AGNCP - Ready Capital: Leverage Vs. Distributions

2023-08-08 16:01:20 ET

Summary

- Ready Capital reported Q2-2023 results with a higher provision for credit losses.

- Distributable income fell short of actual distributions, again.

- Q3-2023 should see a further drop and we tell you how we would play this company.

On our last coverage of Ready Capital ( RC ) we spoke about the distribution and its unsustainability over the long run.

The base run-rate for Ready Capital already looks like it cannot keep up with the distribution. We will add another 62 million shares on BRMK's closing, and that side of the equity will produce progressively less income over time. Sure, some loans will be paid off and can be reinvested, but we doubt Ready Capital will be levering up into the recession. Realistically, 25 cents a quarter is what is sustainable after the two companies merge. That does not mean that they need to cut right away. Overpayment can sometimes continue for a long time in the case of REITs before the reality is acknowledged.

Source: Quite The Deterioration In Q1-2023

Our base number might have seemed way off base for a company paying 40 cents, but as we had stressed, it was a long run forecast. Companies can always pay a few more dollars than they earn over the short run. Let's look at Q2-2023 results to see how things are shaping up.

Q2-2023

Q2-2023 was the first set of declared results after the Broadmark Capital merger. The net income showed a large gain as Broadmark was bought out at a discount to tangible book value. While that may sound great, keep in mind that RC also issued shares at a big discount to book value for the merger. As a result tangible book value per share did not get any benefit from this discount purchase though one showed up on the income statement.

Net book value of $15.07 per share of common stock as of March 31, 2023.

As of June 30, the company's net book value stood at $14.52.

Source: Company press releases from Q1-2023 and Q2-2023

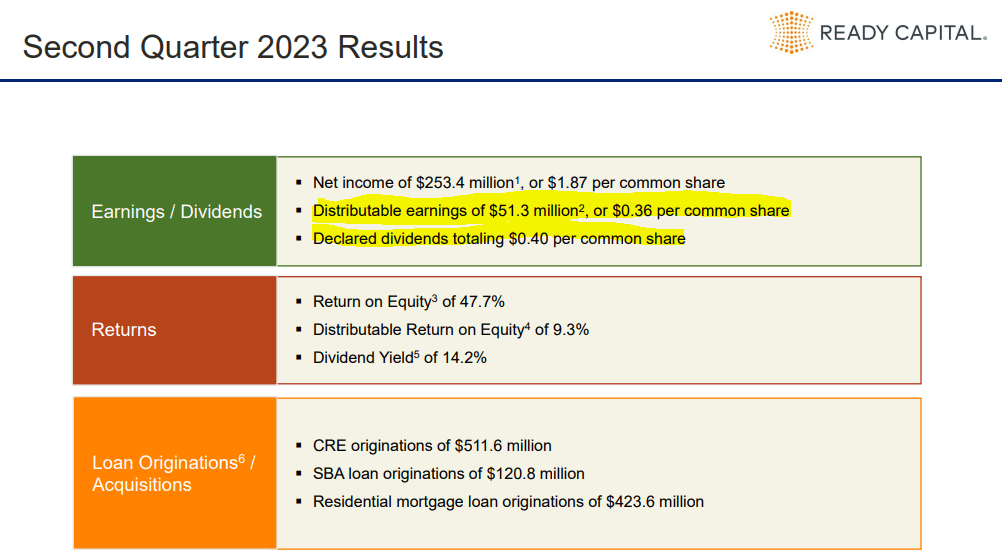

The company reported distributable earnings of $0.36 per share, trailing the dividends once more.

{kind=link}

RC Q2-2023 Presentation

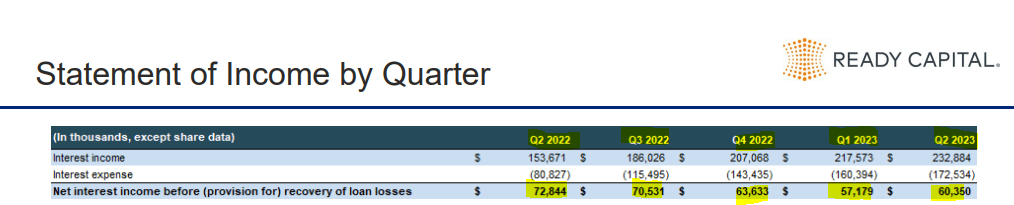

RC's net interest income metric (before provision for losses) has been suffering for the last few quarters and this quarter was no different. Investors might be surprised at that statement considering that the number went up this quarter.

{kind=link}

RC Q2-2023 Presentation

But the reason we are sticking with that verdict is that this was the post-merger quarter. Basic weighted average share count went up by 19%.

RC Q2-2023 Presentation

So net interest income going up by just 5.5% is a problem.

More Pressures Ahead

RC's Q2-2023 had just one month of Broadmark's earnings consolidated into it as the closing date was May 31, 2023. As we have previously shown, Broadmark's return on equity run-rate was far lower than RC's. So as we transition into Q3-2023, we expect distributable earnings to take a bigger hit. This will happen as the weighted average common shares outstanding rises from 131.6 million all the way to 171.6 million.

