RCC - Ready Capital: Distribution Cut Should Be Lauded

2023-12-15 09:45:15 ET

Summary

- Ready Capital showed that it was once again ready to cut its distribution, should the occasion call for it.

- Q3-2023 results showed that the occasion did indeed call for it.

- We break down the recent results and show how the company is facing high levels of stress on Broadmark's acquired portfolio.

- We also tell the bears why they need to calm down.

We like Ready Capital Corporation's ( RC ) management. Since we have started monitoring the firm, they have erred on the side of caution in all their activities. On our last coverage, with the stock at $9.35, we gave long-suffering investors some (well, 3 to be precise) reasons to be a tad more bullish.

A key question will be as to when they dial the leverage back up. If they start doing it now, we would expect poor returns over the next 15 months. If they wait, things should be ok. From a tactical stand point, we would consider a trading buy under $9.00 and a sell rating over $11.50 for this stock.

Source: 3 Reasons To Not Get Bearish Down Here

The stock had a fantastic rally from there and went just a bit over our "Sell" point yesterday. This morning marked a full reversal.

Seeking Alpha

So what's going on? Let us take a quick look at the Q3-2023 results and tell you exactly why we are headed where we are headed.

Q3-2023

RC's Q3-2023 numbers confirmed what we had pointed to in May 2023. Sustainable distributions and earnings are likely be closer to 25 cents a share.

{kind=link}

RC reported 28 cents of distributable earnings, and we think there is some more pressure in the next two quarters. There are a few reasons for that. Originations continue to be weak and RC is finding less convincing opportunities to deploy capital. Compare where activity was in Q3-2022.

{kind=link}

Now adjust all of this origination activity levels for the fact that RC has Broadmark under its fold and a far, far higher share count.

So on a per-share basis, origination activity has collapsed and with it, the distributable earnings per share.

{kind=link}

Before we proceed further, let us quickly add here that this is a good thing. RC's primary bread and butter areas are in distress, and the company showing deep levels of caution is the perfect reaction.

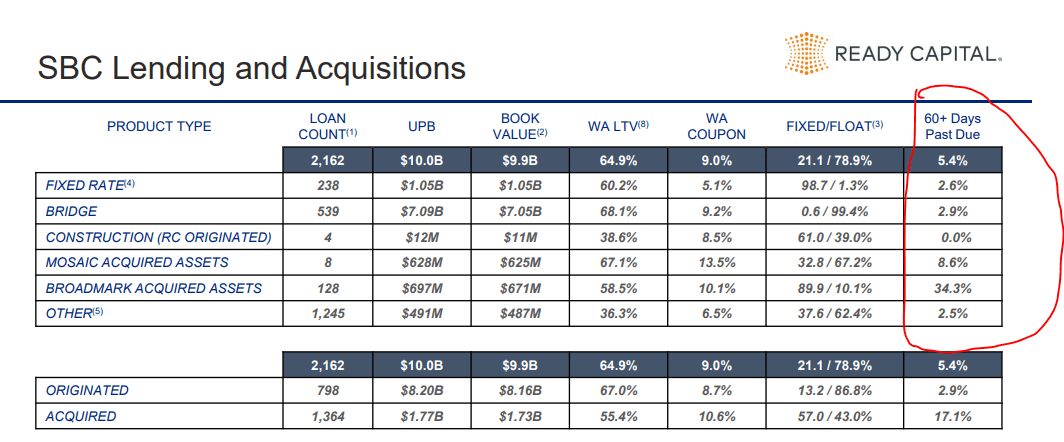

That leads up to the next point, which is why we think there are problems. Well, Commercial Real Estate or CRE as a whole is in trouble, and you would have to be living under a rock financed by a mezzanine loan, not to know about it. RC's 60 days past due number continues to creep up. In Q3-2023, this number was at 5.4%. Broadmark's assets looked like a dumpster fire, with 34.3% past due.

{kind=link}

This 34.3% number has been reduced by the company actually taking over some of these assets and moving them to a different category on the balance sheet. The real estate owned, held for sale, is currently at $281.9 million, up from $117.1 million at end of Q4-2022 (Q2-2023-$251.3 million).

RC 10-Q

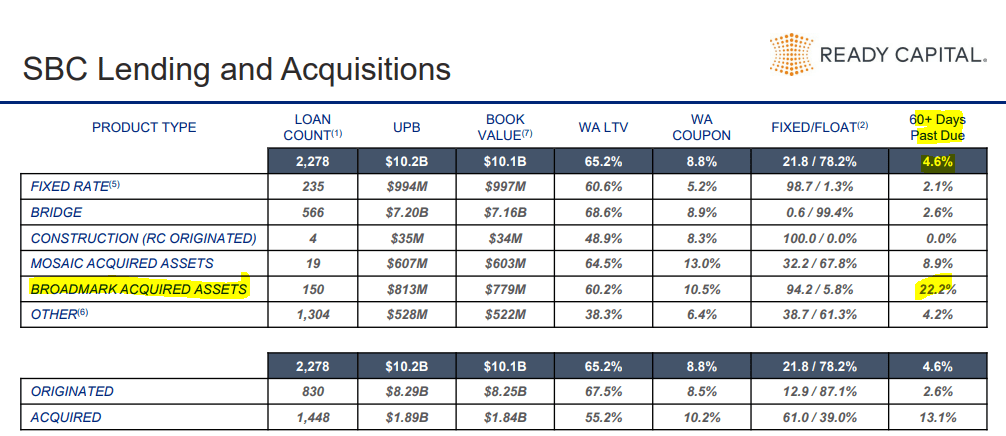

Getting back to the 34.3% of loans that are 60+ days late, that number is up from 22.2% just last quarter.

