PDO - PTY: 100 Big-Yield CEFs These 4 Worth Considering

Summary

- PIMCO's Corporate & Income Opportunity Fund is hot.

- We share comparative data on over 100 big-yield CEFs, including performance, yield, strategy, discount versus premium, z-scores and more.

- We review four big-yield CEFs from the list (two that may be overheating and two that are particularly attractive), and with a special focus on PTY.

- We conclude with more big-yield CEF ideas for you to consider.

In this report we share updated data on over 100 big-yield CEFs, and then review four of them that are worth considering, including two popular CEFs that may be starting to overheat and two alternatives that are particularly compelling. We have a special focus on PIMCO's popular Corporate & Income Opportunity Fund ( PTY ), so we will dive into the details on that one (right after sharing valuable data on the 100+ big-yield CEFs). After reviewing four CEFs in total, we conclude with our very strong opinion on investing in select CEFs (especially PTY), plus a few more compelling big-yielders worth considering.

100+ Big-Yield CEFs:

Before getting into specific ideas, let’s start with some data (see below). This data is sorted by CEF style (“Strategy”) and then by market cap, and includes lots of additional valuable data points (including yield, recent performance, price discount or premium versus net asset value, 3-month and 1-year z-scores (a comparison of the price discount or premium versus recent history—lower is generally considered better) and more).

data as of Fri 1/27/23 (CEF Connect and StockRover)

data as of Fri 1/27/23 (CEF Connect and StockRover)

data as of Fri 1/27/23 (CEF Connect and StockRover)

data as of Fri 1/27/23 (CEF Connect and StockRover)

Please note: a downloadable (and sortable) spreadsheet of the above table is available to members.

The above data can be a good starting point for identifying attractive CEFs opportunities (and risks), but deeper analysis is a requirement in our opinion. Before getting into specific ideas, here are a few critical CEF considerations to keep in mind.

-

Holdings : As suggested by the "strategy" column in the table above, CEFs have widely different strategies (ranging from bonds, to REITs, to sector-specific equities). And because CEFs are funds they have many underlying holding (often ranging from 50 to 60 underlying holdings and all the way up to 1,000 to 2,000 or more!). This helps create some instant diversification of risks within each fund’s target strategy

-

Price Discounts and Premiums : Another important characteristic of closed-end funds (which is different from other mutual funds and exchange traded funds) is that CEFs can trade at wide price premiums and/or discount to the aggregate market value of their underlying holdings (i.e. net asset value, or “NAV”) as you can see in the “Disc/ Prem” column in our table above. This can create significant risks and opportunities, as we will explain with examples later in this report.

-

Leverage : CEFs often use leverage or borrowed money. This can help magnify returns and income in the good times, but it can also magnify risks and losses in the challenging times (such as 2022). CEFs use a wide range of leverage (depending on their strategies), but bond fund are generally limited to 50% leverage (by regulation) and equity funds to 30%.

-

Distribution Sources : As you may already know, CEFs don’t usually source 100% of their distribution payments from dividends or income on their underlying holdings. Rather, a portion of the distribution is often comprised of capital gains (short-term versus long-term can have different tax consequences) as well as even a return of capital in some instances (which can act to reduce your cost basis thereby resulting in some unexpected capital gains taxes if/when you do sell, assuming you hold it within a taxable account.

-

Fees and Expenses : CEFs have a variety of fees and expenses, and this ultimately detracts from your performance. For example, management fees often range from 0.50% to 2.00% per year. Further, operating expenses (including the interest expense on borrowed money—remember some use leverage) also rolls up into the total expense ratio. Some investors avoid CEFs because they cannot stand the fees, whereas others don’t mind the fees as long as the bottom line performance meets their needs. We often prefer to purchase individual securities instead of CEFs (to avoid the fees), but in some cases CEFs are extremely attractive regardless of the fees (for example, some bond funds have access to bonds that we cannot buy on our own, and CEFs also generally have access to lower cost (and more operationally efficient) leverage than do most individual investors—which is a legitimate “value add” for select CEFs).

So with that backdrop in mind, let’s get into four names from the above list that we believe are worth considering.

