QRTEP - Qurate Retail: Solvency Risks Subside Commercial Concerns Remain

2024-01-17 08:00:00 ET

Summary

- Qurate’s revenue growth remains negative while its margins stabilize, as the company continues to struggle with customer acquisition.

- Retailers are struggling to generate growth due to intense competition and economic conditions, although Qurate is underperforming due to a poor market offering.

- A three-year turnaround process is underway, which we believe is not close to being achieved. We expect several more years of struggles, with no certainty at the end.

- Qurate’s solvency risk has declined as it boasts ~$1.1b in cash, although we should reiterate that its ND/EBITDA ratio is 6.9x and its interest coverage is 2x, making its position weak.

- Qurate is trading at a 12% FCF yield, which is only 2% higher than its peer group average. Given the substantial difference in financial and commercial fortunes, we consider this unattractive.

Investment thesis

Our current investment thesis is:

- Qurate's debt concerns have softened as FCF has returned and cash has been raised. This means its commercial position is now at the forefront, and it is a more difficult issue to solve. The majority of its sales are comprised of a (declining) cohort of sticky customers, with Management seemingly unable to adapt its business model to the new market dynamics.

- We expect Qurate to struggle with growth in the coming 3 years, with limited scope for margin improvement as investment is required to protect growth and turn the company around.

- Its valuation may seem attractive but until we see a fundamental improvement in its commercial position, we cannot justify a buy rating.

Company description

Qurate Retail, Inc. ([[QRTEA]], [[QRTEB]]) is a company that operates in the video and online commerce space across North America, Europe, and Asia. They primarily sell consumer products through T.V. shopping programs, mobile, and online. Its brands offer a wide variety of products, such as apparel, home goods, and beauty products.

Qurate Retail's portfolio of brands includes QVC, HSN, Frontgate, Garnet Hill, and Grandin Road, among others.

Share price

We last covered Qurate in Mar23, rating the stock a sell. The company was struggling financially, its business model appeared obsolete despite a sticky customer base, and we were concerned that its solvency risk was rapidly increasing. Since then, the share price has declined ~36%, although we note this was ~65% at its lowest.

We will look to refresh our view of the company within this analysis, with a key eye on Qurate's financial progress and whether there is potential for upside. For a more detailed analysis of Qurate's business model, see our prior paper .

