RJF - Raymond James: Definitely A Decent Showing YoY Growth If Not For SEC Lawsuits

2023-12-01 14:06:30 ET

Summary

- Raymond James performed well, in line with mid-market peers in their IB business, and benefited from some resilience in brokerage, although they have too much FI exposure.

- The market rally helped them in their asset management business, and the MM focus in IB let them attach to recent ebullience.

- However, there were quite a few inorganic effects, and a company like Lazard is more respected and has a cleaner model to study and follow.

- Moreover, they offer a yield and do look cheaper, with a more vigorous EU exposure than RJF.

The YoY performance in Q4 was good, pointing to improvements in conditions owed to Raymond James ( RJF ) substantial focus on AUM driven businesses. Their IB franchise is performing in line with mid-market peers, and their model is quite stable when removing some of the one-off expenses like that related to the sweeping SEC off-platform lawsuit. However, there were quite a lot of inorganic effects that made results quite rosy, with a doubling almost in the bank business due to the TriState acquisition. While we can't complain, we still prefer Lazard which is more Europe focused but still has an anchor in asset management.

Breakdown of the Q4 and FY

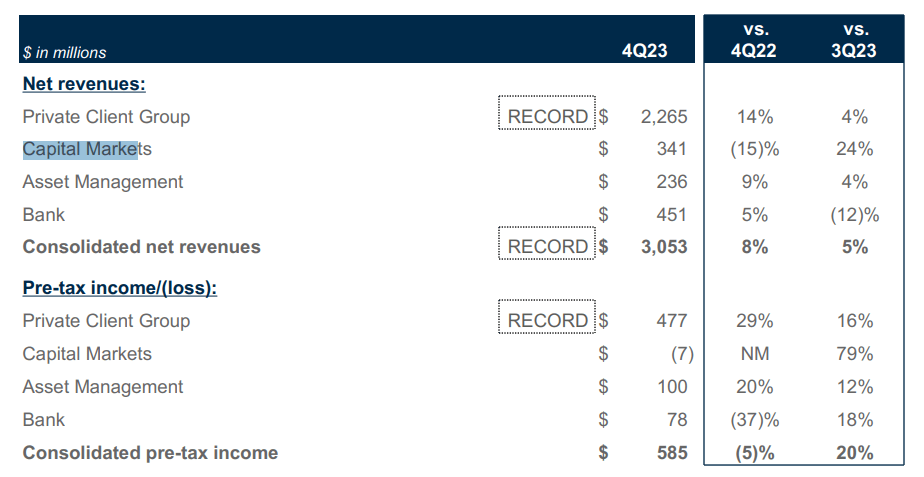

The following is the Q4 breakdown of results.

{kind=link}

Some of the declines in income are from increased regulatory provisions around the SEC lawsuit concerning off-platform communications. The amount was $55 million, so a meaningful 10% negative delta on the quarterly results.

PCG was up thanks to YoY growth in AUA in fee-based accounts. That growth mirrored exactly the PCG revenue growth of 15%. Similarly, AM grew quite in line with growth in accounts. General market appreciation also helped. They did not add a lot of advisors to their teams here.

{kind=link}

Capital markets is composed of substantial M&A advisory revenue, almost half, and the rest is related to underwriting and brokerage. Activity in PCG created higher brokerage revenues there, but sidelined fixed income players means not much growth in fixed income brokerage.

M&A is up 34% sequentially, and also up 7% YoY, which is a strong performance in absolute terms and in line with what we would have expected from a mid-market player, where the mid-market is the more resilient segment right now, less dependent on big ticket financing. However, the deals are pretty unpredictable, and the next quarter may look incrementally worse .

Worsening NIMs and flattish loan growth meant an underwhelming bank performance YoY.

