RBGPF - Reckitt Benckiser: A Pick To Avoid The Banking Turmoil

2023-03-21 06:29:23 ET

Summary

- Reckitt Benckiser could report great results for fiscal 2022 with the top and bottom lines improving and all three segments contributing to growth.

- While management is a little more cautious for 2023 (only low single-digit growth), the long-term targets see growth rates in the mid-to-high single digits.

- For the first time since 2019, the dividend was increased again, and the stock can be seen undervalued by about 20%.

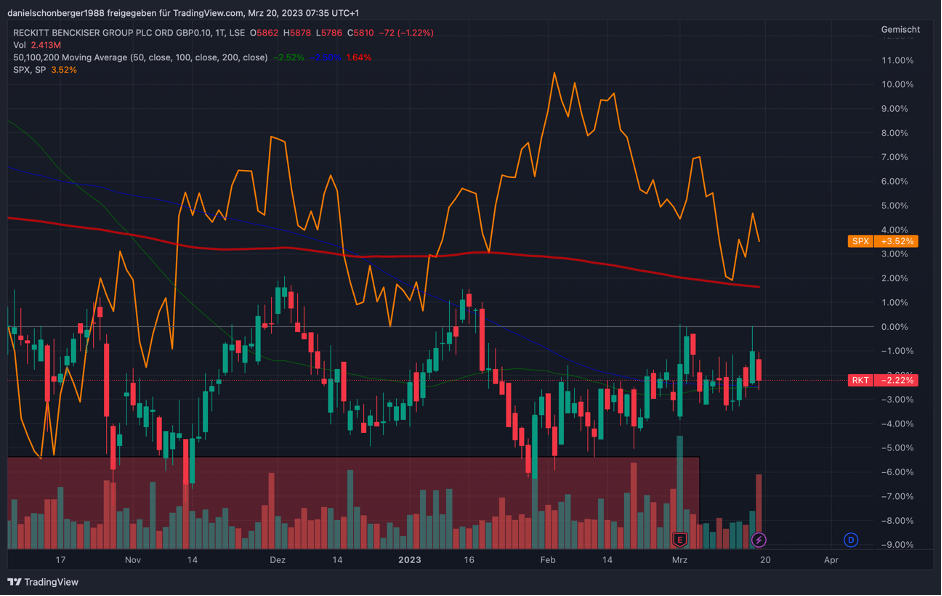

In my last article about Reckitt Benckiser ( OTCPK:RBGPF ), I stated that the company is on the right path. The article was published on October 5, 2022, and while the stock increased about 6% since the article was published, the performance in Great British Pound was different (and this is the currency Reckitt Benckiser is mostly traded in). While the S&P 500 could gain about 3% during that time, Reckitt Benckiser (in Great British Pound) lost about 2% in value.

{kind=link}

In times as we are in right now (higher volatility, bear market, liquidity probably drying up) it is more important than ever to make the right decisions. It is important to be neither greedy nor fearful. And Reckitt Benckiser is a "Sleep-Well-At-Night" stock and therefore a good pick for the next few years. It is a company selling mostly everyday items and can therefore be seen as recession resilient. And as the stock is also not trading for too high valuation multiples, we have some form of downside protection.