Commercial analysis

{kind=link}

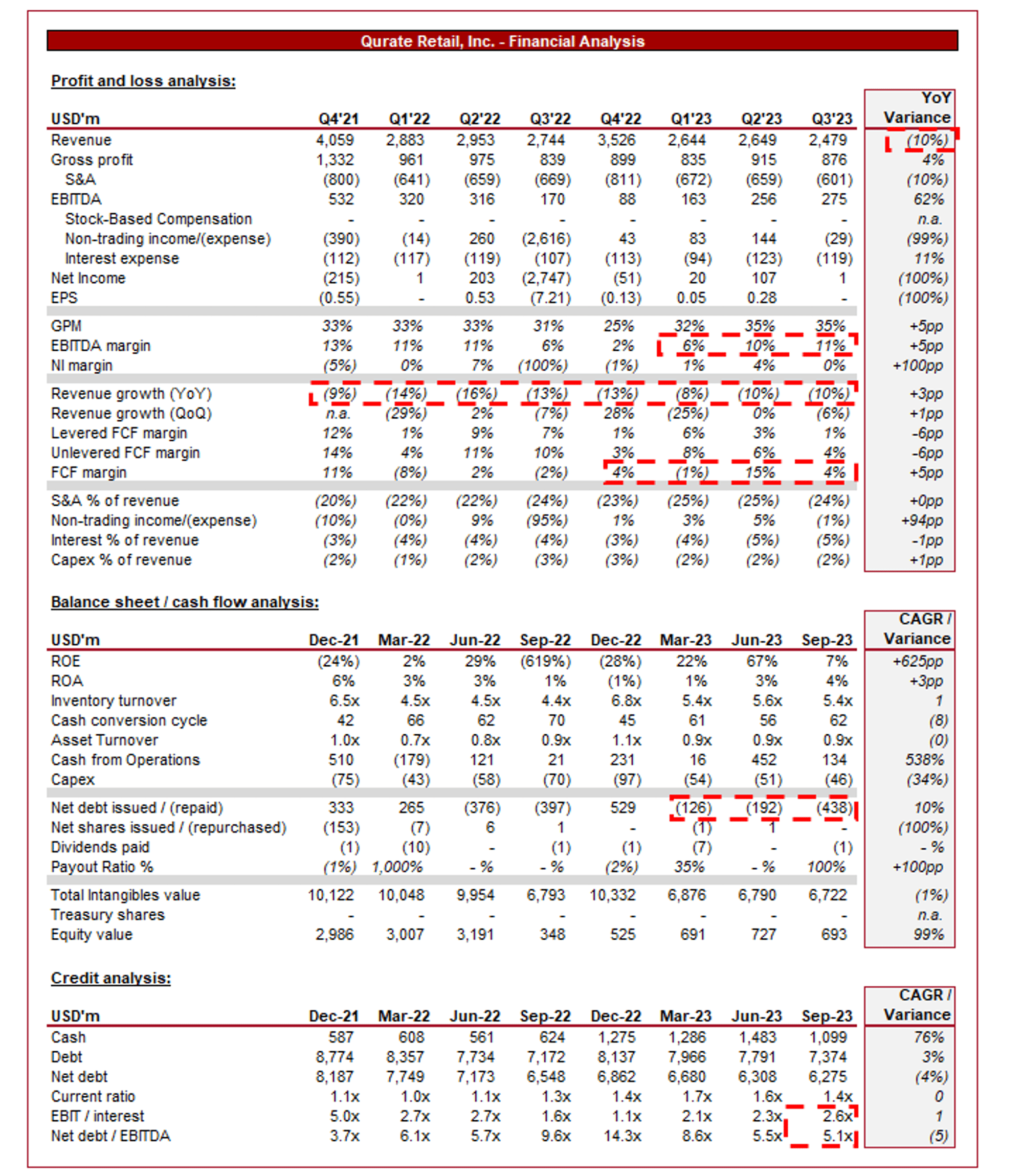

Presented above are Qurate's financial results.

Qurate's revenue has been on a consistent decline since FY18, contributing to a CAGR of +1% since FY13. The company is currently down (7)% during LTM23.

Financial progress

Qurate's revenue development continues to be disappointing, with its top-line declining by (13)%, (8)%, (10)%, and (10)% in its last four quarters. This said, the company's margins have improved in the last two quarters to its pre-Q3'22 levels. Note: The company disposed of Zulily in 2023, contributing to overstated declines. When adjusting for this, growth is (7)% in Q2 and (3)% in Q3.

The decline is primarily driven by a continuation of the downward trend in electronics demand, down (18)% YoY (Q3'22 was down (11)%). This is part of the broader electronics down-cycle in our view, as the industry benefited heavily from stimulus checks during the pandemic and has seen a downward trend since

Further, Apparel and Beauty are down (8)% and (7)%, respectively. We attribute this to execution, with increased competition and discounting by competitors restricting Qurate's ability to achieve price-driven growth, with quantity insufficient given its declining relevance.

