KIO - Quick Notes: KIO Rights Offering

Summary

- KIO announces a rights offering.

- This offering may be highly dilutive to NAV.

- Investors who held past the ex-rights date should subscribe or sell their rights to offset the effect of dilution.

Author's note: This article was released to CEF/ETF Income Laboratory members as part of the CEF Weekly Roundup on January 17, 2023, with certain numbers updated. Please check the latest data before investing.

KIO rights offering

The KKR Income Opportunities Fund ( KIO ) have announced a rights offering. From the press release (excepts):

January 12, 2023 | KKR Income Opportunities Fund Announces Terms of Rights Offering and Declares Monthly Distributions. The Board of Trustees (the “ Board ”) of KKR Income Opportunities Fund (the “ Fund ”) ((KIO)) has approved the terms of the issuance of transferable rights to its shareholders of record as specified below. The record date for the Offer is currently expected to be January 23, 2023 (the “Record Date”). Record Date Common Shareholders will be entitled to purchase one new Common Share for every three Rights held (1 for 3). The proposed subscription period is currently anticipated to expire on February 16, 2023 , unless extended by the Fund (the “Expiration Date”). The Rights are transferable and are expected to be admitted for trading on the New York Stock Exchange (the “NYSE”) under the symbol “KIO RT” during the course of the Offer. The subscription price per Common Share (the “Subscription Price”) will be determined on the Expiration Date, and will be equal to 92.5% of the average of the last reported sales price of a Common Share of the Fund on the NYSE on the Expiration Date and each of the four (4) immediately preceding trading days (the “Formula Price”). If, however, the Formula Price is less than 82% of the Fund’s net asset value (“NAV”) per Common Share at the close of trading on the NYSE on the Expiration Date, the Subscription Price will be 82% of the Fund’s NAV per Common Share at the close of trading on the NYSE on that day.

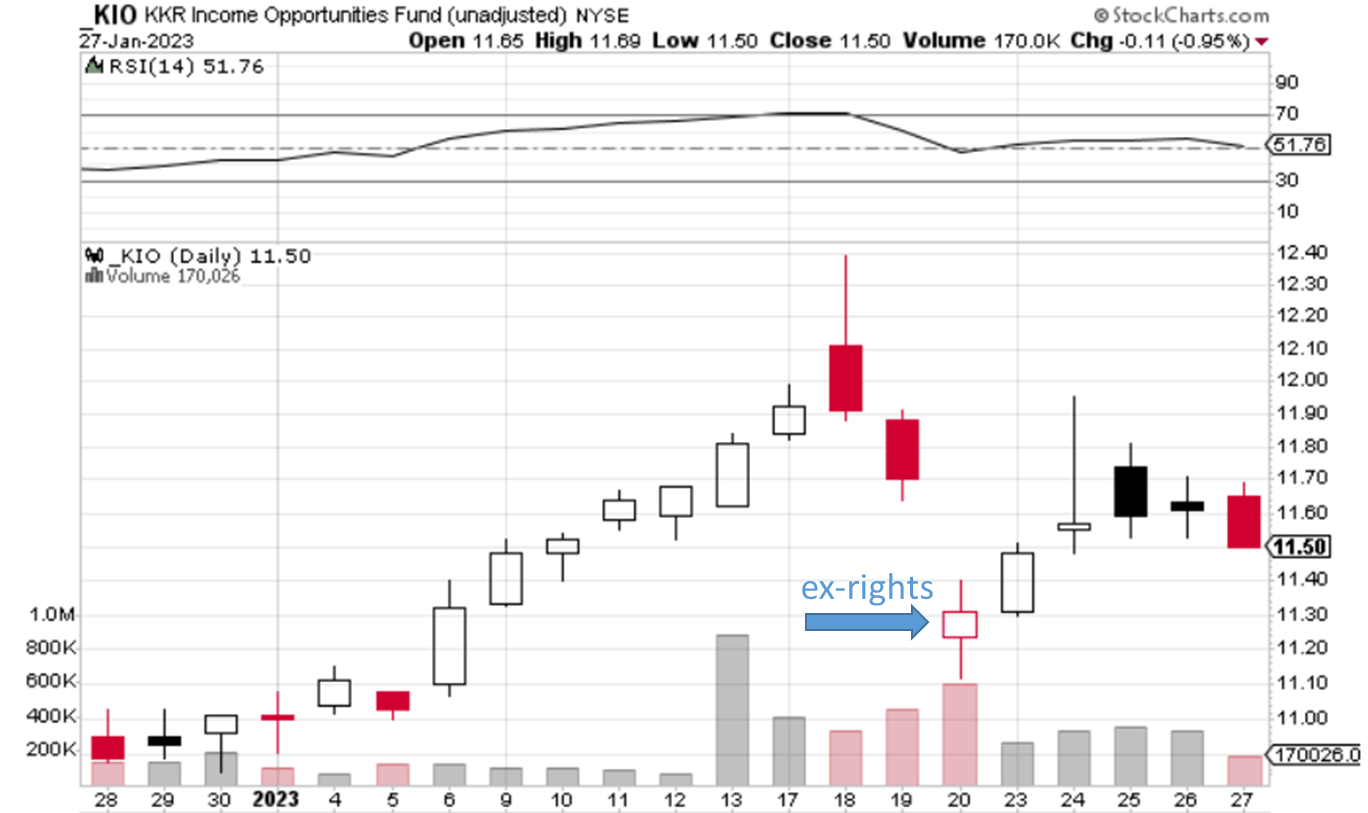

To sum up, this will be a transferable 1-for-3 offering with a subscription price that will be the higher of 92.5% of market price or 82% of NAV, with the market price being defined as the average of the closing market price of the fund on the final five days of the offering. The ex-rights date for the offering is January 20, 2023 , while the offering is anticipated to expire on February 16, 2023. The rights are expected to trade on the NYSE under the symbol “KIO RT” during the course of the offering.

