KHYB - Q4 2023 Fixed Income Outlook: Recession Takeoff Delayed But Not Canceled

2023-10-11 03:24:00 ET

Summary

- Consumer spending has remained resilient to date; therefore, the timing of a recession has become unclear.

- Higher rates have made yield the beacon for bondholders and drawn stability-seeking investors toward investment-grade credit.

- Solid reserves and balanced budgets should allow U.S. state and local credits to weather economic and revenue pressures.

- Across broader EM, there is a divergence in growth, inflation, and the likely speed of policy actions.

- Most fixed-income asset classes should fare well, supported by attractive yields and resilient fundamentals.

While the timing of a recession remains uncertain, unique opportunities exist for fixed-income investors as we head into the final quarter of 2023.

1. Policymakers are likely to remain hawkish, countering market expectations for rate cuts in 2023 and budgeting room for easing in 2024. This should support elevated front-end yields.

2. With market expectations shifting toward a soft landing, credit spreads are likely to remain rangebound, exhibiting a widening bias as a recession becomes more evident.

3. Though economic data has been resilient, key market indicators continue to signal an impending recession, and we strongly believe there is further economic slowing on the horizon

Macro outlook

U.S.

Robust consumer spending continues to support U.S. economic growth, causing many market participants to re-evaluate their recession expectations and embrace the elusive soft-landing scenario as the consensus base case. However, it is presumptive to extrapolate recent strength in consumer spending for many reasons including (but not limited to) the lagged impact of Federal Reserve (Fed) and commercial bank tightening, normalizing corporate profit margins, a more balanced labor market, dwindling excess savings, increasing consumer delinquencies and credit card debt, and student loan payments resuming.

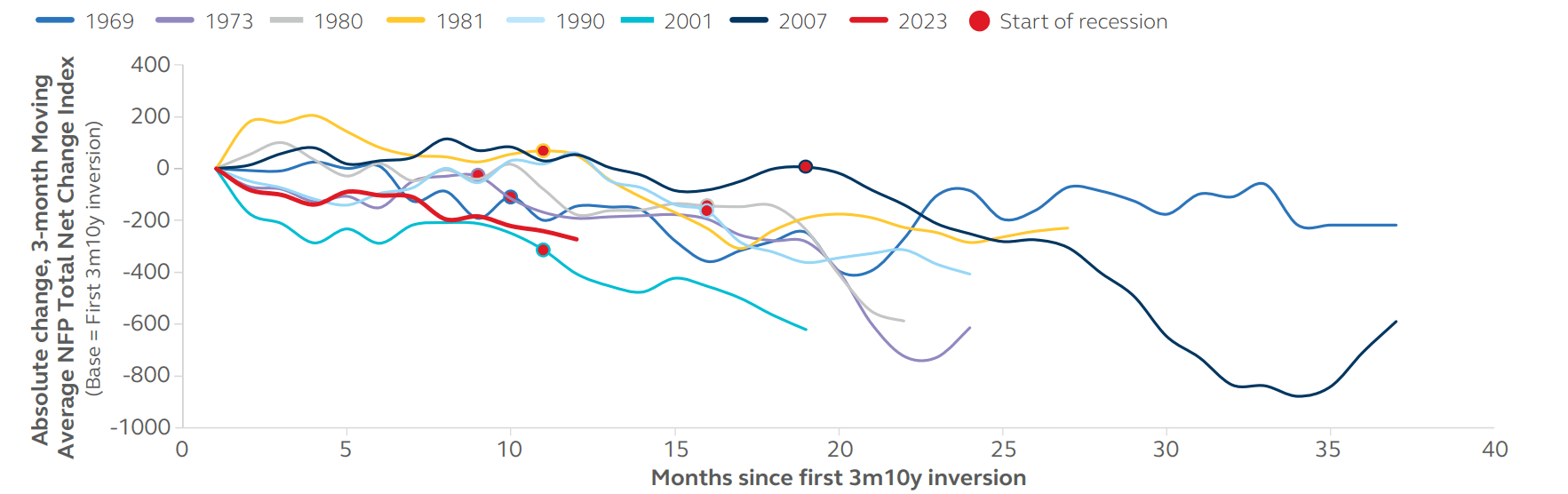

While we agree that a recession does not appear imminent, we strongly believe that further economic slowdown remains on the horizon, ultimately culminating in a recession. The yield curve - which is arguably the most reliable indicator of a recession - has inverted nine times since 1968, of which a recession has followed eight times. Soft landings have only occurred after Fed hiking cycles that were not accompanied by a yield curve inversion.

A close examination of current economic metrics relative to the prior eight inversions does not suggest that this time will be different. Recent economic data is consistent with the evolution in prior inversions/recessions including purchasing managers indices, jobless and continuing claims, nonfarm payrolls, and bank lending.

EXHIBIT 1

Nonfarm payrolls (3m moving average) from first inversion to end of recession

{kind=link}

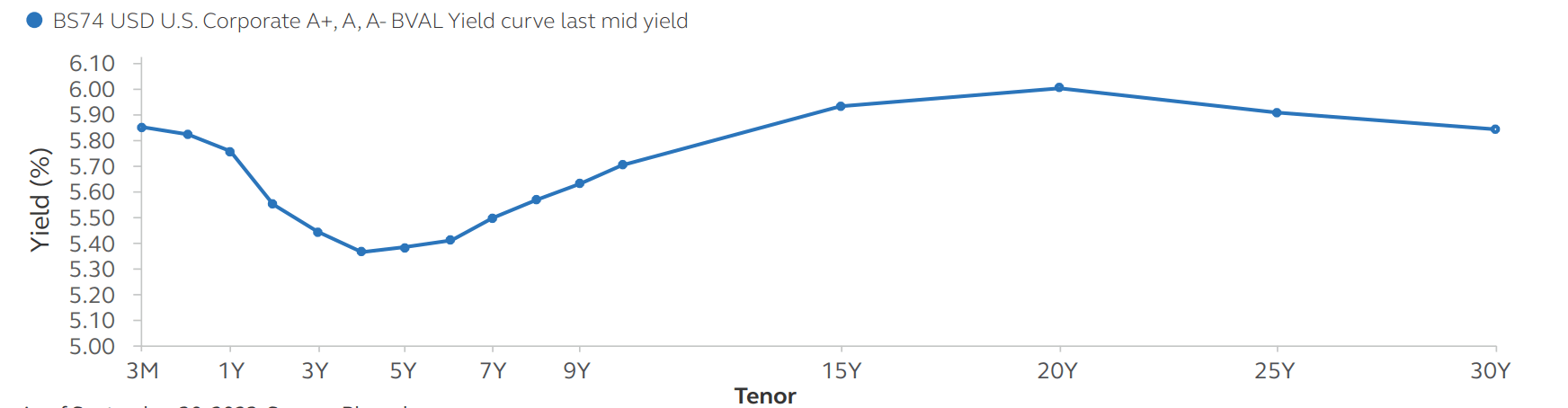

However, consumer spending has remained resilient to date; therefore, the timing of a recession has become unclear. Fortunately, the current yield curve inversion provides attractive yield opportunities for fixed-income investors, most notably in short-dated instruments that have less sensitivity to credit spreads (spread duration). With most market participants now expecting a soft landing, spreads in credit sectors are tight relative to history. Although some additional tightening is possible, spreads are likely to start to drift wider when a recession does begin to materialize. Short-dated paper in asset-backed securities ((ABS)), select commercial mortgage-backed securities ((CMBS)), and investment grade credit ((IG)) offer higher spread/carry than longer-dated securities and insulate investors from potential spread widening. The following yield curve of high-quality investment-grade corporate paper demonstrates the unique opportunity in short-dated securities.

EXHIBIT 2

Unique opportunity in short-dated securities: high-quality investment grade corporates

{kind=link}

As mentioned, an inversion in three-month vs. ten-year rates has been extremely reliable in predicting recessions over the past 50+ years. Additionally, a Fed pause usually marks the peak inversion for the cycle, favoring the front end of the yield curve. As we await further evidence that a recession is imminent, the inversion provides an opportunity for a carry/yield advantage while also limiting spread duration - a desirable combination for investors.