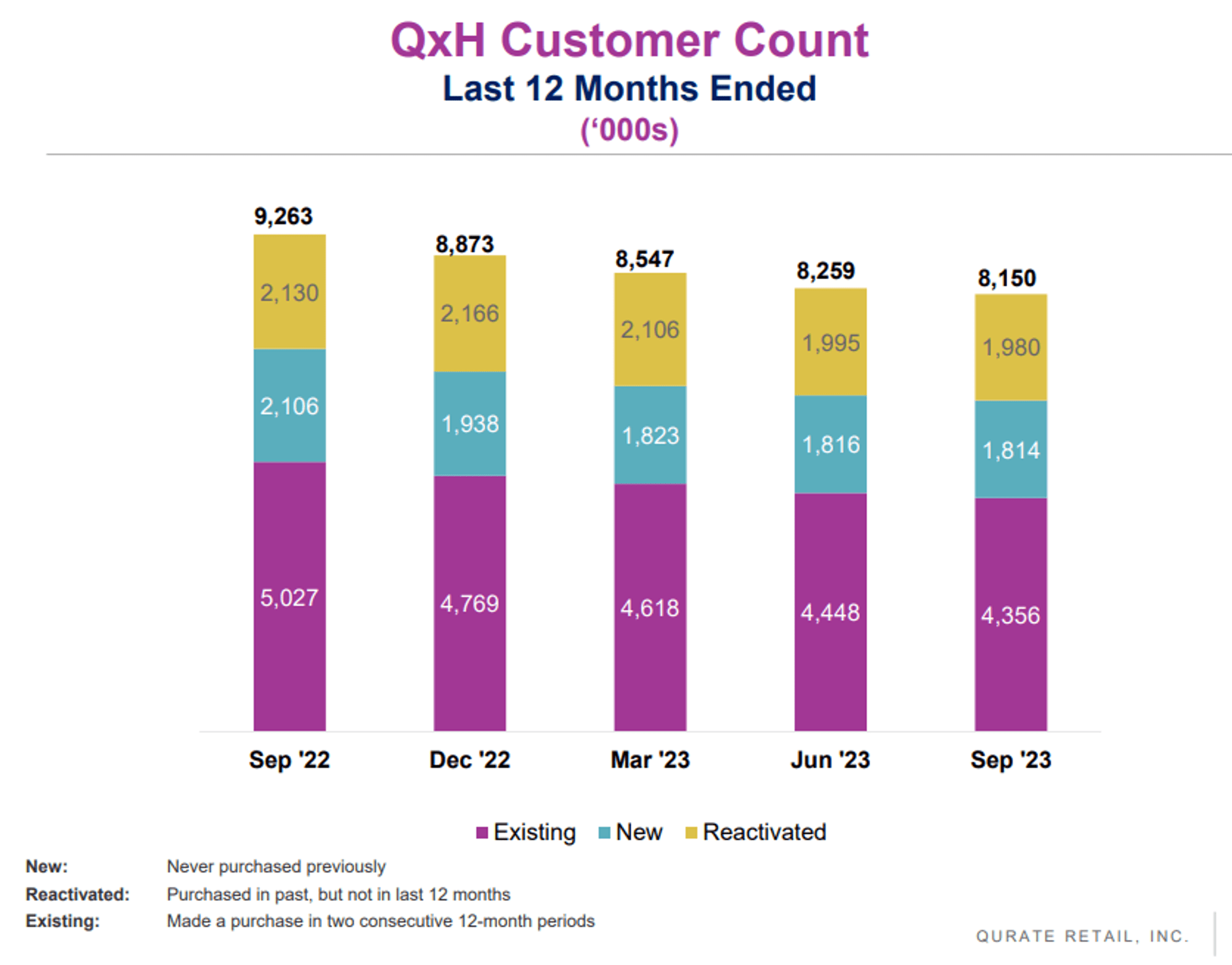

Additionally, the company's customer count declined again in Sep23, although to a lesser extent than prior quarters. Stabilization in its core customer base is critical to changing fortunes given its biggest issue is obsolescence. Until this occurs, it's difficult not to expect its trajectory to continue.

{kind=link}

From a sales perspective, this has been another poor quarter for the company. Realistically, a turnaround effort will likely take several years, particularly given its existing customer base and go-to-market approach. This said, we would have expected a "bottom" to be reached.

As the following illustrates, US retail sales have broadly flatlined in recent quarters, although importantly remain ticking upward. This trajectory does not align with Qurate, supporting the argument that it's a fundamental issue.

