FAT - Red Robin Gourmet Burgers: A Risky But Potentially Stellar Turnaround Prospect

Summary

- Red Robin Gourmet Burgers has faced a lot of pain in recent years, with sales, profits, and cash flows all falling.

- Recent data has been far from great, but management has admitted their problems and seems to be working on a solution.

- This plan lacks the serious details investors need to see, but given how cheap RRGB shares are, it could result in material upside if all goes well.

So far, restaurant chain Red Robin Gourmet Burgers ( RRGB ) seems to be starting the 2023 fiscal year off on the right foot. On January 9th alone, shares of the company roared higher, closing up 14.6% compared to what they closed at one day earlier. This move was brought about in response to management releasing preliminary results covering the final quarter of the firm's 2022 fiscal year. In addition to that, it also announced a strategic review and a five-point plan aimed at boosting profitability in the years to come. At the end of the day, this ultimately brings up a good question of whether the company makes sense for investors to consider or not. Given how cheap shares are, the company could offer a nice bit of upside. But this upside does not come without meaningful risks.

Red Robin Gourmet Burgers - A firm reinventing itself

Before we dig into the juicy details, we should touch on how the company feels about the final quarter of its 2022 fiscal year. Truth be told, not much was offered in the way of results. What we do know, however, is that the company said that revenue should come in at around $290.2 million. This would translate to a 2.4% increase over the sales generated one year earlier. This sales figure should be the result of a 2.5% rise in comparable restaurant sales, representing the 8th consecutive quarter of comparable sales growth for the firm. On its own, this is not all that great a development. While it's great to see revenue increase year over year, analysts were actually forecasting sales of nearly $295.6 million. In addition to reporting preliminary sales figures, the company also said that the number of members under its royalty program, called Red Robin Royalty, end of the year at 11.3 million. That's roughly 0.3 million higher than it was previously.