Global

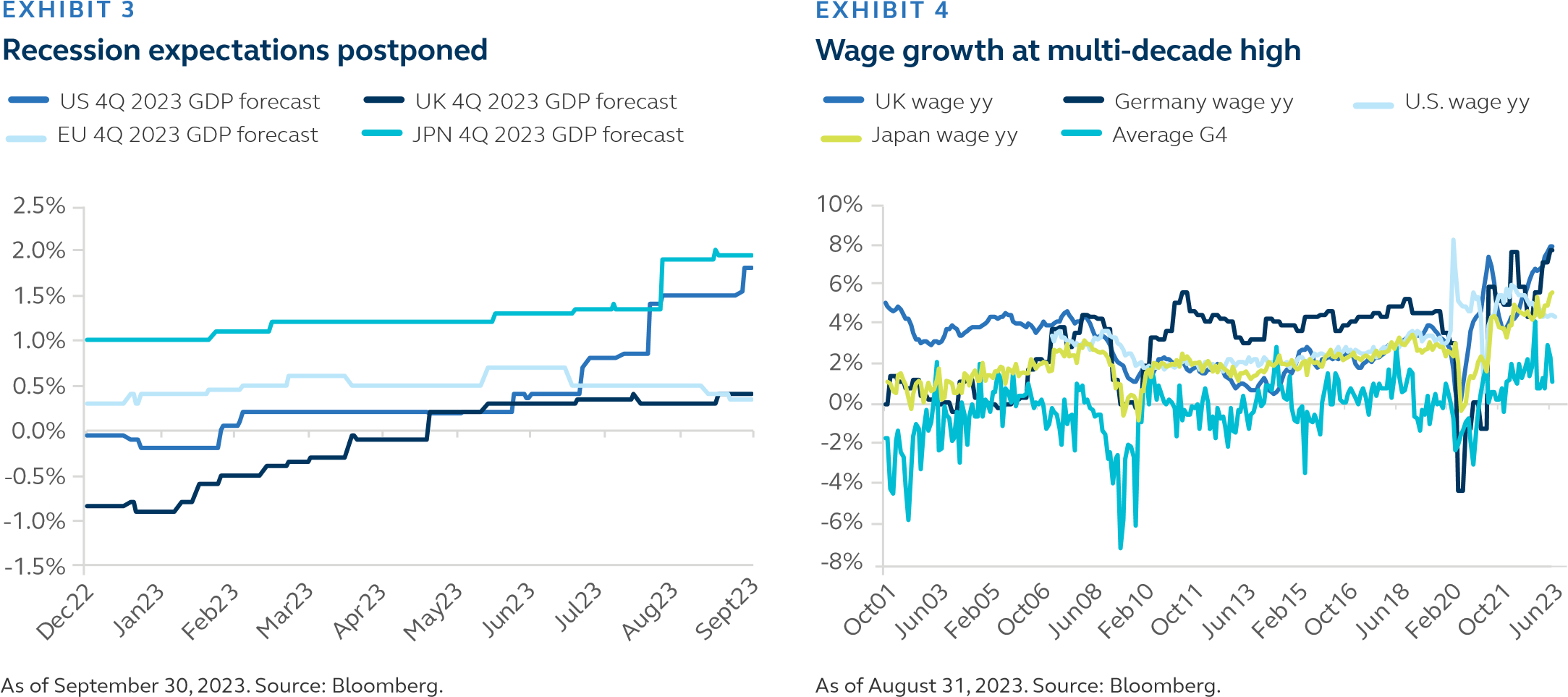

The third quarter of 2023 was dominated by two themes, the first of which was the growing consensus for a soft landing. As growth data in the U.S. and Europe raised the likelihood that a recession could be avoided, market participants pivoted to pricing for resilience and a rebound in economic growth. Indeed, this corroborates the Atlanta Fed's GDPNowcast which projected a >5% growth rate for the U.S. economy in 3Q. The consensus forecast also raised projections of U.S. 2023 growth from -0.2% in February to 1.8% in September.

The other dominant narrative involved expectations of tighter-for-longer monetary policy. Policymakers have been consistently hawkish, pushing back against market expectations of rate cuts in 2023 while allowing for some easing in 2024 subject to inflation data. Over the past quarter, developed markets reported tight labor markets and high wage growth. On a year-on-year basis, wages in the G4 economies (U.S., eurozone, Japan, and the U.K.) have broken out of a two-decade range, leading the market to price in tighter monetary policy for years to come.

Collectively, these two themes led global yields, as represented by the global aggregate index, to rise almost 40 basis points (bps) in 3Q, even as G4 central banks indicated they are done with rate hikes based on current data. The Bank of Japan's (BOJ) adjustment to its yield curve control policy in July added to the duration overhang, a known risk that we highlighted in our 3Q outlook. The BOJ chose to make a more meaningful adjustment in one go, lifting the stated yield cap by 50 bps and subsequently managing market volatility with unscheduled bond purchases.

Notwithstanding this backdrop, we caution against extrapolating the current themes. There is a high likelihood that the current drivers of higher-for-longer yields are not sustainable. Current key economic indicators, such as the Purchasing Managers' Index, point to falling output and orders. Even the tight labor market is showing signs of cracks, with job gains revising lower and some economies, such as the U.K., seeing outright job losses. All of these indicators are in line with historical norms, as banks tighten credit alongside monetary policy tightening, and are consistent with policymakers' expectations that the lagged effects of policy adjustments are yet to be fully reflected in current economic data. In Asia, China's growth challenges were further brought into the limelight with misses in the usually benign official economic data, adding to the risks for global growth over the next six months.

Accordingly, we believe there is a very high probability that the recession trade returns to the market.

{kind=link}

Summary of investment implications

Investment Grade Credit

With rate cuts unlikely over the remainder of 2023, we believe the market environment for investment-grade investors should remain enticing, as higher yields are creating a technical tailwind for the investment-grade market and should bolster spreads.

High Yield Credit

Our base case scenario calls for wider spreads in high yield and slightly higher default rates. However, high yield offers very compelling return prospects due to strong corporate fundamentals and a receptive primary market, presenting an advantageous long-term risk/reward profile.

Securitized Debt

High-quality, short-duration consumer asset-backed securities remain a compelling opportunity for investors, while recent regulatory changes and rate stability driven by a pause in the Fed hiking cycle should produce increased bank demand for mortgage-backed securities over the longer term.

Municipals

Our outlook on the U.S. state and local government sector remains stable-to-positive under a mild recession scenario. Solid reserves and balanced budgets should allow U.S. state and local credits to ride out a short and shallow economic slowdown.

Emerging Market Debt

Emerging market ((EM)) credit spreads have widened recently (driven by rising U.S. yields and China's fading recovery momentum), unwinding some of the gains made in 3Q 2023. Moving forward, EM policymakers will be challenged to balance their domestic growth outlooks, rate trajectories, and foreign exchange dynamics.

Private Credit

Though public markets rallied through much of 2023, opportunities remain attractive for investors in middle-market private credit. Investment grade private credit year-over-year deals vs. 2022 are down an estimated 20%, but we expect flow volume to increase the pace in 4Q after a slow summer for middle-market direct lending; however, we believe the loans originated during the upcoming period will deliver investors value.

Investment grade credit

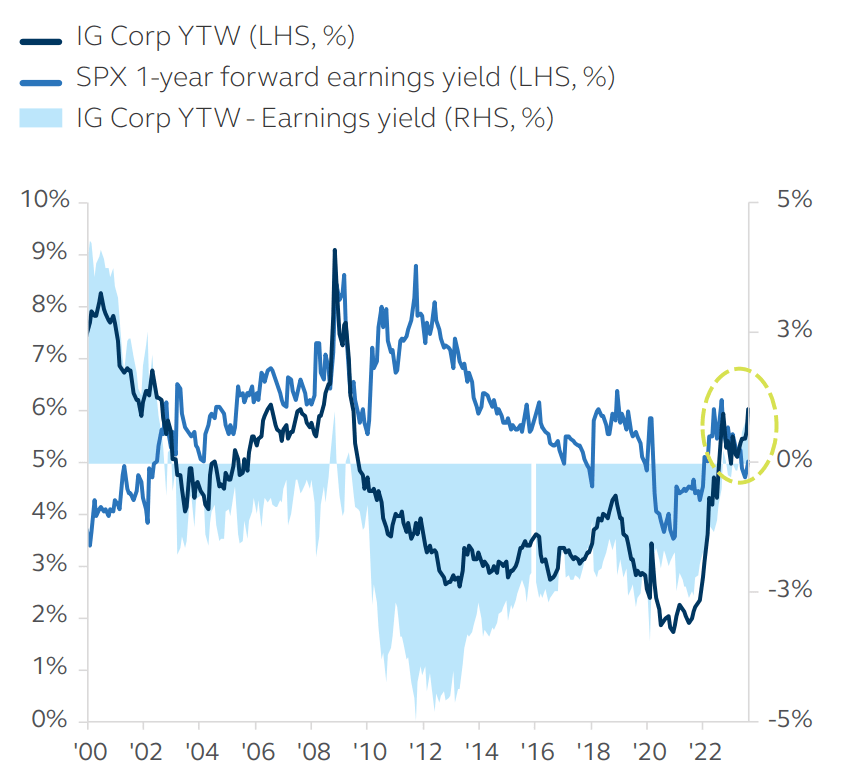

Higher rates have made yield the beacon for bondholders and drawn stability-seeking investors toward investment-grade ((IG)) credit. At the end of the quarter, investment grade yields were closing in on heights last seen during the Great Financial Crisis ((GFC)) (Exhibit 5). Put simply, the risk/return profile for corporate bonds appears quite compelling from a yield standpoint.