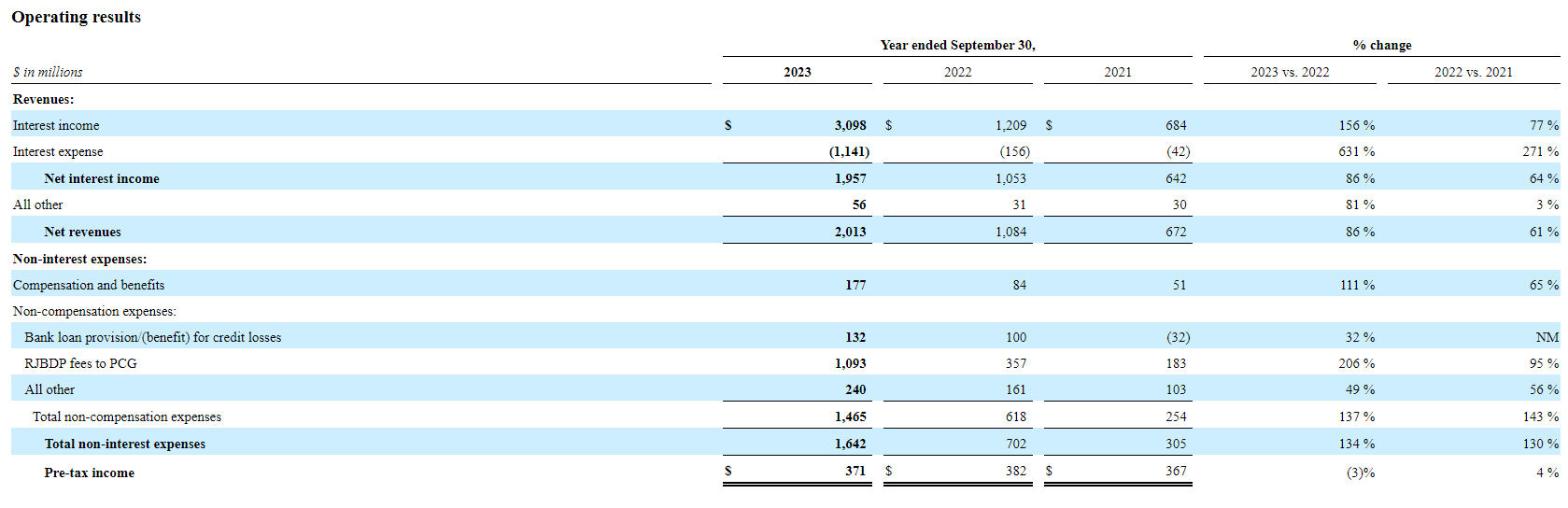

The FY results are pretty different, starting from bank.

{kind=link}

TriState was acquired halfway through last year, so that year's results ignore half of the contribution that TriState is making to 2023 results. Therefore, inorganic base effects means a rocketing set of figures. An incremental $30 million, or 10% effect came from changing provisions based on macroeconomic concerns YoY.

