RJF - Raymond James Downgraded To Hold An Overvalued But Strong Earner

2023-09-13 10:18:55 ET

Summary

- Raymond James Financial downgrade to Hold from my Buy Rating in June, agreeing with the quant system rating.

- Positives: dividend growth/stability, earnings YoY growth, company financial health.

- Challenges: overvaluation vs sector, share price +8% higher than June.

- Downside risk of credit loss provisions has been discussed, too.

Research Summary

Today I'll be rating Raymond James Financial (RJF) , in the financials sector, subsector of investment banking / brokerage.

I last rated this stock on June 17th when I rated it a buy. Since then, it had its FY2023 Q3 earnings result on July 26th and I will do a deep dive into some of that data to see if my prior rating stands.

I am pleased to report that since my last buy rating, the share price has risen by 8.3%:

RJF - price gain since last rating (Seeking Alpha)

For readers less familiar with this company, here are a few relevant points from their website that I think could be interesting to readers: roots go back to 1962, diversified business segments include wealth advisory / investment banking / equities research. Their banking segment is called Raymond James Bank , an FDIC member bank.

Two key peers of this company, according to Seeking Alpha data, are Nomura Holdings (NMR) and Robinhood Markets (HOOD).

A fun fact, according to Wikipedia , is that Raymond James is listed as #39 in the largest banks in the US .

Rating Methodology

Using a process similar to 5 project phases in project management, I break down my overall holistic rating of this stock into 5 categories I rank individually and of equal weight: dividends, valuation, share price, earnings growth, financial health.

If I recommend this stock on at least 3 of 5 categories, it gets a hold rating. 4 of 5 gets a buy, and less than 3 gets a sell rating. Then I compare my rating to the consensus from analysts, Wall Street, and the quant system.

Dividends

In this category, I will analyze the dividends of this stock and whether I think they present an opportunity for dividend-income investors. The data comes from official Seeking Alpha dividend info.

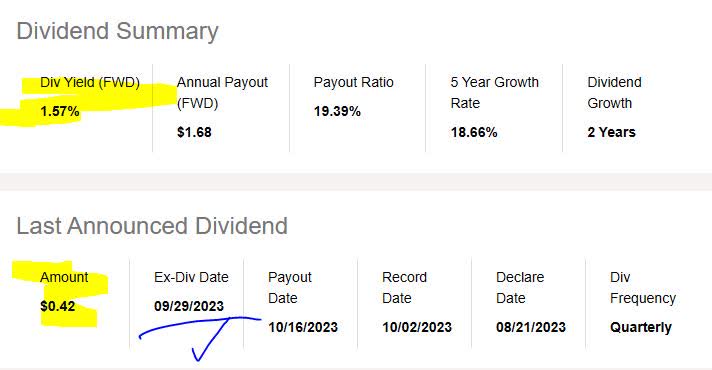

As of the writing of this analysis, the forward dividend yield is 1.57% , with a payout of $0.42 per share on a quarterly basis, with an upcoming ex-date on Sept. 29th that could be an opportunity to take advantage of.

While this yield may not seem like anything to write home about, as I have come across some that over 5% lately, it is only one factor in the whole picture, and next I will see how it relates to the sector overall.

{kind=link}

When comparing to its sector average, this dividend yield is 59% below its sector average. I believe this is a negative point to consider for dividend investors who are comparing multiple stocks in which to invest. In my opinion, my target range is 3% - 5%, to stay within a few points of the sector average. In this case, the yield seems low, and even got a "D-" rating from Seeking Alpha which does not add confidence to this stock.

RJF - div yield vs sector (Seeking Alpha)

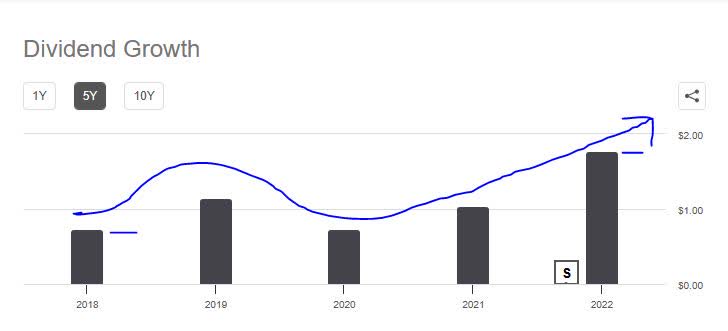

In looking at the 5-year dividend growth for this stock, it has shown a lopsided growth trend however has improved from 2020 onwards. This is, in my opinion, a modestly positive point for dividend investors and a sign of this firm's capacity to return capital back to shareholders.

