REG - Realty Income Buys Spirit: More Proof That Value Matters

2023-11-02 11:01:38 ET

Summary

- Realty Income Corporation's acquisition of Spirit Realty Capital, Inc. received a negative market reaction, causing a drop in Realty Income's stock price.

- The acquisition is done in all stock and is immediately accretive to Realty Income's AFFO/share.

- The market's negative reaction may stem from an unrealistic view of Realty Income's portfolio and the dilution of its perceived quality.

After years of being bearish on Realty Income Corporation (O), I feel inclined to step in to defend it after the clobbering it received upon announcing its planned acquisition of Spirit Realty Capital, Inc. (SRC).

If you were an SRC investor, it was a good day, up about 8%. If you were an O investor, it was less fun: O fell 5.7% on the back of an already rough year.

{kind=link}

This was an overall positive announcement. While I think the market is wrong to have reacted so harshly, I think there is a lesson to be learned here: value matters.

In this article, there are 3 topics I want to discuss:

- The merits and demerits of the acquisition

- Source of the market's negative reaction

- Why value has and will continue to matter.

The acquisition

A key aspect of the acquisition is that it is done as an all-stock deal as opposed to cash. Thus, its accretion is determined by the relative valuation of the 2 entities.

Realty Income trades at a higher adjusted funds from operations, or AFFO, multiple than SRC, which makes the deal immediately accretive to AFFO/share. Specifically, O is expected to earn $4.14 per share of AFFO in 2024 while SRC is slated for $3.68.

Each share of SRC is to receive 0.762 shares of O. In AFFO terms, that is $4.14 X 0.762 or $3.15.

Thus, O is paying $3.15 of AFFO in dilutive cost of equity issued in exchange for $3.68 of fresh AFFO/share from SRC.

There are going to be some transaction costs, but that spread is easily wide enough to make it accretive even inclusive of the costs.

That is the raw immediate accretion. Over time, there will also be significant accretion from G&A savings.

Here are the synergies claimed by O in the merger presentation.

{kind=link}

This seems entirely plausible to me. The operations of the companies are quite similar, so a large portion of the redundant functions can be eliminated. While it is unfortunate for those who get laid off, it will result in substantial synergies.

2.5% accretion to AFFO/share is not enormous, but it seems like a great deal to me given the minimal risk involved. The transaction is roughly leverage neutral, and triple net properties are quite seamless to move over relative to more operations-intensive businesses.

In my opinion, there are almost no downsides to the merger. SRC shareholders win due to the pop in share price and O shareholders win from the accretion to AFFO/share.

Source of the market's negative reaction

The market seems to have a problem with the transaction based on the price reaction, and I think it stems from a false notion of O's portfolio as immaculate.

Many have come to view O as untouchable, even using pseudo-religious terms in discussing its "sacrosanct" monthly dividend. This concept of inviolability is largely why Realty Income has consistently traded at a premium multiple relative to peer triple net real estate investment trusts, or REITs.

This is why O traded down on the announcement. Its royal bloodline is being diluted by mixing it with the provincial blood of SRC.

The idea that O is somehow cut from a different cloth is based upon extrapolation of historical data. Yes, O is a dividend aristocrat, but it still is subject to the fundamentals of business just like everyone else. O's portfolio is nearly identical to SRC's portfolio. The risks are the same, and some macroeconomic tail risk could force O to cut its dividend just as it could with SRC or any other company.

I am not in any way suggesting that O's dividend is at risk. It is well supported and after acquiring SRC it will be even better supported due to the accretion to AFFO/share.

Instead, what I am suggesting is that there is no dilution of quality in this transaction.

Continuing with the bloodline analogy, O was already a mutt. It consists of half a dozen other companies that it already absorbed, such as Vereit . Adding SRC to the mix doesn't change that pattern.

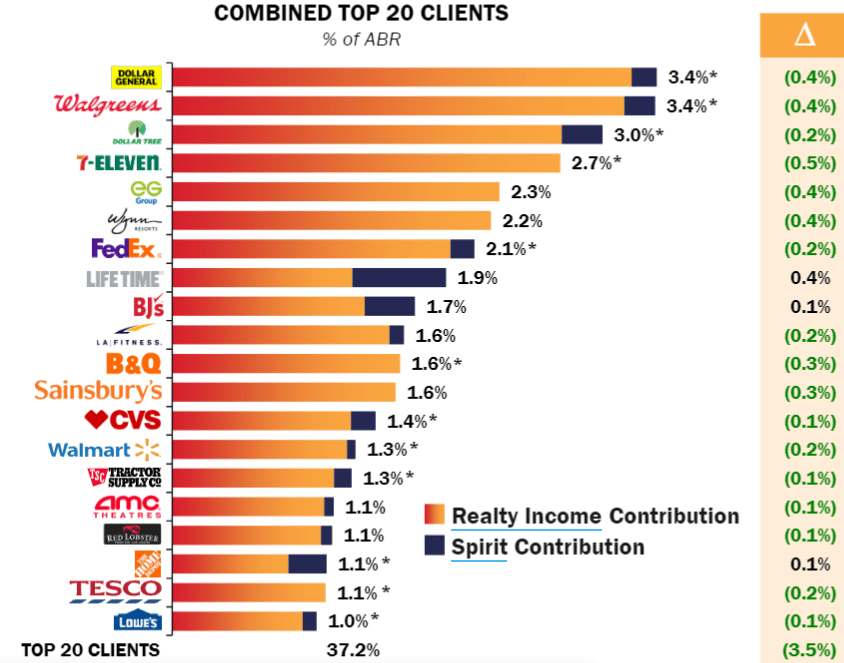

O is a great company with reasonably good assets. SRC is a great company with reasonably good assets. Combining simply saves operating costs and creates immediate accretion. It also has minor diversification benefits in reducing exposure to 18 of the top 20 Realty Income tenant exposures

{kind=link}

These are small numbers, so I consider the diversification benefits mostly negligible.

