FRI - Rate Cut Rethink

2024-01-21 09:00:00 ET

Summary

- U.S. equity markets posted another week of gains as investors weighed conflicting indications on economic momentum and the need for rate cuts, with strong economic data offsetting soft corporate earnings.

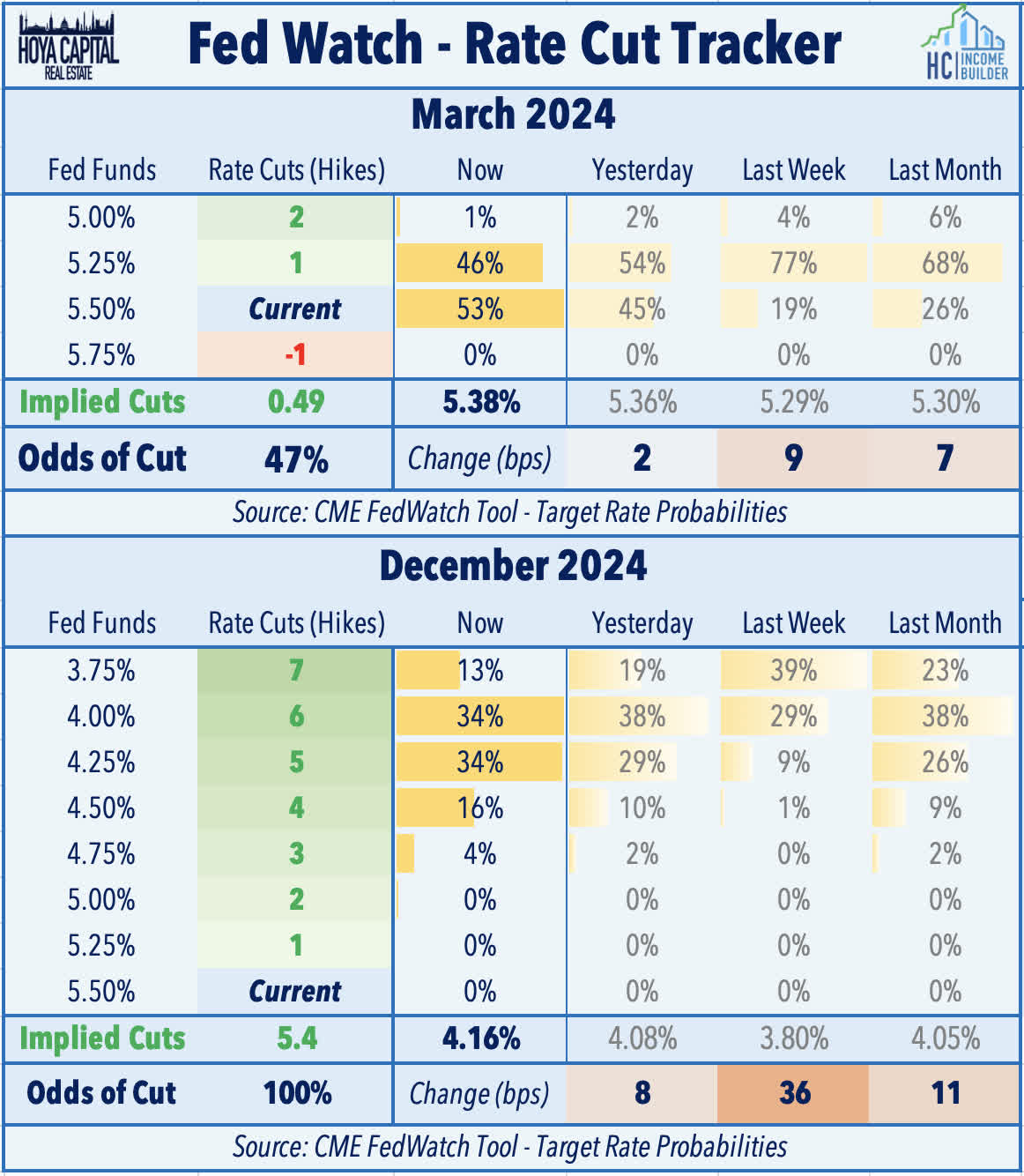

- Swaps markets are now pricing in roughly 45% probability that the Federal Reserve will begin its rate-cutting cycle in March, down from odds of over 80% in the prior week.

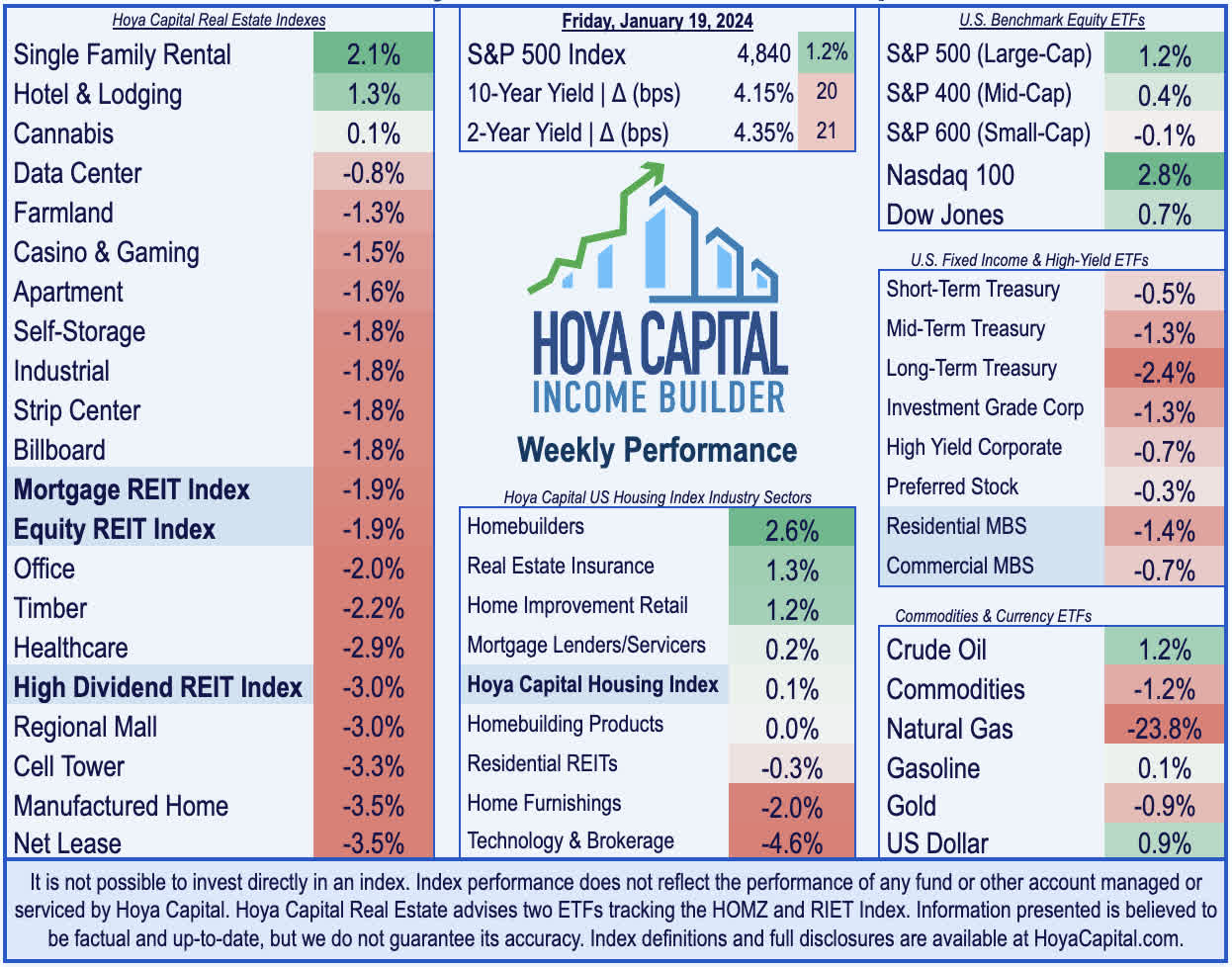

- Notching gains in 11 of the past 12 weeks, the S&P 500 advanced 1.2% on the week to close at record-highs for the first time in two years.