Results 2022

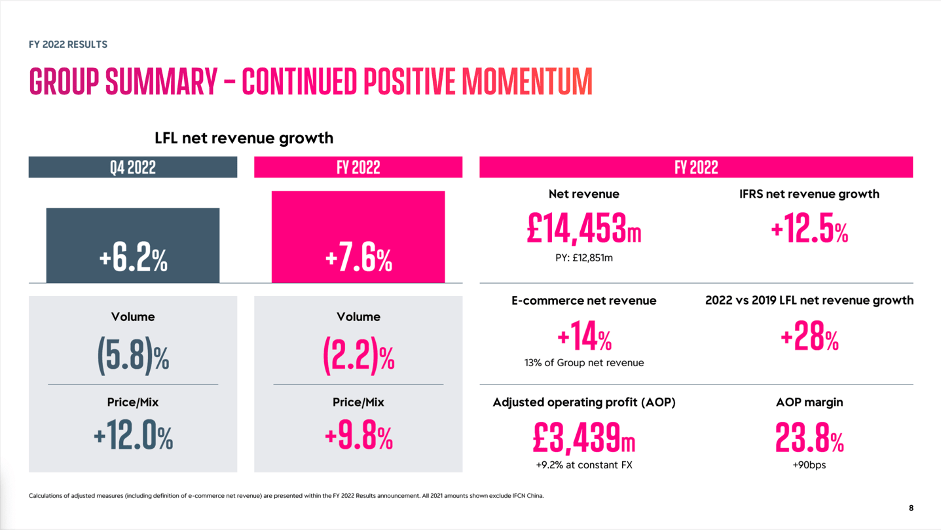

After mediocre results in the last few years, Reckitt Benckiser could report solid results for fiscal 2022 with top and bottom line increasing at a solid pace. Net revenue increased from GBP 13,234 million in fiscal 2021 to GBP 14,453 million in fiscal 2022 - resulting in 9.2% year-over-year growth. Like-for-like revenue growth was 7.6% in fiscal 2022. And while the company had to report an operating loss of GBP 804 million in fiscal 2021, it could report an operating income of GBP 3,249 million in fiscal 2022. And instead of a diluted loss per share of 4.5 pence in fiscal 2021, Reckitt Benckiser reported earnings per share of 324.7 pence in fiscal 2022.

Reckitt Benckiser Q4/22 Presentation

{kind=link}

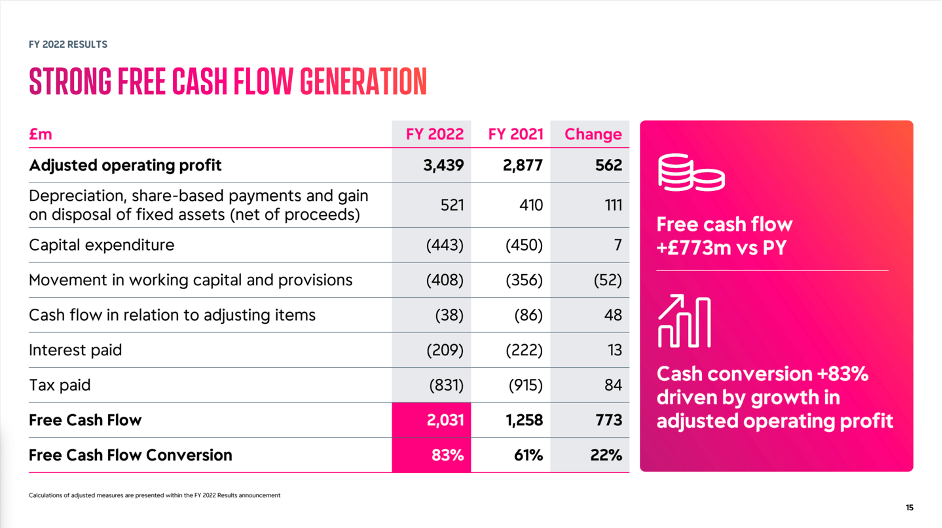

Adjusted earnings per share could even increase 18.4% compared to fiscal 2021 and was 341.7 pence in fiscal 2022. And free cash flow also improved from GBP 1,258 million in fiscal 2021 to GBP 2,031 million in fiscal 2022 - an increase of 61.4% YoY. Cash conversion also improved from only 61% in fiscal 2021 to 83% in fiscal 2022 and was therefore more or less in line with cash conversion in previous years.

Reckitt Benckiser Q4/22 Presentation

{kind=link}

And regarding cash flow, management is optimistic the situation normalized again and cash conversion as well as free cash flow will improve in the years to come. CFO Jeffrey Carr stated during the last earnings call :

Now COVID has caused some volatility in our cash flows. But I now feel we have returned to a more normalized position with working capital at a sustainable level at around minus 11% of net revenue, and we're confident of delivering strong future cash flows and high cash conversion in the coming years.