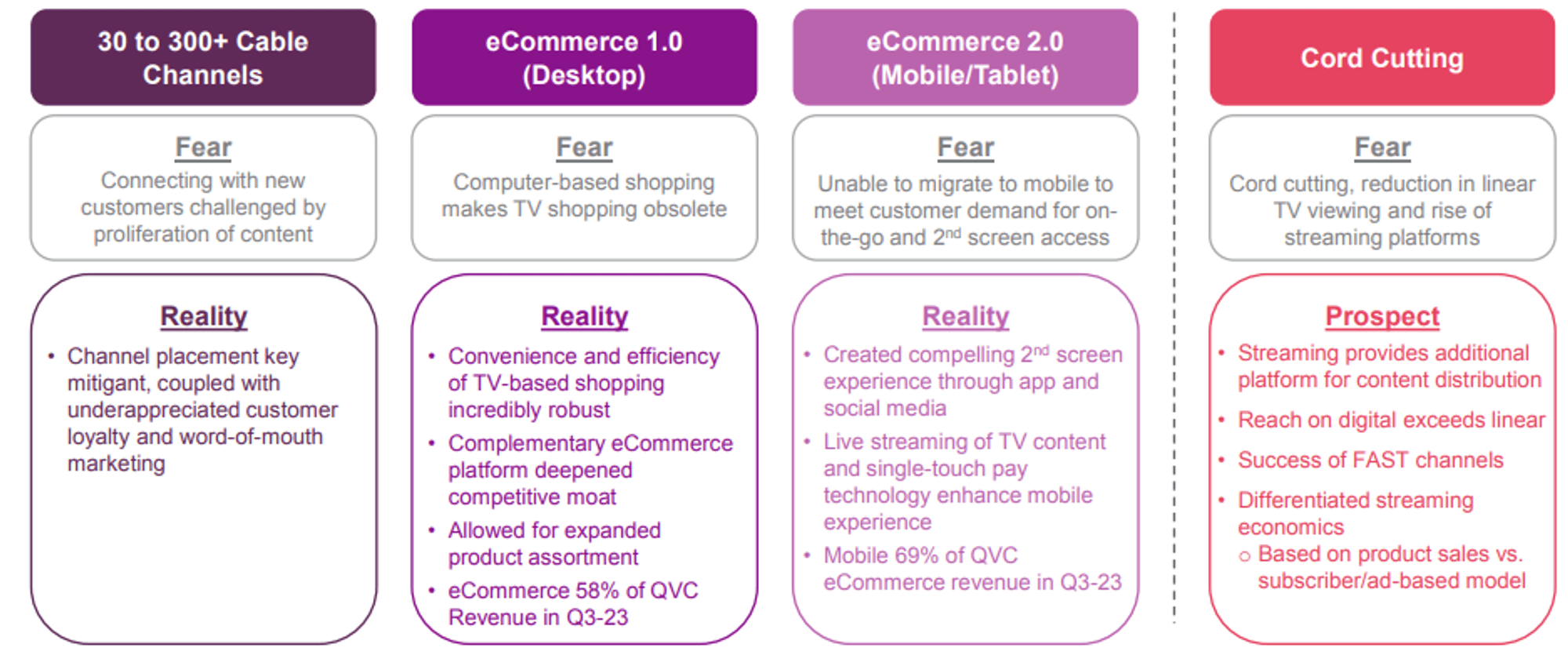

Business model

In Jun22, Qurate announced a three-year turnaround plan, designed to stabilize and differentiate its core businesses, and expand its leadership in video streaming commerce. This would contribute to a double-digit CAGR in FCF and stable revenue growth through 2024.

This involves 5 pillars which are listed below. Against each, we comment on how we believe Qurate has progressed.

This involves 5 pillars :

- Improve Customer Experience and Grow Relationships - Although we have observed development in how Qurate reaches its customers, its customer count across all segments has persistently declined.

- Rigorously Execute Core Processes - Similarly to the prior point, we believe the opposite has been observed. Pricing competition continues to be underwhelming, the choice is uncompetitive (quality of brands and their products vs. quantity), and reaching consumers through online channels is far behind its peers.

- Lower Cost to Serve - Once again, this has not been delivered, at least relative to its revenue. GM% has declined from 34% in FY21 to 31% in LTM23 (although LTM23 is 1ppt ahead of FY22) and S&A as a % of revenue has increased from 20% in FY21 to 24% in LTM23.

- Optimize Brand Portfolio - Management specifically called out Zulily and Cornerstone, one of which has been divested and subsequently closed, and the other continues to see revenue declining in the double-digits.

- Build New High-Growth Businesses Anchored in Strength - To give Management credit, expanding into the new digital age was always going to be difficult, and they have not completely failed, which is credit in itself. This said, no single reporting segment can be described as "High-growth".

{kind=link}

Overall, the company has made limited progress toward its strategic objectives. At best, the company will have stabilized its revenue by 2024, but this will not be underpinned by quality commercial development.

For this reason, we remain bearish about the company's business model. Retail is incredibly difficult at the best of times but at such a disadvantage, we struggle to see even growth stabilizing, let alone the other pillars.

Economic & external consideration

Current economic conditions have not been friendly to Qurate. With elevated inflation and interest rates, consumers are experiencing a cost-of-living crisis. This has disproportionately impacted the working class and elderly, both of which are core targets for Qurate.

Wage inflation and sticky employment have kept the West out of a recession, although this may not remain the case. The US recession probability indicator has exceeded 50% for the first time, and unemployment has begun to tick up.

We suspect the first half of 2024 (at the very least) will be difficult, with retail spending potentially turning negative but likely being <3%. This will limit Qurate's scope for a return to growth, particularly as its peers focus on pricing competition which will restrict the scope for new customer acquisition.

