CHIC - Questions About China Intensify

2023-08-22 07:00:00 ET

Summary

- We have seen Chinese real estate and wealth management issues in years past, and they never came to a hard landing.

- China has once again slipped into deflation. The latest year-over-year inflation rate was -0.3%.

- A Chinese devaluation would be particularly hard on export-driven Asian economies, and it is unknowable for now if a Second Asian Financial Crisis may be in the cards, despite the many reforms made since the last one.

We have seen Chinese real estate and wealth management issues in years past, and they never came to a hard landing, but the mere fact that it has not happened yet does not mean it won't ultimately happen. It is those failing real estate developers and issuers of wealth management products that cannot pay their clients of late that are raising alarms in the institutional and retail investor communities.

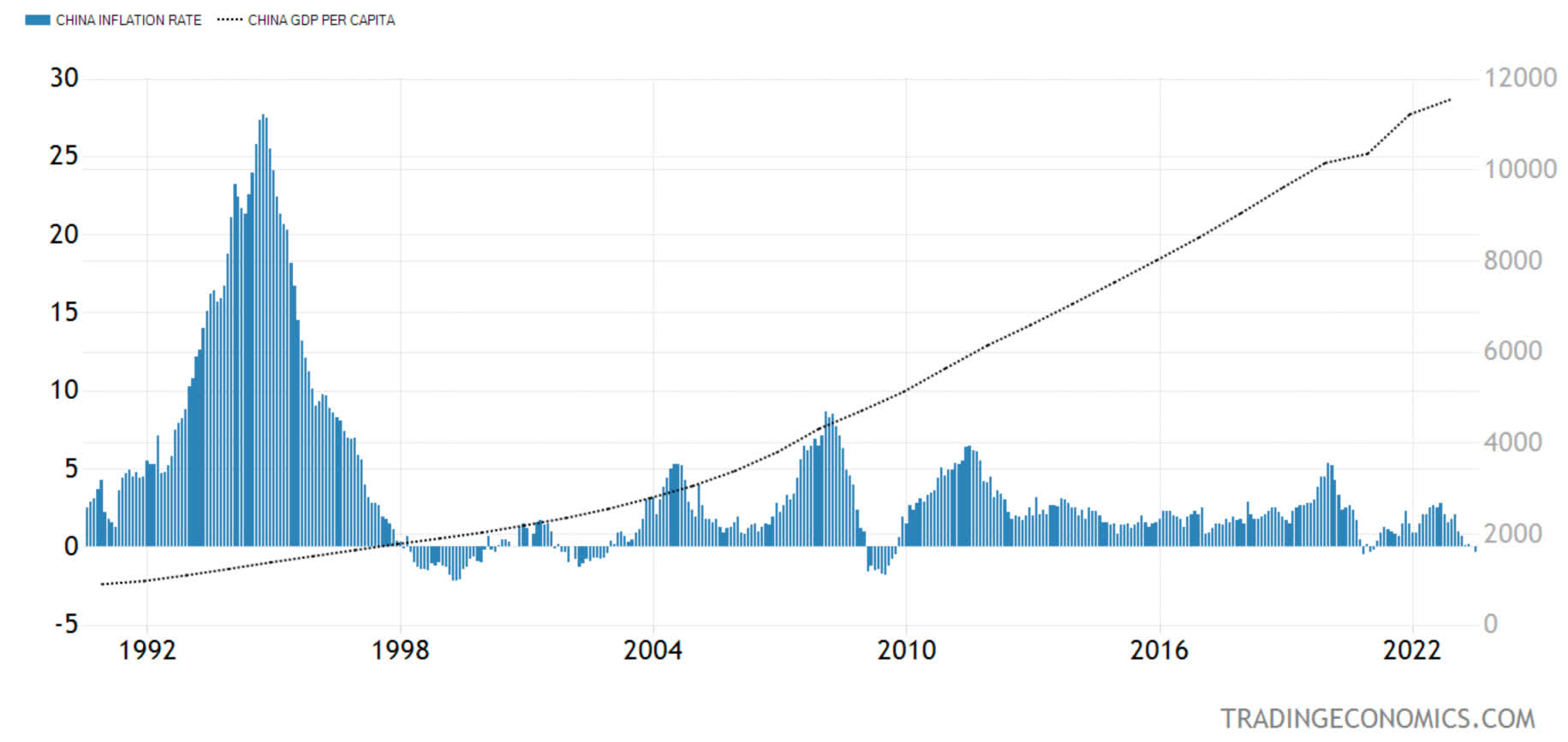

China has once again slipped into deflation. The latest year-over-year inflation rate was -0.3%.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