RC Q2-2023 Presentation

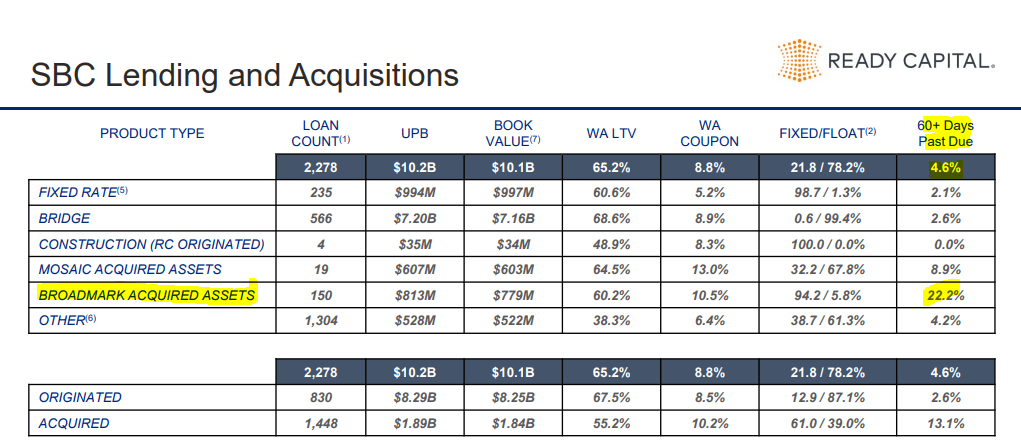

RC's overall book with loans 60 days past due hit a new high as Broadmark was consolidated into the numbers.

{kind=link}

RC Q2-2023 Presentation

One year back (see Q2-2022 numbers below) this was at 2.4%.

RC Q1-2023 Presentation

Bridge loans, which are the largest part of RC's self originated loans, deteriorated this quarter to 2.6% from 2.4%. Credit provisions were higher this quarter, but we think this is just the warm-up.

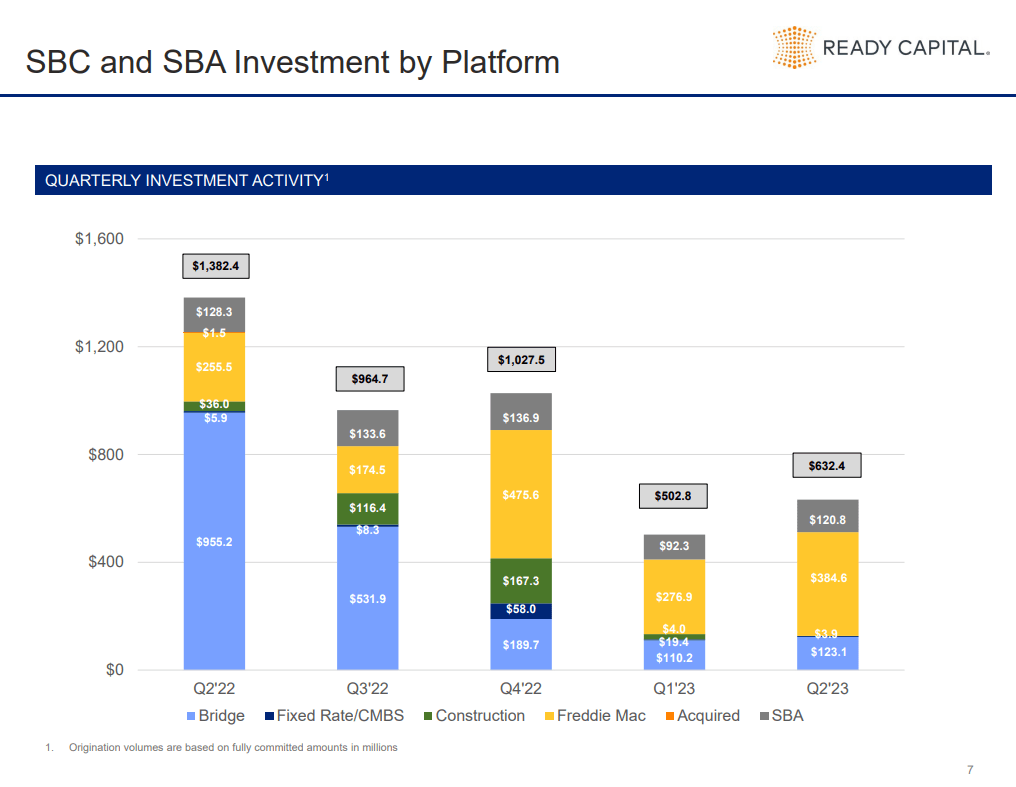

RC is still originating a healthy chunk of new loans but the volume has tapered off compared to 2022.