Fortunately, market forces tipped the scales in yield buyers' favor as rates soared off near-zero levels last year, creating a crescendo in yields. With yield-focused bond investors making up a majority of the institutional investor base, this substantial source of demand should lend solid structural support to the asset class. Indeed, insurance companies, pension funds, and overseas investors make up more than 60% of the investment-grade buyer mix.

Spreads - the credit component to IG yields - have remained resilient and resistant to widening as of late. Part of the reason for that has to do with the yield for which investors are yearning. As yield has become the backbone of bond investing, corporate debt buyers are capitalizing on it. We foresee that trend continuing to play out, especially amid the higher-for-longer rate environment. In fact, the longer rates remain elevated, the sharper the focus and larger the appetite of yield buyers, which, in turn, begets bond buying.

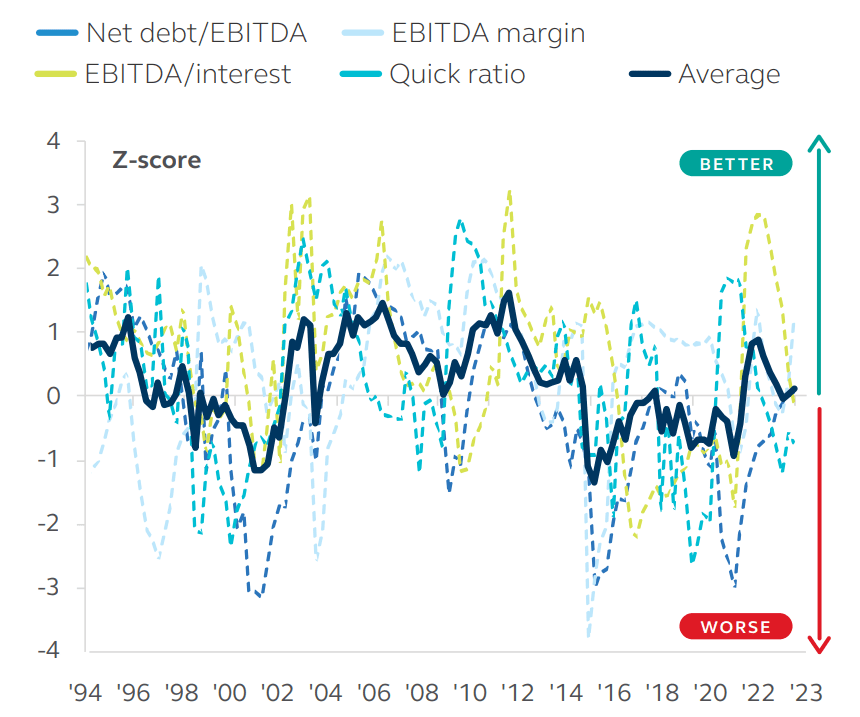

With spreads at the tighter end of their recent range and as we head toward a potential turning point, credit selection matters now more than ever. A time-tested, bottom-up bond-picking process that is tailored to the environment will define the outperforming bond managers. And though fundamentals may weaken as economic conditions worsen, they start from a position of strength (Exhibit 6).

The yield represents one of many factors that have been enabling stronger technicals to win over weakening fundamentals. Bond supply is another, which should remain manageable this fall and winter. Companies issuing debt and seeing higher rates may pause, particularly at the long end where locking in higher-cost funding loses appeal. Indeed, only 12% of issuance has come at the long end of the curve since July (vs. 22% in the first six months) despite demand. Lower new issue volume and more short-dated supply would serve as positive technical factors to pair with high IG yields.

Higher yields create a technical tailwind for the IG market and should bolster spreads. As yields beckon bond investors, that technical tailwind should serve to anchor demand. With rate cuts unlikely over the remainder of 2023, we believe the market environment for investment-grade investors should remain enticing. In short, stronger technicals should outweigh weaker fundamentals in the near term.

EXHIBIT 5

Attractiveness of investment-grade corporate bond yield

{kind=link}

EXHIBIT 6

Sound fundamentals gradually weakening

{kind=link}

High yield credit

Despite an anticipated economic slowdown, we do not believe investors should shy away from high yields. A large proportion of issuers saw earnings decelerate in the second quarter while the third quarter produced flat earnings growth at best. However, earnings have fared much better than feared, and we expect earnings to improve in 2024. According to JP Morgan, 2.4x as many high-yield companies beat EBITDA expectations than missed, and more importantly, 1.6x as many high-yield companies provided forward-looking guidance interpreted as positive than negative, giving us confidence that companies can weather the macro headwinds.

There's been a modest rise in the global default rate since last quarter, however, our baseline forecast remains steady at 4%. Our base case scenario continues to call for wider spreads in high yield and slightly higher default rates. However, high yield offers very compelling return prospects due to strong corporate fundamentals. High-yield issuers entered this slowdown with low leverage and extremely strong interest coverage. We expected a slight deterioration in fundamentals due to the interest rate hikes but from extremely strong starting points.

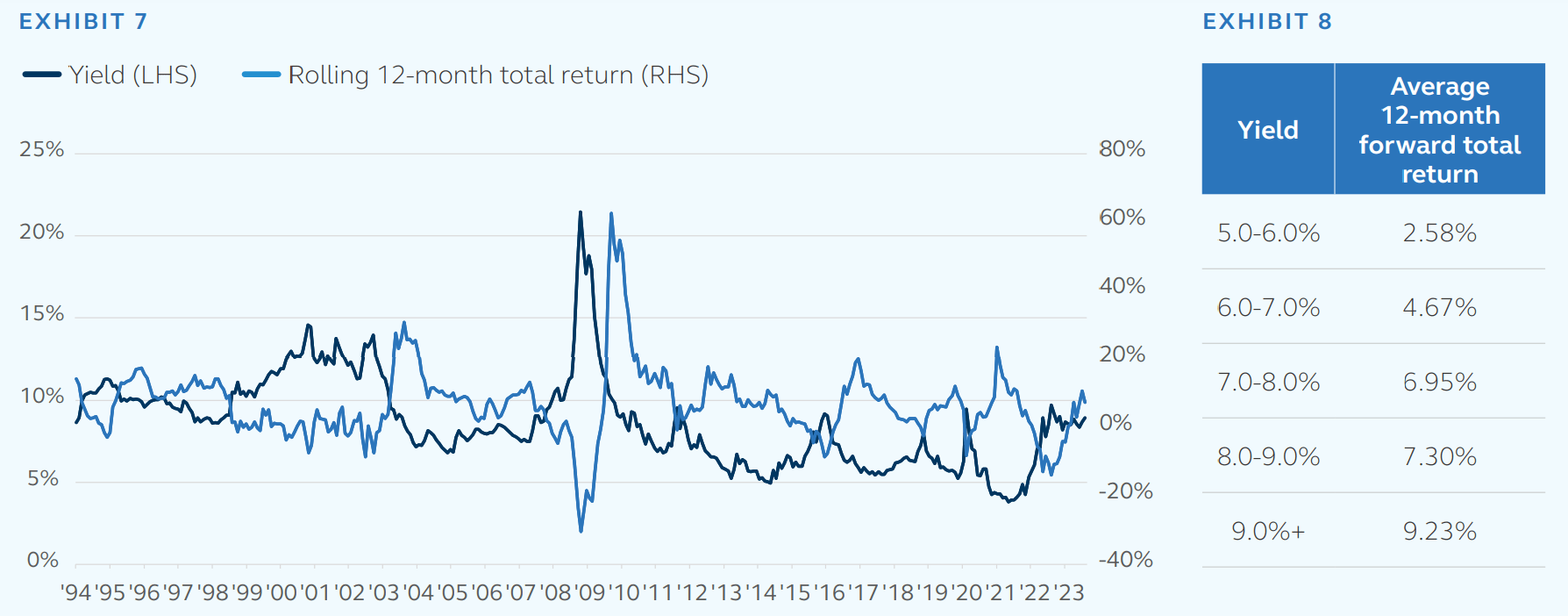

Even assuming we see a modest spread widening, the elevated yield environment still generates significant income and a reasonable total return. We understand the argument that spreads are not cheap, but history has shown that these starting yields generate attractive total returns as illustrated by the following graph (Exhibit 7). Taking it one step further, we have looked at "average" returns over the next 12 months in different starting yield regimes (Exhibit 8), and the asset class currently yields nearly 9%. High yield typically performs very well in the 12 months following higher-yield environments. Additionally, this yield regime has the potential to benefit new investors who see the underperformance of high yield relative to equities.