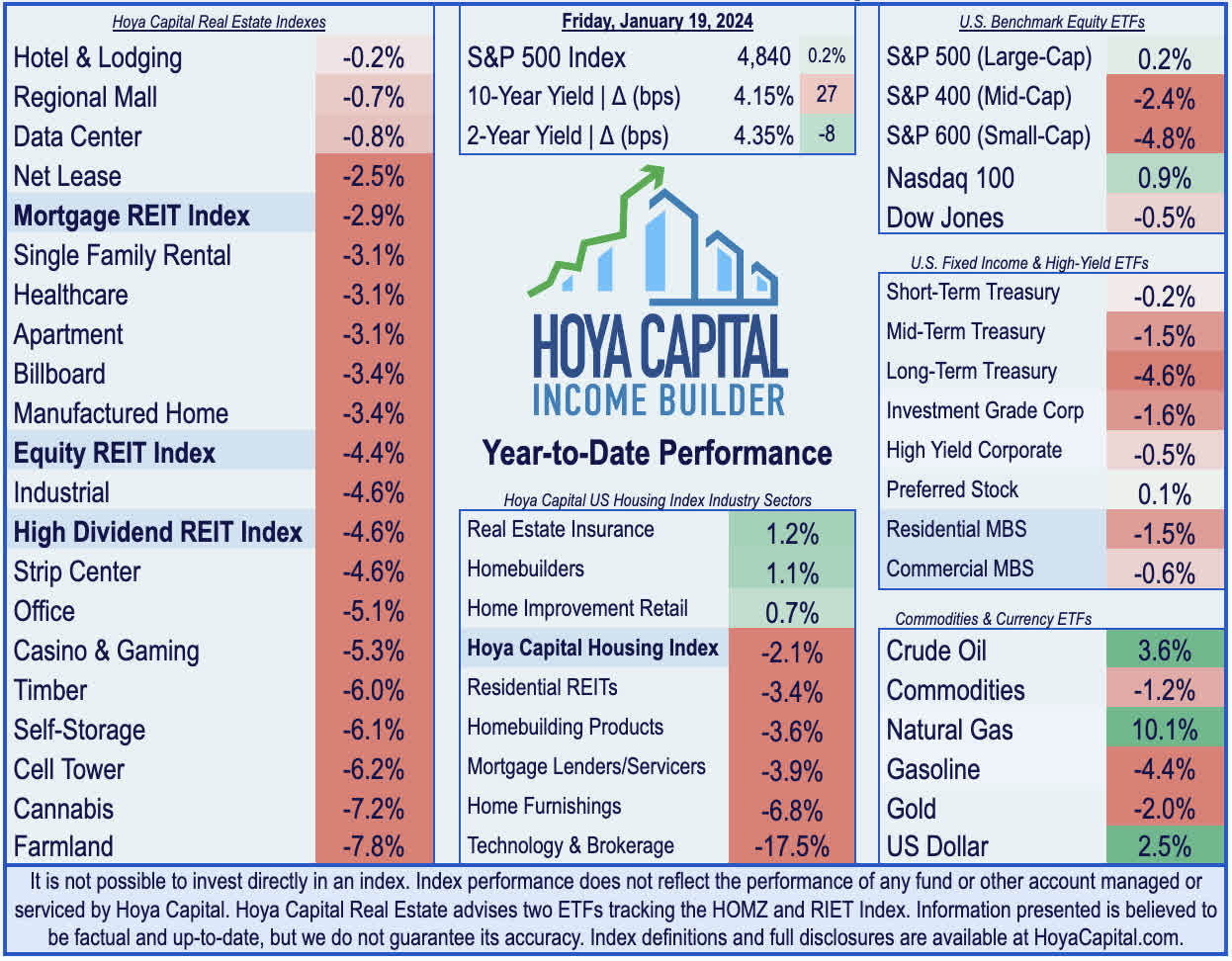

- Real estate equities were laggards this week as the rebound in benchmark interest rates counteracted a relatively solid start to earnings season and a lift from several notable M&A developments. The Equity REIT Index slipped 1.9% this week.

- Tricon Residential - the third-largest SFR REIT owning roughly 38,000 homes - surged after Blackstone announced a $3.5B deal to take the company private. MDC Holdings - the ninth-largest public homebuilder - also rallied after it agreed to be acquired by Japanese firm Sekisui House in an all-cash deal.

Real Estate Weekly Outlook

U.S. equity markets posted another week of gains as investors weighed conflicting indications on economic momentum and the need for rate cuts, with resilient employment, retail sales, and housing market data countering a relatively downbeat start to corporate earnings season, which included a wave of corporate layoff announcements across a wide swath of industry groups.

