RBGPF - Reckitt Benckiser: Still Optimistic For The Long Run

2023-11-06 04:41:54 ET

Summary

- Reckitt Benckiser reported mediocre third quarter results and provided a strategy update recently.

- While that strategy update was mostly a reaffirmation that Reckitt Benckiser is positioned well in a growing market, it announced a new share buyback program.

- While the company is continuing to struggle, I still see the business having a wide economic moat as well as the stock being undervalued.

In March 2023 I published my last article about Reckitt Benckiser (RBGPF), and as the article was published shortly after two major US banks collapsed - the Silicon Valley Bank and Signature Bank - and shocked the financial world, I claimed in my title that Reckitt Benckiser might be a good pick to avoid the banking turmoil.

In the last few months, we didn't see much turmoil - neither for Reckitt Benckiser nor for the regional banks. Nevertheless, Reckitt Benckiser did underperform the S&P 500 since my last article was published: While the S&P 500 gained almost 8% in about eight months, Reckitt Benckiser lost about 8% (not including dividends) and the investment was probably not the best idea. But as Reckitt Benckiser recently reported third quarter results and announced a new strategy, the company (and stock) deserve an update.

Quarterly Results

Similar to many other European businesses, Reckitt Benckiser is only reporting detailed results in the second and fourth quarter - half-year results and full-year results. In the quarters in between, they are only offering a small update.

Reckitt Benckiser Q3/23 Presentation

{kind=link}

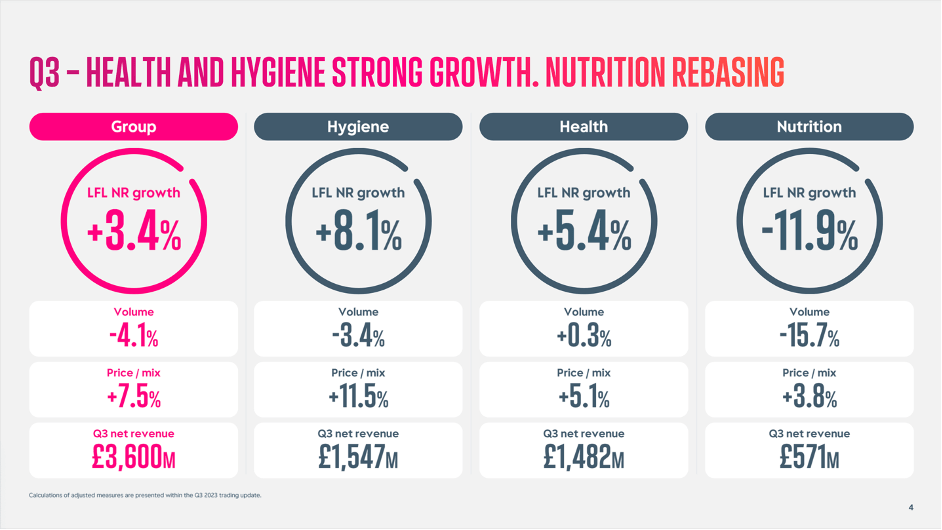

When looking at the third quarter, revenue for the group declined 3.6% year-over-year to GBP 3,600 million. On the other hand, like-for-like numbers saw 3.4% growth for the third quarter. And while volume declined 4.1%, especially price increased 7.5% YoY. Looking at the three different segments, the main problem was "Nutrition" - the segment reported 11.9% like-for-like revenue decline with volume declining 15.7%. Health reported 5.4% like-for-like growth with volume increasing 0.3% and price increasing 5.1% YoY. Hygiene reported 8.1% year-over-year like-for-like growth with volume declining 3.4% but price increasing 11.5%.

To be honest, I am not impressed by the numbers. The company could grow its prices at a solid pace - that is a good sign for a wide economic moat - but in times of high inflation with increasing prices, this is not so impressive. And the declining volume is not a great sign. We must point out, that the "Nutrition" segment could grow 22.9% like-for-like in fiscal 2022 - a strong growth rate due to "special effects". In my last article, I wrote:

And despite all excitement about the great numbers, we must point out that the high double-digit growth rates were mostly the resulted impact of the competitor supply chain disruption in the U.S. nutrition business. When excluding this impact, like-for-like growth was 5.4%, which is still a solid number, but not so impressive.