We believe a combination of moderating inflation, global rates closer to their terminal rates, and a very resilient consumer reduces the probability of a pronounced recession and will help avoid a significant uptick in defaults. Issuer fundamentals and a receptive primary market provide additional support for high yield. Although we expect spreads to slightly widen from current levels with the starting yield close to 9%, there is still potential for attractive total returns for the remainder of 2023 and into 2024. We still expect volatility, especially for companies and sectors that cannot withstand these higher rates, but an investor is not taking undue duration risk or credit risk at these levels and fundamentals. The asset class continues to present an advantageous long-term risk/ reward profile.

Elevated yields typically indicate higher total returns

As of September 30, 2023. Data represents Bloomberg U.S. Corporate High Yield Total Return Index Value Unhedged USD. Yield represents yield-to-worst (Bloomberg)

{kind=link}

Securitized debt

Asset-backed securities

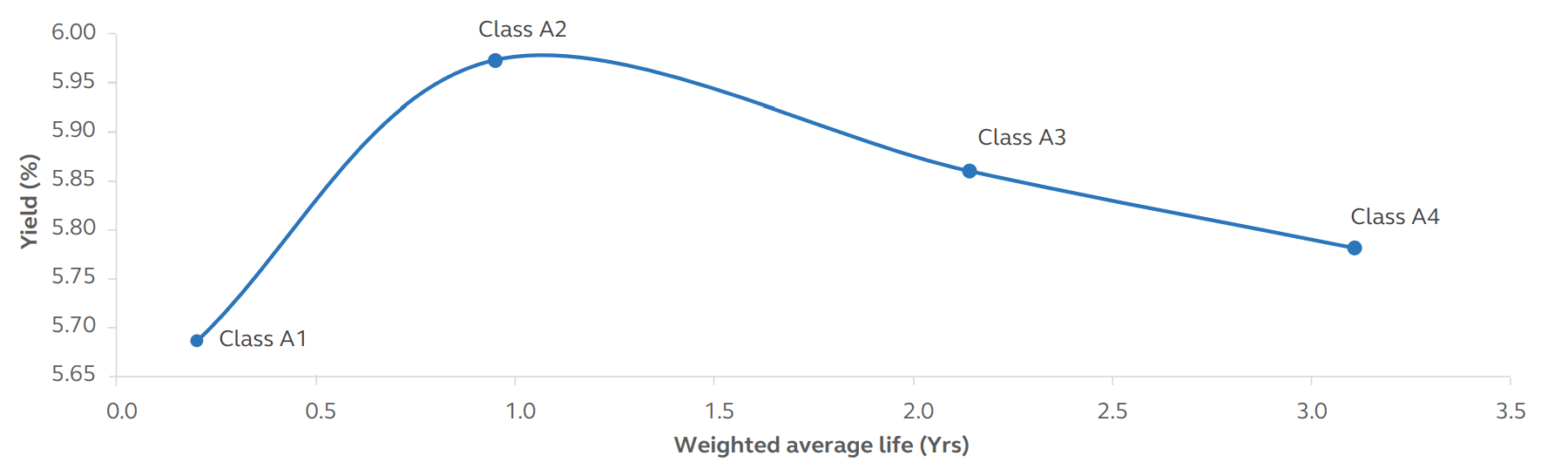

High-quality, short-duration consumer asset-backed securities ((ABS)) remain a compelling opportunity for investors. The sector saw measurable spread tightening during the third quarter, but robust supply and high benchmark rates helped keep ABS spread relatively wide and yields elevated. AAA-rated ABS near the front of the yield curve not only offers an attractive yield but also minimizes exposure to "negative roll" and helps investors limit traditional bond risks, like duration and credit.

EXHIBIT 9

AAA-rated auto ABS yield curve

{kind=link}

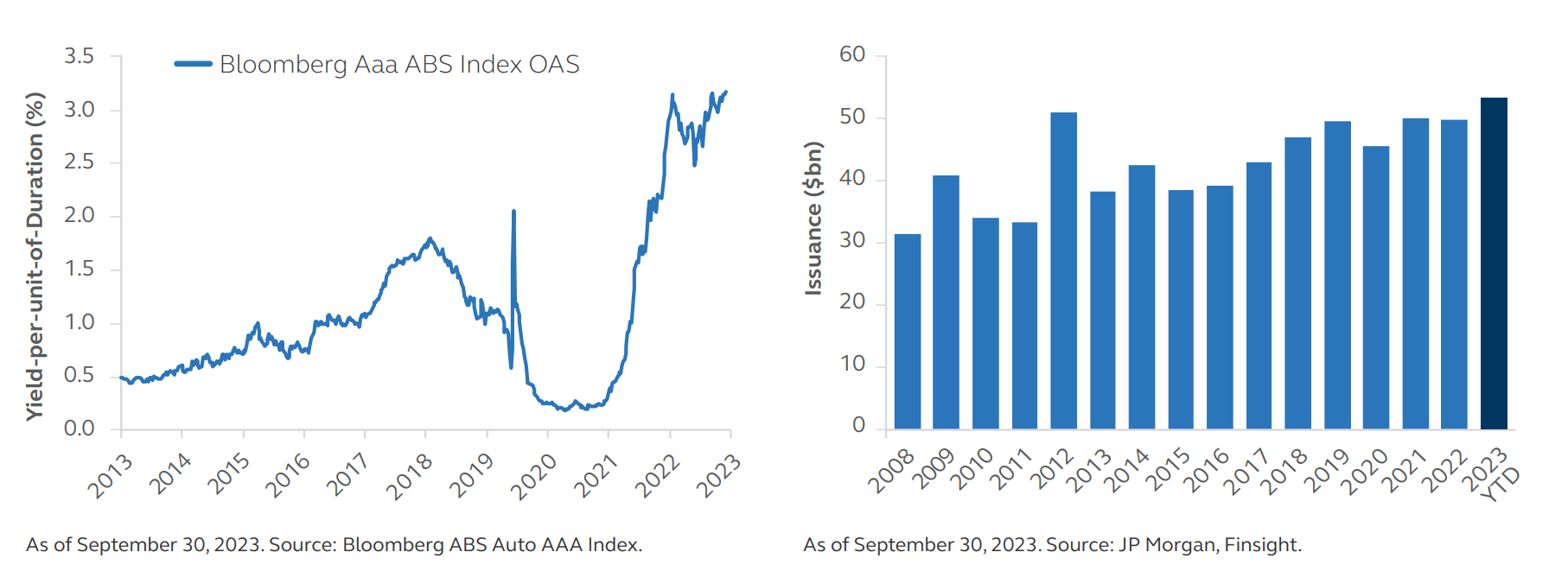

The third quarter saw elevated prime auto ABS, and opportunities for investors are likely to persist, with heavy supply expected from banks and credit unions looking to strengthen their balance sheets. Year-to-date (YTD) prime auto ABS supply already exceeds full-year 2022 issuance, and 2023 is on track to be the busiest year for prime auto ABS following the GFC. Supply pressures and benchmark rates helped push the return-per-unit-of-risk for prime auto ABS near the highest levels of the post-GFC period.

EXHIBIT 10

AAA-rated auto ABS return-per-unit-of-risk; Prime auto ABS Issuance

{kind=link}

Broad measures of consumer and labor market conditions have shown resilience. However, we maintain a quality bias, as lower-quality borrowers have seen worsening delinquencies and defaults. This trend has moderated but continues to deteriorate now that the favorable seasonal impact from tax refunds has faded. The resumption of Federal student loan payments in October will add further stress. Although the gradual on-ramp and expanded income-driven repayment options have likely taken the worst outcomes off the table, challenges for households and the broader economy remain. By strategically positioning along the yield curve, investors can benefit from attractive yields while mitigating the risks associated with an inverted curve.

Commercial mortgage-backed securities

The single asset/single borrower (SASB) sector of the commercial mortgage-backed securities ((CMBS)) market has grown substantially over the past three to four years, now comprising 35% of all outstanding private label CMBS. The SASB market is a mix of floating and fixed-rate deals with a majority in the floating rate space. That segment has come under pressure due to the sizable increase in debt service burden alongside negative commercial real estate headlines; however, most of these deals are secured by institutional-quality real estate with strong sponsors, and the amount of credit enhancement at the top of the capital stack is strong, averaging over 50%. Combining these factors, we continue to like floating rate AAA SASB bonds due to their lack of duration, strong carry, liquidity profile, and ability to dig into the underlying collateral and target favorable credit profiles.