{kind=link}

Additionally, I am looking for stability with dividend payouts, and this stock has shown regular dividend payment history lately without interruption, and also had paid out an extra quarterly payment in 2022 it seems, which is a positive point to think about.

RJF - div history (Seeking Alpha)

On the whole, although the yield is considerably below sector average what makes up for it is the recent dividend growth and stability/reliability.

I would therefore recommend this company on the category of dividends.

Valuation

In this category, I will analyze the valuation of this stock. The data comes from official valuation info on Seeking Alpha, specifically the forward P/E ratio and forward P/B ratio, the key metrics I look at.

This stock has a forward P/E ratio of 13.09, which is 37% above its sector average. I think that a reasonable price to earnings for this stock would be between 8x earnings and 10x earnings, to stay within a reasonable 2 point range of the average. In this case, on this metric the stock appears moderately overvalued vs its overall sector.

RJF - PE Ratio (Seeking Alpha)

This stock has a forward P/B ratio of 2.17 , which is a whopping 119% above its sector average . I think that a reasonable price-to-book value for this stock would be between 0.50x book value and 1.5x book value, to stay within a 1/2 point range of the average. In this situation, this stock appears severely overvalued vs its overall sector.

RJF - PB ratio (Seeking Alpha)

Based on the examples I gave, with the stock being moderately to severely overvalued on both metrics I track, I would not recommend this stock on the basis of valuation.

Share Price

Next, I determine if the current share price is a potential buying opportunity based on my portfolio goal of buying at current price, holding for 1 year until Aug. 2024, and achieving an unrealized gain of 10%.

The price chart (as of the writing of this article) shows a share price of $106.83, compared to its 200-day simple moving average "SMA" of $102.83 , over the last 1-year period.

Next, I plug in the current SMA and share price into the following simulator I created, which simulates unrealized gains & losses if the share price as of Aug. 2024 reaches +10% above the current SMA but also if it drops -10% below the current SMA:

{kind=link}

In the above simulation, my goal is to meet or exceed a +10% unrealized gain in 1 year, and I have a maximum loss tolerance of -10% unrealized loss.

Based on the simulation results testing the current buy price, I fall short of my goal for unrealized gains, only generating 3.77% in unrealized gains. I also exceed my loss tolerance since my projected unrealized loss is -15.09%.

In this case, I would not recommend the current buying price.

Since every investor has different profit goals and risk profiles, consider this simulator just a general framework to help think about this stock in a longer-term sense, with the moving average being a long-term trend indicator.

Earnings Growth

In this category, I examine the earnings trends over the last year, looking at both top-line and bottom-line results but also any relevant company commentary.

The first thing I want to call out that is relevant in this rate environment is the fact that since I last wrote about this firm they achieved YoY positive growth in net interest income, a great sign I think that points to this firm benefitting from this elevated rate environment.

Looking forward, I think considering that CME Fedwatch is predicting the Fed keeping rates the same after their next meeting, continued tailwind from that will benefit this firm's interest-earning assets but also the challenge of managing increased interest expenses also.

{kind=link}

On a YoY basis, also impressive is that the total revenues also showed positive growth, so this firm is a proven money-maker beyond just interest-earning assets it holds. It also makes money, for example, from trading, asset management fees, investment banking fees, and gains/losses from selling assets.

This points to a highly diversified business model, in my opinion.

{kind=link}

To help me understand what was the driver behind some of these results, I turned to the (quarter name) earnings commentary and presentation.

Also, the bottom line showed YoY positive growth, which I think shows this firm can manage expenses effectively as well.

{kind=link}

Turning to earnings comments from CEO Paul Reilly , we can see the positive sentiment that management has for this firm:

Through the strength of our businesses and perseverance of our advisors and associates, we generated record net revenues and record net income to common shareholders during the first nine months of the fiscal year, up 5% and 22%, respectively, over fiscal 2022 despite challenging macroeconomic conditions.