{kind=link}

Last year, the overall 60+ days past due number was at just 2.4% (versus 5.4% today).

RC Q2-2022 Presentation

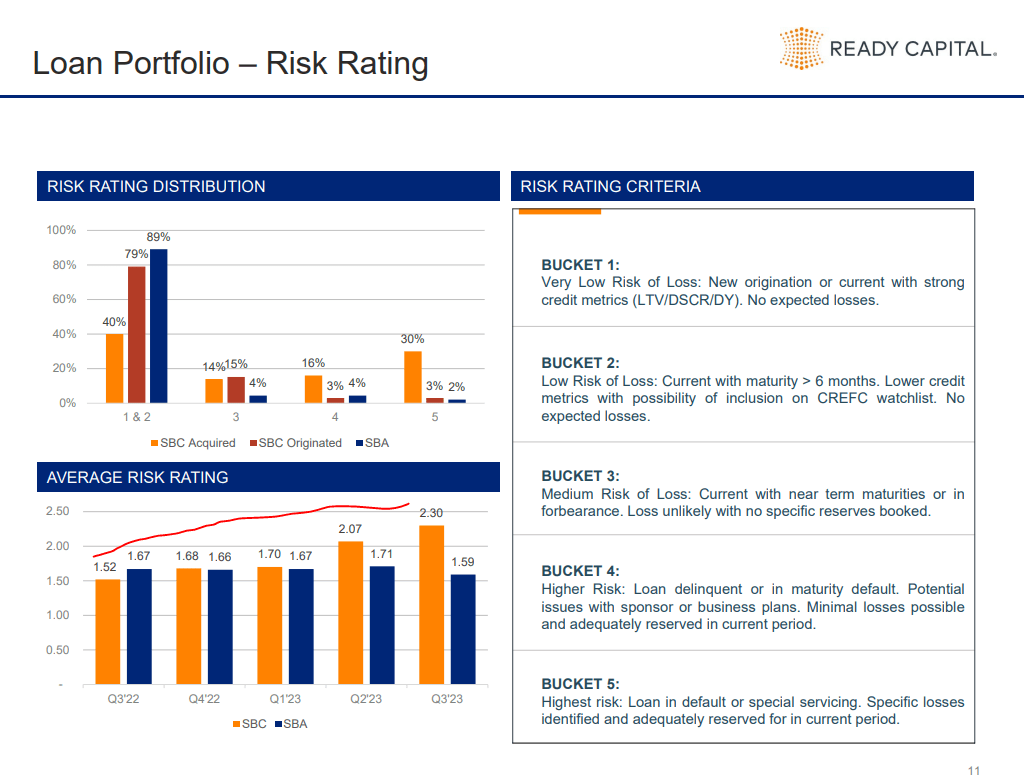

RC does a pretty honest appraisal of their portfolio every quarter, and you can see the SBC category risk levels moving up materially over the past 5 quarters.

{kind=link}

With mortgage REITs (at least the ones that don't operate in the risk-free areas) you have to always remember that small levels of defaults create big blowbacks on the stock. That is how leverage works. So we have a lot of balance sheet level problems that are also flowing down to the income statement.

Outlook

RC cut its distribution for the second consecutive quarter and went with the idea that this was temporary.

The quarterly dividend reflects the impact on earnings of lower leverage and portfolio yield compression due to the ongoing integration of the Broadmark portfolio. The Company expects earnings to migrate towards historical return targets over the course of 2024 as increased liquidity is deployed into current market yields and underperforming assets in the Broadmark portfolio are repositioned into the Company’s proven loan origination and acquisition products. The current dividend will result in the retention of excess liquidity for reinvestment while preserving book value during the coming year.

“The current dividend is a temporary, short-term reflection of our merger with Broadmark,” said Thomas Capasse , Chief Executive Officer and Chairman of the Board of Directors. “We remain confident that the merger will start to deliver long-term earnings accretion as we move through next year and beyond.”

Source: Seeking Alpha

As much as we like what management is doing (i.e. cutting distributions to realign with reality) we are pretty certain they did not foresee this level of problems in their, or Broadmark's, portfolio. If you disagree, you can change your mind after you read the Q4-2022 conference call transcript . The good part here is that RC is firmly focused on preserving tangible book value per share, and they are not paying more than what they are making. This is an excellent strategy for preserving value. It does not work very well for retaining "income investors". Added to this is the fact that recourse leverage is just at 0.9X. Total leverage is also on the low side.

RC Q3-2023 Presentation

What is making us a bit nervous this morning is the fact that Broadmark's 60-day rate delinquency rate is off the charts. The loan to value ratios there should likely ensure a net positive outcome, but this is hardly going to be a walk in the park. There is a long slog here, even in a soft landing. In a hard landing, we would expect some damage to book value, likely wiping out $1-$2 per share.

Verdict

Some setups are difficult, and you can look foolish being extremely bullish or bearish. This is one of them. The chronic distribution cuts might make the bears excited, but let us not forget that there is a big tangible book value buffer ($14.42) relative to the price. So bears will get some blood if they went in near the $11.50 price point we suggested, but it won't be easy unless things break market wide. Bulls likely have some ability to make money if you buy it deep under tangible book. For our part, we have stuck with Ready Capital Corporation 6.50% CUM PFD E ( RC.PR.E ). The very low levels of recourse leverage, alongside a management that is "ready" to deal with common shareholders in order to preserve tangible book value, make this a no-brainer. Since our entry in July 2022, the preferreds have actually done better than the common shares in total returns, despite having a smaller yield. They have also done so with far lower volatility. We remain positive on those and would look to get constructive on RC common shares only under $9.00 per share.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Ready Capital: Distribution Cut Should Be Lauded