PIMCO's PTY Is Hot - Yield: 10.4%

PTY is a popular PIMCO bond fund, and for good reason. For starters, it's managed by PIMCO , generally considered the top bond CEF manager (thanks to the company's track record of delivering the goods). For example, PTY has a long history of paying big monthly income to investors, plus an occasional special dividend to boot.

{kind=link}

CEF Connect

PTY's objective is maximum total return through a combination of current income and capital appreciation. Specifically, PTY seeks to achieve its investment objective by utilizing a dynamic asset allocation strategy among multiple fixed income sectors in the global credit markets, including corporate debt, mortgage-related and other asset-backed securities, government and sovereign debt, taxable municipal bonds and other fixed-, variable- and floating-rate income-producing securities of U.S. and foreign issuers, including emerging market issuers.

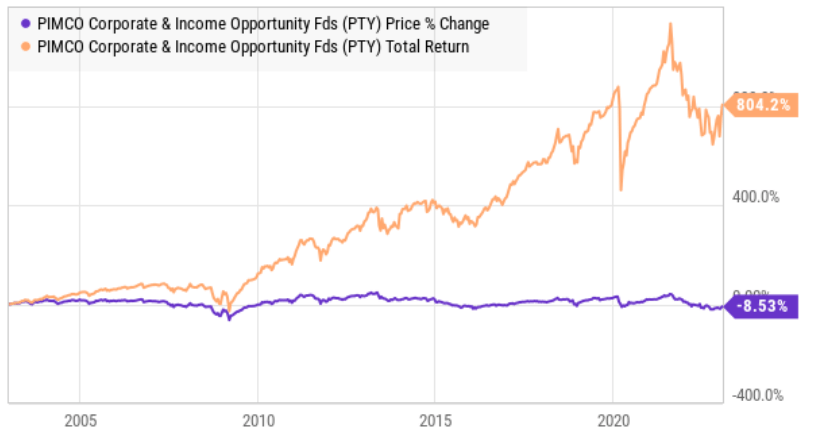

Long-Term Returns : In addition to a long history of paying big steady distributions to investors, PTY does have a long history of delivering solid total returns. As you can see in the following chart, PTY's since-inception total return (orange line) is impressive.

{kind=link}

CEF Connect

Also noteworthy, PTY's price return has been somewhat flat-ish over the years (as you might expect, considering so many people own it for the income), but has shown some price weakness over the last year. The price has been weak due mainly to rising interest rates (as rates go up, bond prices go down, ceteris paribus). And with inflation finally starting to show signs of slowing, interest rates are expected to stop increases this year, and that is a good thing for PTY (its interest rate risk, as measured by duration, was recently just over 4 years--quite reasonable in our view).