Margins

{kind=link}

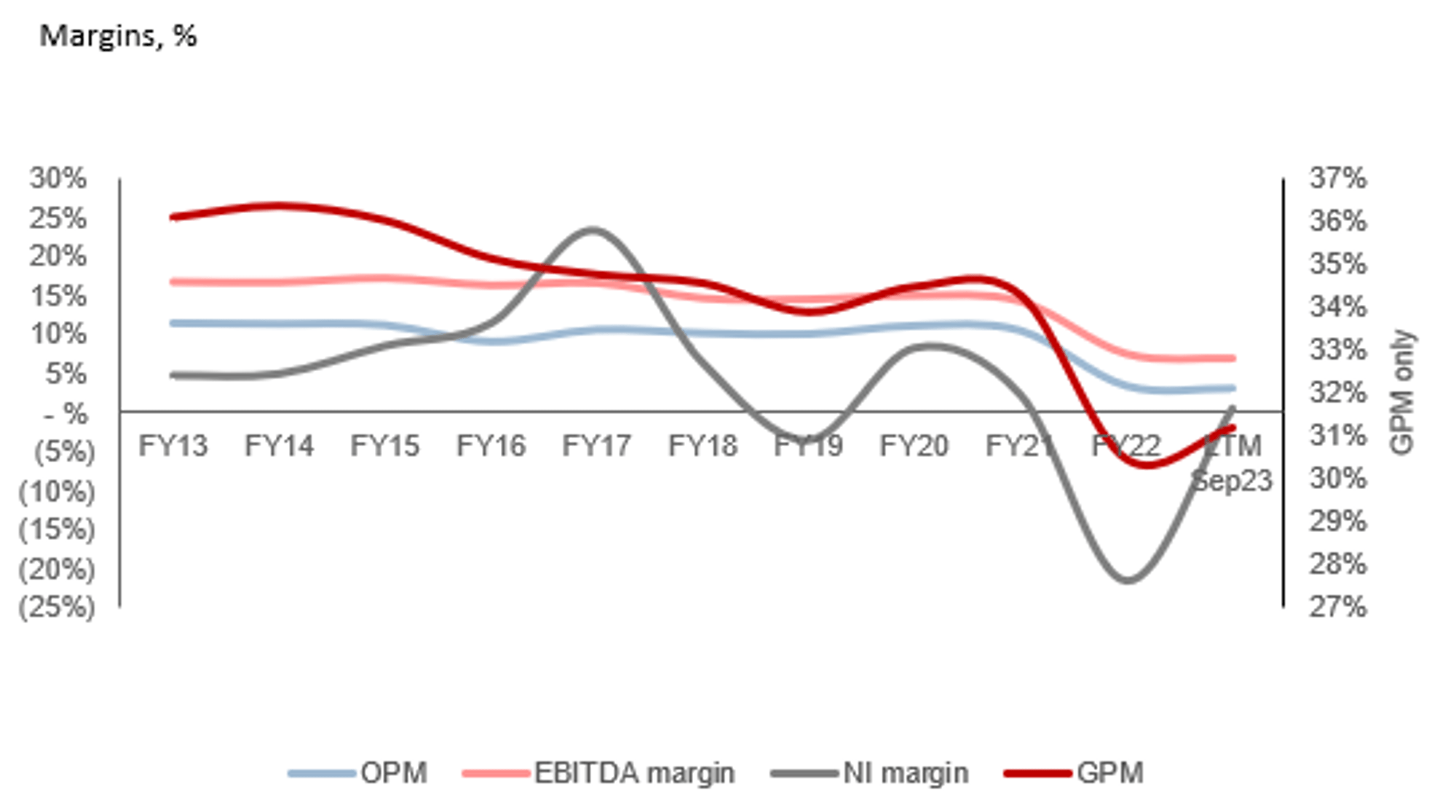

As previously touched on, Qurate's margins have consistently trended down during the last decade. This has been driven by a combination of its declining price advantage and increased investment in customer acquisitions, which has clearly been unsuccessful.

To illustrate this with numbers, between FY18 and LTM23, revenue declined 20%, CoS declined 15.6%, and S&A costs declined 2%. Management's ability to flexibly adjust its cost base has been limited, contributing to further pressure.

Balance sheet & cash flows

One area of positivity is Qurate's development regarding debt. The company has managed to raise cash, in part through sale-and-leaseback transactions. This has contributed to a cash balance of ~$1.1b, which Management considers sufficient to get it through 2024 and 2025.

Qurate has returned to FCF positivity, which is critical to its long-term success. It means Management can continue to invest in revitalizing growth without having to worry about solvency, even if they have been unsuccessful thus far.

This said, it is worth contextualizing that Qurate's ND/LTM23 EBITDA is 6.9x, which is incredibly high. The company's interest coverage is 2x on an LTM basis, which makes it both concerning in the long-term when it comes to deleveraging and precarious in the short-term, particularly if a recession does occur.

