QSI - Quantum-Si: Highly Speculative With A Strong Appeal

2023-10-22 09:33:16 ET

Summary

- Quantum-Si incorporated is a pioneering company in the field of proteomics with its innovative Platinum platform.

- The company's revenue model is still in its early stages, making it a highly speculative investment.

- QSI's valuation is challenging but has explosive revenue potential in the growing proteomics market.

- I rate QSI a "buy," albeit with caution, advocating for a speculative allocation within an investment portfolio, given the potential multibagger nature of the stock and inherent risks.

Quantum-Si incorporated. ( QSI ) has been a pioneering entity in proteomics since 2013. I believe QSI's revolutionary Platinum platform is the linchpin of its revenue model. However, QSI’s nascent revenues still make it a highly speculative investment proposition. QSI’s valuation is challenging because it’s just starting to finish its developmental phase and should start ramping up production into Q3 and Q4 of this year. While I recognize that the company has explosive revenue potential, it’s also important to temper such expectations by acknowledging that investing in promises and PowerPoint growth is not advisable. Hence, I posit a 'buy' rating on QSI, accentuating the prospective multibagger nature of the stock, albeit within a speculative tranche of an investment portfolio.

Business Overview

Quantum-Si incorporated has held a significant position in the expanding field of proteomics since 2013 to enhance protein sequencing through its innovative technology. Their main source of income comes from the Platinum platform, a special chip technology that offers a new way to study proteins. Being the first to market and currently the only available low-cost protein sequencing tool, QSI has a unique advantage. This platform can help speed up drug discovery and diagnostics by making proteomics research digital.

Source: Quantum-Si at the 41st Annual J.P. Morgan Healthcare Conference

The Platinum platform is designed to democratize single-molecule protein sequencing globally. This initiative propels comprehension of complex biological systems forward, a pivotal step for advancing medical science. In my view, the positioning of QSI in the market, coupled with its innovative product line, harbors substantial growth prospects, sketching a promising trajectory toward achieving commercial success. The Platinum platform caters to a wide range of users , including academic institutions and industry-based laboratories, regardless of their level of bioinformatics expertise.

QSI was developing the Carbon platform to automate sample preparation for protein sequencing and genomics, streamlining lab procedures, particularly with third-party DNA sequencing technologies. Carbon, part of a broader technology suite including the Platinum platform and QSI Cloud software, aims to address common challenges in genomics and proteomics by enhancing sample prep efficiency and reliability. Although Carbon can minimize sample prep variation and optimize workflow, it's not essential for operating the Platinum instrument. Currently, its development is paused , and its business case is under analysis.

Source: Quantum-Si at the 41st Annual J.P. Morgan Healthcare Conference

Market Entry and Technological Advancements

The Platinum instrument commenced its journey into the market by initiating order-taking in December 2022, followed by the onset of commercial shipments in January 2023. Parallel to this, the sustained endeavor in research and development is targeted toward refining this instrument and scrutinizing the business viability of the Carbon sample preparation solution. QSI released a software upgrade in July, addressing customer feedback. This upgrade enhanced the user interface and provided additional visualizations at the amino acid level, resulting in positive feedback from users .

The Cloud software seamlessly pairs with the Platinum instrument, providing a unified, intuitive environment for planning, setting up, and analyzing sequencing runs. As each run proceeds, the generated data is automatically uploaded to the Cloud, where proteins are identified without requiring bioinformatics expertise. This software can be securely accessed from any computer, allowing analysis from any location and promoting collaboration with colleagues and partners worldwide, making the process of protein sequencing data analysis effortless and accessible.

An expenditure increase is anticipated to invigorate the sales, marketing, development sectors, and inventory accumulation. Several factors could potentially fuel the acceleration of cash requirements, including but not limited to setbacks in reaching scientific and technical milestones, unforeseen capital outlays, modifications in business or commercialization strategies, ramifications of the COVID-19 pandemic, the financial demands of maintaining a public company status, and the prospect of future acquisitions.

QSI's latest earnings call underscored fiscal vulnerability, hinging on acquiring future financing under favorable terms. As stated, the inability to secure such financing could impart a detrimental effect on business operations, financial stability, and the capacity to respond adeptly to market pressures or seize acquisition opportunities. The mention of potential setbacks, particularly those tied to scientific and technical milestones and unforeseen capital expenditures, underlines a level of uncertainty that could, in my opinion, necessitate a conservative financial strategy to ensure sustained growth and stability.