{kind=link}

As this chart shows, China has slipped into deflation before, most recently after the draconian COVID lockdowns in 2020, and also right after the Wall Street crash in 2008-09, and right after the dot.com crash in 2001, and during the Asian Crisis of 1997-1998. None of these previous deflationary periods came during good times for the global or Asian economy, but the fact that the global and regional economies are holding up right now and China has still entered into deflation may indicate that this may be a sign of a much bigger domestic economic problem than Beijing will ever admit.

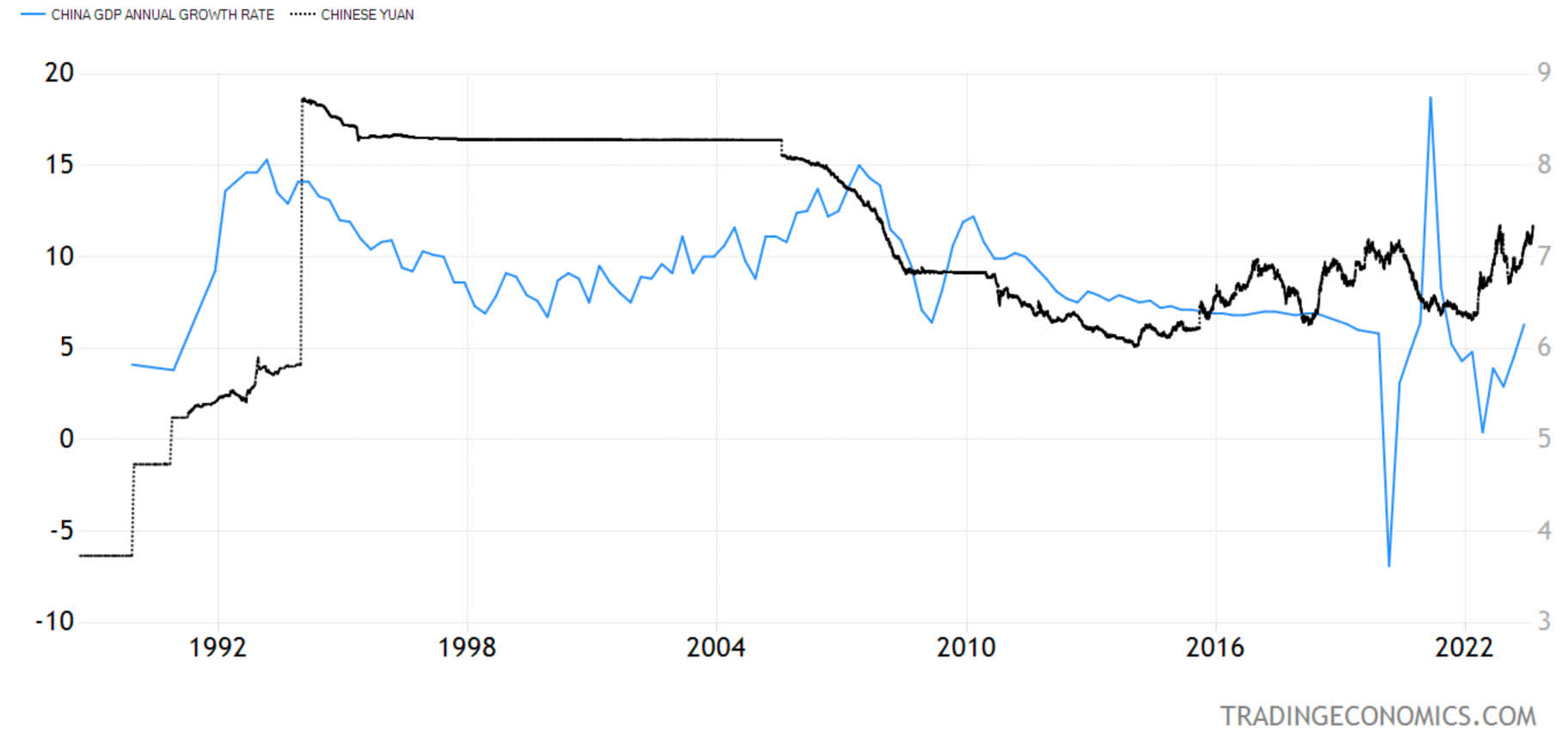

The reason for the massive Chinese devaluation of the yuan in 1994 - to the tune of 33% (see the spike in inflation rates, above) - was a nasty recession in 1993 that was never officially acknowledged by the Chinese authorities, but it showed up in bank loan loss provisions, according to some experts on Asia. Officially, there was no recession, but the horrific devaluation ultimately was a big contributing factor to the onset of the Asian Crisis in 1997-1998, which was nasty for their local economic partners.

The Chinese have a new Premier - a President Xi loyalist who will do as he is told - so I would not put that much weight in the promises of the previous Premier, who used to often say that they would never use the currency to jump-start the Chinese economy. I think they will - if they feel they have no other choice.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

{kind=link}

A Chinese devaluation would be like a deflationary tsunami for the global economy. A Chinese devaluation would be particularly hard on export-driven Asian economies, and it is unknowable for now if a Second Asian Financial Crisis may be in the cards, despite the many reforms made since the last one.

A teetering Chinese real estate market is not good for domestic demand as many Chinese use a reported 60 million empty apartments as their savings accounts. Any further weakening of the real estate market should have a notable effect on Chinese economic growth.