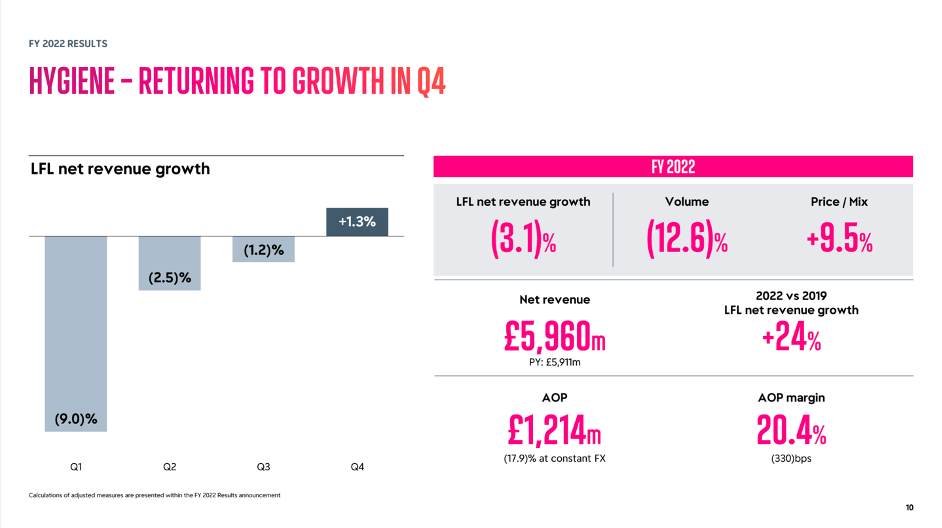

And not only could Reckitt Benckiser report strong growth for the top and bottom line, all three segments contributed to growth in fiscal 2022. Hygiene was probably the worst performing segment in 2022 with revenue increasing only 0.8% to GBP 5,960 million, but the segment is still responsible for 41% of total revenue. And while price and mix contributed 9.5% to growth in fiscal 2022, volume declined 12.6% and resulted in a like-for-like revenue decline of 3.1%.

Reckitt Benckiser Q4/22 Presentation

{kind=link}

And especially Lysol sales declined 25% while the rest of the hygiene portfolio grew 5.1%. The declining sales are also not surprising considering the strong hygiene sales during COVID-19 and we are just seeing a regression to the mean. But when looking at the quarterly numbers, we see improving results and in the fourth quarter, like-for-like revenue could grow 1.3% again.

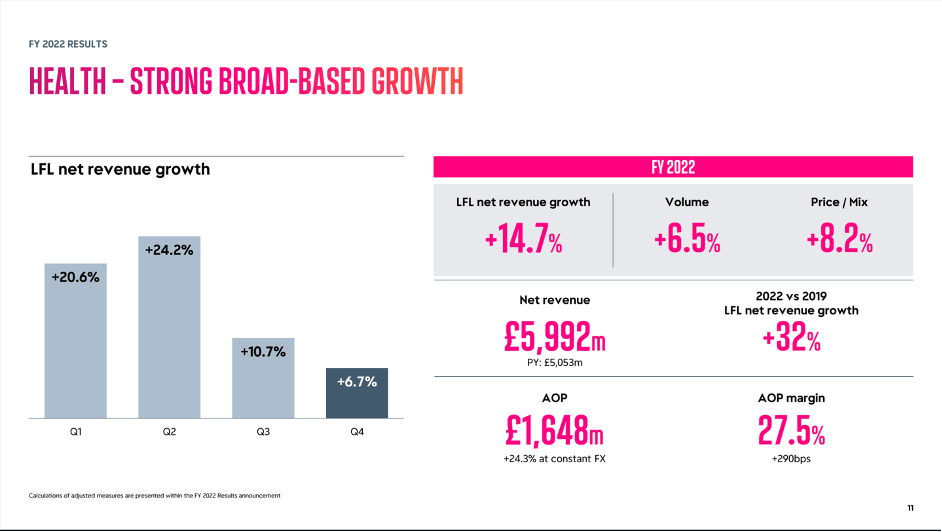

In comparison, the Health segment could report impressive results. Revenue for the segment increased 18.6% YoY to GBP 5,992 million and volume (6.5% growth) as well as price/mix (8.2% growth) contributed to a like-for-like growth of 14.7%.