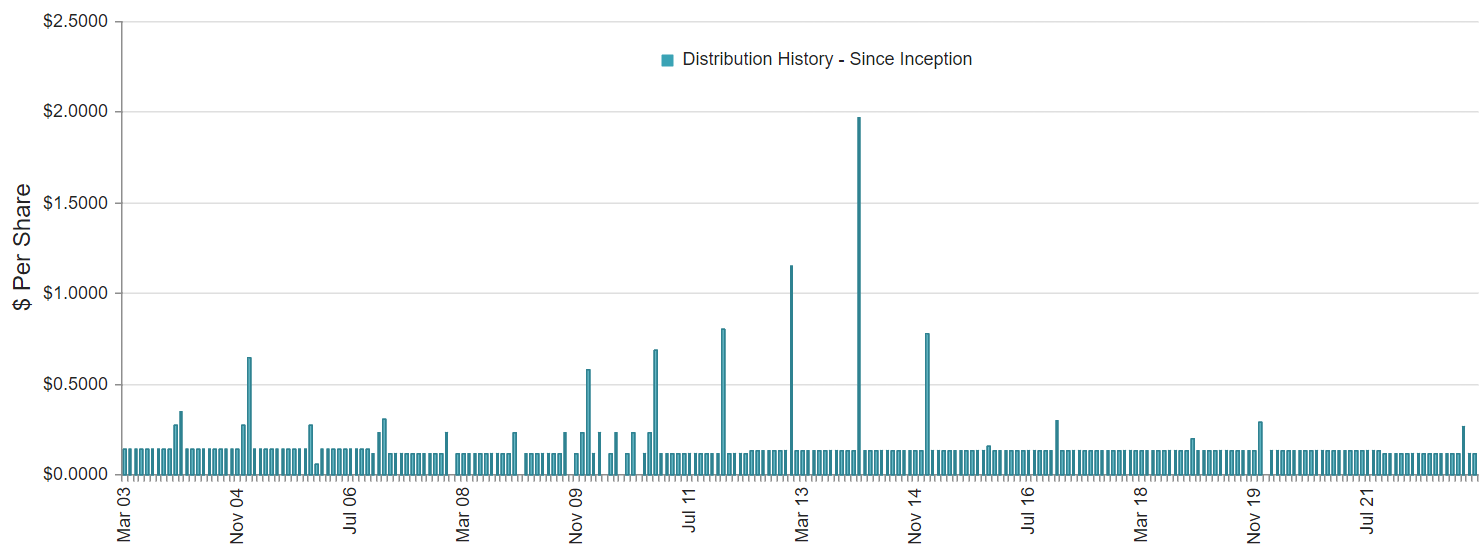

Sources of Income : Another attractive quality of PTY is that it has been sourcing its big monthly distributions from income and NOT capital gains or return of capital.

{kind=link}

CEF Connect

Many investors argue this is a very good thing because it is a testament to the income-generation power of the fund. And because return of capital can reduce your cost basis thereby resulting in some additional capital gains taxes if/when you sell (assuming you own in a taxable account).

Leverage : One important thing to be aware of about PTY is that it does have a significant amount of leverage or borrowed money (currently around 39.5%). This can act to magnify income and returns in the good times, but it can magnify losses in the challenging times (such as the challenging interest rate environment of 2022). We are comfortable with this level of borrowing (it's actually conservative for PIMCO and average for many other top bond CEFs).

Expense Ratio : The high leverage brings up another point--expense ratio. PTY has a relatively low total expense ratio, recently at 1.13% (which includes management fees and the interest expense on borrowing costs). And as interest rates have risen, the cost of borrowing has increased. It won't be surprising to see this total expense ratio go up in the years ahead-especially considering it is still quite low for a PIMCO CEF in particular.

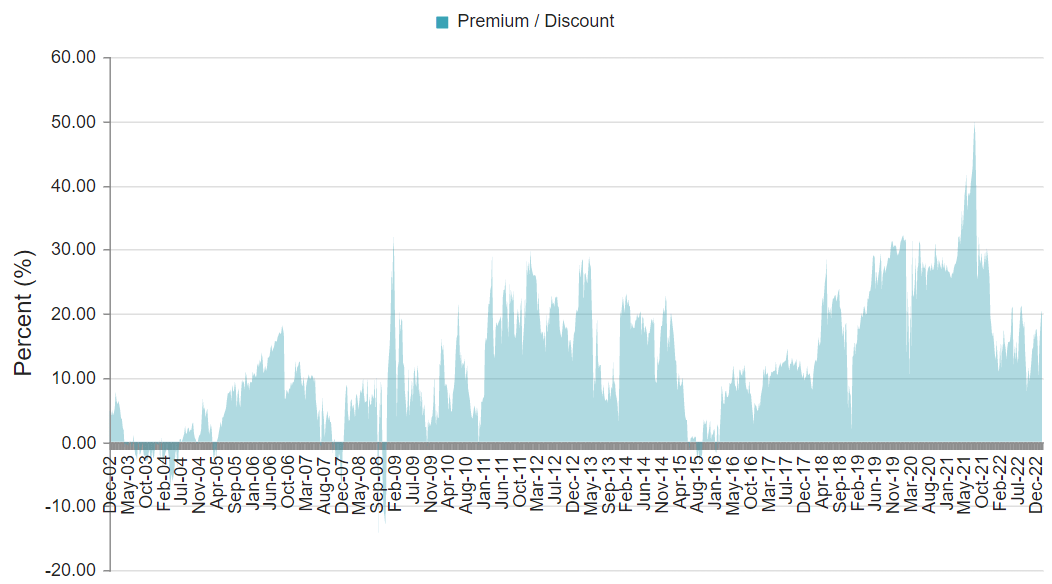

Premium to NAV : However, as mentioned, CEFs can trade at large premiums or discounts to their NAV's, and PTY currently trades at a significant premium (+20.5%), as you can see in the following chart.