And after strong growth rates in one year we often see a reversion to the mean in the following year.

Strategy Update

Aside from reporting third quarter results, Reckitt Benckiser also reported a strategy update. To be honest, when hearing the words "strategy update" I am expecting new information and the company to have new ideas on how to grow its top and bottom line. However, when looking at the presentation and reading the transcript I am missing the new and updated strategy. And as CEO Kris Licht admitted himself: "Not all of this is new."

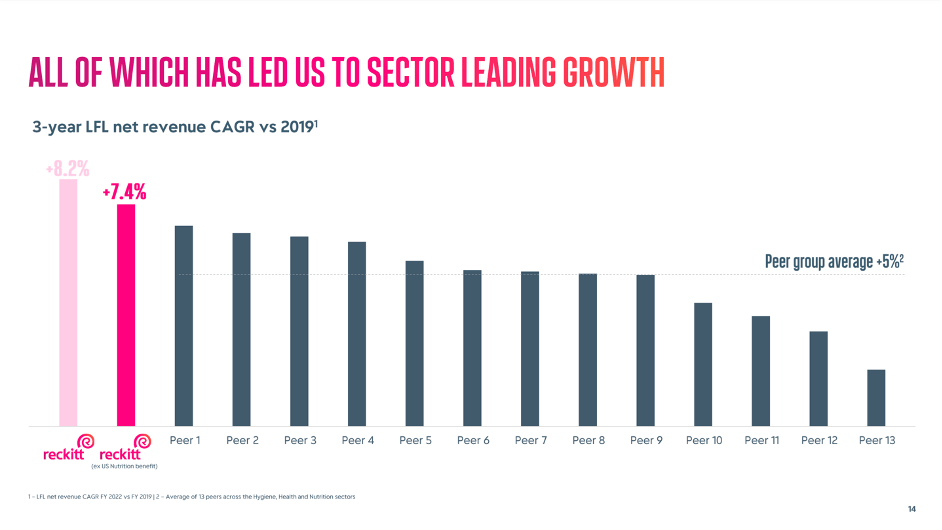

Overall, I would see this strategy update being rather a disappointment. Nonetheless, let's take a closer look. A huge part of the strategy update is about Reckitt Benckiser assuring investors that the business is positioned well in a growing market. And it is good to know that Reckitt Benckiser is seeing itself operating in several long-term growth categories and seeing itself already ahead of all its peers (regarding growth rates in the last few years).

Reckitt Benckiser Q3/23 Presentation

{kind=link}

Additionally, the company is also claiming to report higher gross margins than its peers. All in all, the conclusion of the strategy update seems to be that Reckitt Benckiser is positioned well ahead of its peers and is focusing on growing markets. And don't get me wrong, this is extremely important for any business - I just don't think this is a strategy update.

New Share Buyback Program and Dividend Growth

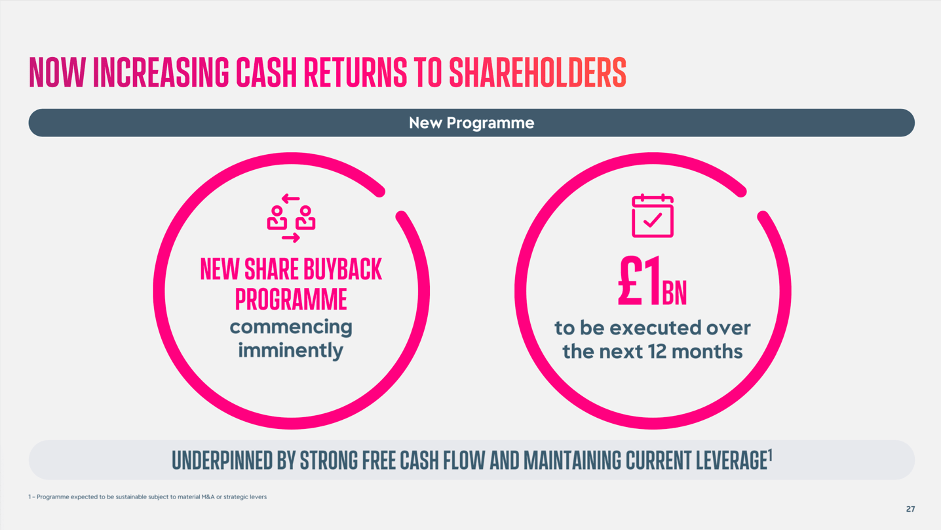

In my discussion of the new strategy, I excluded the most important information so far. Reckitt Benckiser announced a new share buyback program and during the next 12 months, the company will repurchase shares worth GBP 1 billion.