KIO's last rights offering was in October 2017, which we covered at the time here ( public link ). I'm not sure what determined the timing of this rights offering, being executed 5.5 years after the previous one and while we are still in the throes of bear market. One possibility could be to top-up the asset base of the fund. As we can see from the chart below, 2017's offering raised the AUM from around $270 million to over $350 million. However two bear quick markets in succession have brought the fund's assets back down to around the $250 million mark. KIO isn't a very large fund at this size, so I imagine that the managers wanted to make the fund more economical run by expanding its size and increasing its economies of scale.

YCharts

Unfortunately, what benefits the managers may not necessarily be beneficial for shareholders. For investors, the total AUM is generally of little consideration (liquidity aside); rather, performance is determined on a per-share basis.

Here, we see that the offering is likely going to be very dilutive to the NAV/share of the fund. KIO's subscription price will be the higher of 92.5% of market price or 82% of NAV at expiry (same conditions at the 2017 offering). While this does place a floor on the offering price (preventing a vicious cycle of widening discounts causing further dilution causing further discount widening), the floor is set at a very low -18% level.

We have previously observed for other rights offering that a discount floor for a rights offering can act as a magnet to draw the valuation of the fund towards it as the expiry date approaches. However, given that the discount floor is at a very low level of -18%, I consider this unlikely to be reached in this case. For the 2017 offering, the discount declined from around -2% before the offering was announced to a low of around -14% at expiry, but the floor of -18% was not breached.

YCharts

So far, we haven't seen much reaction from KIO after the offering was announced after hours last Thursday (January 12th, 2023). The next day, KIO even rose by +1.13%!

YCharts

It is also not clear whether there will be a sales load for the newly offered shares as well. The 2017 rights offering was underwritten by UBS which charged a hefty 3.75% sales load on the newly issued shares, which was borne by shareholders. The relevant section of the N-2/A form is currently blank, but it remains to be seen whether this will be updated as the offering gets underway.

{kind=link}

{kind=link}

As this is a 1-for-3 offering, so the maximum that the fund can grow is by +33% from this offering. Assuming full subscription at a -18% discount floor, the maximum dilution is -4.5% to the NAV/share, not counting any additional sales load charged. An investor can offset the effect of dilution by subscribing for the maximum amount possible.

Plan of action

When this article was initially released to our members on January 17, 2023, we wrote:

I do expect there to be a large ex-rights day drop for KIO on January 20th, 2023 because the rights will be very valuable unless the fund's discount approaches the -18% discount floor. This is because the subscription price is set at an attractive discount of -7.5% to the market price of the fund at expiring, giving a large incentive to subscribe. At the same time, because the shares will likely be offered at a deep discount to the NAV, the extent of dilution will likely be large as well. For investors who do not wish to expand their share count in KIO, I would recommend selling the fund before the ex-rights date of January 20th, 2023. History has shown that CEF prices tend to drift lower over the course of the offering period, so one can potentially rebuy the shares at a lower price once the offering concludes.

We do see that KIO did drop significantly on ex-rights date, but it has since made up some ground. KIO's current discount (as of 1/27) is -12.41%. I expect KIO's discount to hover between this level and the -18% discount floor until the offering expires.

{kind=link}

For those who sold out of KIO before the ex-rights date, in order to reduce market risk, we suggested switching to a similar fund like Ares Dynamic Credit Allocation Fund ( ARDC ) or Apollo Tactical Income Fund ( AIF ) over the course of the offering. I consider these two funds peers of KIO because they all have a flexible loan/bond fixed income mandate. KIO is probably the most aggressive of the three because of its highest allocation to CCC-rated credits (basically the lowest default rating for companies that aren't in imminent default).

{kind=link}

As can be seen from the chart below, KIO rose the most after the 2020 pandemic low, but also declined most quickly in the current bear market.

YCharts

For investors who held through the rights offering (tax reasons or otherwise) but who do not wish to expand their share count KIO, they should not forget to sell their rights on the open market to offset the effects of dilution. Letting the rights expire worthless would be the worst possible outcome!

For those who wish to subscribe for new shares, check whether your broker charges for voluntary corporate actions like rights offerings. Some of our members have reported managing to get this fee waived with a phone call to their rep.

However, remember that if KIO were to trade below at -18% discount at expiry, then one should not subscribe as it would be cheaper to buy the fund on the open market.

It should also be noted that KIO shareholders who hold the fund through the ex-rights date are primary rightsholders who also have the ability to oversubscribe for excess shares that are not allocated through the primary offering. Investors who buy KIO rights on the open market are secondary rightsholders and will not have the oversubscription privilege.

In the same announcement as the rights offering, KIO also announced a boost in its monthly distribution from $0.1050 to $0.1215 per share (+15.71%). This is positive and also follows similar moves by ARDC and AIF. Remember, these funds have a significant senior loans component which are floating rate, allowing their income to rise in a rising rate environment. According to the fund's annual report dated October 31, 2022, the distribution for the financial year of 2022 was 107% covered by net investment income at the old rate. As of 1/27, KIO yields 10.96%.

YCharts

For further details see:

Quick Notes: KIO Rights Offering