PTY - PTY: This 10% Yielder Is Underwater But The Prospects Are Still Attractive

2023-12-18 12:45:52 ET

Summary

- PIMCO Corporate and Income Opportunity Fund offers an attractive yield of around 10.6%.

- Yet, the dividend is underwater as there is a notable gap in the underlying coverage. The fact that most of PTY's AuM is placed in high-risk segments makes matters worse.

- Moreover, PTY carries ~27% of external leverage, which could magnify any further declines in PTY's holdings.

- The fact that interest rates are becoming more accommodative should send PTY's price higher from here because of the duration profile and short-term funding at the external leverage front.

- For me, PTY remains too speculative with its dividend likely to be revised downwards, but over the foreseeable future, the probability is high of experiencing a solid performance.

PIMCO Corporate and Income Opportunity Fund ( PTY ) is another CEF managed by PIMCO that delivers a rather attractive yield of ~10.6% level.

PTY applies a dynamic and diverse asset allocation strategy, where there is a great distribution across different duration segments, credit qualities, industries, and issuers.

While PTY seeks maximum total return through both current income and capital appreciation, it is clear that the former component explains the majority of the returns.

{kind=link}

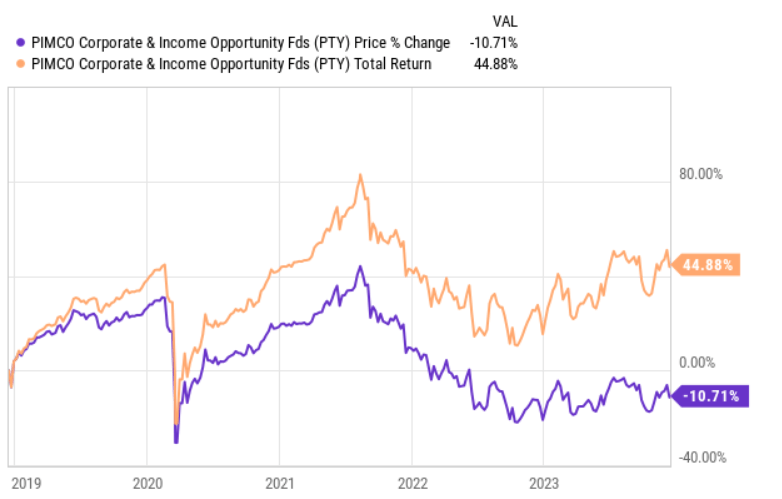

Looking at the 5-year history, we can nicely notice how PTY's dividends have contributed to the overall total return equation, whereas on a price per unit level, the Fund is actually down.

This is only logical considering PTY's exposure to high-yield credit and non-agency mortgages.

PIMCO 2023

As of now, PTY carries around half of its AuM in instruments, which inherently generate attractive streams of current income. Plus, there are a bit safer allocations in fixed-income type securities as well, such as the U.S. Treasury notes and bills, investment grade corporate credit, and municipal bonds.

All of this creates a solid base from which PTY could deliver relatively attractive distributions.

Moreover, a critical aspect in the context of PTY's ability to achieve a double-digit dividend is the additional leverage, which depending on the period tends to account for roughly 30% of the underlying portfolio value. Currently, the external leverage ratio is just over 27%.

What this does is it allows PTY to magnify the yield potential that stems from the fixed income allocations as long as the spread between the cost of financing and portfolio yield is positive.

Thesis

Let's start with the key areas of concern.