Reckitt Benckiser Q3/23 Presentation

{kind=link}

With free cash flow being around GBP 2.1 billion in H2/22 and H1/23, Reckitt Benckiser will spend about 50% of its free cash flow on share buybacks. And considering that the company spent GPB 1,284 million on dividends in fiscal 2022, Reckitt Benckiser will spend more on share buybacks and dividends in 2023 combined than it will most likely generate in free cash flow. According to its H1/23 guidance, the company is expecting free cash flow to be above GBP 2 billion, but probably not as high as GBP 2.3 billion. This is still not a problem as Reckitt Benckiser has GBP 1,027 million in cash and cash equivalents on its balance sheet and it is acceptable for the business to spend a part of the available cash on share buybacks.

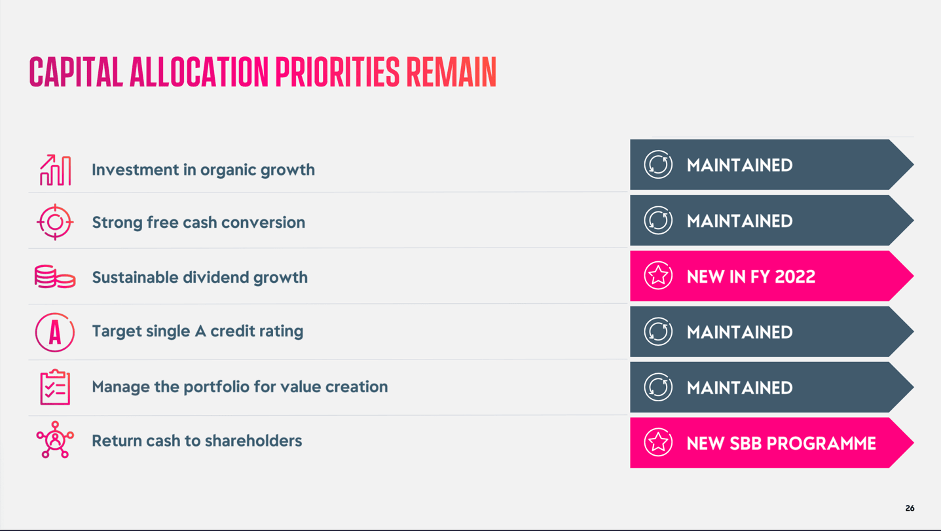

With a current market capitalization of GPB 41 billion, the company can repurchase about 2.5% of outstanding shares and boost its bottom line by about 2.5%. Aside from the announced share buyback program, management also pointed out it will focus on a sustainable dividend growth in the years to come (the company began to increase the dividend again in 2022 after it kept the dividend stable for several years before).

Reckitt Benckiser Q3/23 Presentation

{kind=link}

I personally see the share buyback program being a good idea as I still consider the stock undervalued and as long as management doesn't see better ways to use its free cash flow, share buybacks are a reasonable way to use cash. Of course, Reckitt Benckiser should not ignore its short- and long-term debt on the balance sheet that must be repaid at some point in time.

Intrinsic Value Calculation

When looking back at my articles I published about Reckitt Benckiser so far, I was always bullish about Reckitt Benckiser - except for my first article. And I remain bullish about the stock as I still think it is undervalued.

Using a discount cash flow calculation once again, we must make several assumptions. As free cash flow we can use the combined reported numbers for H2/22 and H1/23 resulting in a FCF of GBP 2,062 million. Additionally, we are taking 718.1 million diluted shares outstanding and - as always - we are using a 10% discount rate.