{kind=link}

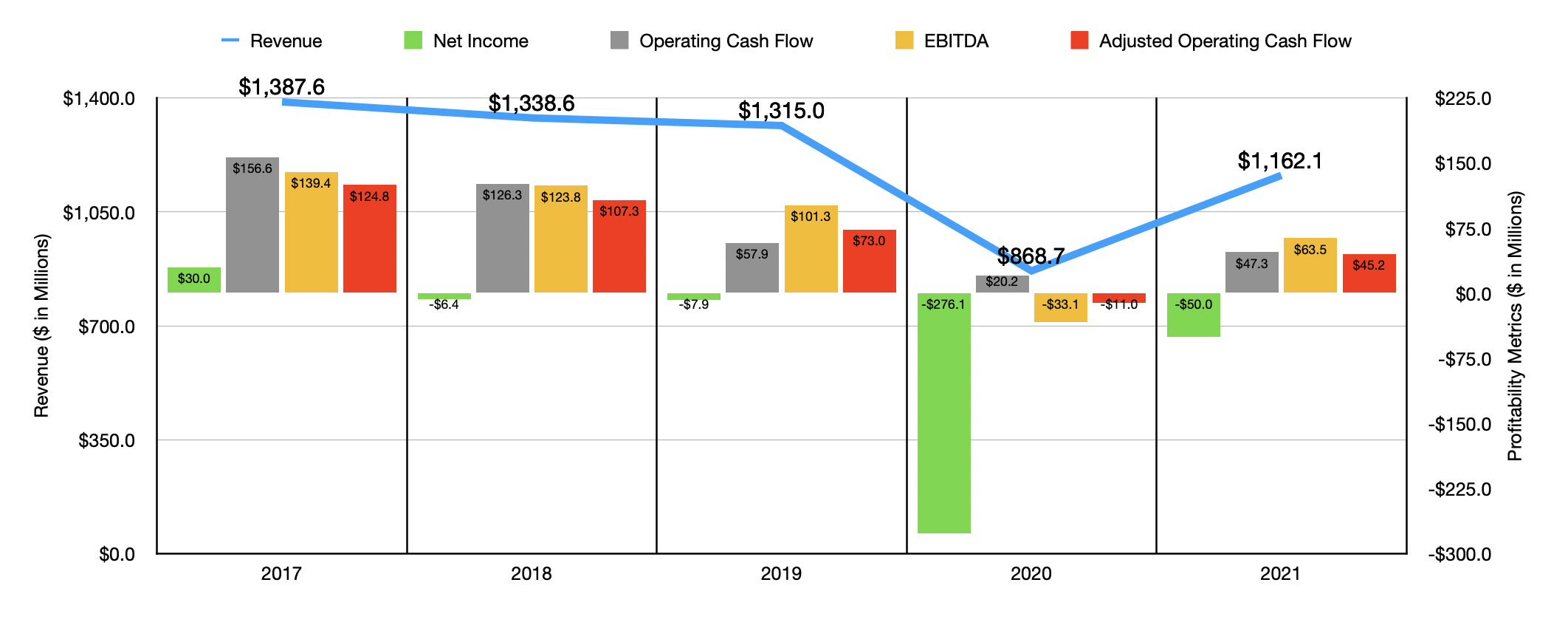

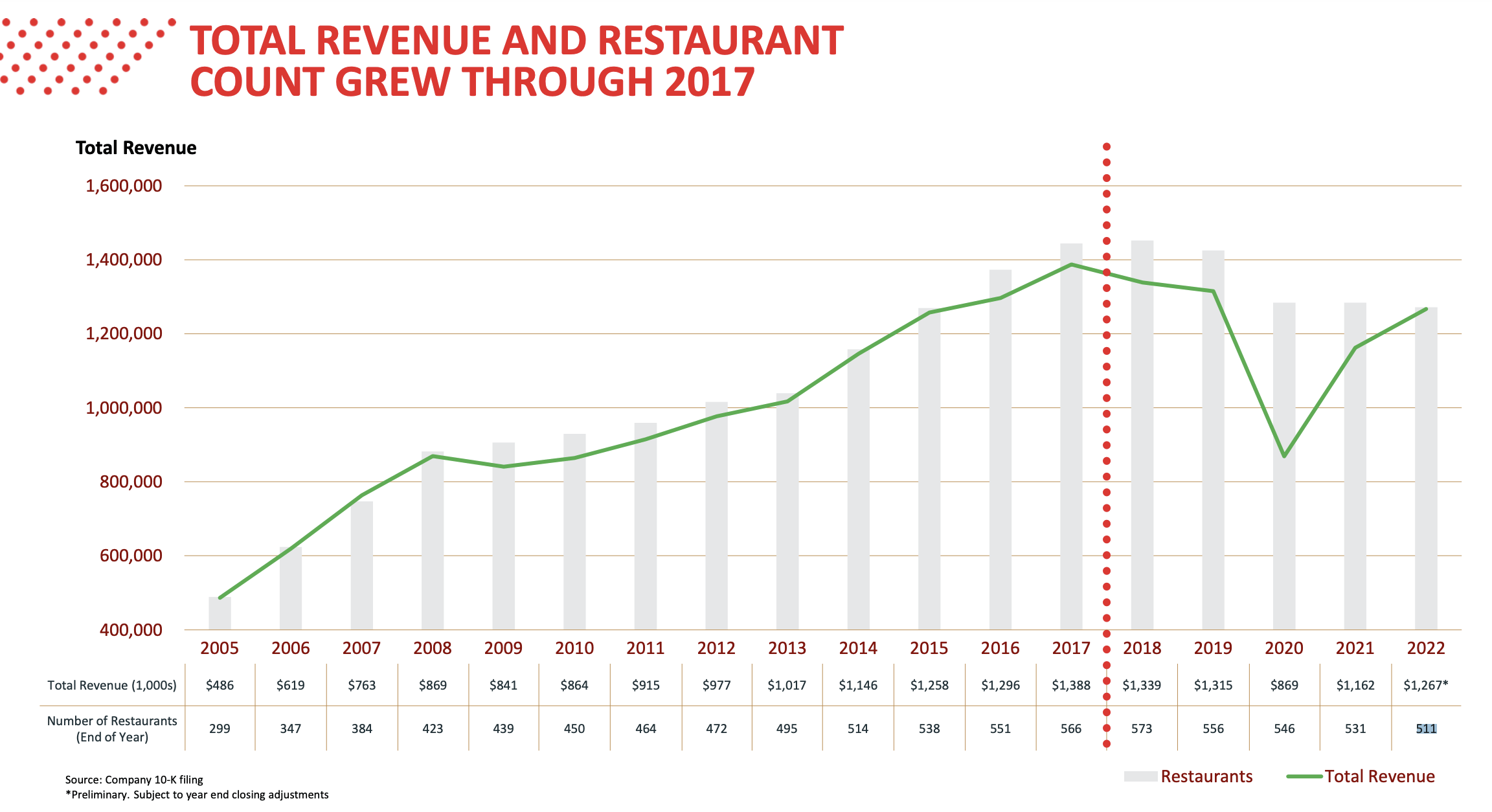

If this were all the news that was reported, it's likely that shares of the company would have fallen. But management did not stop there. For years , the company has been struggling. As you can see in the chart above, revenue decreased between 2017 and 2020, plunging from $1.39 billion to $868.7 million. Though it is worth noting that the largest portion of that decline came during the COVID-19 pandemic. Sales rebounded to some degree in 2021, ending that year at $1.16 billion. Although the pandemic had an impact on the company, it's important to note that one drag on the firm has been the fact that the number of locations it has in operation has been on the decline for years. After peaking at 573 locations in 2018, the company began a steady decline, hitting 531 locations in 2021 and 511 by 2022. Comparable store sales were also problematic, decreasing double digits in some years.

