RBGPF - Reckitt Benckiser: Potential For Strong Free Cash Flow

2023-07-06 02:41:56 ET

Summary

- Reckitt Benckiser Group is a global manufacturer and seller of health, hygiene, and nutrition products.

- Reckitt has benefited well from the pandemic, but is fundamentally attractive due to the brands it owns.

- Margins are above the industry average, allowing Reckitt to deleverage and fund distributions.

- Looking ahead, we think margins will slightly contract, but growth should remain healthy.

- Reckitt's valuation suggests an upside in the region of 12-14%.

Investment thesis

With economic conditions uncertain and investors seeing markets react negatively, many are searching for defensive picks for their portfolio as an all-weather pick. Our view is that Reckitt has the potential to be this choice. To assess this, we will conduct a deep dive into Reckitt's financials to assess the sustainability of its commercial standing, as well as FCF generation.

Company description

Reckitt Benckiser Group ( OTCPK:RBGPF / OTCPK:RBGLY ) is a global manufacturer and seller of health, hygiene, and nutrition products. Their products include treatments for acne, heartburn, and coughs, as well as germ protection, pest control, and hygiene products for homes. They sell their products under well-known brands like Dettol, Gaviscon, Lysol, and Woolite.

Share price

As a leading company in the consumer staples industry, Reckitt is highly mature and not expected to see share price appreciation at a significant level. Across the last decade, the company has seen its share price remain relatively flat, trading between $60 and $100. Things were looking positive until a disastrous transaction to buy Mead Johnson , which resulted in a £10BN write off across several years. The pandemic contributed to improving fortunes as the company is a leader in cleaning and health products, with consumers/businesses stocking up on these products out of fear of Covid.

Financial analysis

{kind=link}

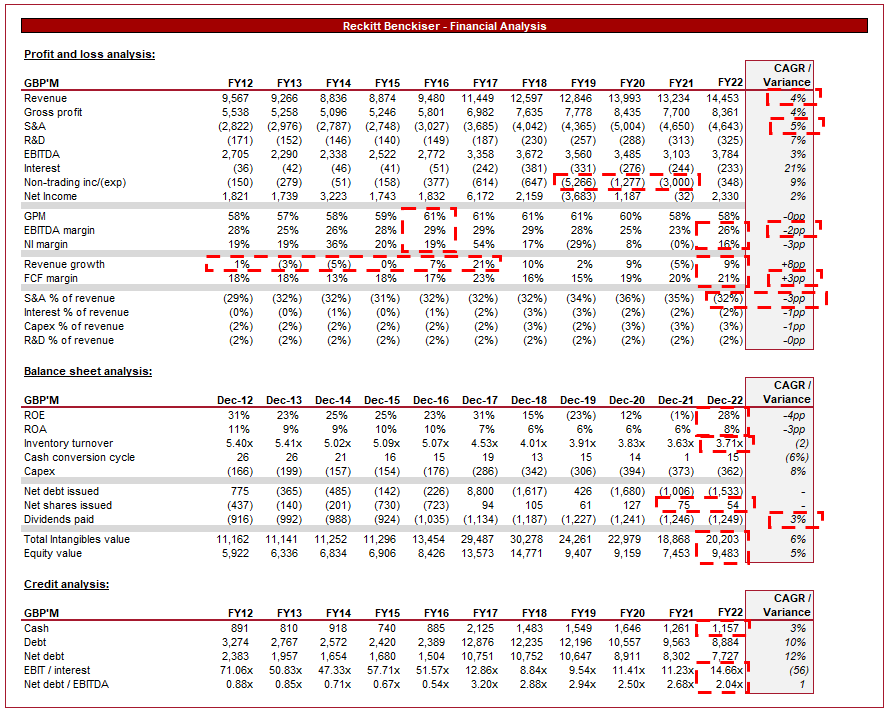

Reckitt Benckiser Financial performance (Capital IQ)

Presented above is Reckitt Benckiser's financial performance for the last decade. Our view is that the company is fundamentally attractive as a reliable defensive pick.