Reckitt Benckiser Q4/22 Presentation

{kind=link}

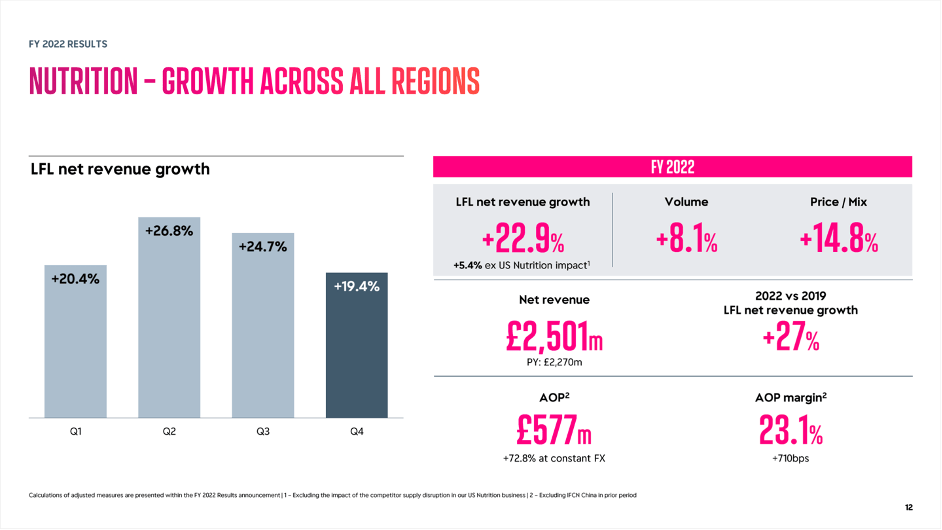

Finally, the Nutrition segment generated GBP 2,501 million in revenue, which resulted in 10.2% YoY growth. However, like-for-like revenue grew 22.9% with volume contributing 8.1% and price/mix contributing 14.8%. And despite all excitement about the great numbers, we must point out that the high double-digit growth rates were mostly the resulted impact of the competitor supply chain disruption in the U.S. nutrition business. When excluding this impact, like-for-like growth was 5.4%, which is still a solid number, but not so impressive.

Reckitt Benckiser Q4/22 Presentation

{kind=link}

During the earnings call, management also commented on the situation:

Now separately, let me just refer to the situation in the U.S. related to the infant formula market. This had a significant impact on top line growth and on our adjusted operating profit margins. Breaking this out, we believe the benefit on like-for-like net revenue growth was approximately 2.5% in the year, and the impact on adjusted operating profit margins in 2022 was approximately 80 basis points.

Continuing On The Path Of Growth?

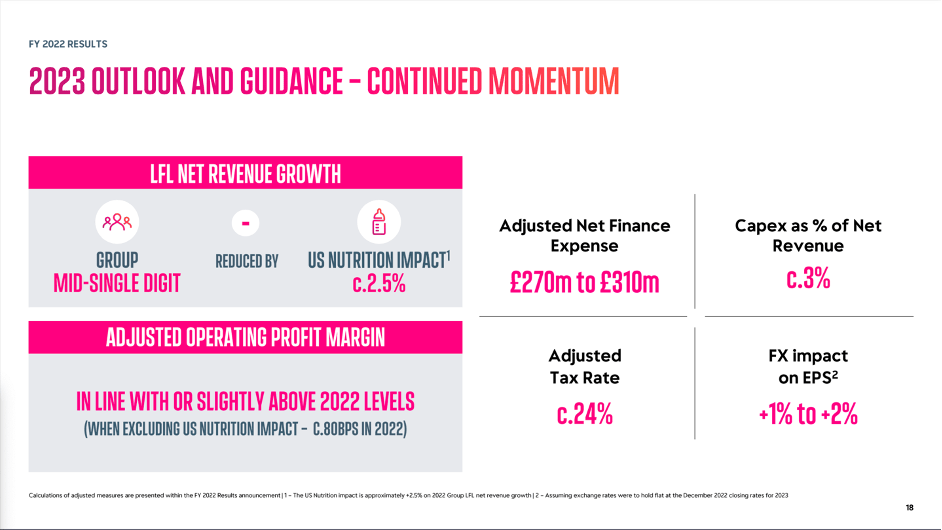

And while a great performance in fiscal 2022 is certainly nice to have, more important is the question if Reckitt Benckiser can continue its growth in the years to come. For fiscal 2023, management is a little more cautious, but it is still expecting like-for-like net revenue growth in the mid-single digits for the group, but only when excluding the negative impact by the U.S. nutrition business.