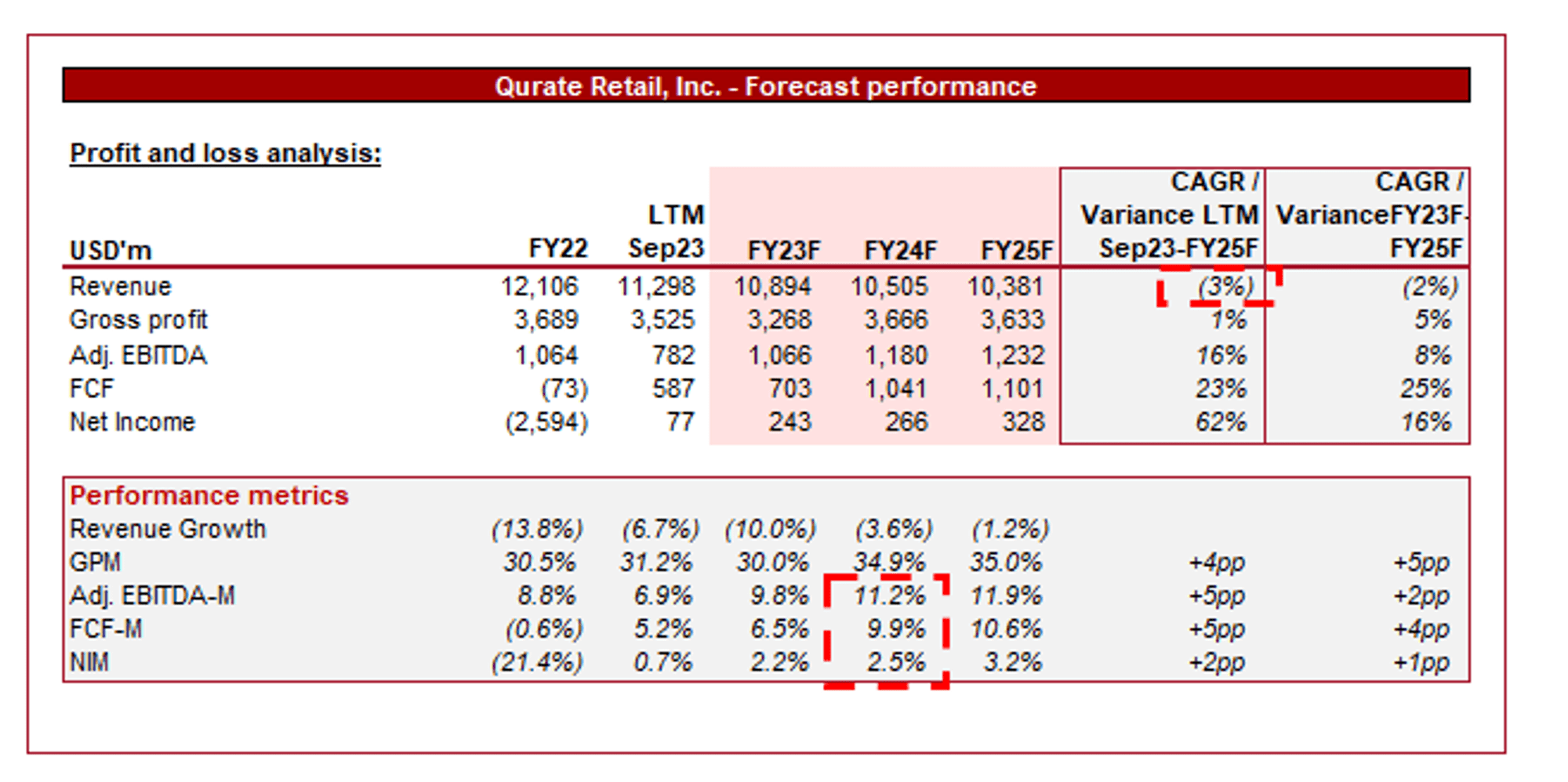

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its revenue decline, with a CAGR of (3)% into FY25F. Alongside this, margins are expected to incrementally improve.

We concur with the trajectory forecast but expect growth to be better and margins to be slightly lower. Our view is that a bottom is imminent from a fundamental perspective while margin growth will be restricted by reinvestment.