Revenue

Revenue has grown at a CAGR of 4%, driven in large part by both acquisitions and Covid-19. As a mature consumer goods business, the company does not have the scope to organically grow at a rate above population growth / inflation, with value stemming from the consistency and reliability of revenue. For this reason, the key to long-term success is the quality of the brands, as they will allow the business to grow in perpetuity.

Our view is that Reckitt owns a host of fantastic brands which have the scope to consistently grow forever. Just to name a few, we see superior value with Durex (Sex-related products), Gaviscon (Heartburn), Clearasil (Skincare), Finish/Lysol (Cleaning), Veet (Female body hair), Nurophen (Painkiller), Air Wick (Home fragrance), and Enfamil/Nutramigen (Infant nutrition). All these brands have several value drivers in common. Firstly, they are all products that the majority of consumers will need at many points in their lives, if not consistently. Growth in the world's population and the elimination of poverty is a natural tailwind for the majority of businesses, but their benefits are not equal. FMCGs companies gain the most due to their products being "every day" staples, thus are applicable to everybody. Secondly, these brands are leaders in their industry, allowing Reckitt to enjoy a large chunk of the sales. What differentiates Reckitt from other FMCGs businesses is its range of brands, with the company not overly exposed to cyclical trends.

The COVID-19 pandemic has significantly increased the demand for health and hygiene products such as disinfectants, sanitizers, and other cleaning products. This was especially the case during lockdowns due to the fear around the virus but has continued to a lesser extent. Many businesses and consumers still maintain their hygiene habits which were borne out of the pandemic. Reckitt is a leading business in this segment, allowing the company to capitalize on this demand, especially in the consumer segment.

Consumers are increasingly focused on health and wellness, which looks to be beyond a trend and more likely a structure change in consumers' habits. This is driven by a greater understanding of diets and what is good/bad for humans, as well as healthy living marketing supported by Governments. Reckitt has strong exposure to this segment through nutrition and health products. This should act as a natural tailwind in the coming years.

From a financial perspective, the most recent revenue driver has been pricing action. We are currently experiencing inflationary pressures due to many factors including supply-chain issues, which have led to rising costs for businesses. Reckitt is not immune to this and as an FMCGs company, is arguably overexposed given its global supply chain. For most businesses, the demand-side impact of declining discretionary income is an issue, as consumers defer spending. This is not the case for a FMCG business due to the relative inelasticity of their products. Consumers who suffer from heartburn are not going to stop buying Gaviscon, just likely people will not stop having sex. For this reason, judging FMCGs companies is based on the degree to which they can increase prices relative to volume declining. Our view is that Reckitt performs amazingly in this regard, seeing a 2.2% decline due to volume but gaining 10% due to price.

Reckitt pricing development (Reckitt Benckiser)

We have covered many FMCGs businesses including Clorox , KMB , Newell , Sysco , Hershey , Mondelez , and Unilever (all linked) and it is fair to say this degree of inelasticity is rare. This has allowed revenue growth to not miss a beat. The most recent quarter has seen a greater decline in volume than the year as a whole, suggesting: 1) Reckitt is reaching its limit 2) Demand-side issues are taking hold 3) Private labels are becoming attractive.