Now we must make some assumptions for growth rates in the years to come. During one of the last presentations, management set a mid-term growth target of 7% to 9% for earnings per share. I personally would be rather cautious as Reckitt Benckiser was not really able to grow at a solid pace in the last few years and use the lower end of that guidance and calculate with only 7% growth in the next ten years. Following that, we will calculate with 6% growth till perpetuity - as always. When calculating with these assumptions we get an intrinsic value of GBP 77.06 for Reckitt Benckiser. And as the stock is trading for GBP 56 right now, the stock trading about 27% below its intrinsic value.

We can also ask the question if 7% growth in the next ten years is realistic for Reckitt Benckiser. When looking at the last five years, the company could grow revenue with a CAGR of 4.66% and earnings per share declined with a CAGR of 17.85%. Looking at these metrics, assuming 7% growth for the years to come seems extremely optimistic. Nevertheless, we can assume 2% growth will stem from share buybacks in the years to come with the company's newly reinstated share buyback program. Management is also expecting revenue to grow in the low-to-mid single digits and therefore we can assume at least 4% growth right now. Additionally, we can assume margins to improve by 1% in the years to come as Reckitt Benckiser was pointing out its superior margins- compared to peers - but also pointed out it is seeing room to be more efficient. Overall, I think 7% growth in the years to come is an achievable target for the business.

Economic Moat and Further Thoughts

Reckitt Benckiser is a stock I am holding for several different reasons. One of the reasons is my deep conviction that we are headed for a recession and (probably brutal) bear market and the business can be seen as rather recession-resilient and defensive consumer stock. Another reason was the overvaluation of many other high-quality businesses. In my watchlist of about 150 companies that have most likely a wide economic moat, Reckitt Benckiser was one of the cheaper stocks that still had a wide economic moat.

Keeping these aspects in mind, I might switch investments in the coming quarters. We already saw several high-quality businesses declining extremely steeply. Some examples including PayPal ( PYPL ), the Estée Lauder Companies ( EL ), or the United Parcel Service ( UPS ) fall in the category of stocks that can report high RoIC and declined rather steep already.

And I might sell Reckitt Benckiser in the coming quarters and invest the cash in another business that offers a better risk-return ratio. Henkel might be another business falling in that category of rather defensive stocks I might sell. On the other hand, I am not clearly saying at this point that I will sell Reckitt Benckiser in the next few quarters. If I see a strategy update and improvement in the business, I might hold the stock.

The question if I might sell Reckitt Benckiser in the coming quarters for another (maybe better) investment also depends on Reckitt Benckiser itself. In the last few years, Reckitt Benckiser was clearly struggling and making the argument that the business has a wide economic moat is not so easy. With return on invested capital being only 3.15% on average and gross margin declining a little bit and operating margin declining a bit more, we must question if the company actually can have a wide economic moat.