Reckitt Benckiser Q4/22 Presentation

{kind=link}

Adjusted operating profit margin is expected to be in line with or slightly above 2022 levels and therefore top line might also grow in the low single digits in fiscal 2023. For 2023, Reckitt Benckiser is also expecting a savings target of GBP 500 million as part of its mission to improve productivity.

Reckitt Benckiser Q4/22 Presentation

{kind=link}

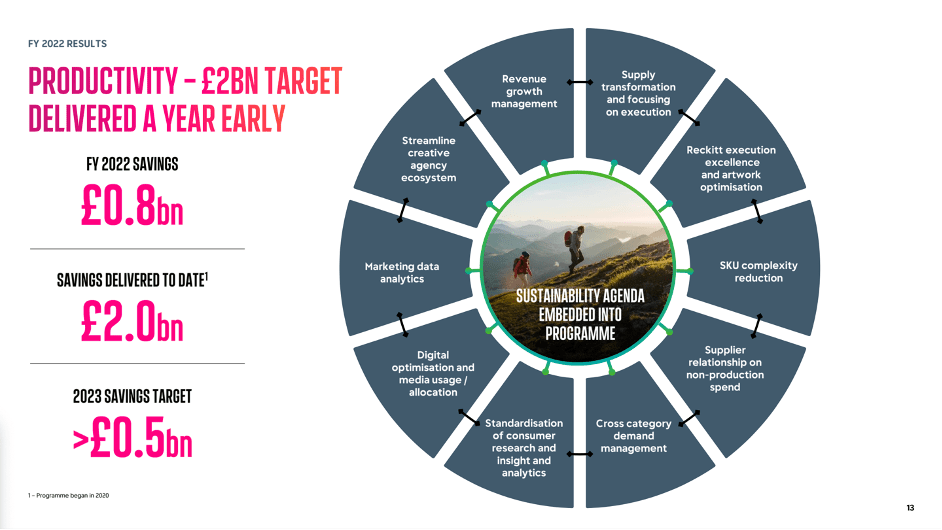

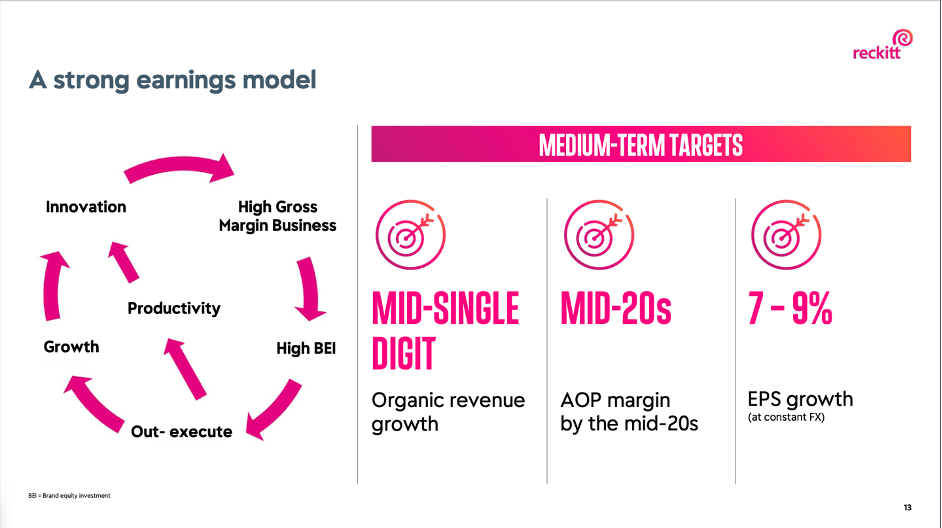

To date, the company delivered savings of GBP 2.0 billion and delivered this target a year earlier than previously expected. And as mentioned in our last article, improving productivity is only one step in Reckitt Benckiser's earnings model and overall, the company has a medium-term target of 7% to 9% growth in the years to come.