{kind=link}

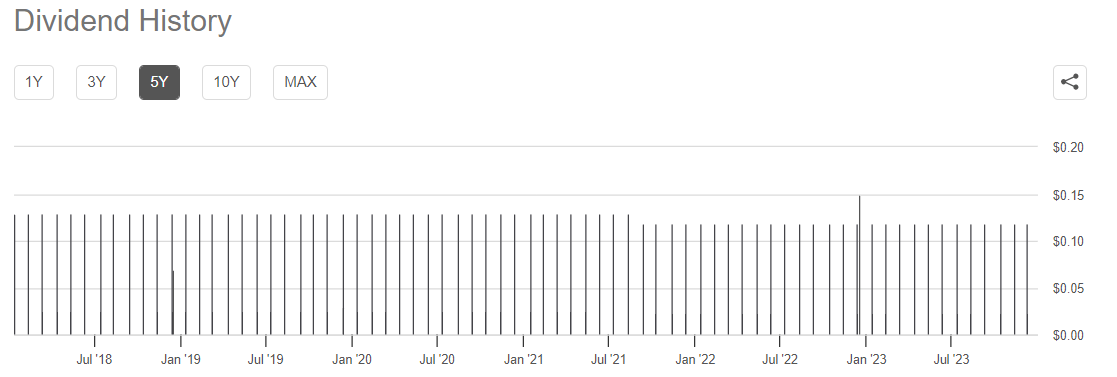

Currently, PTY's dividend is underwater. Roughly 30% of the monthly distributions this year have been sponsored by divesting parts of the NAV base. So, the ~10.6% yield gives an illusion that all of this attractive yield could be directly pocketed on top of the price appreciation potential. In reality, this should be viewed as partially fresh dividend income and partially as a return of capital (to an extent, where the NII does not cover distributions).

{kind=link}

A more sustained undercoverage of the distributions could potentially lead to a new dividend cut, just as PTY already did in mid-2021. In such cases, not only the dividend would drop but the unit price would most likely suffer as well.

Since PTY is heavily biased toward relatively low-quality fixed-income securities, there is per definition a low margin of safety embedded in the fund that further weakens the sustainability of the current dividend.

Given the 27% of external leverage, this risk is further elevated, where any struggle of a specific PTY's constituency renders a more pronounced impact due to the relevant magnifying effects.

So, the combination of a notable gap in the dividend coverage, concentration in inherently risky asset classes, and an external leverage on top of that does not bode well for PTY's chances to enhance the NII level so that it is sufficient to fully accommodate the monthly distributions. To put it differently, there is, obviously, such a probability, but the risks associated with it are extremely high.

On the flip side, the overall game has changed since the market has now calibrated a peak of the interest rates and expects a gradual normalization of interest rates already in 2024. Given that PTY embodies characteristics, which resemble fixed-income factors, the fund is set to become a great beneficiary of falling interest rates.

I see two major reasons why this should happen:

- Duration factor . As of now, PTY has 3.7 years of duration profile that is adjusted for the external leverage component (otherwise, it would land at ~7-year territory). This means that PTY is on average more skewed toward the front and mid segment of the curve, which in the case of interest rate cuts should directly respond to changes in the SOFR.

- Leverage. Almost the entire position that is associated with the external leverage stems from reverse repo financings. This is great news for PTY as the current debt proceeds are not locked in, thereby allowing the reduced SOFR to quickly percolate through the system and bring down the cost of financing.

The Bottom Line

PTY's dividend of 10.6% carries an overly speculative nature as there is a notable gap between the generated income and the distribution level that has to be paid out on a monthly basis. The fact that the underlying portfolio is heavily exposed to rather volatile and risky asset classes that are coupled with a sizeable load of external leverage worsens the prospects of receiving a stable and predictable stream of current income.

Nevertheless, falling interest rates should inject a rather positive boost for PTY's holdings, which together form a notable duration factor. Plus, the external leverage component should become more attractive with the cost of capital declining and directly impacting PTY's NII given that the lion's share of the external leverage is assumed via short-term instruments.

With that being said, I still believe that PTY will have to make additional dividend cuts because the gap between the NII and distribution levels is just too wide. Plus, the current market's assumption of considerably dropping interest rates in 2024 might as well turn out to not be true (e.g., there could be more gradual normalization), which would make PTY's chances of maintaining its dividend very slim.

For further details see:

PTY: This 10% Yielder Is Underwater, But The Prospects Are Still Attractive