QSI's conservative stance could act as a buffer, mitigating the adverse impacts of unforeseen challenges, thereby ensuring a steadier, albeit possibly slower, trajectory toward achieving long-term business objectives. And it's important to note that financial stability is crucial for attracting customers and growth. Fortunately, I estimate that, indeed, QSI should have enough liquidity to last until roughly 2027 at the current cash burn rate. Thus, I believe it'll be able to benefit from the promising proteomics market valued at $36.8 billion . In fact, QSI’s market continues to grow at an impressive CAGR of 14.6%. So, QSI's Platinum platform is undoubtedly poised to benefit from this growth trend.

Source: Markets and Markets.

QSI's Cash Burn and Liquidity

However, QSI’s promising potential differs significantly from its nascent revenue streams. QSI’s current revenue largely depends on instrument and consumables sales, augmented by service maintenance contracts. The launch of the Platinum instrument and the commencement of commercial shipments in January 2023 marked a significant milestone. However, QSI has only recognized revenue of $0.2 million in Q2 2023, underscoring the company’s embryonic commercialization stage. QSI’s ongoing R&D efforts to enhance the Platinum instrument and the evaluation surrounding the Carbon sample preparation solution are crucial for long-term success, and it anticipates accelerated spending to bolster sales and marketing teams, continue product development, and build inventory.

Therefore, QSI's cash burn dynamics for the six months ending on June 30, 2023, primarily stem from the operating activities, with net cash used in operating activities amounting to $51.6 million. Cash 1H2023 cash burn increased compared to 1H2022, which was $49.2 million. The primary driver of this cash usage is the continued investments in R&D efforts and the ramp-up of commercialization activities. QSI’s operating expenses reveal a YoY decrease in R&D costs by 14.2% for Q2 2023, primarily attributed to refined R&D activities and restructuring initiated in Q1 2023. Conversely, SG&A expenses saw a slight uptick due to ramping up commercial sales activities.

So, to finance this cash burn, QSI generated positive cash flows from its investing activities, which amounted to $55.2 million. Yet, these were primarily due to sales of marketable securities totaling $59.5 million. Similarly, in 2022, the net cash provided by investing activities was considerably higher at $94.5 million, primarily due to sales of marketable securities totaling $100.1 million. For context, at the end of the latest quarter, QSI reported $87.9 million in cash and $209.3 million in marketable securities, representing approximately $297.2 million in remaining liquidity to fund its ongoing cash burn. As previously noted, such cash burn is roughly $103.2 million (annualizing 1H2023 figures). Thus, QSI should have enough liquidity to last another 2.9 years (late 2026, more or less).

Valuation Analysis

From a valuation perspective, pricing a company like QSI is tricky. The company has no revenues and is still in the development phase of its product. Yet the key consideration regarding QSI is its technology platform that departs from traditional proteomics, often replacing lengthy conventional procedures with a streamlined workflow that delivers results within a day. The introduction of NGPS, characterized by its massively parallel sequencing capability, signifies a notable advancement over previous sequential methodologies. This enhancement provides a high-resolution, unbiased insight into the proteome, with recent developments enabling an in-depth examination of amino acid variations. In my view, the company's integration of Platinum instruments alongside the QSI Cloud software service is a thoughtful step toward digitizing proteomics. This assertion stems from reputable academic institutions' noted adoption of the Platinum instrument, indicating a positive reception within the scientific community. The instrument’s simplified workflow, which doesn't necessitate advanced expertise, could lower the entry barriers to proteomics research, making it a valuable asset to the field.

This digital transition, highlighted by the capacity for single-molecule detection, embodies the company’s innovative ethos. The Quantum-Si Cloud software service, as a scalable informatics platform for protein sequence data analysis, aids in seamlessly integrating protein identification into existing research initiatives, thus hastening the realization of research objectives. This ease of integration is crucial as it could foster broader platform adoption, supporting the claim of digital transformation as a linchpin for contemporary scientific progress. This is further illustrated by the collaborative integration of Biovista’s VIZIT exploration tool, which augments the platform's analytical competencies. This enhancement allows researchers to delineate connections between protein sequences and diseases, other proteins, and post-translational modifications, cultivating a favorable environment for innovation within the proteomics sector.

Yet, QSI's revenue capabilities are still budding, as demonstrated by the revenues of $0.5 million in the first half of 2023. A backlog of around $0.1 million hints at potential revenue, although its conversion remains to be determined due to the company's fledgling status in the market. Furthermore, such a backlog is modest compared to the ongoing cash burn rate.

Seeking Alpha.