{kind=link}

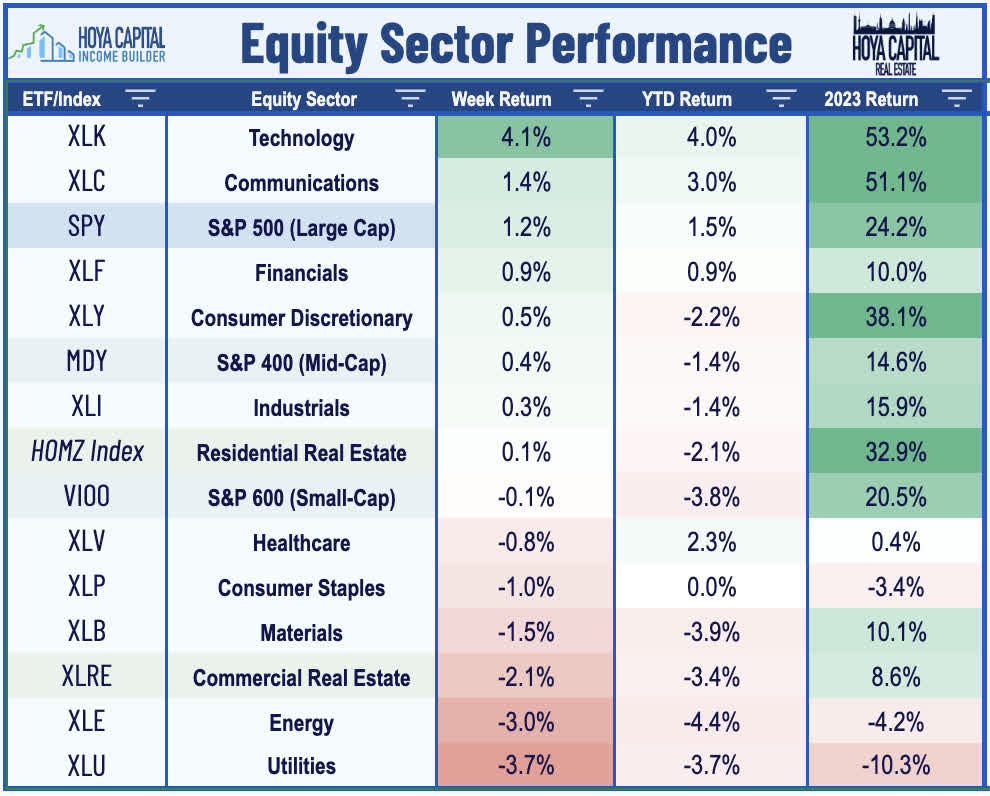

Notching gains in 11 of the past 12 weeks, the S&P 500 advanced 1.2% on the week to close at record-highs for the first time in two years. Heavyweight technology stocks led the rally this week, with the Nasdaq 100 advancing nearly 3% on reports showing strong demand for high-end computing chips. Gains were once again top-heavy this week, however, as the Mid-Cap 400 posted muted gains of 0.4%, while the Small-Cap 600 finished lower by 0.1%. Real estate equities were laggards this week as the rebound in benchmark interest rates counteracted a relatively solid start to earnings season and a lift from several notable M&A developments. The Equity REIT Index slipped 1.9% this week, with 15-of-18 property sectors in negative territory, while the Mortgage REIT Index declined 1.9%. Homebuilders were upside standouts on upbeat housing market data and a takeover bid for MDC Holdings - the ninth-largest builder.

{kind=link}

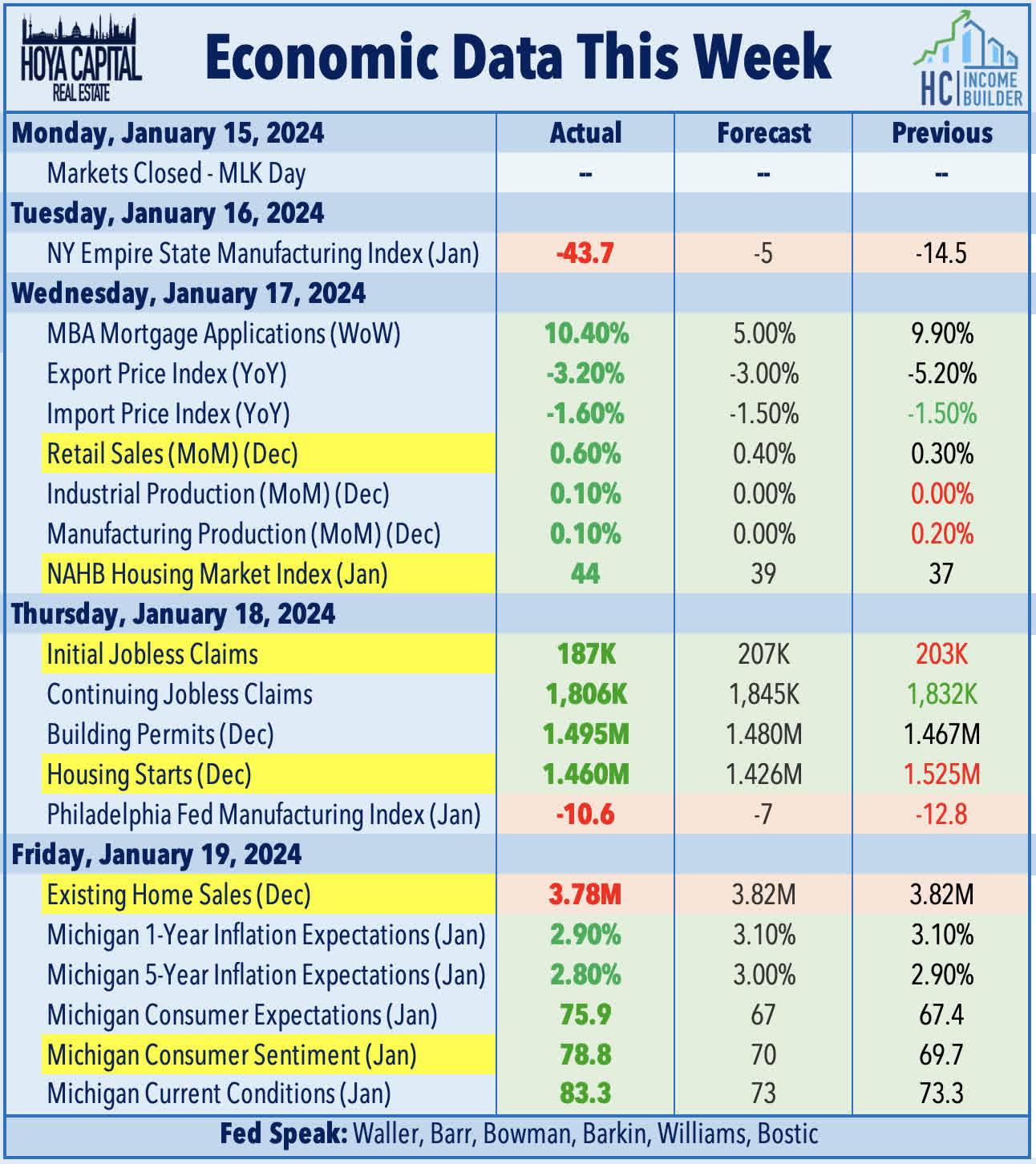

Surprisingly solid economic data and relatively hawkish central bank commentary throughout the week weighed on bond markets as traders reprice the magnitude and timing of Fed rate cuts. Notably, U.S. employment market continued to show surprising resiliency in the early days of 2024, with initial jobless claims dipping to the lowest levels since September 2022. Combined with data showing a reacceleration in retail sales and a rebound in housing market activity, there are renewed concerns that a reacceleration in economic momentum may stall the recent deflationary trends and delay the Fed's rate cut path. Swaps markets are now pricing in a 47% probability that the Fed will cut interest rates for the first time this cycle in March, down from 80% last week. The 10-Year Treasury Yield jumped 20 basis points this week to 4.15% - its highest since mid-December and up from early January lows of 3.79%. The policy-sensitive 2-Year Treasury Yield also jumped 21 basis points to 4.35%, up from recent lows of 4.15%.

{kind=link}

While economic data surprised to the upside this week, corporate newsflow was less-than-impressive, underscored by a wave of job cut announcements across a range of industries, including tech firms Google and Amazon , retailers Macy's and Wayfair , financials Citigroup and BlackRock , and automaker Ford . Meanwhile, Spirit Airlines dipped over 60% amid bankruptcy concerns following the failed merger with JetBlue . While still very early in earnings season, FactSet notes that earning season is "off to a weak start," with 62% of companies beating EPS estimates, which is below the 5-year average of 77%. Commodities were mixed this week as traders evaluated the impacts of ongoing tensions in the Middle East. WTI Crude Oil advanced 1% on the week, while Natural Gas dipped over 20% amid an escalation of disruptions in the Red Sea, which have halted some LNG shipments. Six of the eleven GICS equity sectors finished lower on the week, with Utilities ( XLU ) and Energy ( XLE ) lagging on the downside.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

A key look into the health and sentiment of the U.S. consumer, data this week showed that Retail Sales rose at the strongest pace in three months in December, rounding out a surprisingly strong holiday season for retailers. Total retail sales increased 0.6% in December compared to the prior month and 5.6% from last year - above the 0.4% forecasted month-over-month increase. Excluding gasoline stations, Core Retail sales were even stronger, posting a year-over-year increase of 5.8%, which was the strongest increase since February. Spending strength was relatively broad-based, with 9 of 13 categories posting sequential monthly increases, led by clothing, general merchandise stores, and home improvement retailers. The e-commerce category (non-store retailers) was also an outperformer. Car sales were up 1.1%, matching the biggest increase since May, while spending at gasoline stations fell for a fourth month.

