RBGPF - Reckitt Benckiser: Not A Bargain Despite Its Potential

2023-11-06 04:52:11 ET

Summary

- Reckitt Benckiser has struggled to consistently exploit its portfolio of premium brands and return to its historical growth trajectory.

- The company's third-quarter performance was impacted by foreign exchange headwinds, but this does not necessarily indicate underlying weakness.

- The lack of consistency in Reckitt's earnings growth strategy has affected its fair valuation, although it has the potential for strong business performance.

U.K.-based consumer goods multinational Reckitt Benckiser ( RBGPF ) has had both challenges and opportunities in the past several years and I am not sure it has excelled in managing them. I remain a fan of its portfolio of premium brands and broad market reach. However, compared to some peers it has struggled to exploit them consistently and, even after huge writedowns, continues to struggle to return to its historical growth trajectory following its disastrous, costly 2017 infant nutrition acquisition (covered in many previous pieces on SA).

I last covered the name in July 2022 with my "hold" note Reckitt Benckiser: On The Road To Recovery . Since then, the shares have lost 16% of their value.

Business Performance is Mixed

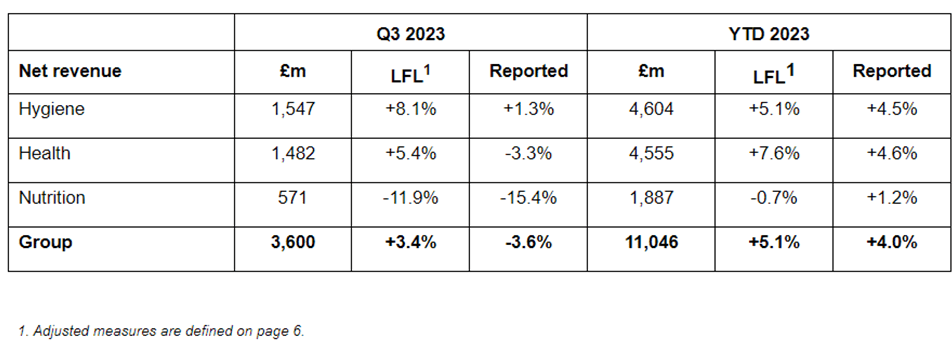

Last month the company released its third quarter trading update .

Year-to-date reported revenues have grown across the business, although on a like-for-like basis, the long-term problem child of nutrition continued to show some weakness. But the third quarter showed a marked downturn in performance compared to the year-to-date figures. A key reason for the relatively weak third quarter performance, at least on a like-for-like basis, was foreign exchange headwinds. As Reckitt reports in pounds but derives most income overseas, that makes sense and does not necessarily suggest underlying weakness in the business performance.

{kind=link}

The company also started a £1bn share buyback programme alongside the announcement and announced what it called a strategic update .

I am not sure I would use that term. The strategic update revolved around the buyback (which I don't see as a strategic move per se other than in financial terms) and then referenced various somewhat self-congratulatory tropes. The interesting points from an investor's perspective seem to be a goal to deliver sustainable mid-single digit like-for-like (LFL) net revenue growth over the medium term (with little detail on how), investing in product superiority (whatever that means - it's not clear to me) and cost-cutting.

In fact, I took the strategy update as a sign of weakness. If it was labelled as an announcement of a share buyback, fine. But what was termed strategy largely consisted of setting out a variety of objectives (with or without accompanying measures) while not giving any clear strategic plan of how to achieve them. That makes me wonder how well current management really understands strategic thinking and whether they are able to form the right set of strategies to hit those targets.

Outlook Seems Solid But Could do with Clearer Targets

At the full-year level, the company expects to deliver adjusted operating margins slightly above previous year (when excluding the benefit of circa 80bps in 2022 related to US Nutrition).

In the medium term, the guidance is for adjusted operating profit to grow ahead of net revenue growth, achieving mid-20s margins by the mid-2020s. The first half already saw adjusted operating margins of 23.8%, so I do not see that outlook as a big change. Mid-20s could mean 27% not 23.8%, sure, but it might mean 23.8% and adjusted operating margin is not necessarily a good indicator of what will actually be delivered when it comes to reported post-tax profit.