{kind=link}

CEF Connect

Some investors will point out that PTY has historical traded at even higher premiums, and that as long as it keeps paying those big steady monthly income payments--who cares about a 20.5% premium. Afterall, this is PIMCO we're talking about--the global leader in bond CEF management and deserving of some premium pricing. Others will argue, why pay such a big premium when there are comparable funds trading without such a big price premium.

PTY Bottom Line : If you can get comfortable with PTY's big premium to NAV (it's gone from below 10% to above 20% in recent months), it's a very attractive big-income fund. But if you just can get comfortable with the big premium, here is another bond CEF idea for you to consider.

PIMCO Dynamic Inc Opps ( PDO ), Yield: 10.8%

Both are bond CEFs managed by PIMCO, but there are some notable differences between PDO and PTY. For starters, PDO offers a bigger yield (also paid monthly) and it trades at a dramatically smaller price premium to its NAV (currently only around 3.7% versus 20.5%). The objective is similar (PDO seeks current income as a primary objective and capital appreciation as a secondary objective) and the holdings are also similar but different (they both have a lot of non-agency mortgage-backed securities and high-yield credit--but in slightly different weights). The interest rate risk of the two funds, as measured by duration, is almost identical (4.08 versus 4.09 years).

One key difference among the two funds is that PDO has more borrowed money. Specifically, PDO's leverage ratio is backing up hard against the 50% regulatory limit. In theory, this can result in some forced sales at less than optimal prices to bring the leverage amount lower (falling bond prices over the last year has increased the leverage ratio for virtually all long bond funds, all else equal). However, considering PIMCO's sophistication and resources (and it's 33.5% allocation to investments maturing in 0 to 1 years), we believe PDO can navigate this challenge essentially unscathed. Notably, PDO also has a higher total expense ratio, recently 2.78% (similar to other PIMCO bond CEFs) in large part due to the higher cost of borrowing (again, PDO has a higher leverage ratio).

Overall, if you are looking for a bigger PIMCO bond CEF distribution (paid monthly) that currently trades much closer to NAV (instead of at PTY's large premium), PDO is worth considering.

