So what is going on here?

One answer is that the fund did not actually fully leverage up until 2021, meaning its 2020 net income numbers are very understated. For instance, as of Oct-2020, it had 21% of leverage which rose to 32% by Apr-21 and would continue to climb from there towards the high 30s.

The other reason that we shouldn't only look at annual numbers is because more granular semi-annual numbers are available. And if we do that, we see that PTA generated $0.56 in net income for 6 months ending in April-22 and $1.04 for 12 months ending in Oct-22. This implies net income of $0.48 for the most recent semi-annual period from Apr-Oct 22.

In other words, instead of focusing on an annual rise in net income from $1.02 to $1.04, what we saw was a drop in net income from $0.56 to $0.48, if we look at semi-annual rather than annual periods. This makes a lot more sense and ties in with our intuition that a fund like PTA should not be seeing an increase in net income in a period of rising short-term rates and if we do see a rise in net income, we need to dig a little deeper to see what's really going on. The drop in net income over the most recent semi-annual period is not a big deal because of two key factors. One, Cohen funds have hedged around 85% of their leverage cost at a favourable rate and PTA has done this out to 2027. And two, because interest rate swaps are off-balance sheet instruments, they don't make it into GAAP net income figures. A final reason to be fairly upbeat about the fund is that it hasn't changed its borrowings over 2022 unlike a number of other funds in the sector and this has supported its net income. So net net the fund's net income has fallen but it has fallen much less than we see in the semi-annual periods.

It's also important to highlight that PTA is the only fund in the sector that has managed a rise in its distribution. This is in the context of significant cuts in the rest of the sector (John Hancock funds have not made distribution cuts however their coverage remains around 90%). This unexpected rise has to do with the fact that PTA was under-distributing relative to its Cohen sister funds (a quick check of the NAV distribution rate prior to the raise shows this) as well as the fact that its leverage was slightly higher and its leverage cost was slightly lower - two additional factors that supported a higher level of net income despite a somewhat higher management fee. Apart from these intra-Cohen factors, low cost of leverage and leverage resilience relative to the rest of the sector, as discussed above, were other key factors that allowed the fund to make this distribution raise.

Takeaways

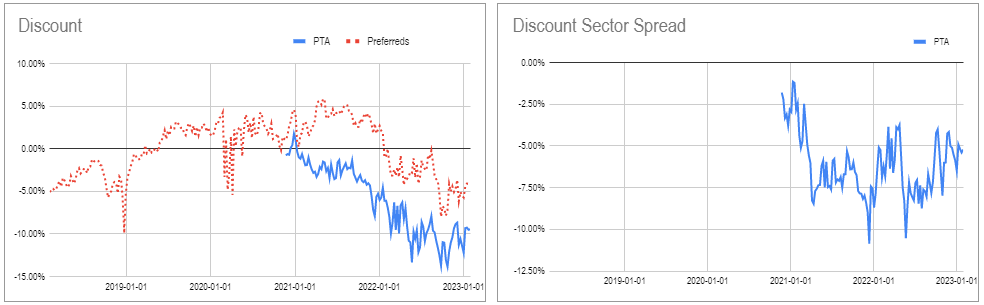

PTA remains our favorite pick in the preferreds CEF sector (with JPI a good lower-beta option and LDP as a potential rotation option for PTA holders). PTA benefits from a number of key structural features which have allowed it to perform relatively well since the start of the drawdown in 2022. Currently, the fund enjoys an unusually low level of leverage cost for credit funds due to its hedges. This, plus its attractive valuation with the discount at near 10% (about 5% wider of the sector average as shown in the second chart), makes it a good choice in the sector going forward as well.

{kind=link}

For further details see:

PTA: This 8.3% Yielding Preferred CEF Remains Our Favorite Sector Pick