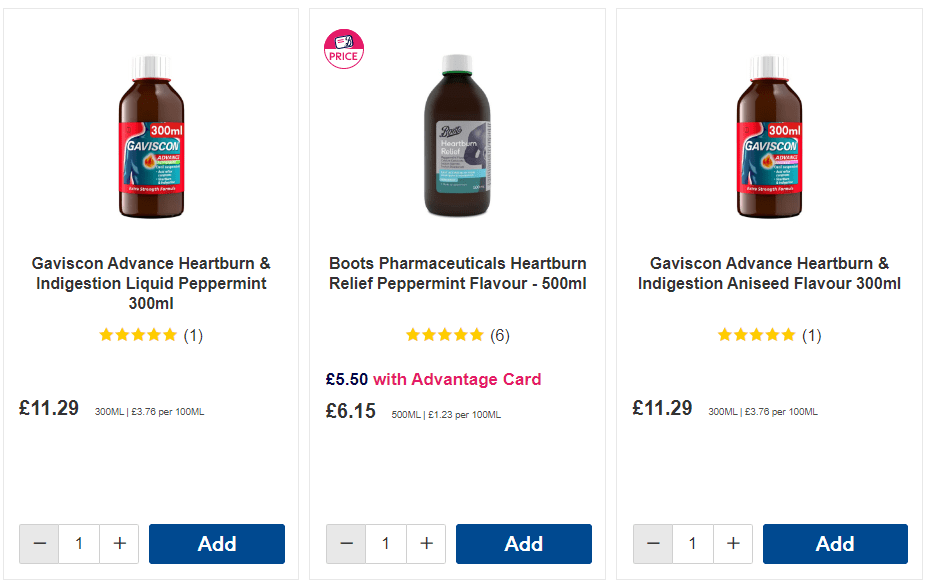

Private labels represent a key risk to Reckitt. These are "unbranded" products that are sold at a lower price than traditional branded products, enticing the value-conscious consumer. What we have observed in the market is that these private-label products have been less trigger-happy with price increases, resulting in a larger delta between the "branded" products. This is likely a strategy to gain market share, as they know the FMCGs businesses must protect margins whereas the private label owners are usually retailers and so less sensitive to specific product pricing. See below an example of this, where Gaviscon is now more than 3x as expensive per 100ml as a private label alternative.

{kind=link}

Boots product v. Gaviscon (Boots)

Overall, we are bullish on the company's revenue profile, seeing only commercial positives in the coming years. Our only concern is with private-label competition, which is a risk we cannot see the impact of until conditions normalize.

Costs

As we have mentioned, Reckitt has very strong pricing power, which allows the business to achieve an impressive 58% GPM. GPM was improving, however, competition has contributed to a subsequent reversal of this. Management is seeking to improve margins but this looks to be a difficult task.

Operational cost controls have been poor in our view, growing disproportionately against revenue. This is due in part to poor business integration, which Management has looked to right in recent periods. S&A expenses remain at 32% of revenue, which is a fairly large amount. Our target would be c.30%.

Productivity gains (Reckitt Benckiser)

What investors will observe is a lot of non-trading "noise" in the accounts, which primarily relates to the incremental write-off of the Mead business. To date, Reckitt has written off something to the tune of £10BN , having only paid £12BN. This is a loss of monumental proportions and a leading factor as to why the company's share price failed to improve. Management has spent a considerable amount of time attempting to sort this mess out and should now be in a position to kick on. The key here is that this not repeated, as Unilever's Management has shown recently that transactions like this are still being contemplated (Unilever attempted to buy GSK's Consumer division for a ROIC of 5%). To quote Terry Smith , "since Kraft bought Heinz in July 2015, its shares are down 48%; since ABI bought SAB Miller in October 2016 its shares are down 49%; since Reckitt bought Mead Johnson in June 2017 its shares are down 21%; and since Danone bought WhiteWave in April 2017, its shares are down 10%. Bloomberg refers to ‘the curse of the consumer deal’" (Quote from 2022). The good news is that the company does not look to be materially damaged by this transaction.

Margins

The net of these factors is an EBITDA-M of 26% and an FCF-M of 16%. This looks to be a sustainable level for the business, although there is scope for improvement. At these levels, consistent buybacks and dividends are possible.

BS

Moving onto the balance sheet, Reckitt's operational decline is observed in its ROE and inventory turnover, which have both fallen compared to their respective highs. Levels still remain at attractive points but show Management still has scope for improvement.

As a cash-generative business, dividend payments have been sustainable, growing at a rate of 3%. Reckitt currently has a yield of 3%, which in our view is good alongside other distributions.

Buybacks were also a mainstay until the transactions bloated the balance sheet. With Management rightly focusing on deleveraging and improving the top-line performance, these buybacks were stopped. Our view is that the company is slowly reaching a stage where buybacks can return.

Unlike many of its peers, Reckitt is financed conservatively, spending a large chunk of its history with a ND/EBITDA ratio of <1x. Our view is that a 3x level is the maximum a company should trade at, with Reckitt avoiding this level like the plague. It has aggressively deleveraged since the transaction, falling to 2x. We think this level is already quite good but Management will likely continue based on their track record and communications.

