RCS - RCS: Far Too Expensive To Justify A Purchase

2023-09-12 17:43:57 ET

Summary

- PIMCO Strategic Income Fund offers a high current yield of 11.27%, which is higher than most other assets in the market.

- The fund's share price has remained flat over the past year despite rising interest rates. This has been a better performance than most other bond funds.

- The fund primarily invests in investment-grade debt securities using leverage to boost its effective yield.

- The fund has failed to cover its distributions over the past two years, casting doubt on its ability to avoid a distribution cut.

- The fund is trading at an incredibly expensive price right now that cannot be justified based on its actual portfolio performance.

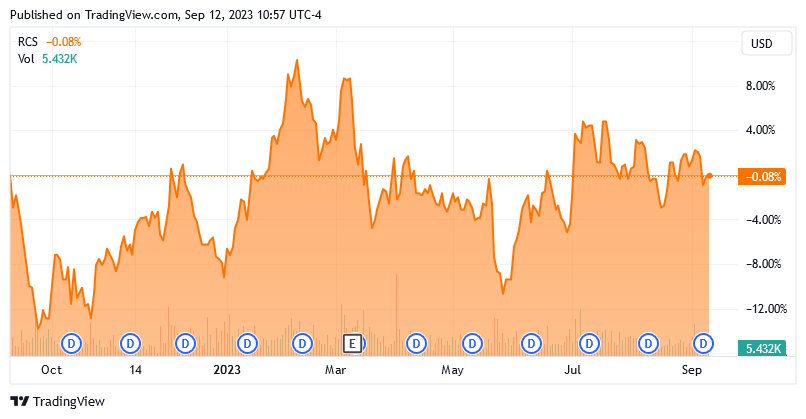

The PIMCO Strategic Income Fund ( RCS ) is a very popular closed-end fund, or CEF, among investors who are seeking to earn a high level of current income from the assets in their portfolios. The fund generally does a good job at this, as its 11.27% current yield is quite a lot higher than just about anything else in the market. The fund has also given a reasonably strong performance recently, especially for a debt fund. In fact, as we can see here, the fund’s share price has been almost flat over the past year:

{kind=link}

This is despite the fact that interest rates have increased by quite a lot over the period in question, which has pushed down the price of just about every other fund that invests in debt securities. This has, arguably, made this fund incredibly expensive and in fact, its shares are trading for a price that is far above their intrinsic value. It is not unusual for a PIMCO closed-end fund to trade at a fairly high premium, but this one is well beyond that of even its sister PIMCO funds. As such, it might not be a great pick for risk-averse value investors despite the attraction of that yield. This certainly does not mean that this is a bad fund, though, as there are certainly many things to like about it. The only real problem here is the incredibly high price that investors have to pay to get access to it.

About The Fund

According to the fund’s website , the PIMCO Strategic Income Fund has the objective of generating a higher level of current income than is available from an ordinary portfolio of medium-term investment-grade debt. This is, to put it mildly, one of the most specific investment objectives that I have seen any fund possess. Normally, a fund like this will state that it seeks to achieve a high level of current income. This one certainly goes a lot further, though:

PIMCO Funds

As might be expected from both this objective and from the fact that this is a PIMCO fund, the fund seeks to achieve its objectives by investing primarily in debt securities. The website specifically states:

“The fund normally invests at least 80% of its net assets (plus any borrowings for investment purposes) in a combination of income-producing securities of non-corporate issuers, such as securities issued or guaranteed by the U.S. or foreign governments, mortgage-related or other asset-backed securities issued on a public or private basis, corporate debt obligations, and other income-producing securities of varying maturities issued by U.S. or foreign (non-U.S.) corporations or other business entities, including emerging market issuers and municipal securities.”