EXHIBIT 11

Historical spread of AAA SASB

{kind=link}

Mortgage-backed securities

As highlighted last quarter, agency mortgage-backed security (MBS) valuations had widened amid higher rate volatility and the technical supply headwind from Federal Deposit Insurance Corporation (FDIC) liquidations of the Signature and Silicon Valley Bank portfolios. The MBS sector spent most of the recent quarter treading water on a spread basis, whether measured using an option-adjusted spread or production/current coupon spreads. As of the end of August, the FDIC completed the auction of the $60 billion mortgage pass-throughs, removing a very large supply headwind to the sector. Further, the outlook for organic supply is also positive, as primary mortgage rates remain above 7% thereby reducing/slowing housing activity and related mortgage originations.

While the outlook for the supply side of the technical environment remains positive, the demand side of the equation remains cloudy. Banks - historically one of the largest buyers of MBS - largely remain on the sidelines. The reduction in bank demand is most clearly shown in current coupon production spreads that remain extremely wide versus history and relative to spreads asset classes. Recent regulatory changes and rate stability driven by a pause in the Fed hiking cycle should produce increased bank demand for MBS over the longer term. Agency MBS also enjoys a government guarantee of credit risk, which should bode well if the economy slows into a recession in the coming quarters. Current spread levels allow MBS investors to capture a historically wide yield/spread with a government guarantee of credit risk. These spreads look poised to tighten with the removal of technical supply pressure, normalizing rate volatility, and the eventual return of the bank demand for the asset class.

Municipals

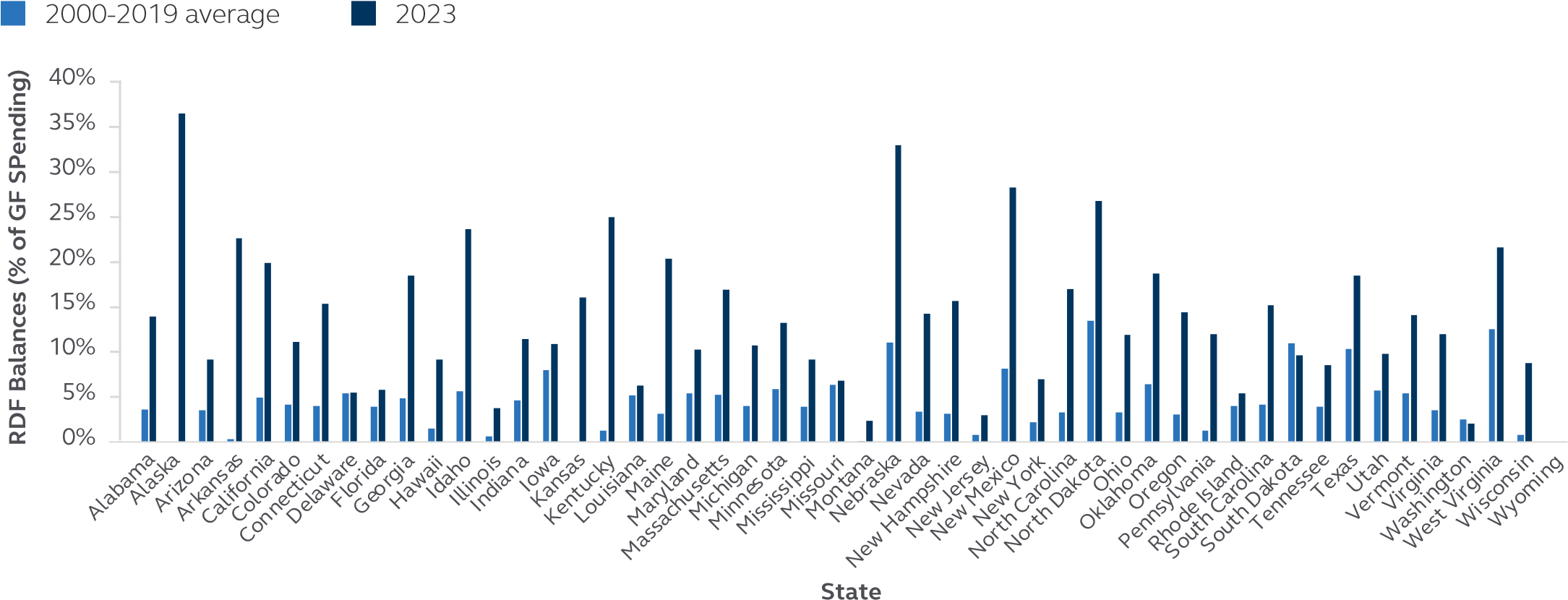

Solid reserves and balanced budgets should allow U.S. state and local credits to weather economic and revenue pressures. National economic and revenue moderation in calendar year 2023 is expected to continue into 2024, challenging state and local budgets. Early reports for fiscal year-end (June 30, 2023) performance indicate that U.S. state and local credit fundamentals remain in good shape despite the economic slowdown as governments adopted sound 2023 budgets expecting slower revenues, incorporated spending moderation, and bolstered solid reserve balances to manage potential shortfalls and/or emergencies. Prior to the pandemic, U.S. state reserves averaged approximately 10% of the budget whereas they currently stand close to 20% (Exhibit 12).

Based on conservative economic forecasts continuing the expectation of slower revenue growth and moderate spending increases, state and local governments have introduced reasonable fiscal year 2024 budgets. Over the past three years, governments have focused on bolstering reserves, maintaining budgetary balance, and increasing pension liability funding, all positive credit factors. Additionally, governments have institutionalized many of these policies thereby eliminating much of the political change risk.

While certain governments remain vulnerable to cyclical vagaries (e.g., equity-driven income taxes, natural resources/energy generated excise taxes, and natural disasters), our outlook on the U.S. state and local government sector remains stable-to-positive under a mild recession scenario.

EXHIBIT 12

U.S. states increase reserves (2000-2019 average vs. 2023)

{kind=link}

As of June 22, 2023. Source: National Association of State Budget Officers (NASBO), Fall Fiscal Survey of States (1989 - 2022), and Spring Fiscal Survey of States (2023). Survey data were self-reported by executive state budget officers in all 50 states.