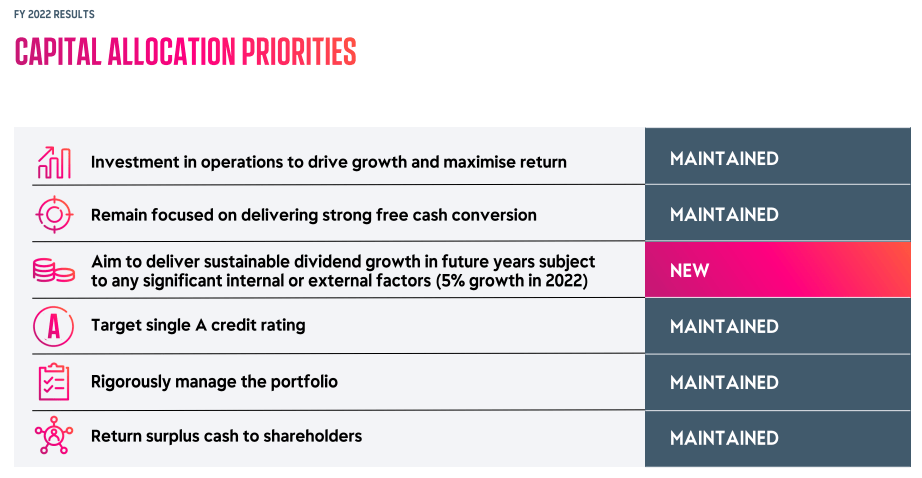

{kind=link}

Capital allocation plans (Reckitt Benckiser)

Outlook

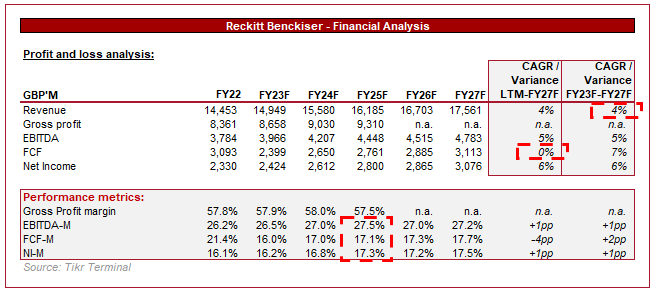

{kind=link}

Outlook (Capital IQ)

Presented above is Wall Street's consensus view on the company's next 5 years.

Revenue is expected to grow at what we believe to be an impressive 4%, exceeding the target inflation level of 2-3%. This will be driven by pricing actions, as well as commercial improvement.

Analysts are also forecasting an improvement in margins, with Reckitt likely seeing some continued operational gains. This is still not to the level required to return to its historical peak but likely reflects how difficult of a task that would be.

FCF is expected to trend down, which is unsurprising given the elevated levels we have seen in the last 2 years. c.17% is still a highly attractive level in our view.

Peer comparison

{kind=link}

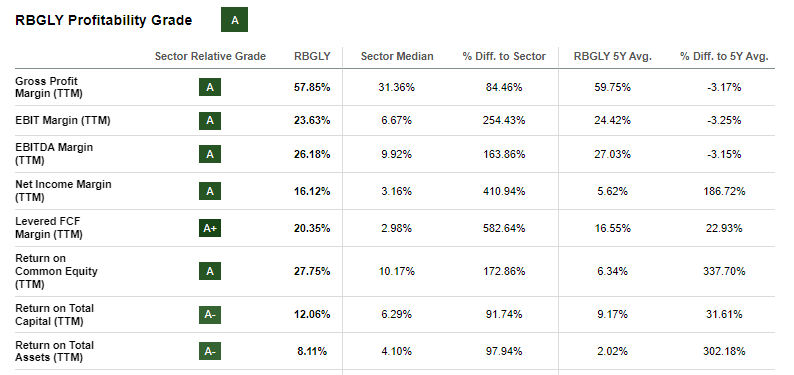

Profitability (Seeking Alpha)

Presented above is a comparison of Reckitt to its household FMCGs peers, with Seeking Alpha attributing a rating based on relative performance.