If we need any more confirmation that this is a debt fund, we can get it by looking at the fund’s portfolio, which mostly complies with this description of its strategy. As of the time of writing, 76.39% of the fund’s portfolio is invested in bonds alongside a fairly large allocation to cash:

CEF Connect

This is, in fact, one of the largest cash allocations that I have ever seen a fund possess. Indeed, due to that cash allocation, the fund has failed to comply with its own statement that “at least 80% of its assets will be invested in income-producing securities.” However, there are two caveats here:

At least some portion of that cash is going to be invested in money market securities. While CEF Connect might call this cash, it is actually a cash equivalent. Common stock can technically be “income-producing,” even though the fund does not explicitly list it in the strategy description above. The preferred stock position is also going to be income-producing, even though the preferred stock is also not explicitly mentioned above.

The fund’s most recent RCS)%20Portfolio%20Holdings.xlsx&id=9rergRVAF%2bxZTmEhXYD3Ji5obb3vPsUZG%2bnip4CMYnKKnaX1LAvJa4vg%2bBwzJMNwxRWHsAyxQ23pqG0HBHJyyibbj9h6uCOXaYPswh%2f7yC%2fkee4I4JV8X7ZwjzZ6%2f12zSCiYr9zrzFlg75WMGwn9oeZkINwMr2uzNG6eBH93Uu%2bzlI5AJpGJtgOLbmOo0xZY2i8VC%2fn8aGWXpMu0BGE9ypA2kfDMMtoL6jnshyRJ9iSVLO186b7lnPS4AFdM15d2%2bRefI3r3EeEKGtvOxqbhmMXRKKSFWgJDfdbye7fj5UY5AAIu5SVBdW7mUZCfahbaETa0Lv598H%2bXpBfiyV6PTz%2bHqjHHFSgdG10j2KmTmQzswvyk%2bEpp2NUNrB3VcI4IIuBuVjh9iRdSSnaLqAceJfn%2bR%2fudg501Uv5FUmsHjoExSSAzaL4YPSLNU0BXubY6" > holdings report , which dates from June 30, 2023 (so it is a little bit older than CEF Connect’s data) lists a few short-term holdings:

{kind=link}

While the Argentine Treasury bills are definitely not the sort of thing that a money-market fund might be invested in, the repurchase agreements and the U.S. Treasuries might be. This accounts for 6.361% of the fund’s assets. That would certainly be enough to push its “income-producing” securities over the 80% threshold. Thus, this might be a case of CEF Connect classifying money-market securities as cash instead of bonds.

We also see three real estate investment trusts listed in the fund’s holdings report:

{kind=link}

While these are technically common stocks, nobody is going to deny that real estate investment trusts, or REITs, are income-producing securities. After all, real estate investment trusts have to pay out 90% of their net income by law and most of them pay out significantly more than that. This therefore adds to the fund’s allocation to “income-producing securities,” even though real estate investment trusts are not specifically listed as an asset that this fund might invest in. Thus, this fund certainly appears to be meeting its requirement to invest 80% of its assets in income-producing assets even if it might not appear to be on the surface.

As already stated, the fund’s objective is one of the most specific that I have ever seen a closed-end fund possess. It specifically states that it wants to achieve a level of current income that is higher than could be obtained by simply buying high-quality American intermediate-term debt securities. An intermediate-term security is anything with a term between two years and ten years. As of the time of writing, the five-year Treasury has a 4.417% yield. The Invesco Total Return Bond ETF ( GTO ), which invests in short-term, intermediate-term, and long-term bonds, has a 4.17% yield at the current price. This will work reasonably well to see whether or not this fund is achieving its current income goal. We do not have to look very far because the fund’s 11.27% current yield is far above that of American investment-grade intermediate-term securities. The fund’s total return was 11.76% over the past twelve months, so it seems to be satisfying that requirement on a total return basis.

Overall, it certainly looks like this fund is managing to achieve its investment objective and strategy as outlined on its website.

