QRTEP - Qurate Retail Preferred Is A Bargain That Has Plenty Of Outs

2023-12-05 04:24:25 ET

Summary

- QRTEP (QRTEA 8.00% Cumulative Preferred Shares) are misunderstood securities within the Qurate structure.

- The collateral currently at Q more than covers the current market price.

- Q has plenty of outs to move more assets to the box, thus greatly increasing potential recovery value.

[[QRTEP]] (also referred to as the QRTEA 8.00% Cumulative Preferred Shares) are arguably one of the most misunderstood securities within the Qurate structure. What I want to accomplish today is to break down the various assets and claims that go into QRTEP to establish a valuation for these shares.

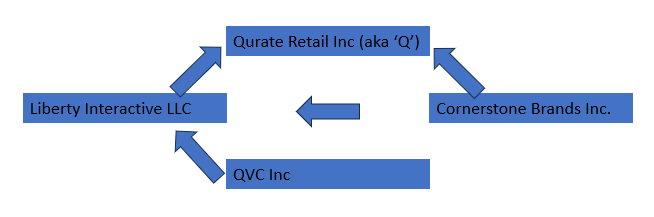

Let's first start by addressing the structure.

Qurate Corporate Structure (Created by Bruins on the Trade Floor)

{kind=link}

The top box is Qurate Retail Inc , this is where the QRTEP baby bonds sit. QRI (which is referred to as simply "Q" on all the earnings calls, so as to avoid confusion, we will also refer to it as "Q") is the parent entity. Beneath Q sit Liberty Interactive LLC ("LI") which is a holding company for QVC Inc ("QVCI") , the main producing asset in this entire structure.

Outside of this, there is also Cornerstone Brands Inc. ("CBI") , a separate, smaller producing asset that is 62% owned by Q and 38% owned by LI.

Now that we have that out of the way, let's look at what exactly underlies the QRTEP baby bonds. Firstly, we note that as of 3Q2023, there was 1271mm outstanding of debt at Q. For our analysis, we will normalize everything to $100, which is the face value of a single bond, and conduct our analysis relative to that.

- Cash - As of 3Q2023, there was $329mm cash at Q, which equates to roughly $26 per $100. We can subtract $2 from that because of the dividend that was just paid at the end of November to get to $24.

- 62% of CBI - Firstly, if we were to put a dollar value on CBI standalone, a 5x OIBDA multiple would put it around $250-300mm. Using this method, we could say this adds another $13 per $100 to the valuation. It would be prudent to point out here that CBI is a co-borrower on the revolver, it is not a cross-guarantor . In other words, CBI is not collateral against QVCI's drawing on the revolver. As of this moment, CBI does not have anything drawn on the revolver and historically, CBI has only used the revolver as seasonal financing (working capital for holiday season).

- Zulily - When Zulily was divested earlier this year, the consideration for the transaction was a right to future earnings of Zulily. Essentially, they sold Zulily for a call option. I personally don't think Zulily has many, if any, future prospects but certainly, if it took off, it wouldn't be the first time a company has turned around under new management. For the sake of being conservative, we won't assign any value to this, but know that it's there.

These are the easily identifiable assets, and thus far, we've come to a sum total of $24+$13=$37 per $100. This is what you would arguably get if Qurate filed tomorrow and things stayed exactly as is.

The next logical question is, can Qurate move additional funds upstream to Q? Now the common perception is that it can't, due to the restricted payments covenants under the indentures of the debt at QVCI. But to illustrate why this argument is wrong, imagine you have a ship with multiple holes in the hull. The restricted payments capacity is like plugging just one of those holes. If there are other holes the ship still takes on water.

So let me explain, the RP covenants only restrict the flow of cash between QVCI and LI to the extent that they can only move money from QVCI to LI for debt service and principal repayments at LI. However , there is absolutely nothing stopping them from moving existing cash at LI to Q. They pretty much verified this on Q2's earnings call. That means that anything currently at LI is fair game to be moved up to Q. So let's look at what sits at LI

- Cash - As of 3Q2023, there was $448mm cash at LI, remember any needs for debt service at LI can be met with cash from QVCI.

- 32% of CBI - Using the above methodology we can value this approximately $104mm

- "Other Investments" - There are some other assets held in this box that are carried around $50mm on the balance sheet

All in all, that's approximately $602mm or an additional $47 per $100 that they can move up from LI to Q between now and 2029.

So even assuming the bear case for Qurate, which would be a scenario where they do not improve enough to get over the 2029-2030 maturity wall, we can figure something to the tune of $84 per $100 recovery at Q.

The bull case is even better. As of 3Q2022, trailing OIBDA to net debt was sitting around 4.2x, which is the metric used for the RP under the QVCI indentures. Well, if we factor in cost reductions under Project Athens and see top line stabilize, they're not far from getting back under 3.5x which would allow them to move additional funds upstream to Q. Between now and 2029 is a long time and anything can happen. Moreover, outcomes are not so much binary. If the company can stabilize, creditors will have a decent incentive to work with Qurate and so there are many potential scenarios where holders give some kind of concession so they can restructure their capital stack.

On a relative value note, I like these much more than LI bonds for the reasons being that there is really nothing to stop them from moving cash and assets up and that Maffei and Malone personally own the QRTEP. It's in their own best interests to do so.

One final note is that I'm sure there is bound to be a debate around how long of a runway Qurate actually has. The past few authors on SA have all written with a lens that Qurate probably won't make it past the revolver in 2026. This is a separate topic in its entirety and merits a whole separate article but for the purposes of our analysis today, it is useful to point out that the market is indicating otherwise with QVCN medium-term bonds trending in the high 70s.

At the end of the day, at a price of $33.00, you're sitting even below just the value currently at Q in the worst case scenario. I think fair value right now would probably be in the $50-$60 range and depending on how things look going into 2024, could see this extent into the $70's. As of today, I would rate QRTEP a buy anywhere under $45, a hold to $55, and a sell at $55.

For further details see:

Qurate Retail Preferred Is A Bargain That Has Plenty Of Outs