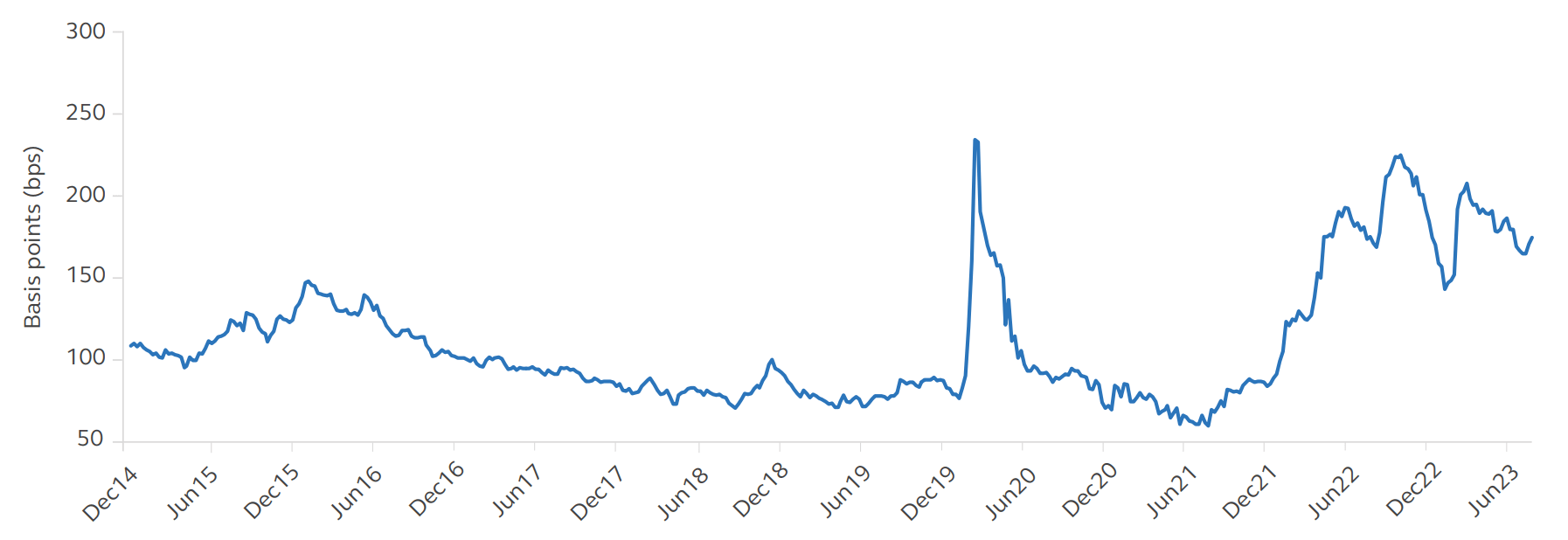

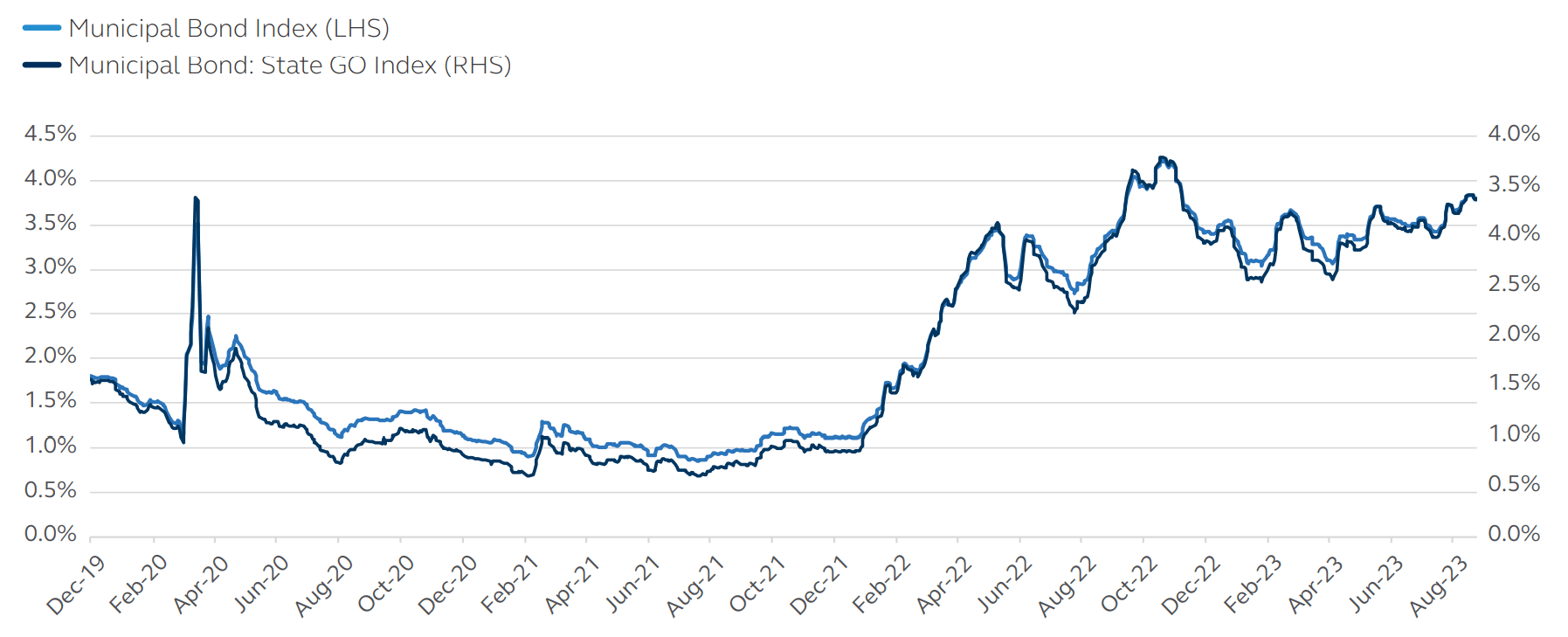

Despite relatively tight credit spreads, we continue to like state general obligations ((GO)) as one of the more resilient and defensive municipal sectors. State GOs are largely high-quality credits (33% are AAA-rated, 63% are AA-rated, and 4% are A-rated), which should help the sector weather an economic slowdown. The S&P Municipal Bond State General Obligation Index has outperformed the broader municipal index since early 2021, primarily due to credit spreads of higher beta names compressing on stronger financial performance as well as rating upgrades (Exhibit 13).

While there may be limited upside in the near term at current spreads, we still see value in this sector due to its defensive characteristics and find it attractive to go into a more challenging economic environment. Total state tax-supported debt levels are expected to remain flat this year relative to prior years, and financial performance will likely remain solid though supply from this sector might gradually increase. Given the defensive characteristics of this sector, we favor down in credit quality to names offering more spread (i.e., Illinois (A3/A-) and New Jersey (A1/A)).

EXHIBIT 13

Yield-to-worst: State GO Index vs. Municipal Bond Index

{kind=link}

Emerging market debt

In China, negative sentiment from the property sector, the collapse in local government revenues, sharp drops in credit demand, and recent issues in the wealth management trust industry have all weighed on the macro backdrop. We are likely to see more downgrades to China's growth (below 5%) and a follow-on impact on global activity. Country Garden, one of China's largest developers, has been affected by weak home sales, especially due to its large exposure to lower-tier cities that have not been doing well over the past year. A debt default of Country Garden could potentially trigger more pain for the property sector along with social issues associated with undelivered homes. Combined with a slump in credit data and stresses in the wealth management sector, this has led to worries about a larger credit problem in China. We believe that the actions taken by the government so far have been more focused on reducing downside risks rather than on stimulatory effects. Effective policy response is required to prevent a steeper falloff in growth, and we are nearing a point in which Beijing will have to take more measures to stem the downward spiral.

Across broader EM, there is a divergence in growth, inflation, and the likely speed of policy actions. Led by Latin America, disinflation is evident across several markets. Growth across key markets, including Mexico and Brazil, remained resilient while slower growth in Chile allowed the central bank to ease monetary policy with a 100 bps rate cut. Excluding China, inflation has proven stickier in Asian economies thus rate cuts will be slower to arrive, and policy will likely remain more in line with the U.S. Fed. Across the remainder of EM, there is a wide spectrum of profiles. Sub-Saharan Africa continued to struggle with high inflation; Poland and Hungary wrestled with EU dictates; South Africa's consumer price index ((CPI)) eased despite a South African Reserve Bank on pause; and Turkey's monetary and fiscal policy indicated a return to some semblance of normal.

Within this varied macro backdrop, EM flows turned consistently negative. Higher yields in developed markets ((DM)) - driven by lower near-term recession risks and a steepening U.S. rate curve - have pulled flows back. The EM sovereign and corporate universe is somewhat bifurcated with a significant portion finding themselves fundamentally in a much better position relative to previous global liquidity cycles. Net EM issuance has remained deeply negative (gross issuance less maturities/amortizations), and all three major regions (Latin America, Asia, and EMEA) showed negative issuance levels. This issuance trend has eased technical pressure, as hard currency EMD has shown outflows YTD.

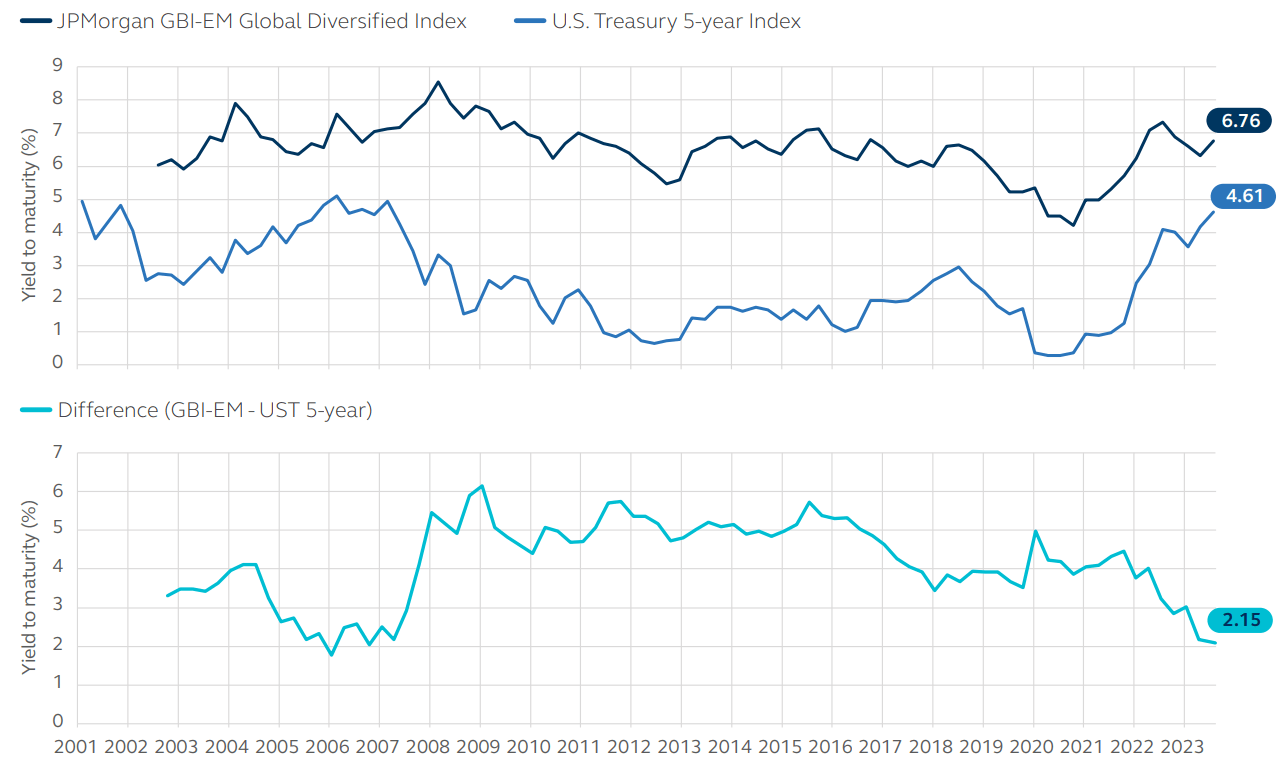

Local EM markets have proven resilient and local bond yields have significantly compressed relative to U.S. yields with risk premia now leaving very little cushion (see Exhibit 14). As we move forward, EM policymakers will be challenged to balance their domestic growth outlooks, rate trajectories, and foreign exchange dynamics all while the larger EM market keeps an eye on China's macroeconomic policy response and potential global GDP secondary impacts.