{kind=link}

RC Q2-2023 Presentation

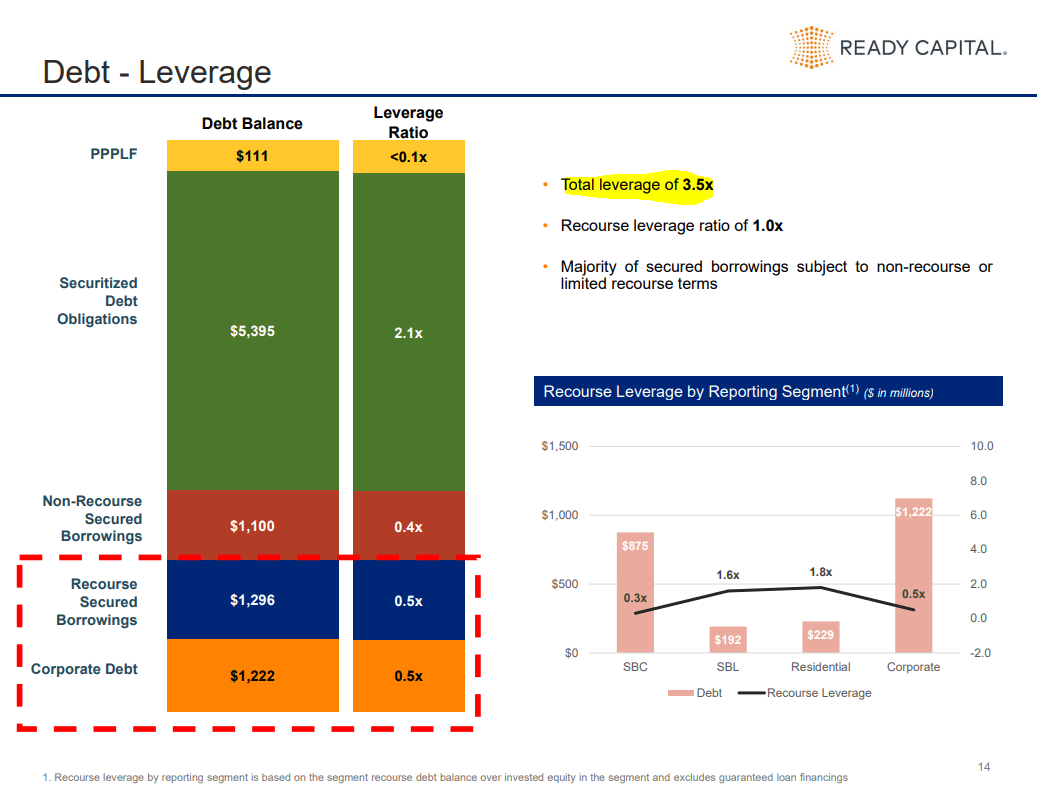

That lower origination combined with the Broadmark acquisition via equity has pushed leverage down to 3.5X.

{kind=link}

RC Q2-2023 Presentation

This is down from 5.1X before the acquisition.

RC Q2-2023 Presentation

Now this is definitely a good thing for the company's viability and credit metrics. Lowering leverage going into what is likely to be a recession, is a great thing. But it will decimate the distribution coverage. RC was struggling in Q1-2023 to produce 40 cents of distributable earnings with a 5.1X leverage. There is no way in Hades they are going to cover it with a 3.5X leverage.

Verdict

It is a matter of time before the distribution is realigned lower, likely to 25 cents a quarter. In the interim, every quarter that they do pay 40 cents will be treated as empirical proof that they won't cut. Every time management says "distribution is important to shareholders", or "plan is to get coverage back up" will be greeted with cheers by the yield chasers. Of course, the math is the math, and won't change based on what management says.

On the positive side, you can also argue that the stock is undervalued based on tangible book value and the reduced dividend. Over the last decade the stock has done better than other mortgage REITs like Annaly Capital Management, Inc. ( NLY ) and AGNC Investment Corp. ( AGNC ) with a solid total return.

So we are not going to put a Sell rating here, but investors should know that yield is likely going lower.

Other Securities

Ready Capital Corporation 7% CN SR NT 2023 ( RCA ) is one of the RC securities that we have suggested in the past and it is part of CIP. That one is due to be redeemed in a week (August 15) for $25.00. So you won't squeeze more than a few pennies out of that.

Ready Capital Corporation 6.50% CUM PFD E ( RC.PE ) is another security we currently own. We really liked this one before and like it even more now as RC has brought leverage levels down. This one currently yields 8.55% on a stripped basis. If we are correct about the 25 cents of common dividend down the line, RC.PE becomes a compelling alternative. Over the last decade, RC's common stock return without dividends reinvested has been 5.19%.

Split History

Astute investors might point out that this was a product of valuation compression, but price to tangible book value is higher today (about 10% higher) than it was a decade back.

So no, it was not due to valuation compression.

We think it will likely do worse than the historic 5.19% total returns over the next 2-3 years. But whatever it does do, we think it will have a hard time matching the total return potential of RC.PE.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Ready Capital: Leverage Vs. Distributions