So while the outlook seems fine to me, it does not in itself make the investment case more attractive. Again, I'd like more specific details and concrete targets.

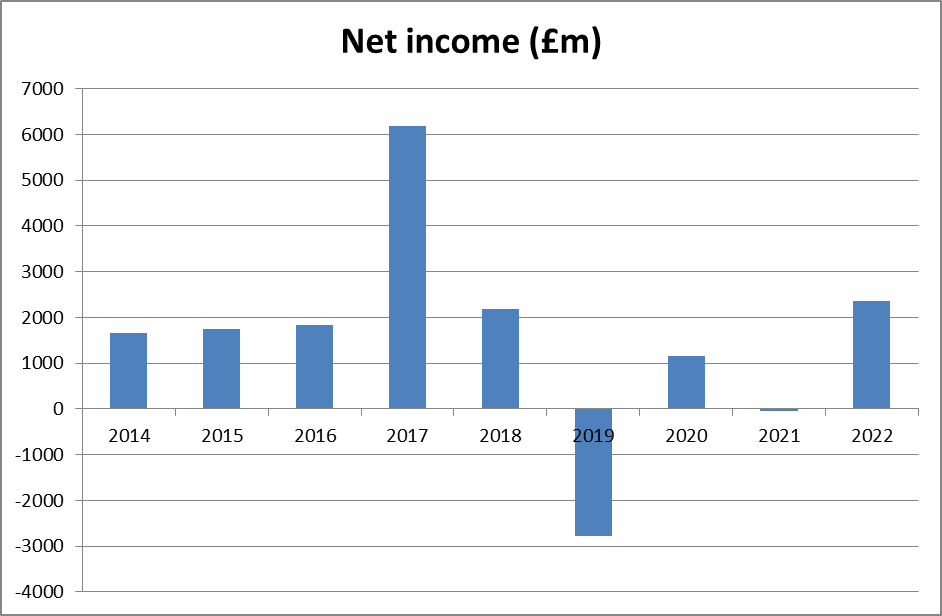

In the first half, net income fell 7% year-on-year. Last year's post-tax profit of £2.3bn was the highest since before the pandemic. But, for what ought to be a relatively stable company (and one that benefitted from soaring demand in the pandemic, thanks to its portfolio of hygiene brands like "Lysol").

Looking back at the past few years, Reckitt has hardly been delivering the sort of consistency of income one would hope for from a large consumer goods firm. A lot of this might be put down to its ill-fated nutrition strategy and the impact of the pandemic. Even allowing for that, though (both things that to some extent would have responded to the company's approach and could have worked in the business's favour not against it), the inconsistency is unsettling. However, if one ignores 2017 and 2019-21 in the chart below, there is at least a fairly clear trendline. For any investor, of course, the question of simply ignoring years that don't fit a trendline could be a costly one. But there is the potential justification here that 2017 was different due to organisational changes and 2019-21 due to the pandemic, but that future performance ought to be more consistent.

Chart compiled by author using data from company announcements

{kind=link}

Then again, one could have said that in 2016 and look what has happened since then.

The lack of consistency eats into the fair valuation for the company, in my opinion. So far, current management has not reassured me that it has a clear, well-grounded, deliverable strategy for earnings growth at the adjusted operating, let alone what I consider to be the far more important reported level.

I feel Reckitt has the right assets for a strong business and it has performed well often in the past. So, in broad terms, I remain upbeat about its short-, medium- and long-term business performance. However, greater clarity on expectations could help support the shares in my opinion.

Valuing Reckitt shares

Currently the shares trade on a P/E ratio of 16. I do not think that is cheap but see it as reasonable for a company with the assets and potential of Reckitt, although I would be more comfortable if there was a clear glidepath to more consistent earnings performance than we have seen in recent years. Accordingly, I continue to rate the shares as a hold.

The P/E ratio may look somewhat cheap by U.S. standards (Procter & Gamble ( PG ) trades on a ratio of 24) but U.K. rival Unilever ( UL ) trades on a P/E ratio of 14 and, while it has its own problems in terms of strategic choices, I think has been performing more consistently in recent years.

For further details see:

Reckitt Benckiser: Not A Bargain Despite Its Potential