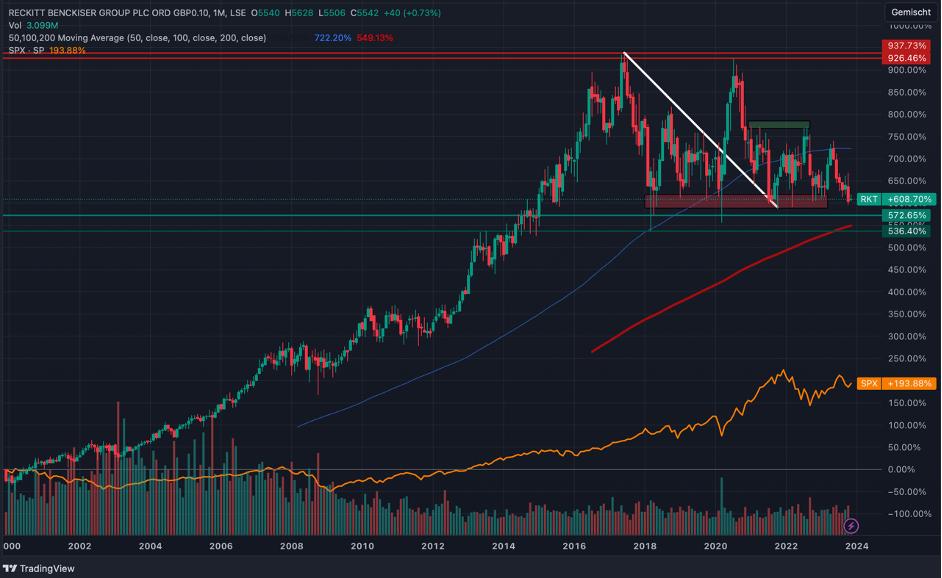

But when looking at longer timeframes, Reckitt Benckiser is without doubt a great business. In the last ten years, Reckitt Benckiser could report a return on invested capital of 22.08% on average which is a strong hint for a wide economic moat. And since 2000, Reckitt Benckiser increased 616% in value (not including dividends) while the S&P 500 increased only 193% in value (also not including dividends). When looking at the long timeframe, we can certainly make the argument that Reckitt Benckiser is a great business. Over the long run it has stable margins, an extremely high return on invested capital and the stock clearly outperformed the index over the last 23 years.

{kind=link}

By the way, we can also see in the chart above that Reckitt Benckiser is a good example of a stock that was performing well while the market and economy were in serious trouble. When looking at the years 2000 to 2002, the S&P 500 declined almost 50% while Reckitt Benckiser increased almost 60% in value. This is valuable information for the years to come: I am expecting a recession and bear market, but that does not mean every single stock has to decline as well. Many stocks are drawn down with the overall market, but some undervalued, good-performing companies might be able to increase during this time. This is a solid argument for holding on to stocks - even in times of a recession and brutal bear market. If one has done the necessary research to identify companies that are undervalued and will perform solid (or great) in the years to come, one does not necessarily have to fear a recession or bear market.

Reckitt Benckiser Q3/23 Presentation

{kind=link}

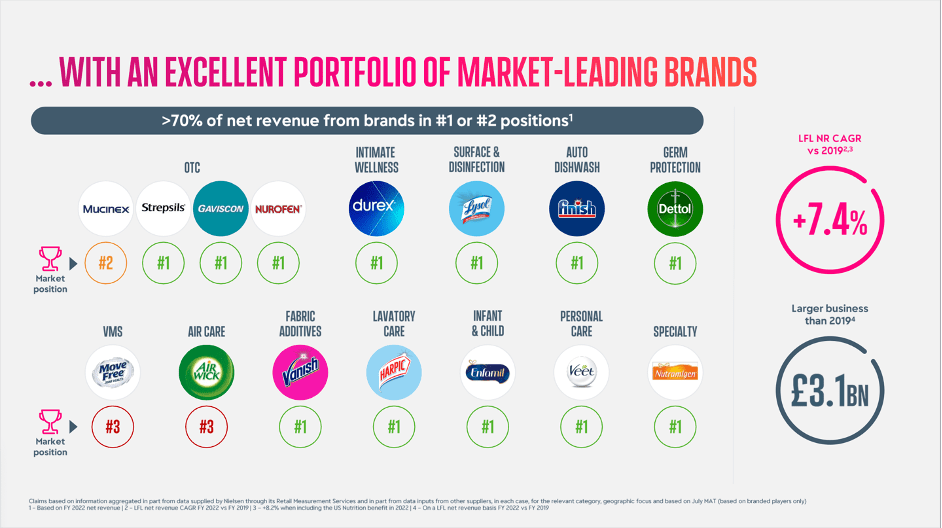

The question right now is if Reckitt Benckiser is one of those companies and is able to return to its previous great performance. At least it is good to know that Reckitt Benckiser has a portfolio of market-leading brands and many of its products are market leaders. About 70% of net revenue is stemming from brands being #1 or #2 in their markets.

Bottom Line

I still think Reckitt Benckiser is a great investment and certainly a "Buy" at this point. And although I might switch investments in the coming quarters, if better opportunities would present themselves, I don't claim that Reckitt Benckiser is not a good investment and that the company does not have a wide economic moat. It is only Reckitt Benckiser still must prove if it is able to return to the path of growth and report similar results again as it has in the past decades. In the last few years, we saw the picture of a business struggling a little bit.

But the good thing about a wide economic moat is the fact, that these moats are in most cases very durable and despite a company struggling for quite some time - several years - it is often helping the business to return back on the path of success. It is not easy to destroy an economic moat.

For further details see:

Reckitt Benckiser: Still Optimistic For The Long Run