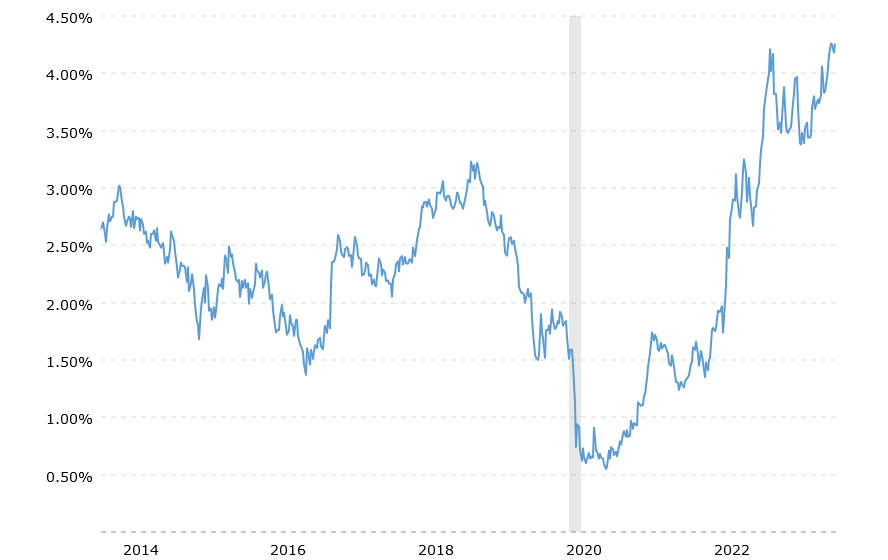

As I have pointed out in numerous previous articles on fixed-income closed-end funds, these funds have a tendency to invest fairly heavily in speculative-grade securities (“junk bonds”) in order to boost their yields. After all, the yield on most investment-grade securities has been fairly minimal over the past fifteen years or so, with the ten-year U.S. Treasury rarely exceeding 3.0%:

{kind=link}

There are very few people that would be satisfied with a 3.00% yield. After all, that is only $30,000 per year on a $1 million investment, and I very much doubt that anyone who managed to save up $1 million would be happy with the lifestyle that they could live on $30,000 annually! Thus, fixed-income funds have been forced to find ways to earn higher yields and one of the easiest ways to do that is to invest in junk bonds, as these securities typically have much higher yields than investment-grade corporate bonds or government securities. The PIMCO Income Strategic Income Fund is no exception to this, as we can see by looking at the credit ratings of the securities in its portfolio:

CEF Connect

An investment-grade bond is anything rated BBB or higher, which would account for 67.55% of the fund’s holdings. This is substantially higher than most closed-end funds possess, as most of them have well under half of their assets invested in investment-grade securities. However, this does still leave a lot of room for junk bonds, and we can see that above.

Perhaps the most interesting thing here is that 16.62% of the fund’s assets are invested in unrated securities. Obviously, we do not know exactly how these would be rated but it is fair to assume that they are more in line with junk bonds than with investment-grade bonds. After all, it is substantially cheaper to carry the payment on an investment-grade security than it is to make the interest payments on a speculative-grade security. As such, any company or entity with a strong enough balance sheet to receive an investment-grade rating would probably spend the money to get its securities rated as such. This would save the company much more money over time than it would actually cost it to have the bonds rated.

For the most part, this portfolio will probably appeal to those investors that are fairly risk-averse. The majority of the bonds here are investment-grade, with most of them being AAA-rated bonds that are highly unlikely to default. However, we do still see that almost a third of the fund’s assets are not invested in investment-grade bonds so there is still quite a lot of exposure to riskier assets. The fact that this fund has 699 total holdings should serve as a source of comfort in this light, as it should mean that the actual losses that the fund suffers in the event of a single entity defaulting will have a negligible impact on the portfolio. For the most part, the only real risk here is interest-rate risk.

Leverage

As mentioned earlier in this article, the PIMCO Strategic Income Fund has the objective of providing its shareholders with a level of current income that is above that of intermediate-grade debt in the United States. While it does include some junk bonds and other assets that will contribute to its ability to do that, the portfolio is mostly invested in AAA-rated securities. These alone are not going to allow the fund to achieve its objectives. Thus, the fund needs to use some method to artificially boost the effective yield of its portfolio. One way to accomplish this is through the use of leverage. I explained how this works in a recent article about another PIMCO fund:

“In short, the fund is borrowing money and then using those borrowed funds to purchase bonds and other income-producing assets. As long as the interest rate that the fund pays on the borrowed money is less than the yield that it receives on the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As a result of this, we want to be sure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.”