{kind=link}

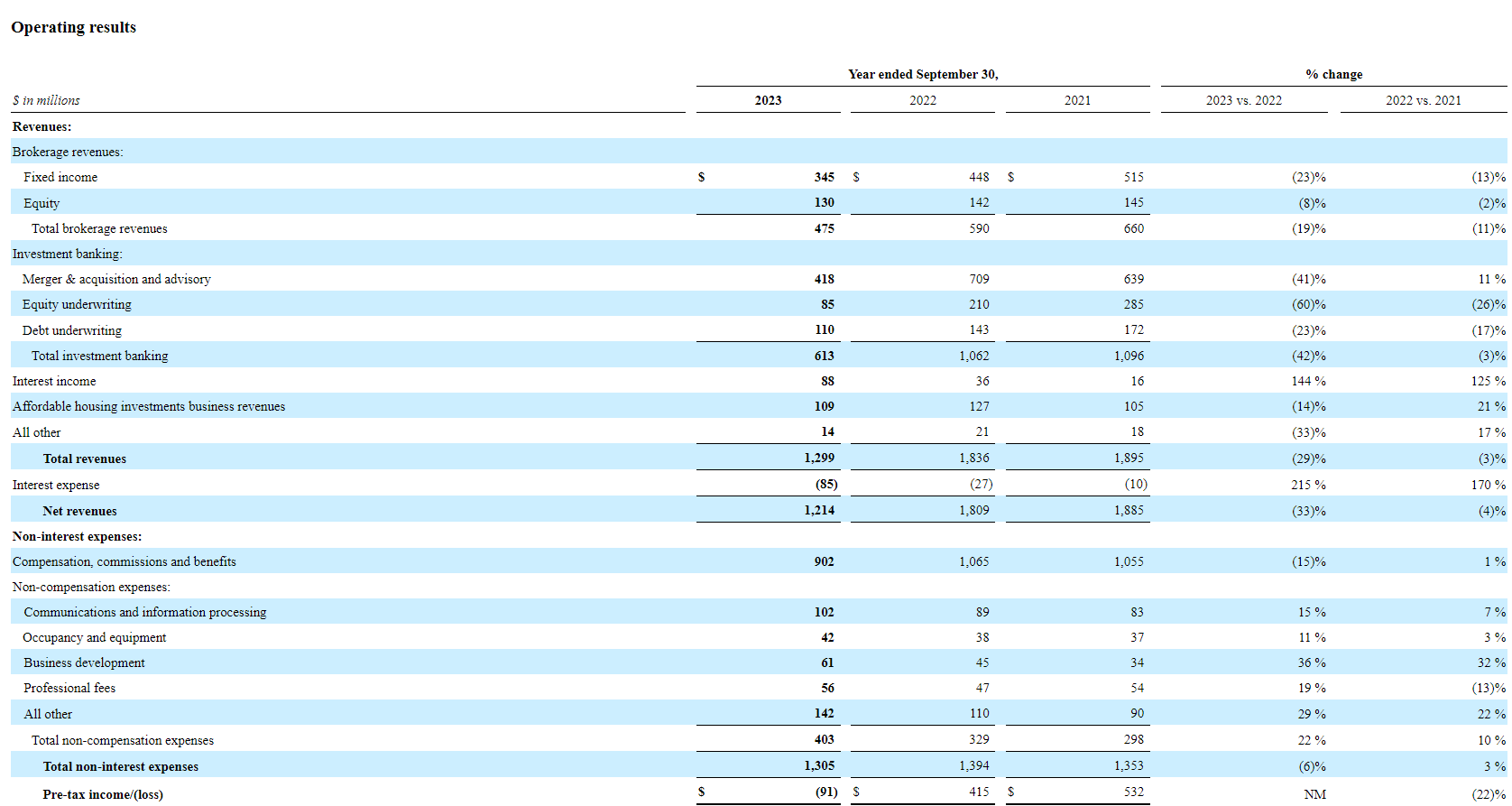

People are coming off the sidelines now in fixed income, hence the on and off bond rallies recently, so the Q4 results look better than the FY results in FI. Equity is flattish to down due to reduced overall FY volatility, but was probably worse in the Q4 breakdown. IB was much worse in the FY due to the very weak beginning of 2023, which just kept coming down from the highs of early 2022. Declines here in mandates are more consistent with the general dealmaking environment, and Q4 was a relatively good performance. Unsurprisingly, weak issuing activity means that M&A, which still had at least some FY strategic relevance, outperformed ECM meaningfully. DCM wasn't as bad, but clearly a lot of corporates are still holding off on refinancing at these high rates.