What the Chinese have done with their unique system of state-sponsored capitalism under the leadership of the CCP is to try to even out normal economic cycles via draconian intervention in the economy and thus avoid recessions. Personally, I do not believe economic cycles can be ironed out with lending quotas and state control of the financial system. Lending quotas create bad loans and ultimately create a bigger problem later on. I am watching with great interest how the Chinese situation is developing as they are overdue for a reckoning. They have postponed quite a few recessions with their interventions since 1994.

Here Comes Jackson Hole

Fed Chair Jerome Powell rattled both stock and bond markets last year with his Jackson Hole speech, and I doubt he will do the same this year, as we have a much more benign inflation outlook this year, and the Fed tightening cycle is close to completion. Still, you never know with Jay Powell, as his FOMC press conferences have caused many whipsaws over the past year. If the market was weak when the FOMC statement came out, it would rally in the press conferences and vice versa as he elaborated on his views.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

{kind=link}

Keep in mind that the M2 Money Supply shrank for the seventh consecutive month in June to the tune of -3.6%. The Fed is shrinking its balance sheet to the tune of $95 billion per month and the U.S. Treasury is in the midst of a $1 trillion issuance of Treasury bonds as they nearly depleted their account at the Fed, as House Speaker McCarthy negotiated the debt ceiling deal with them. That's a lot of liquidity being sucked out of the U.S. financial system in short order, so more rate hikes at this point seem like overkill, literally.

The 10-year Treasury bond yield tagged 4.33% last week, matching its prior (October 2022) multi-year high. If the 10-year blasts past 4.33% - from a purely technical perspective, in theory - it can rise to 5.25%, but I don't think it can make it there without causing serious economic and stock market problems.

But then, I didn't think we would come anywhere near 4.33% in August 2023, and here we are.

All content above represents the opinion of Ivan Martchev of Navellier & Associates, Inc.

Disclosure: *Navellier may hold securities in one or more investment strategies offered to its clients.

Disclaimer: Please click here for important disclosures located in the "About" section of the Navellier & Associates profile that accompany this article.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Questions About China Intensify