{kind=link}

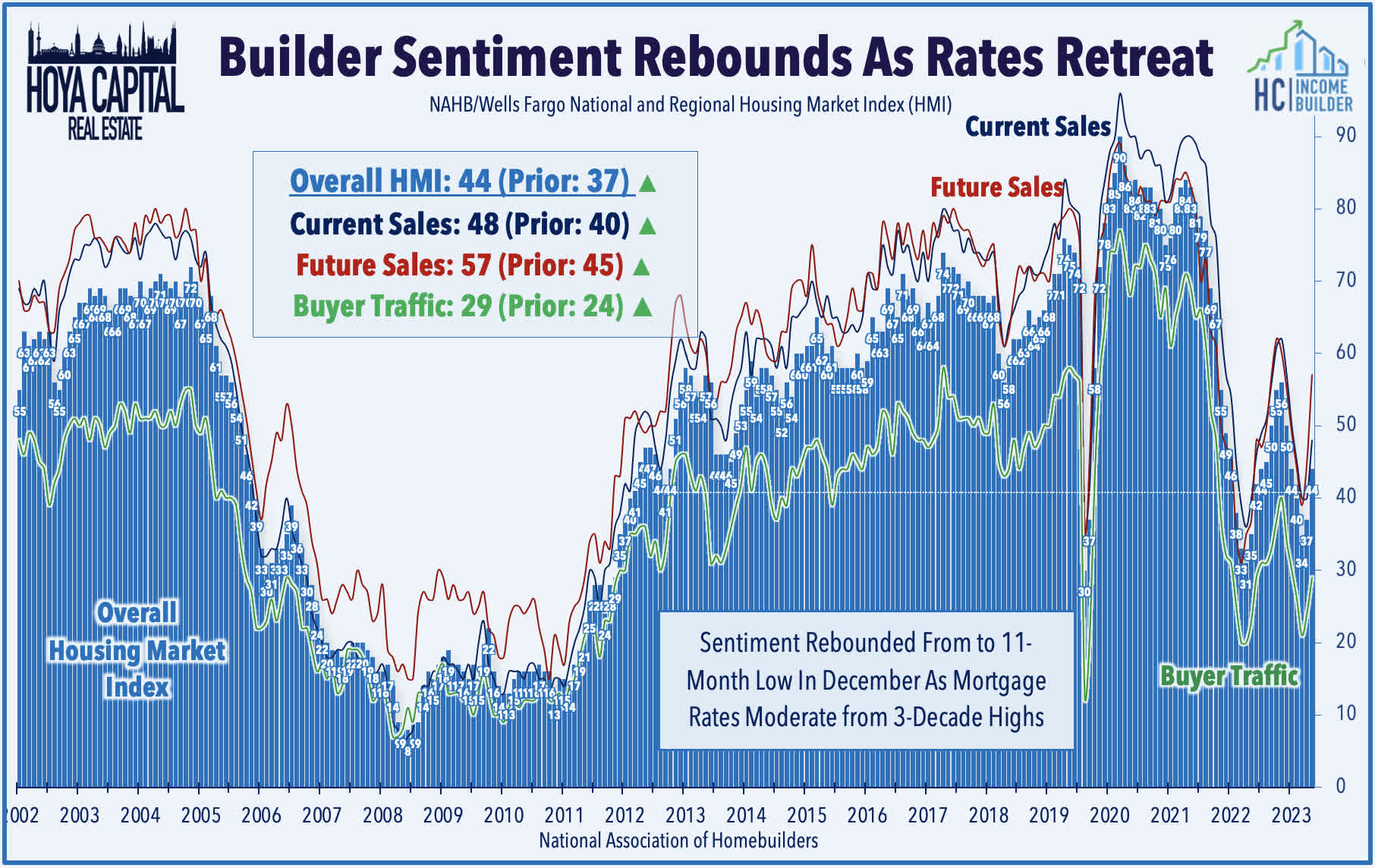

Housing market data, meanwhile, was generally stronger than expected, as the retreat in mortgage rates appears to be reviving some activity following two years of relative stagnation. The NAHB Homebuilder Sentiment Index jumped 7 points in January to 44 - well above estimates of 39 and up sharply from the recent lows of 34 in November. All three sub-components posted increases of at least 5 points, led by a 12 point surge in the index for Future Sales. Sentiment improved in three of four regions, led by advances in the South and West. Since peaking at three-decade highs in November at around 8%, the 30-Year Fixed Mortgage Rate has pulled back by roughly 1.25 percentage points to the mid-to-high 6% range. Existing Home Sales came in a bit lighter than expected in December - falling to their lowest annualized rate since 1995 - but forward-looking metrics indicate that this will likely be the "low point" in sales activity. Data from the Mortgage Bankers Association this week showed that Mortgage Applications for home purchases rose to a six-month high, while Housing Starts and Building Permits each posted their strongest year-over-year increase since early 2022.

{kind=link}

Concluding the surprisingly solid slate of economic data, data from the University of Michigan showed a surge in consumer confidence to the highest levels since July 2021, driven by a sharp retreat in inflation expectations. UM's Consumer Sentiment Index jumped 9 points to 78.8 in early January - the largest monthly advance since 2005 - while its reading for 1-Year and 5-Year Inflation Expectations cooled to the lowest levels since late 2020. Inflation expectations and consumer sentiment have closely tracked movement in gasoline prices in recent years. Per the EIA, consumer gasoline prices averaged $3.06/gallon last week, which was 39% below the June 2020 high, but still about 20% above levels seen at the end of 2019.

{kind=link}

Equity REIT & Homebuilder Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Single-Family Rental : M&A was a major theme this week across the U.S. real estate sector. Tricon Residential ( TCN ) - the third-largest SFR REIT owning roughly 38,000 homes - surged 21% this week after Blackstone ( BX ) announced a $3.5B deal to take the company private. A somewhat surprising move given the redemption pressure on its flagship non-traded Blackstone Real Estate Income Trust ("BREIT") since late 2022, the purchase will be funded primarily from its newly launched $30B drawdown fund - Blackstone Real Estate partners - with a minority share (11%) allocated to BREIT. Tricon becomes the sixth public REIT to be taken private by Blackstone and its affiliates since the start of 2021 - four of which have been residential REITs: American Campus, Bluerock Growth, and Preferred Apartments. The shares will be acquired for $11.25/share in cash - representing a premium of 30% to Tricon's closing share price on January 18th - with the deal expected to close in the second quarter of this year. TCN will not declare its regular quarterly dividend during the pendency of the transaction.