EXHIBIT 14

Yield to maturity

{kind=link}

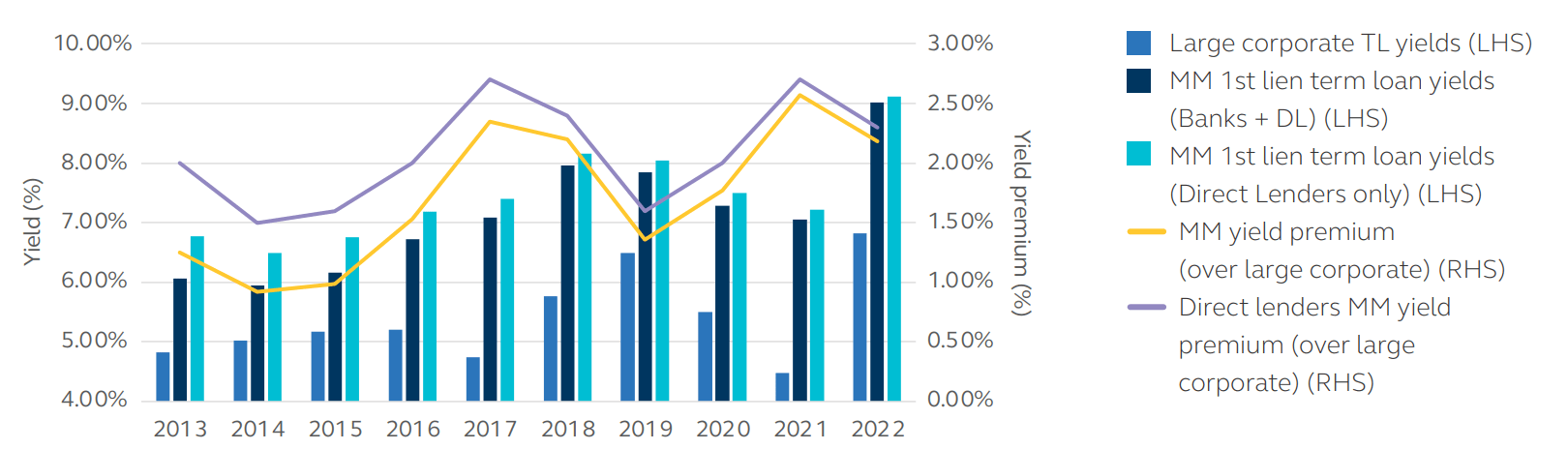

Private credit

Direct Lending

Though public markets rallied through much of 2023, opportunities remain attractive for investors in middle-market private credit. With an uncertain macro environment and less stable credit conditions, it is important for direct lenders to be diligent and assess the actual underlying credit risk of prospective borrowers while overlaying expectations for more challenging economic conditions. Coincidingly, public credit markets are being revalued on liquidity, sentiment, and a potential Fed pivot. Private credit lenders are focused on more resilient industries and borrowers while requiring relatively low leverage on newly originated transactions. Along with tighter credit terms and attractive pricing for investors, this has led to less loan origination for 2023 compared to 2022. Though new loan origination may be down, direct lenders are supporting existing borrowers/portfolio companies, often providing financing for "add-on" acquisitions or organic growth opportunities. The incremental financing is priced and structured based on current lender requirements, providing attractive value for investors.

Over the coming quarters, recessionary fears, high inflation, and public market volatility may cause investors to pause when considering an allocation to middle-market direct lending. However, we believe the loans originated during the current and upcoming period will deliver value. The combination of lower valuations, lenders reducing hold sizes, and higher borrowing costs has made larger deals more challenging in the current market. In addition to lenders being very selective, private equity sponsors are pursuing financing for companies they expect to realize attractive financial performance through more challenging economic conditions. Having less cyclical industry exposure and generally lower leverage than the public market, the private middle market should offer the opportunity for attractive absolute/relative performance, as has been the case during many prior economic cycles and periods of market volatility.

EXHIBIT 15

1st lien term loan (TL) yield and middle market ((MM)) yield premium, annual

{kind=link}

Investment grade private credit

Investment-grade private credit year-over-year deals vs. 2022 are down an estimated 20%; however, we expect flow volume to increase the pace in 4Q after a slow summer, as evidenced by the increase in deal launches through the month of September. As predicted by agent bankers earlier in the year, we are seeing more data center investment opportunities. As bank balance sheet capacity for data center credit risk becomes stretched, banks are considering various structures including private ABS, project finance, credit tenant leases, and real estate investment trusts for the most efficient way for borrowers to raise debt capital. We also saw deal-monetizing renewable power project tax credits under the new rules set by the Inflation Reduction Act, which may be a new source of deal flow. Currently, the impact of the Inflation Reduction Act is relatively benign in terms of private placement deal flow, but we expect tax equity and financing structures to accelerate growth in renewables and energy transition going forward. The trend of structured transactions with high-quality off-takers/guarantors has also continued this year. We expect to see more of these deals going forward.