DNP Select Income Fund ( DNP ), Yield: 6.7%

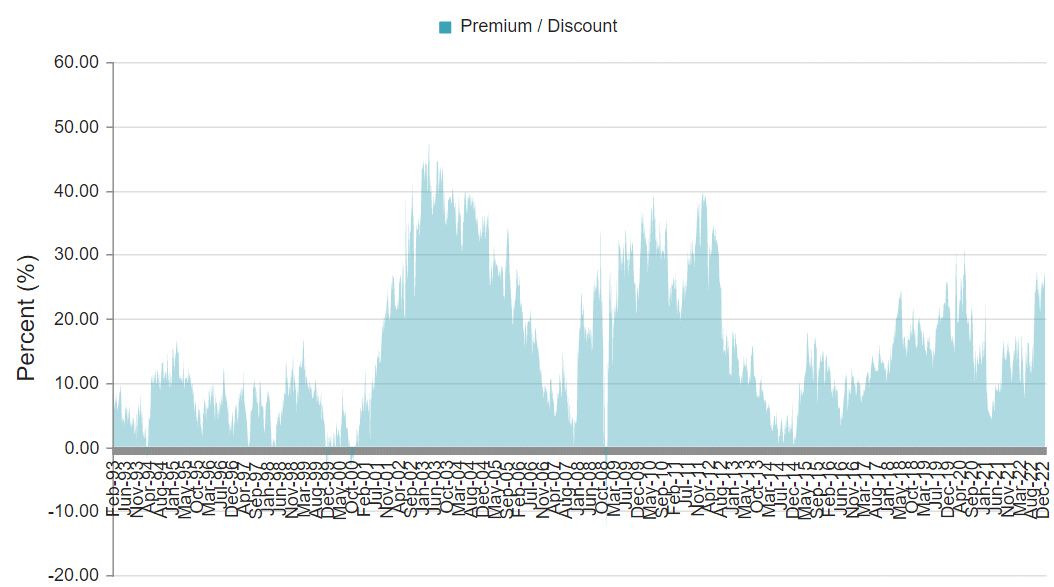

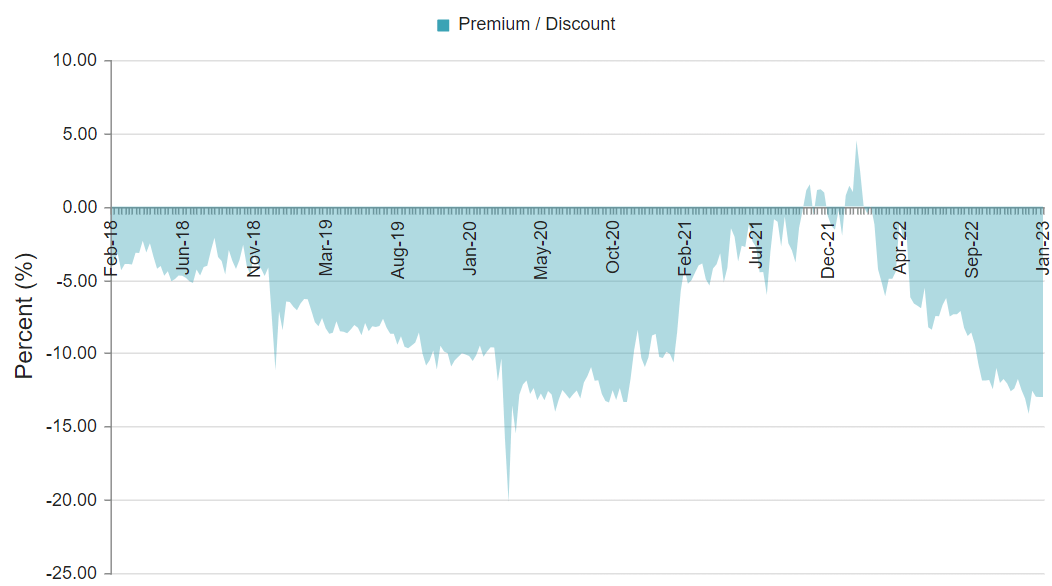

Another "hot" big-yield CEF from our table above is the Duff & Phelps Select Income Fund. We say it's hot because of the wide discrepancy between its 2022 price return and its 2022 NAV return. Because the price performed so much better than the NAV, it suggests frightened investors were piling into this fund for its perceived safety. Specifically, DNP invests primarily in Utility Company securities (both stocks and bonds), which are perceived as a low volatility safe haven, especially during times of heightened market volatility (such as 2022). DNP is very popular (as per its huge $3.3 billion in assets) , but it also now trades at an enormous 27.4% price premium as compared to its NAV.

{kind=link}

CEF Connect

Some investors will point to DNP's historical premium chart (above) and say it has traded at big premiums before, so why should I mind now? However, you'll also note those big historical premiums were also during times of market distress, including the tech bubble bursting and the great financial crisis.