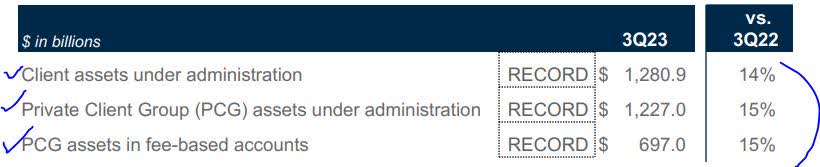

Since it was brought up by readers in the comments a while back, I agree it is important to mention something about growth in assets under administration "AUA", since those generate fees for the firm.

Consider that after my last rating, the latest quarterly results showed some records being set in terms of "AUA", according to the table below. Again, this is relevant because this firm makes money in part by looking after other's money. So, in this industry, growth in assets it is looking after is a positive sign.

{kind=link}

Based on this evidence as whole, I would recommend in this category and expect continued strong results in the next quarter that meet or exceed the prior results, since the firm seems to have the momentum already.

Financial Health

In this category, I will discuss whether the overall company shows strong financial fundamentals beyond just things like dividends, valuation, earnings and share price, with a focus on the capital strength.

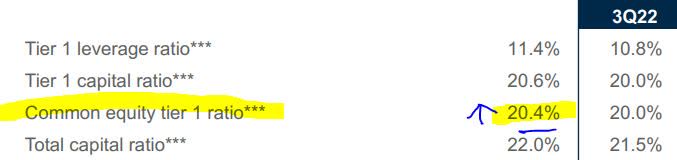

For one thing, I would call out the strong capital ratios of this firm, particularly the CET1 ratio as it is a regulatory standard in the banking industry, and this firm's ratio is past 20% in the last quarter, so well past regulatory benchmarks.

{kind=link}

In addition, dividends payouts and share repurchases by this firm have been continuous since 3Q22, showing more signs of capital strength.

RJF - dividends & share repurchases (company presentation)

According to CEO Reilly, "importantly, our strong capital ratios and flexible balance sheet keep us well-positioned as we look forward."

Speaking of balance sheet , the firm shows $8.3B in cash and $77.6B in total assets, while having just $67B in total liabilities, having around $9.8B in common equity. It has had positive equity for several years actually.

Based on the data, I recommend in this category, and consider it a firm with solid fundamentals.

Rating Score

Today, this stock was recommended in 3 of my 5 rating categories, earning a hold / neutral rating from me today, which is a modest downgrade from my buy rating 3 months ago.

This time I am agreeing with the consensus rating from the SA quant system which also rating it a hold, however I am less bullish than the analyst & Wall Street consensus.

RJF - rating consensus (Seeking Alpha)

My Rating vs Downside & Upside Risk

My neutral rating can face a downside risk as follows:

Investors and analysts could feel bearish about this firm considering the elevated provision for credit losses vs the prior year, as the table below shows, plus a QoQ increase in net charge-offs.

{kind=link}

However, the firm gave reassuring messaging in their quarterly earnings remarks, pointing to a light at the end of the tunnel:

Despite a higher provision, the credit quality of the loan portfolio is solid, with criticized loans as a percent of total loans held for investment ending the quarter at 0.94%, down from 1.63% at June 2022 and up slightly from 0.92% at March 2023.

My rating can also face an upside risk as follows:

This firm continues to be a powerhouse in the wealth advisory space. This could make my rating too cautious, as investors and analysts continue to be bullish on this firm, seeing its potential growth in fees from managing wealth.

Consider that, according to an article last week in Investment News , Raymond James added a $317MM wealth advisory team to its ranks recently.

However, RayJay is not quite among the biggest fish in this space and so I would not be overly bullish on them just on wealth management alone. A 2023 ranking of top 10 wealth management teams by Forbes actually shows the top echelon dominated by teams affiliated with Morgan Stanley (MS), Merrill Lynch , and UBS (UBS).

Analysis Wrapup

To wrap up today's discussion, here are the key points we went over:

This stock got a hold rating today.

Its positive points are: earnings YoY growth, financial health, dividends growth & stability.

The headwinds it faces are: valuation, share price.

Both upside & downside risks have been addressed.

In closing, I continue to have this stock on my watchlist in the financials sector, and consider it worth monitoring for the foreseeable future definitely. What I particularly like about its business model is the diversification across banking, advisory, the in-house research shop, and large institutional trading desk. At the same time, traditional "branches" have not yet gone the way of the dodo and this firm has over 3,000 retail offices .

Though I don't consider it a great "buy" potential at the moment like I did in June, I also would not want to sell it off just yet either.

For further details see:

Raymond James Downgraded To Hold, An Overvalued But Strong Earner