{kind=link}

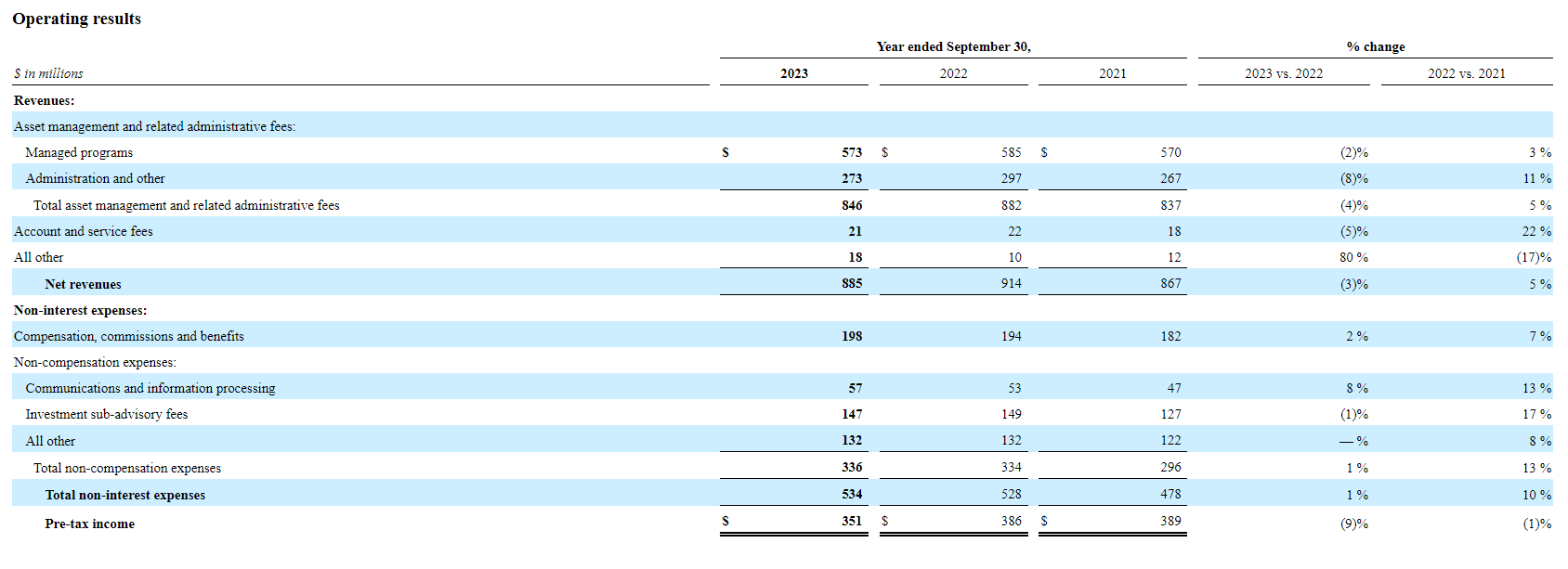

In AM, the FY results were worse since the rally was concentrated in the latter half of 2023.

Bottom Line

Performance looked good, while of course some of the growth, like from TriState, was inorganic. Mid-market continues to be attractive in M&A, and AM is pretty resilient. But when we compare RJF to Lazard ( LAZ ) on performance, we are more impressed by LAZ's results. Also, they seem to earn more on performance based fees, which should give them a kick this year. Furthermore, the IB franchise is more exposed to Europe which has been more consistent, and is aided by a better credit environment than in the US. RJF is far more US exposed than LAZ .

While currently LAZ is getting smashed by their outperformance last year in comp expenses this year, and therefore income is dipping into negative since there's still been a shortfall in revenues on the capital markets side, we still prefer Lazard. The more obviously peaking rates in Europe is attracting allocator attention in general, where Lazard is more exposed. They are also less supported by inorganic factors. While RJF trades at EV/Revenue of 1.3x, LAZ is 1.1x. Historically, LAZ has also been buyable at better rates and with dividends. There's nothing wrong with RJF, but we think LAZ has more going for it as we eventually start seeing rising rates again, and a large restructuring franchise in case it's still further off than expected.

For further details see:

Raymond James: Definitely A Decent Showing, YoY Growth If Not For SEC Lawsuits