{kind=link}

Blackstone has been at the forefront of the "institutionalization" of the single-family rental sector over the past decade, acquiring a portfolio of tens of thousands of single-family homes in the immediate aftermath of the Great Financial Crisis - many purchased in states of distress - which it took public through the IPO of Invitation Homes ( INVH ) in 2017. Blackstone re-entered the SFR business with a preferred investment in Tricon in 2020 and the purchase of Home Partners of America in 2021, which owns nearly 30,000 homes. Combined, Blackstone will become the third largest owner of single-family homes in the United States with roughly 70k homes, trailing only Pretium's Progress Residential and the aforementioned Invitation Homes . After the acquisition, Tricon plans to complete its $1 billion development pipeline of new SFRs in the U.S. and $2.5 billion of new apartments in Canada.

{kind=link}

Homebuilders : M.D.C. Holdings ( MDC ) - the ninth-largest publicly-traded homebuilder by market capitalization - surged 16% this week after it agreed to be acquired by Japanese firm Sekisui House in an all-cash transaction valued at $4.9 billion. Headquartered in Denver and founded in 1972, MDC builds and sells roughly 10,000 homes per year with a focus on higher-end development in West Coast markets, and is the only homebuilder to pay a dividend yield above the S&P 500 average. Sekisui initially entered the U.S. homebuilding market in 2017 through its acquisition of Woodside Homes, and has operations in Australia, the U.K., China, and Singapore. With M.D.C. in its portfolio, Sekisui House would become the fifth-largest homebuilder in the U.S. based on number of completed sales in 2022. MDC shareholders will receive $63 per share in cash, representing a 19% premium to the stock’s closing price on January 17, 2024, the last day before the transaction was announced. The transaction is expected to close in the first half of this year.

{kind=link}

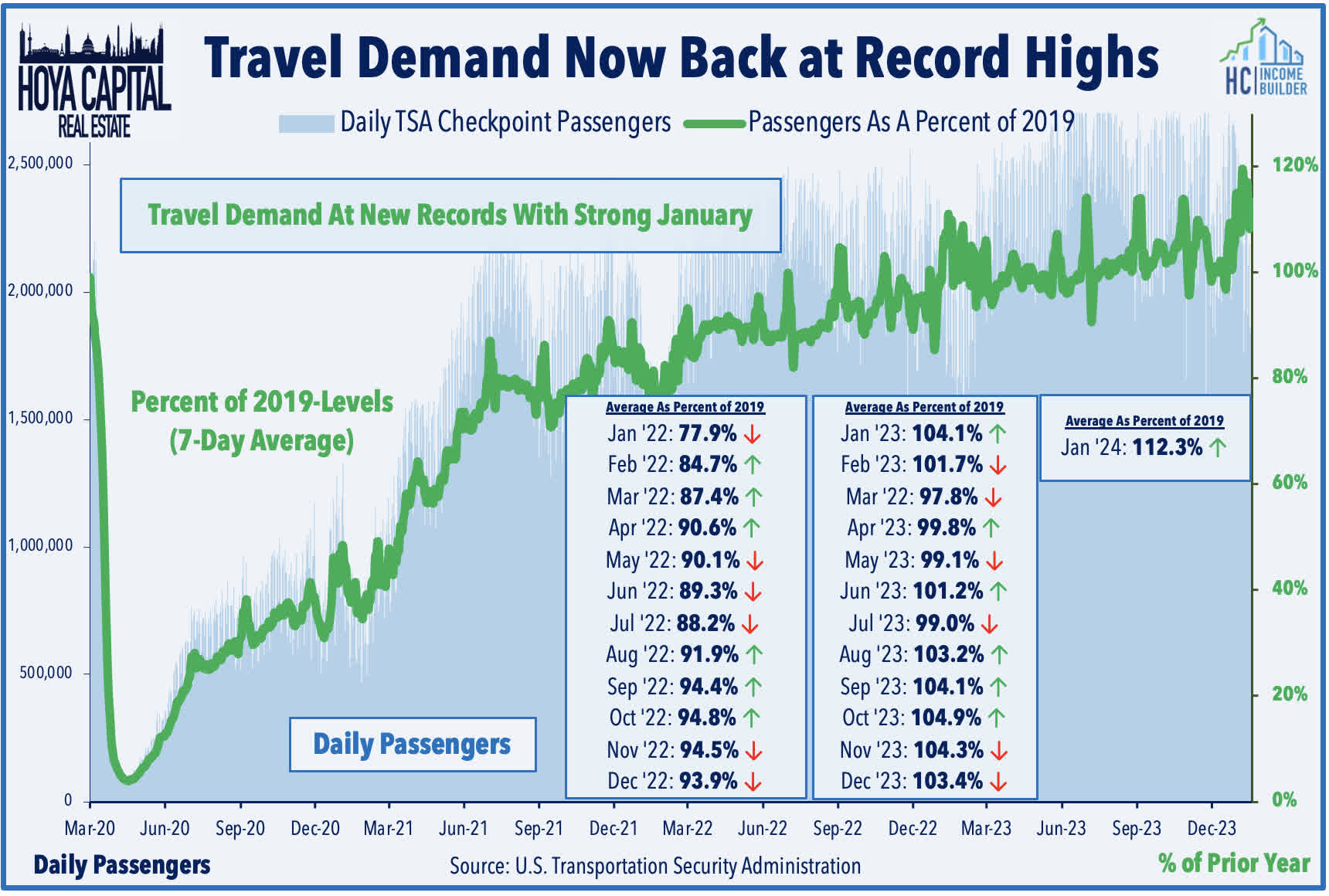

Hotel : Pebblebrook ( PEB ) - which owns 46 hotels with a heavy presence in Coastal urban markets which were hit hardest by the pandemic - rallied nearly 4% this week after it provided preliminary fourth-quarter operating metrics showing an acceleration in demand throughout the third quarter. PEB's Revenue Per Available Room ("RevPAR") rose 5% year-over-year in the fourth quarter to levels that are roughly even with pre-pandemic levels, with each month in Q4 seeing a sequential improvement. PEB commented, "Demand growth was strong all around – on weekdays at resorts through increased business group bookings and on weekends through leisure, and in urban markets from strong growth in weekday business demand, both group and transient, as well as healthy weekend leisure demand." Ryman Hospitality ( RHP ) was also among the leaders this week after providing preliminary fourth-quarter operating metrics showing performance that exceeded its prior guidance. RHP noted that its full-year RevPAR climbed to $458 in 2023 - a 13.2% increase from last year, which was above its prior outlook calling for a 12% increase. Commenting that the results "exceeded its expectations" and citing "continued strength in leisure room rates," RHP now anticipates full-year AFFO growth of nearly 24% at the midpoint of its updated range - up from the roughly 14% growth expected in its prior update. Recent TSA Checkpoint data shows that - despite several recent high-profile airline incidents - travel demand has eclipsed all-time record-highs so far in early January.