The point is that O should not have traded down on this announcement, and the dip likely represents a buying opportunity if O is your cup of tea. It also presents yet more evidence that value matters.

Value matters

In the vast majority of M&A transactions, the target benefits more than the buyer. The 2 most common outcomes when a merger is announced are:

- The target is up materially and the buyer is down (that was the case with O/SRC);

- The target is up materially and the buyer is also up, but less.

As investors, we would rather be invested in the target when M&A gets announced rather than invested in the buyer. Assuming no insider information, it may seem impossible to predict M&A. It can be announced on any given day by any company.

There are, however, patterns.

- In August, Kimco (KIM) announced it was buying RPT Realty (RPT)

- Kimco also bought Weingarten on 8/3/21

- In August, Regency Centers (REG) closed on its purchase of UBA

- In October of 2022 Prologis (PLD) closed on its purchase of Duke Realty

- VICI Properties (VICI) closed on MGM Growth Properties in April of 2022

These companies are in different sectors and the reasons for the acquisitions are various. However, each transaction has one thing in common:

The higher AFFO multiple company is the buyer and the lower AFFO multiple company is the target.

M&A is potentially striking again with an announcement last week that Fortress is trying to buy Whitestone REIT (WSR).

Why? Because WSR trades at a ridiculously low AFFO multiple.

A low AFFO multiple is what creates the accretion. A relatively higher multiple company can use its stock as currency to buy a lower AFFO multiple company and it is immediately accretive.

Relative valuation is the number one predictor of which companies will be bought. Owning a slate of undervalued REITs is the best way to become the beneficiary of M&A. Predicting specific transactions can happen, but it is harder than just preparing for the general pattern of M&A. I own Spirit and I own Whitestone. I did not have the precognition to see these specific transactions (or potential transaction in the case of WSR) coming, but I did know these companies were trading far too cheaply and that trading cheaply is the best predictor of M&A.

Some people can take prediction to the next level. A commentor on my 2022 SRC article predicted precisely the O buyout of SRC. I have redacted their name in the screenshot below to protect anonymity, but they can claim credit if they wish.

{kind=link}

Forward arbitrage?

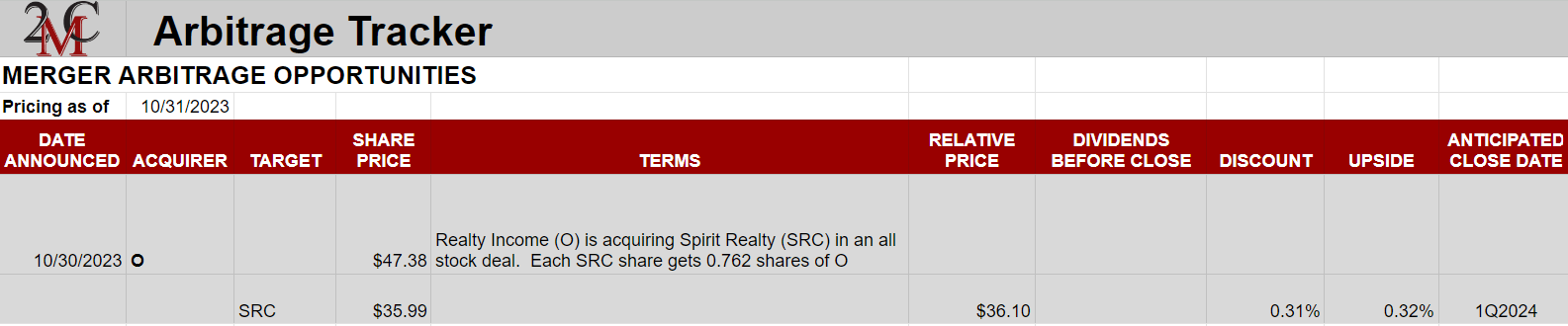

As the transaction is slated to close in 1Q24, there is some potential to trade price spreads in the interim period. Given the stated ratio of 0.762 shares of O for each share of SRC, one can calculate the spread between the two legs of the merger.

We have added this merger to the Portfolio Income Solutions Arbitrage Tracker Spreadsheet which tracks the spreads of ongoing arbitrages.

{kind=link}

Presently, the spread is quite small, with the SRC leg being 0.31% cheaper than O.

That is probably too small of a spread to make an arbitrage worth it, but it can still be worth holding SRC for the dividends and as a play on the combined company which is trading at an attractive valuation.

Wrapping it up

This is one of the cleanest and most straightforward buyouts I have seen in a while. It is a win for both sets of shareholders.

Valuation matters. In addition to the higher cashflows that come with a low AFFO multiple, investors get an increased chance of benefiting from being the target of M&A.

For further details see:

Realty Income Buys Spirit: More Proof That Value Matters