Reckitt performs extremely well, driven by what is market-leading profitability. The key metrics we care about are EBITDA-M and FCF-M, both of which Reckitt is substantially higher in. Importantly, even as margins contract, Reckitt will remain clearly ahead.

{kind=link}

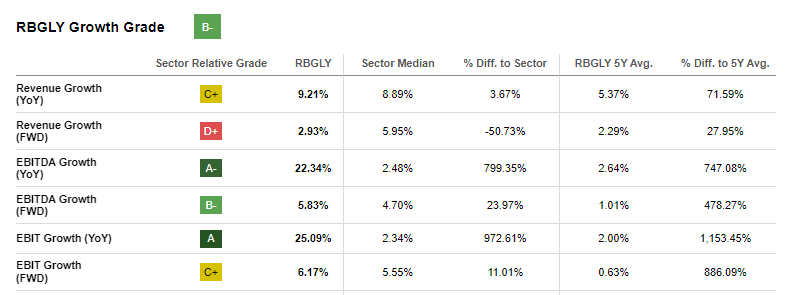

Growth (Seeking Alpha)

Reckitt's growth score is weakened by the fact its far superior margins will contract somewhat and is buoyed by its over-exposure to hygiene products. For this reason, we only care about forward revenue growth, which looks to be underwhelming. A portion of this is likely attributable to aggressive pricing to date but is nevertheless disappointing.

Valuation

{kind=link}

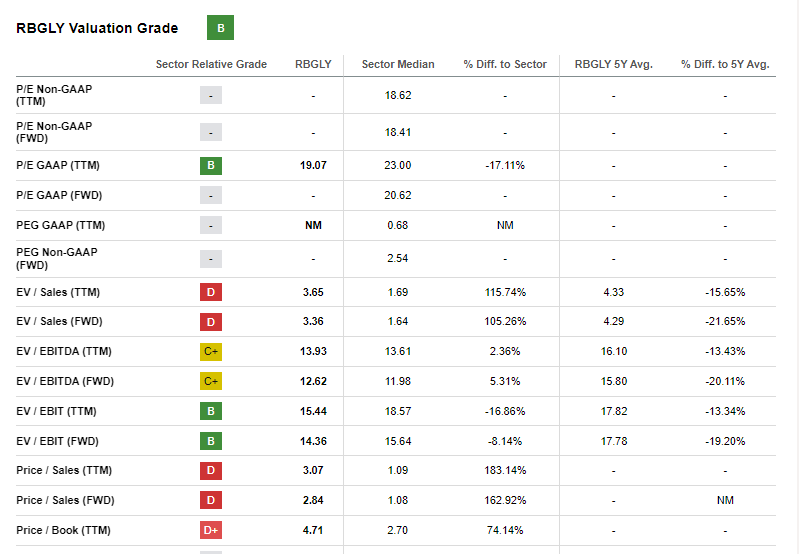

Valuation (Seeking Alpha)

Reckitt's current valuation receives a C rating, with the company partially punished for having an impressive GPM, resulting in a poor sales ratio. On an EBIT(DA) and earnings basis, the company looks slightly undervalued against its peers. Given the superior profitability, we see some upside on the table.

We have also conducted a DCF valuation as a means of cross-checking this view, with our main assumptions being:

- Revenue growth of 2-4%, in line with analysts' estimates.

- FCF conversion declining to 16-17%, reflecting softening trading conditions.

- An exit multiple of 15x EBITDA, a perpetual growth rate of 2%, and a discount rate of 9%.

Based on this, we derive an upside of 14%, which is not too dissimilar to analysts' consensus upside of 12%. For this reason, investors can partake in both capital appreciation, as well as capital distributions.

Final thoughts

Reckitt is the definition of a consumer staple business, owning some of the leading "everyday" brands. Our view is that the company is commercially sound, and positioned well to grow healthily long-term. Like many of its peers, it has failed with a big-ticket M&A transaction, but this has not left Reckitt irreparable. With market-leading margins and an attractive elasticity profile, we think the company represents a great defensive choice.

For further details see:

Reckitt Benckiser: Potential For Strong Free Cash Flow