{kind=link}

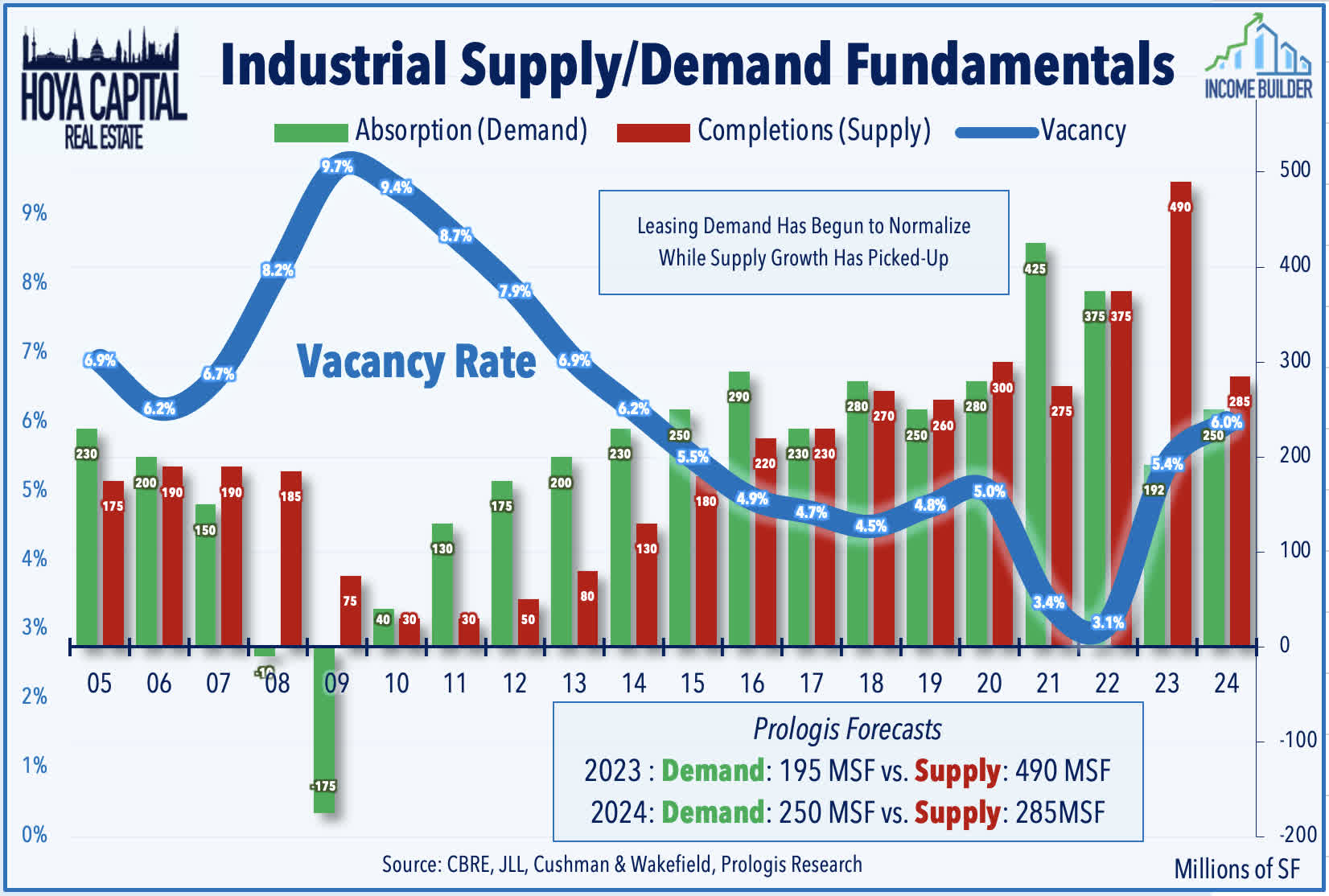

Industrial : Logistics stalwart Prologis ( PLD ) slipped 2.5% this week after kicking-off REIT earnings season with a solid report, but conceded that it continues to see "challenges" in some markets as "near-term outsized deliveries are met with still recovering demand." Prologis reported full-year FFO growth of 10.4% - 20 basis points above its most recent guidance - and expects FFO growth in 2024 of 9.2% at the midpoint of its initial range. At the property-level, Prologis achieved same-store NOI growth of 10.0% in 2023 - fractionally above its prior guidance - and sees same-store growth of 8.5% in 2024. While PLD noted that market rents have turned negative on a year-over-year basis following three years of record-setting growth, the "embedded" growth within the portfolio remains substantial as leases (typically signed with 3-6 year terms) get reset at market rates. PLD recorded net effective rent growth over the quarter of 74%, bringing the full year to a record of 77%.

{kind=link}

PLD forecasts that annual market rent growth will average between 4% and 6% over the next three years, with 2024 "being modestly positive and ramping thereafter." At the market level, PLD noted that rent growth and asset pricing have remained strongest in Sunbelt markets, while Southern California has been an area of pronounced weakness, where rents dipped by 7% in Q4. PLD highlighted two catalysts for strengthening fundamentals by late 2024 and into 2024: an "emptying" supply pipeline given the dearth of recent construction starts, and the "escalating issues in both the Suez and Panama canals, together with the resolution of the West Coast labor negotiations," which have revived some recent movement back to West Coast ports. PLD also provided its initial supply/demand forecast for 2024, projecting 250M square feet of net absorption this year, offset by 285M square feet of completions. Vacancy is expected to peak at 6% around mid-year, and then "making a meaningful move" lower beginning in late 2024 as supply growth moderates. Also of note, PLD commented that it expects acquisition activity to be "much, much higher" in 2024 after a "low-volume year" in 2023.

{kind=link}

Storage : This week, we published Self-Storage REITs: Victims of Their Own Success . Storage REITs delivered incredible growth early in the pandemic, driven by surging housing market activity, but have been victims to their own success of late amid a supply-driven cooldown. Robust double-digit rent growth and relatively low operational barriers to entry prompted a wave of new development, with a roughly 12% expansion in total supply expected between 2022 and 2024. This supply boom- twice the magnitude of the multifamily sector- has reignited fierce "storage wars" between competing facilities, which has led to double-digit dips in new lease rates since mid-2022. Storage demand is driven largely by housing activity – specifically, home sales and rental market turnover - and the recent moderation in mortgage rates has eased some concerns and sparked a rebound for self-storage REITs following a period of weak performance from mid-2022 through late 2023. Softer fundamentals combined with the surge in financing costs have hit the smaller, more highly-levered owners in these markets particularly hard. We expect storage REITs to leverage their stellar balance sheets to scoop-up highly-levered upstarts seeking an exit, providing some accretive external growth at a time of flat-to-negative organic growth.