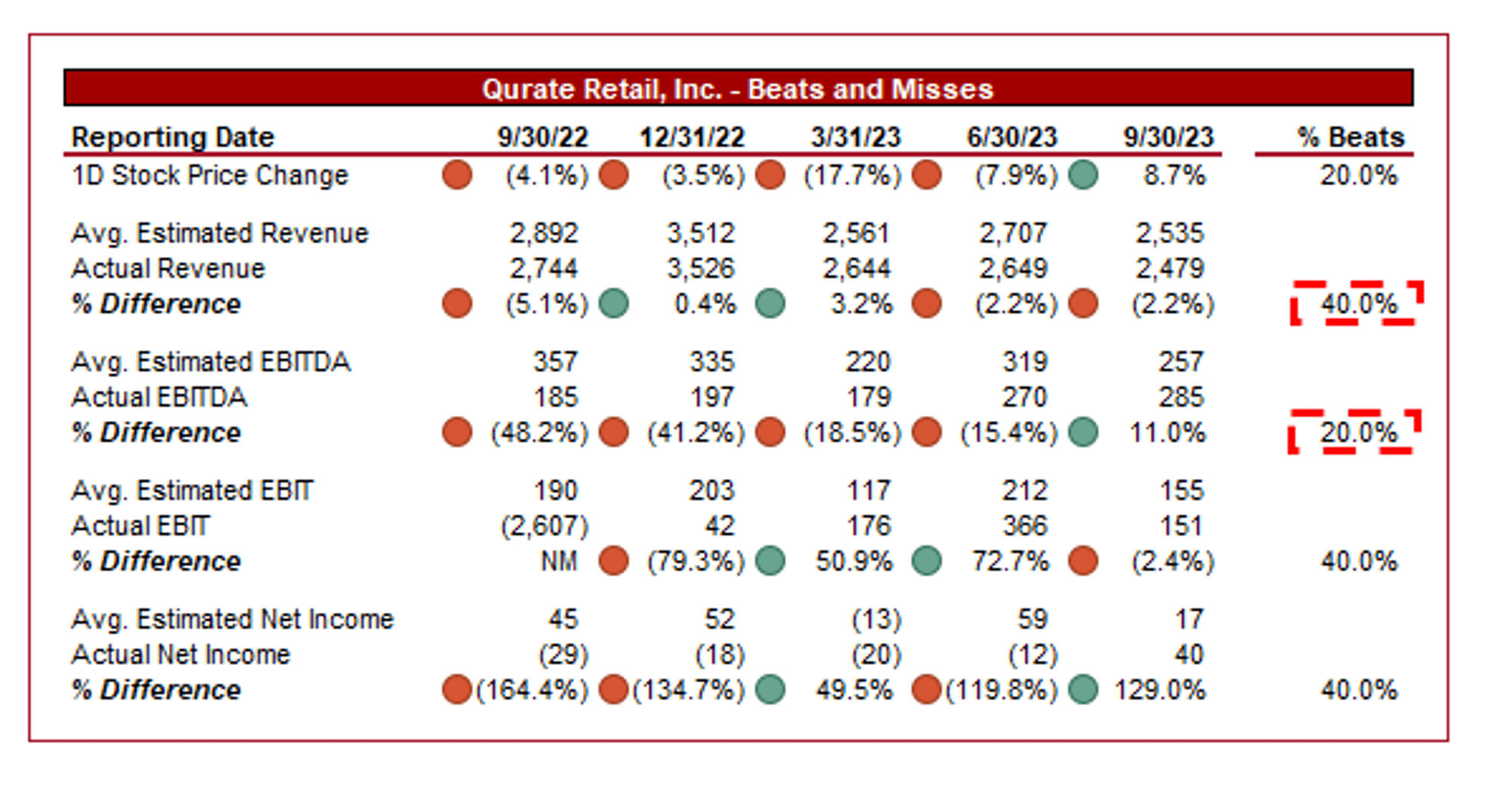

Beats and Misses

{kind=link}

Qurate has been underperforming estimates thus far, particularly from a profitability perspective. This reiterates our margin hesitancy, although its revenue growth has been broadly in line.