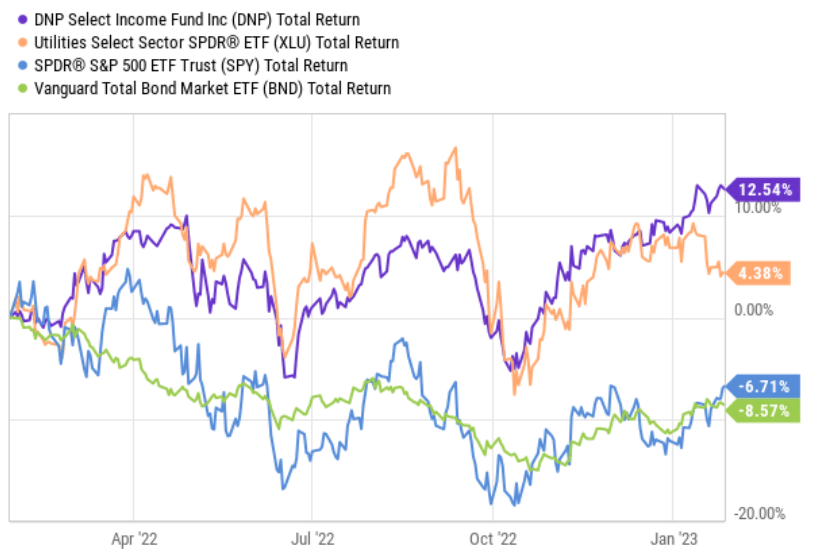

If the market remains painfully challenged in the quarters and years ahead, DNP may be a decent safe haven investment. But considering the market is usually ahead of the economy (the market is already pricing in an ugly recession) and the Utilities sector may be due for some mean reversion (i.e. underperformance versus the rest of the market following its strong 2022), now might be a decent time to consider exiting your DNP investment and moving your money elsewhere. For example, the following chart shows the strong 1-year total return performance of DNP versus the Utilities sector ( XLU ), the S&P 500 ( SPY ) and the aggregate bond index ( AGG ).

{kind=link}

YCharts

We're not saying DNP is a terrible investment (it's not). However, its large price premium to NAV is increasingly worrisome (especially to some investors more than others), and it may be worth moving some of your winners into other contrarian opportunities (particularly ones where the premium hasn't soared in recent months). Also, from a contrarian standpoint, DNP has crushed both the stock and the bond markets over the last year (kudos to you if you've owned it), and it may be worth considering other options now.

Tekla Life Sciences ( HQL ), Yield: 8.4%

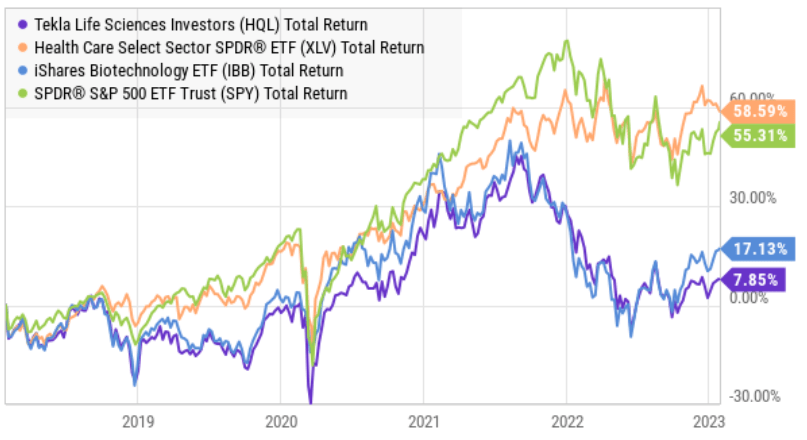

Moving to a different market sector altogether, you might consider investing in the Tekla Life Sciences CEF. It currently offers a bigger yield (than DNP), an attractive price discount of ~13.0% (see chart below), and healthcare stocks can continue to hold up well in most market environment, especially pharmaceutical companies and those that benefit from the healthcare procedures that were postponed during the pandemic lockdowns (as demand continues to resume).

{kind=link}

CEF Connect

Further still, this fund has significant exposure to biotech companies (72.3%), a group that has gotten hit hard during the recent market volatility and may now be poised for a bit of a contrarian rebound.

{kind=link}

YCharts

For a little perspective, this fund uses very low leverage (recently ~2.5%), and has a somewhat reasonable expense ratio (recently ~1.4%). It also has compelling z-scores (a comparison of the price discount or premium versus recent history—lower is generally considered better). Overall, if you are looking for a contrarian big-yield opportunity currently trading at a discount, HQL may be worth considering. And if you don't particularly care for HQL, we share a handful more big-yield CEF ideas here .

The Bottom Line:

CEFs are a widely diverse space with many important nuances and plenty of big-yield opportunities. In our view, PTY and DNP are both attractive, but a little bit on the expensive side. Whereas, we like PDO and HQL as possible alternatives, and have gone so far as to rank them #6 and #10, respectively, on our new Top 10 Big-Yield CEFs members report . However, at the end of the day, you need to select only opportunities that are right for you and your personal situation. We believe disciplined goal-focused long-term investing will continue to be a winning strategy.

For further details see:

PTY: 100 Big-Yield CEFs, These 4 Worth Considering