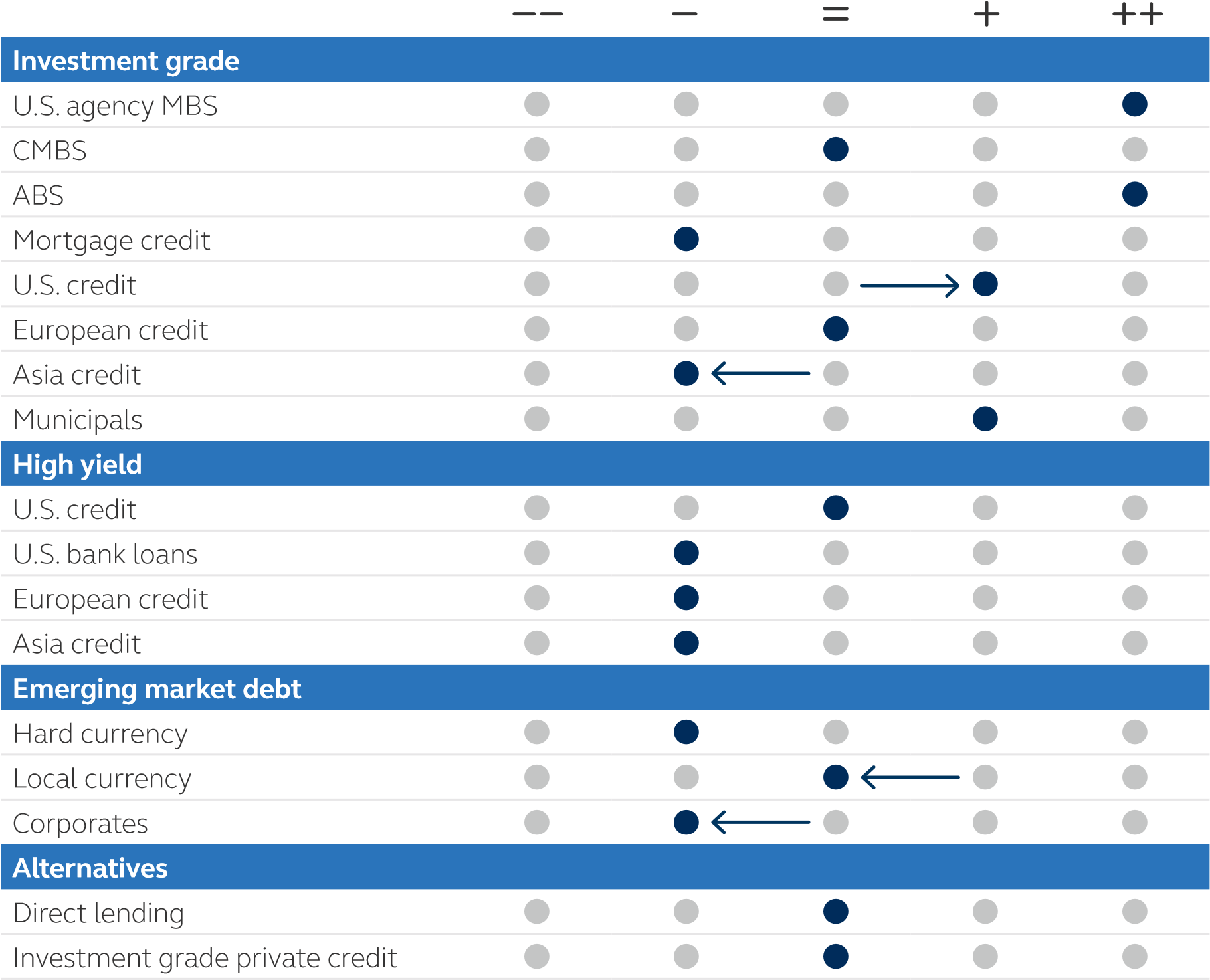

Forward-looking sector views

Underweight Neutral Overweight

{kind=link}

As of September 30, 2023. The above views reflect the relative value of the sectors shown based on forward-looking return expectations over the next 12 months. Arrows represent the quarter-over-quarter change in forward-looking views.

Conclusion

While market participants will continue to view positive economic data as further evidence of an impending soft landing, many recessionary signals are still flashing red as we head into the fourth quarter of 2023, including one of the most reliable recessionary indicators - an inverted yield curve. And while it may not be on the immediate horizon thanks to surprisingly robust consumer spending, we expect further economic slowing that ultimately culminates in a short and shallow U.S. recession over the near term.

With rate cuts unlikely over the remainder of the year, high-quality fixed income will likely continue to deliver attractive returns on a risk-adjusted basis as the Fed maintains its higher-for-longer rate stance. Most fixed-income asset classes should fare well, supported by attractive yields and resilient fundamentals. While no one can say for certain what the final quarter of 2023 will hold, we are preparing for heightened economic uncertainty and turbulence.

Principal Fixed Income: A leading global fixed-income platform

Principal Fixed Income is the fixed-income investment management platform of Principal Asset Management and manages U.S. $135.7 billion in assets under management as of June 30, 2023. Principal Fixed Income has capabilities that span all major fixed-income sectors. Our globally integrated platform with investment centers worldwide and over 100 investment professionals, helps to directly access global fixed-income markets and deliver a diversity of investment perspectives. Our structure and proprietary investment tools foster collaboration across sector-specialty teams, whether the sector is explicitly integrated into a portfolio or not. In our view, this diversity of insight helps each sector-specialty team formulate richer investment theses and make better-informed investment decisions on behalf of our clients.

Investment Strategy Group

The creation of the fixed income outlook is a collaborative effort led by the Principal Fixed Income Investment Strategy Group. The Investment Strategy Group is comprised of the senior-most investment professionals from across the platform and is responsible for identifying key macroeconomic factors that are most likely to drive investment performance across global fixed-income markets. Output from the Investment Strategy Group is formalized through Principal's proprietary Macro Risk Outlook framework and informs investment processes across the platform, acting as a top-down complement to the platform's bottom-up fundamental research capability.

{kind=link}

Risk considerations

Investing involves risk, including possible loss of principal. Past Performance does not guarantee a future return. All financial investments involve an element of risk. Therefore, the value of the investment and the income from it will vary and the initial investment amount cannot be guaranteed. Fixed-income investment options are subject to interest rate risk, and their value will decline as interest rates rise. Potential investors should be aware that Investment grade corporate bonds carry credit risks, default risks, liquidity risks, currency risks, operational risks, legal risks, counterparty risks, and valuation risks. Lower-rated securities are subject to additional credit and default risks. Asset-backed securities are affected by the quality of the credit extended in the underlying loans. As a result, their quality is dependent upon the selection of the commercial mortgage portfolio and the cash flow generated by the commercial real estate assets. Commercial Mortgage-Backed Securities carry greater risk compared to other securities in times of market stress. There may be less information on the financial condition of municipal issuers than on public corporations. The market for municipal bonds may be less liquid than for other bonds. Emerging market debt may be subject to heightened default and liquidity risk. Private credit involves an investment in non-publicly traded securities that are subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss.

Important information

This material covers general information only and does not take account of any investor's investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast, or prediction of future events regarding an investment or the markets in general. Information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity. Any reference to a specific investment or security does not constitute a recommendation to buy, sell, or hold such investment or security, nor an indication that the investment manager or its affiliates has recommended a specific security for any client account. Subject to any contrary provisions of applicable law, the investment manager and its affiliates, and their officers, directors, employees, and agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in the information or data provided.

This material may contain `forward-looking' information that is not purely historical in nature and may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

All figures shown in this document are in U.S. dollars unless otherwise noted. All assets under management figures shown in this document are gross figures, before fees, transaction costs, and other expenses and may include leverage unless otherwise noted. Assets under management may include model-only assets managed by the firm, where the firm has no control as to whether investment recommendations are accepted, or the firm does not have trading authority over the assets.

Index performance information reflects no deduction for fees, expenses, or taxes. Indices are unmanaged and individuals cannot invest directly in an index.

This document is intended for use in:

- The United States by Principal Global Investors, LLC, which is regulated by the U.S. Securities and Exchange Commission.

- Europe by Principal Global Investors (Ireland) Limited, 70 Sir John Rogerson's Quay, Dublin 2, D02 R296, Ireland. Principal Global Investors (Ireland) Limited is regulated by the Central Bank of Ireland. Clients that do not directly contract with Principal Global Investors (Europe) Limited ("PGIE") or Principal Global Investors (Ireland) Limited ("PGII") will not benefit from the protections offered by the rules and regulations of the Financial Conduct Authority or the Central Bank of Ireland, including those enacted under MiFID II. Further, where clients do contract with PGIE or PGII, PGIE or PGII may delegate management authority to affiliates that are not authorized and regulated within Europe, and in any such case, the client may not benefit from all protections offered by the rules and regulations of the Financial Conduct Authority, or the Central Bank of Ireland. In Europe, this document is directed exclusively at Professional Clients and Eligible Counterparties and should not be relied upon by Retail Clients (all as defined by the MiFID).

- United Kingdom by Principal Global Investors (Europe) Limited, Level 1, 1 Wood Street, London, EC2V 7 JB, registered in England, No. 03819986, which is authorized and regulated by the Financial Conduct Authority ("FCA").

- This document is marketing material and is issued in Switzerland by Principal Global Investors (Switzerland) GmbH.

- United Arab Emirates by Principal Global Investors LLC, a branch registered in the Dubai International Financial Centre and authorized by the Dubai Financial Services Authority as a representative office and is delivered on an individual basis to the recipient and should not be passed on or otherwise distributed by the recipient to any other person or organisation.

- Singapore by Principal Global Investors (Singapore)Limited (ACRA Reg.No.199603735H), which is regulated by the Monetary Authority of Singapore and is directed exclusively at institutional investors as defined by the Securities and Futures Act 2001. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

- Australia by Principal Global Investors (Australia) Limited (ABN 45 102 488 068, AFS Licence No. 225385), which is regulated by the Australian Securities and Investments Commission and is only directed at wholesale clients as defined under the Corporations Act 2001.

- Hong Kong SAR (China) by Principal Asset Management Company (Asia) Limited, which is regulated by the Securities and Futures Commission. This document has not been reviewed by the Securities and Futures Commission.

- Other APAC Countries/Jurisdictions. This material is issued for Institutional Investors only (or professional/sophisticated/qualified investors, as such term may apply in local jurisdictions) and is delivered on an individual basis to the recipient and should not be passed on, used by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

Principal Global Investors, LLC ((PGI)) is registered with the U.S. Commodity Futures Trading Commission (CFTC) as a commodity trading advisor ((CTA)), a commodity pool operator (CPO), and is a member of the National Futures Association (NFA). PGI advises qualified eligible persons (QEPs) under CFTC Regulation 4.7.

Principal Asset Management is a trade name of Principal Global Investors, LLC.

Principal Funds are distributed by Principal Funds Distributor, Inc.

Principal Fixed Income is an investment team within Principal Global Investors.

© 2023 Principal Financial Services, Inc. Principal®, Principal Financial Group®, Principal Asset Management, and Principal and the logomark design are registered trademarks and service marks of Principal Financial Services, Inc., a Principal Financial Group company, in various countries around the world and may be used only with the permission of Principal Financial Services, Inc.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Q4 2023 Fixed Income Outlook: Recession Takeoff Delayed But Not Canceled