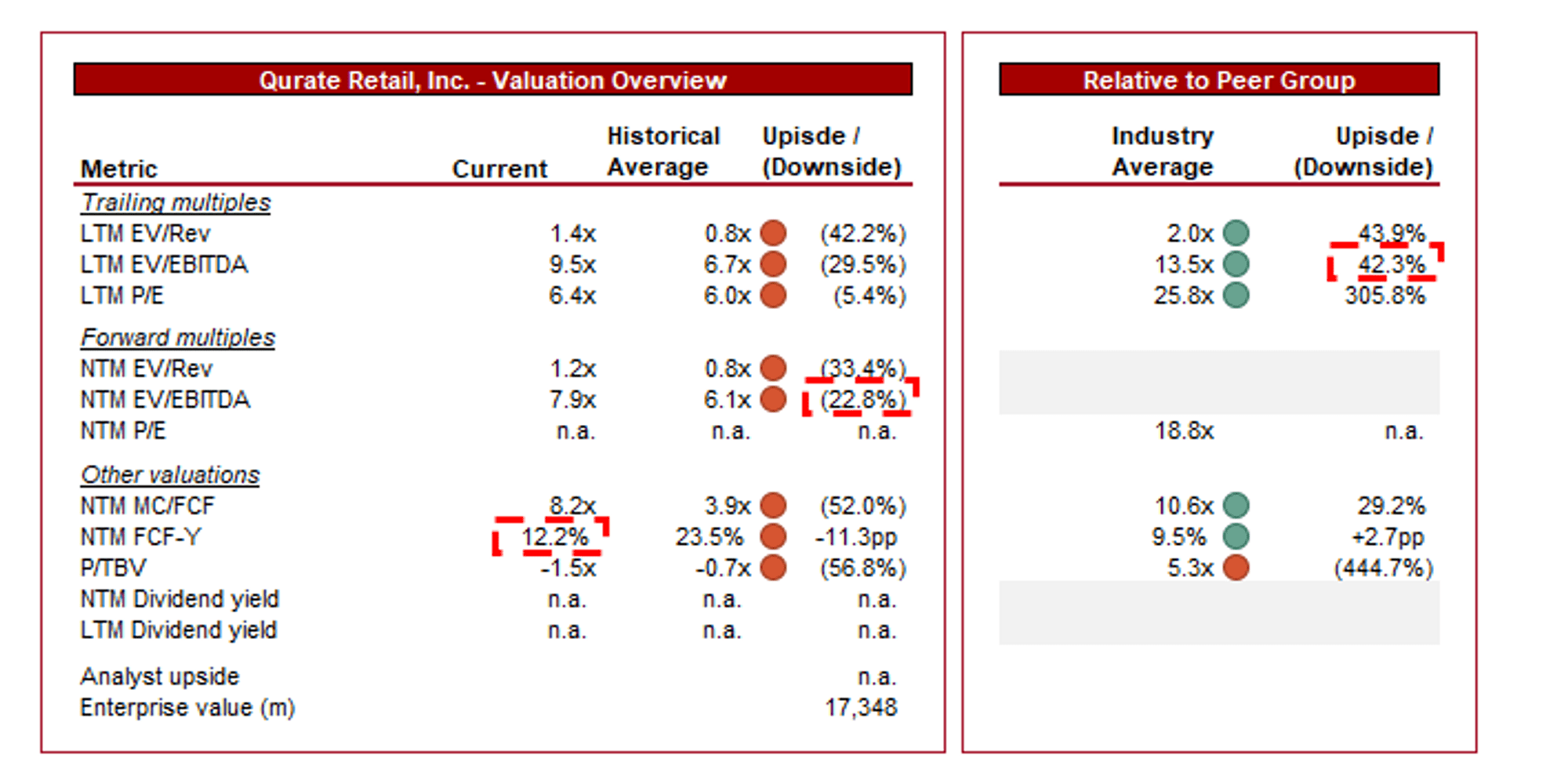

Valuation

{kind=link}

Qurate is currently trading at 10x LTM EBITDA and 8x NTM EBITDA. This is a premium to its historical average.

This valuation represents a deep discount to its peer group average, which we believe reflects its commercial and financial concerns. Qurate is trading at an implied NTM FCF yield of 12%, which is fairly attractive from an absolute basis but not when compared to its peers, which stands at ~10%. This 2% delta is not sufficient. Its peers have an average EBITDA-M of 13% and a 5Y growth rate of 18%, all while not being heavily indebted and experiencing a decline in relevance.

Key risks with our thesis

The risks to our current thesis are:

- Earlier than expected reduction in rates, contributing to an improvement in demand.

- Successful sales-channel innovation that supports consistent new-customer growth.

Final thoughts

We have not made this clear but it is worth giving Management credit where it is due, Qurate has improved since we last covered this company. A bankruptcy situation appears off the table (although not completely). This said, the company's fundamental issues are now front and center, and it is ugly.

Its customer base is progressively declining, these customers are increasingly irrelevant in terms of share of spending, its financial profile is underwhelming, and a resurgence is far from guaranteed.

At a FCF yield of ~12% and a period of reasonable stability ahead (a decline is likely but no more negative FCF), we suggest investors await commercial development before making a decision on this stock.

For further details see:

Qurate Retail: Solvency Risks Subside, Commercial Concerns Remain