As of the time of writing, the PIMCO Strategic Income Fund has leveraged assets comprising 34.19% of its portfolio. This is slightly above the one-third maximum that I prefer, but I am willing to give the fund the benefit of the doubt in this case. First, the fund’s leverage is barely above that one-third level so it might be easily erased in any market rally (although I do not expect any bond market rally to last very long). In addition, this fund is invested mostly in AAA-rated securities, which tend to be less risky than most other assets. As such, it can probably carry more debt than an equity fund could handle. I am inclined to say that the fund is probably fine here, but hopefully, it will not take on any more leverage.

There is one important factor to consider right now when it comes to the fund’s use of leverage. This strategy is much less effective at raising the effective yield of the portfolio than it used to be. This is because the difference between the borrowing rate and the yield on the purchased securities is much less than it was eighteen months ago. As of right now, the federal funds rate, which is the short-term borrowing rate, is significantly above the yield on five-year and ten-year Treasuries. As such, it might be difficult for the fund to be able to borrow money and purchase intermediate-term AAA-rated bonds with a higher yield than the borrowing rate. This would have an adverse effect on the fund’s ability to generate positive returns compared to what it could have achieved back during the post-pandemic euphoria.

Distribution Analysis

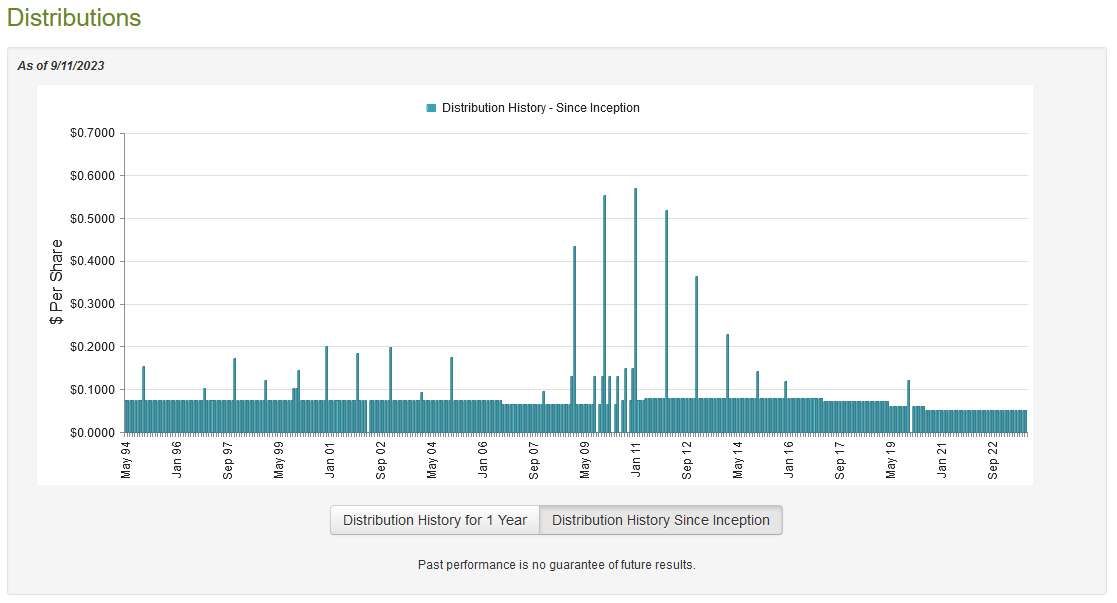

As stated earlier in this article, the primary objective of the PIMCO Strategic Income Fund is to provide its investors with a high level of current income relative to investment-grade intermediate-term bonds. In order to accomplish this, the fund itself is buying bonds in this category and applying a layer of leverage to boost the effective yield. It is also engaging in trading bonds to try and take advantage of price changes. As of right now, the yield of the five-year Treasury is 4.417%, so we can probably assume that the fund has a higher yield than this. That is certainly the case as the fund currently pays a monthly distribution of $0.0510 per share ($0.612 per share annually), which gives it an 11.27% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over time:

{kind=link}

As we can see above, the fund has changed its distribution over time in both a positive and a negative direction. However, the recent trend has been negative, as the fund’s distribution has been steadily declining since early 2017. This is likely to be something of a turn-off for those investors who are seeking a safe and secure source of income that can be used to pay their bills or finance their lifestyles. With that said though, the fund has been more consistent than most other fixed-income funds in recent times as this is one of the few fixed-income funds that did not cut its distribution over the past twelve months.

As is always the case, it is important that we ensure that the fund can actually pay the distribution that it pays out. After all, we do not want to be the victims of a distribution cut since that would reduce our incomes and almost certainly cause the share price to decline. Let us investigate this.

Fortunately, we have a very recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on June 30, 2023. This is one of the most recent financial reports that has been released by any closed-end fund offered by any fund house. Perhaps the nicest thing though is that this report covers a full-year period, so it should give us a good idea of how well the fund handled the challenging bond market conditions in the second half of last year as well as the partial rebound that occurred in the first few months of 2023. There may have been some opportunities during each of these periods for the fund to engage in some trading activities to earn capital gains.

During the full-year period, the PIMCO Strategic Income Fund received $25.382 million in interest and $208,000 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $25.606 million during the period. It paid its expenses out of this amount, which left it with $17.754 million available to shareholders. This was, unfortunately, not nearly enough to cover the $27.677 million that the fund actually paid out in distributions during the period. At first glance, this is likely to be quite concerning as we usually like a fixed-income fund to be able to fully fund its distributions out of net investment income.

However, the fund does have other methods that can be employed to obtain the money that it needs to cover the distribution. PIMCO funds tend to engage in considerable amounts of trading activity (this one has a 639.00% annual turnover) to exploit changes in prices and generate gains. The profits from this activity can obviously be paid out to the fund’s investors. Unfortunately, the fund failed at this task during the period. The PIMCO Strategic Income Fund reported net realized losses of $13.114 million that were only partially offset by $6.292 million in gains. Overall, the fund’s net assets declined by $13.521 million after accounting for all inflows and outflows during the period. This is a repeat of the $80.971 net asset decline that the fund experienced during the preceding full-year period. Thus, this fund has now failed to cover its distributions for two straight years. It is difficult to see how it can really afford to sustain its distribution in that situation. There is a very real risk of a cut here.

Valuation

As of September 11, 2023, the PIMCO Strategic Income Fund had a net asset value of $4.20 per share but the shares currently trade for $5.45 each. That is a 29.76% premium on net asset value. This is not only above the 28.94% premium that the shares have averaged over the past month, but it is also an incredibly high price to pay for any closed-end fund. The premium here is $1.25 per share, which means that it would take just over two years for the distributions to cover the premium. That is far too high of a price to pay for any fund, especially one that has failed to cover its distribution for two years in a row. While I want to like this fund, there is no possible way to justify that high of a premium.

Conclusion

In conclusion, the PIMCO Strategic Income Fund has all of the characteristics of a good fixed-income fund. Its portfolio is invested in securities that are reasonably safe, and its large number of holdings should reduce the risk of those securities that may not be quite so safe.

The problem arises when we look at the fund’s finances, as it has failed to cover its distributions for two straight years now. That makes it incredibly challenging to recommend as it is difficult to see how it will be able to avoid a cut, especially considering its leverage and the fact that interest rates could very easily rise further. The fund’s current price is incredibly expensive even in a good market, but it is virtually impossible to recommend it considering the financial situation.

For further details see:

RCS: Far Too Expensive To Justify A Purchase