Reckitt Benckiser CAGNY 2022 Presentation

{kind=link}

When looking at the last few years, growth targets in the high single digits might seem overly optimistic and in the last ten years, Reckitt Benckiser could grow its earnings per share only with a CAGR of 2.61%. However, when looking at the growth rates in the last four decades (or since 1983, the first year I have data for), Reckitt Benckiser could grow its earnings per share with a CAGR of 8.21% and since 2002, the company could grow its earnings per share even with a CAGR of 9.02%.

| EPS CAGR | Since 1983 | Since 2002 | Since 2012 |

|---|---|---|---|

| 8.21% | |||

| 9.02% | |||

| 2.61% |

And when looking at the performance of Reckitt Benckiser during recessions in the last four decades, the company always performed well. In 2021, revenue declined slightly (which could be seen as an effect of the COVID-19 recession) and in 1992 revenue also declined slightly (which could be seen as a result of the early 1990s recession). However, during the Great Financial Crisis, the years following the Dotcom bubble and the early 1980s Reckitt Benckiser could even improve its top line in years when other companies struggled.

Dividend

And after a few years of holding the dividend flat, Reckitt Benckiser increased its dividend the first time since 2019. While the interim dividend for fiscal 2022 was the same as in the previous year (73 pence), the final dividend increased from 101.6 pence in for fiscal 2021 to 110.3 pence for fiscal 2022. This resulted in a full year dividend of 183.3 pence and an increase of 5% year-over-year. The dividend will be paid on 24 May 2023 and Reckitt Benckiser will once again make the offer to replace the cash dividend by getting paid in shares.

Management mentioned the solid balance sheet as main reason for being able to increase the dividend right now:

After a few years of holding the dividend flat, we're now proposing to increase our total dividend by 5% this year with the intention to sustainably grow dividends in future years, subject to any significant internal or external factors. And this reflects the strength of our balance sheet and our confidence in the cash-generating potential of our business as we look to the future.

And with a payout ratio of 56% the dividend can be seen as safe and under the premise of an increasing EPS, Reckitt Benckiser should also be able to increase the dividend in the years to come.

Intrinsic Value Calculation

And it is not only important to invest in great businesses - at best with a wide economic moat around the business and recession-resilient - but also to buy stocks at a reasonable price. As we have already experienced in 2022 (and in parts also in 2021), stocks trading for astronomically high valuation multiples get punished hard. Reckitt Benckiser is trading for 18 times earnings right now (when taking 2022 EPS) and when using the adjusted numbers, the stock is trading for 17 times earnings. Additionally, the stock is trading for 20.5 times free cash flow. These metrics are no screaming bargains, but Reckitt Benckiser is also not expensive either.

However, these valuation multiples won't give us a clear answer if Reckitt Benckiser can be purchased or not. To achieve this goal, we can use a discount cash flow calculation to determine an intrinsic value for the stock. As basis we can take the free cash flow of GBP 2,031 million from fiscal 2022 and assume the free cash flow will be similar in 2023. For the next ten years we are optimistic and assume 7% growth (the lower end of the company's own mid-term targets) followed by 6% growth till perpetuity (as we can argue Reckitt Benckiser has a wide economic moat around its business). When calculating with these assumptions (and a 10% discount rate as well as 717.5 million outstanding shares) we get an intrinsic value of GBP 75.96 , and the stock can be called undervalued.

Conclusion

Although we should still be a little cautious if we can expect consistent mid-to-high single digit growth rates for Reckitt Benckiser in the years to come, the stock looks undervalued and is trading for a 20% discount. In my opinion, Reckitt Benckiser is one of the stocks that can be bought right now as we are getting a business that is undervalued as well as recession-resilient.

For further details see:

Reckitt Benckiser: A Pick To Avoid The Banking Turmoil