{kind=link}

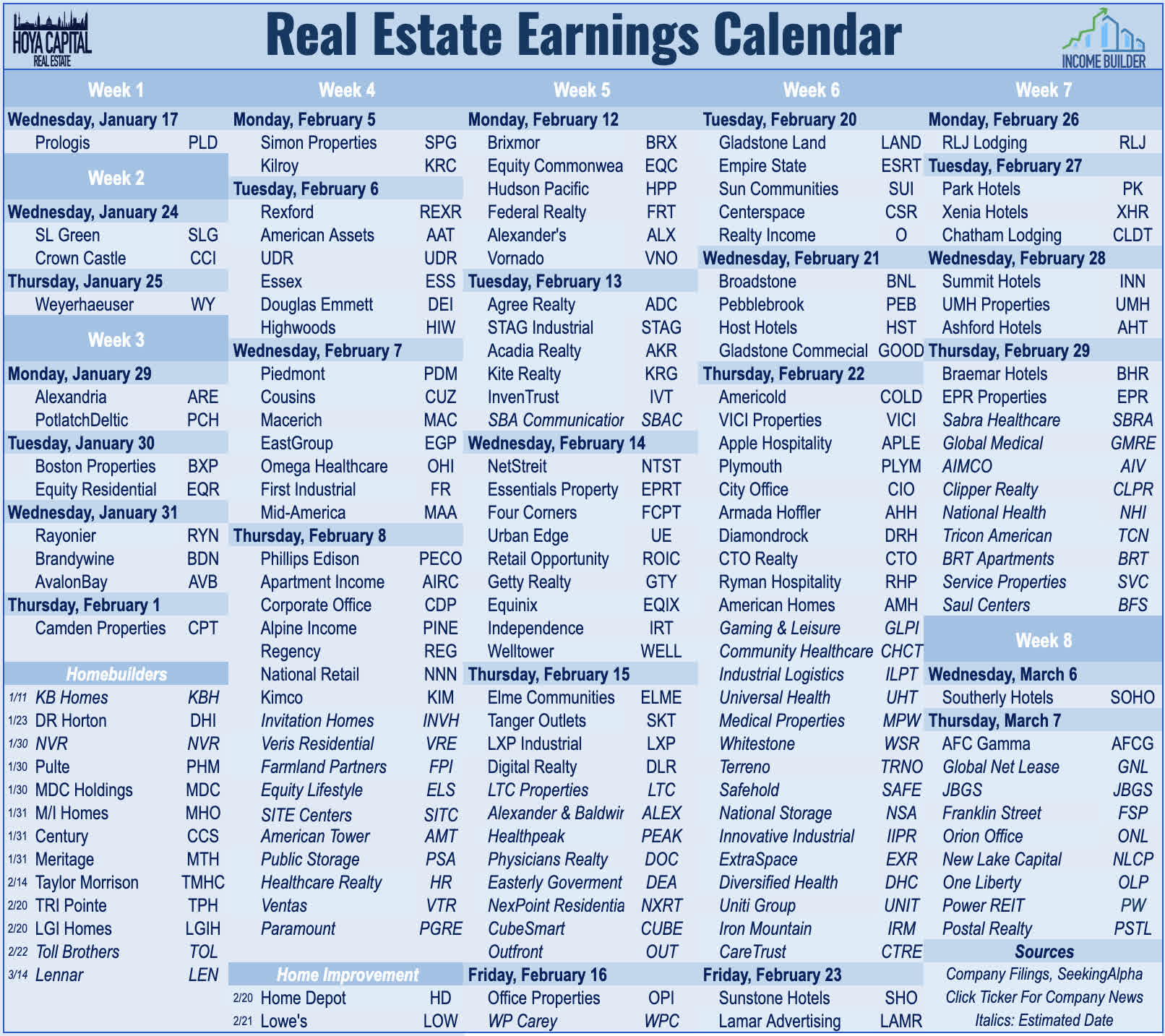

The bulk of real estate earnings reports occur in early to mid-February, but we'll see a trio of REIT reports in the week ahead from office REIT SL Green ( SLG ), cell tower REIT Crown Castle ( CCI ), and timber Weyerhaeuser ( WY ), along with results from homebuilder D.R. Horton ( DHI ). We'll publish our REIT Earnings Preview next week, which will discuss the major themes and metrics we're focused on this earnings season. Below, we compiled the Real Estate Earnings Calendar for Equity REITs and Homebuilders. (Note: Companies that have not announced a release date are in Italics with an estimated date).

{kind=link}

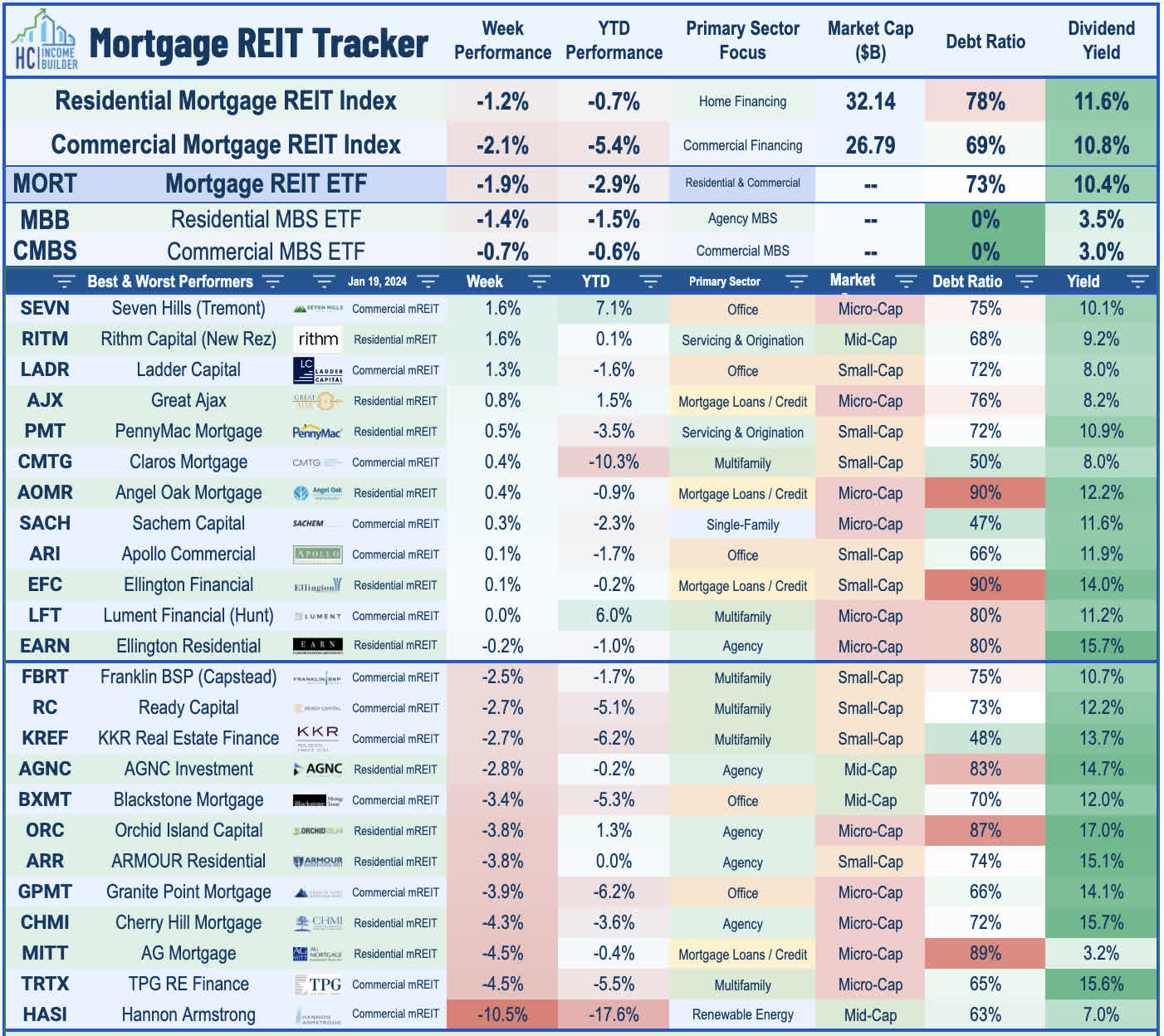

Mortgage REIT Week In Review

Pressured by the rebound in interest rates, Mortgage REITs declined for the third-week in the past four, with the iShares Mortgage REIT ETF ( REM ) slipping 1.9% this week. On an otherwise quiet week of mREIT-related newsflow, Redwood Trust ( RWT ) launched a $60M public offering of exchange-listed 9.125% senior notes due 2029. The "baby bond" will trade on the NYSE under the symbol “RWTN.” Last week, MFA Financial ( MFA ) also issued a new exchange-listed "baby-bond" which will begin trading on NYSE later this month. As with the equity REIT sector, we'll see a trickle of mREIT earnings reports over the next few weeks - kicking off with AGNC Investment ( AGNC ) on Monday - before the bulk of the sector reports in early-to-mid February. Also of note, Hannon Armstrong ( HASI ) has remained under stiff pressure since it announced that it will no longer operate as a REIT, dipping another 10% this week to extend its losses to nearly 20% this year.