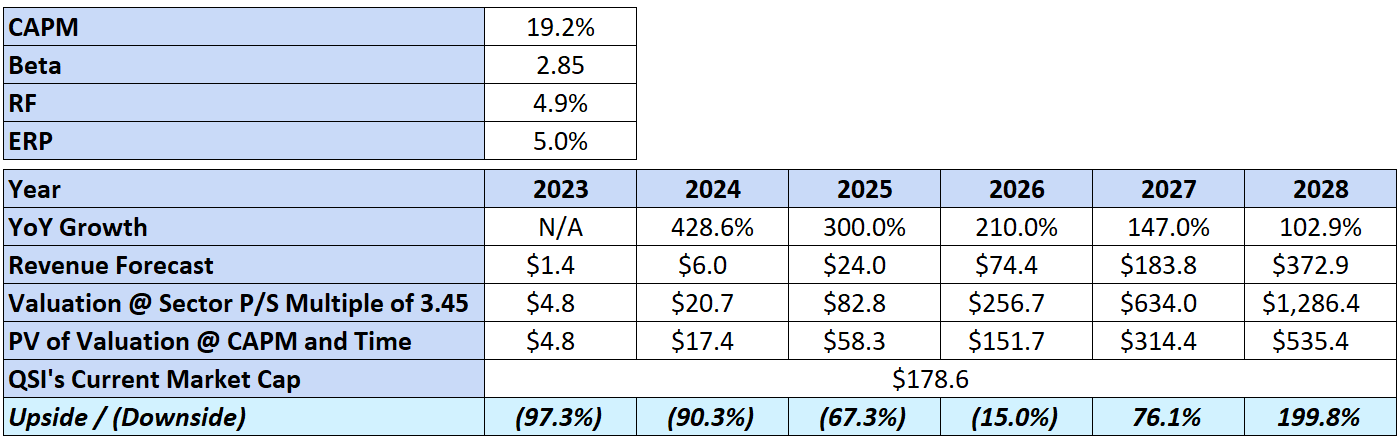

But, as you can see, QSI is expected to escalate its revenue generation starting from Q3 and Q4 of 2023. By 2024, the revenue is projected to reach $6.0 million annually. This anticipated revenue growth underscores the potential effectiveness and acceptance of QSI’s offerings and indicates a pivotal shift in risks from R&D to scaling and production capabilities. This shift is crucial, as it substantially lessens the company's risk profile; securing financing for scaling operations is often less challenging than funding groundbreaking technological development.

Moreover, estimates for QSI’s 2024 revenues reflect significant growth from 2023, illustrating a more than fourfold increase. Suppose QSI maintains this growth trajectory, even with a moderating growth rate. This is reasonable, given the market size is forecasted to burgeon to $72.9 billion by 2028. I believe this market expansion bodes well for QSI as it could continue to increase yearly revenues substantially, provided its scaling and production capabilities are enhanced concurrently. The alignment of QSI's revenue growth with market expansion is pivotal, and this synchrony will be instrumental in realizing the substantial revenue potential projected for 2028.

{kind=link}

Naturally, the above are relatively speculative forecasts, which is the best we can do given QSI’s early ramp-up stages. However, this does showcase that there’s indeed a way to justify QSI’s current valuation. And in fact, the further we forecast its potential growth, the higher its upside potential becomes. However, all of this is contingent on rosy forecasts holding up, and as investors, we often see that is not always the case. Thus, I think, as a whole, QSI remains in a highly speculative phase. Yet, it’s currently in the most exciting part of its speculative phase because it’s just starting to ramp up after seemingly working out its products' quirks.

So, while it’s still highly uncertain the growth pace it’ll experience and the hurdles it’ll encounter, I do think there’s a persuasive bullish case for QSI if one thinks of it as a smaller part of one’s portfolio that could potentially be a multibagger if it all works out. Other than that, I don’t think QSI is viable as a main component of any investor's portfolio. So overall, I rate QSI a “buy” because it looks incredibly promising at this point. Yet, I temper my bullish rating by stressing that QSI should still be considered a small speculative part of one’s portfolio. After all, it’s simply too risky to make it a meaningful portion of an investor's portfolio because, as the table shows, if revenue growth doesn’t materialize or grow as much as expected, then the downside potential is massive.

{kind=link}

Conclusion

Overall, QSI’s financials and prospects reveal a narrative of innovation melded with caution under the broader umbrella of a burgeoning proteomics market. QSI is seemingly teetering on the brink of escalating its operations, with a projection of a notable revenue increment by 2024, benefiting from its market anticipated size of $72.9 billion by 2028. However, its prevailing cash burn further exemplifies the inherent risks entwined with QSI's ambitious growth trajectory. Thus, QSI’s speculative revenue projections frame its bullish narrative with cautious optimism. While I advocate a “buy” rating for QSI, I stress that investors should earmark QSI as a speculative portfolio slice. This prudent stance, dovetailed with the burgeoning promise of QSI's technology, encapsulates the narrative of QSI being a speculative yet potentially rewarding market proposition.

For further details see:

Quantum-Si: Highly Speculative With A Strong Appeal