{kind=link}

As discussed in our prior Weekly Outlook , mortgage REITs are likely to report their best quarter for underlying Book Values since the start of the pandemic. The Residential MBS ETF ( MBB ) - which tracks the un-levered performance of residential mortgage-backed securities - posted total returns of 7.3% in Q4 - one of its strongest quarters on record. The Commercial MBS ETF ( CMBS ) - which tracks the un-levered performance of CMBS - posted gains of 5.0% in Q4, also one of its strongest quarterly gains on record. MBS valuations have been under some pressure in early 2024 as the lift in benchmark rates has offset the continued tightening of spreads. RMBS valuations are lower by about 1.5% so far in 2024, while CMBS valuations are lower by 0.3%.

{kind=link}

2024 Performance Recap & 2023 Review

Through three weeks of 2024, the Equity REIT Index is lower by -4.4%, while the Mortgage REIT Index is lower by -2.9%. This compares with the 0.2% gain on the S&P 500 , the -2.4% decline for the S&P Mid-Cap 400 , and the -4.8% decline for the S&P Small-Cap 600 . Within the REIT sector, all 18 property sectors are lower for the year, led on the upside by Hotel and Mall REITs, while Farmland and Cell Tower REITs have lagged on the downside. At 4.15%, the 10-Year Treasury Yield is higher by 27 basis points on the year, but the 2-Year Treasury Yield has dipped 8 basis points to 4.35%. Following a late-year rally in the final months of 2023, the Bloomberg US Bond Index is lower by 1.4% this year. WTI Crude Oil is higher by 3.6% this year, while Natural Gas has rallied 10%, but the broader Commodities ( DJP ) complex remains lower by 1.2%.

{kind=link}

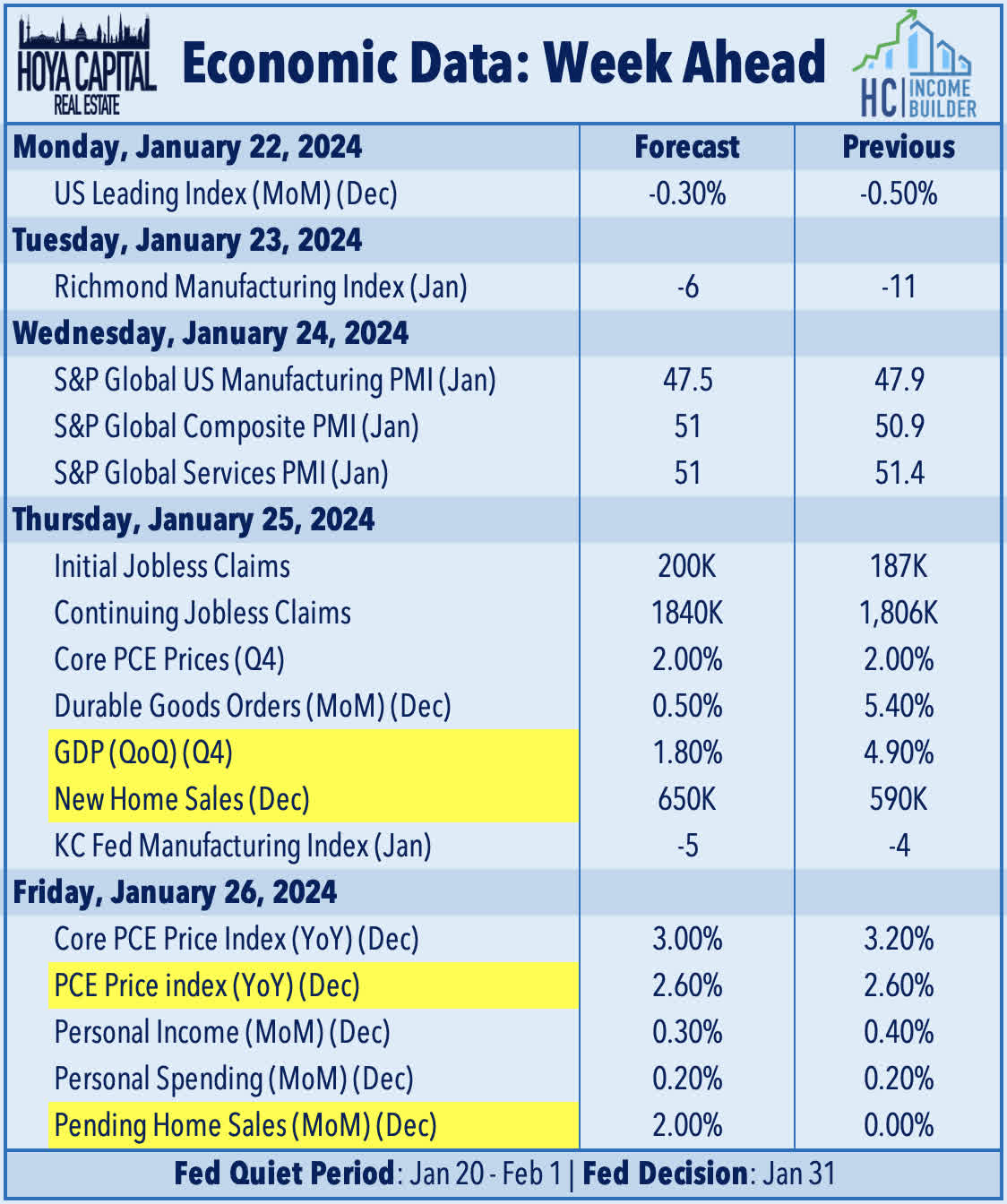

Economic Calendar In The Week Ahead

We'll see another fairly busy week of economic data in the coming week as the Federal Reserve enters its "quiet period" ahead of its January 31st policy decision. On Thursday, we'll get our first look at fourth-quarter Gross Domestic Product , which is expected to show a deceleration in growth in the fourth quarter to a 1.8% annualized rate from the 4.9% rate in the third-quarter. New Home Sales data on Thursday is expected to accelerate to a 650k annualized rate as the largest builders have been able to cope with multi-decade-high mortgage rates by leveraging their relatively healthy balance sheet to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market. We'll also be closely watching the PCE Price Index on Friday - the Fed's preferred gauge of inflation - which is expected to show an annual increase of 2.6% - down sharply from the 7.0% rate seen a year ago.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Rate Cut Rethink