{kind=link}

Profitability for the company has also fallen at the same time. The company went from a net profit of $30 million in 2017 to a net loss of $276.1 million in 2020. While the 2021 fiscal year was better, the company still lost $50 million. Other profitability metrics have been a bit better. Operating cash flow fell from 2017 through 2020, plunging from $156.6 million to only $20.2 million. But in 2021, it more than doubled to $47.3 million. If we adjust for changes in working capital, it actually would have gone from negative $11 million in 2020 to $45.2 million in 2021. A similar trend can be seen when looking at EBITDA, with the metric going from negative $33.1 million in 2020 to $63.5 million in 2021.

{kind=link}

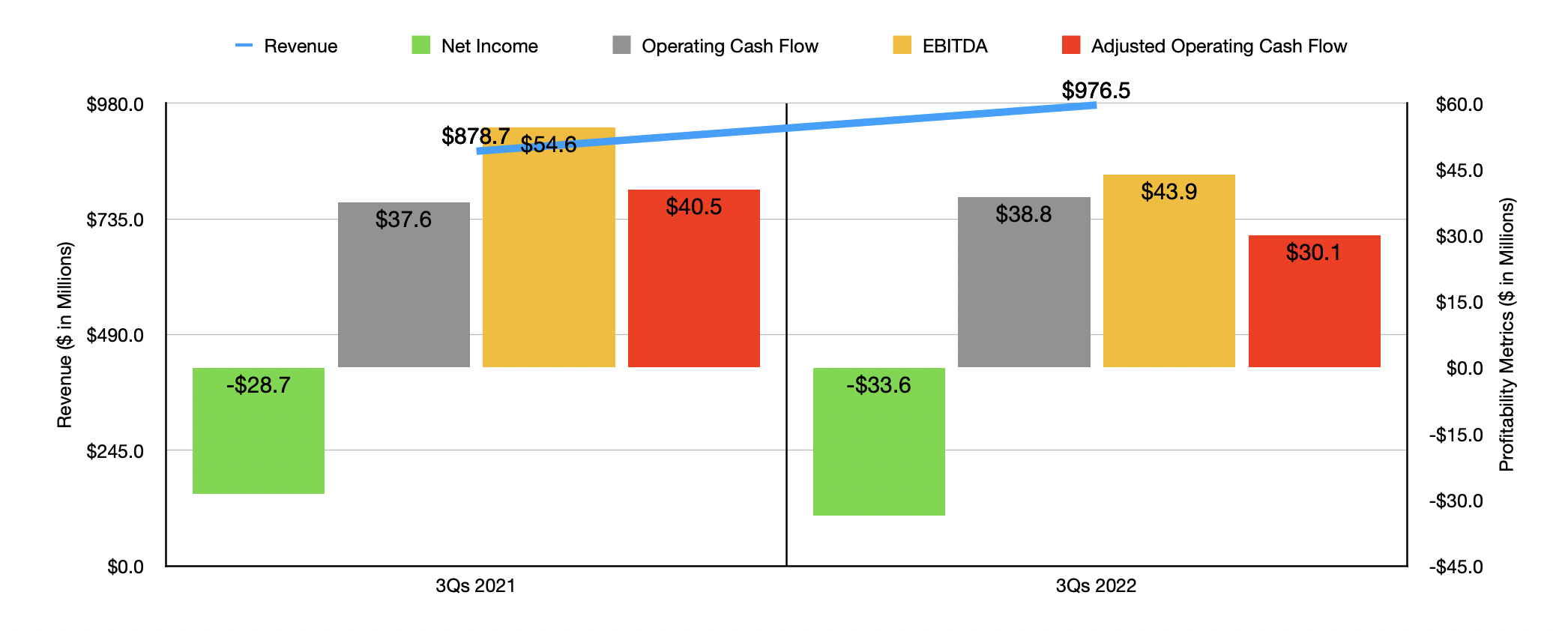

When it comes to the 2022 fiscal year, results have been somewhat mixed. Revenue did increase, jumping from $878.7 million in the first nine months of 2021 to $976.5 million the same time of 2022. Price increases helped the company on this front. Unfortunately, profit figures have been mixed. The firm's net loss went from $28.7 million in the first nine months of 2021 to $33.6 million the same time of 2022. Operating cash flow, on the other hand, improved slightly from $37.6 million to $38.8 million. If we adjust for changes in working capital, however, it would have fallen from $40.5 million to $30.1 million. Similarly, EBITDA dropped from $54.6 million to $43.9 million.

{kind=link}

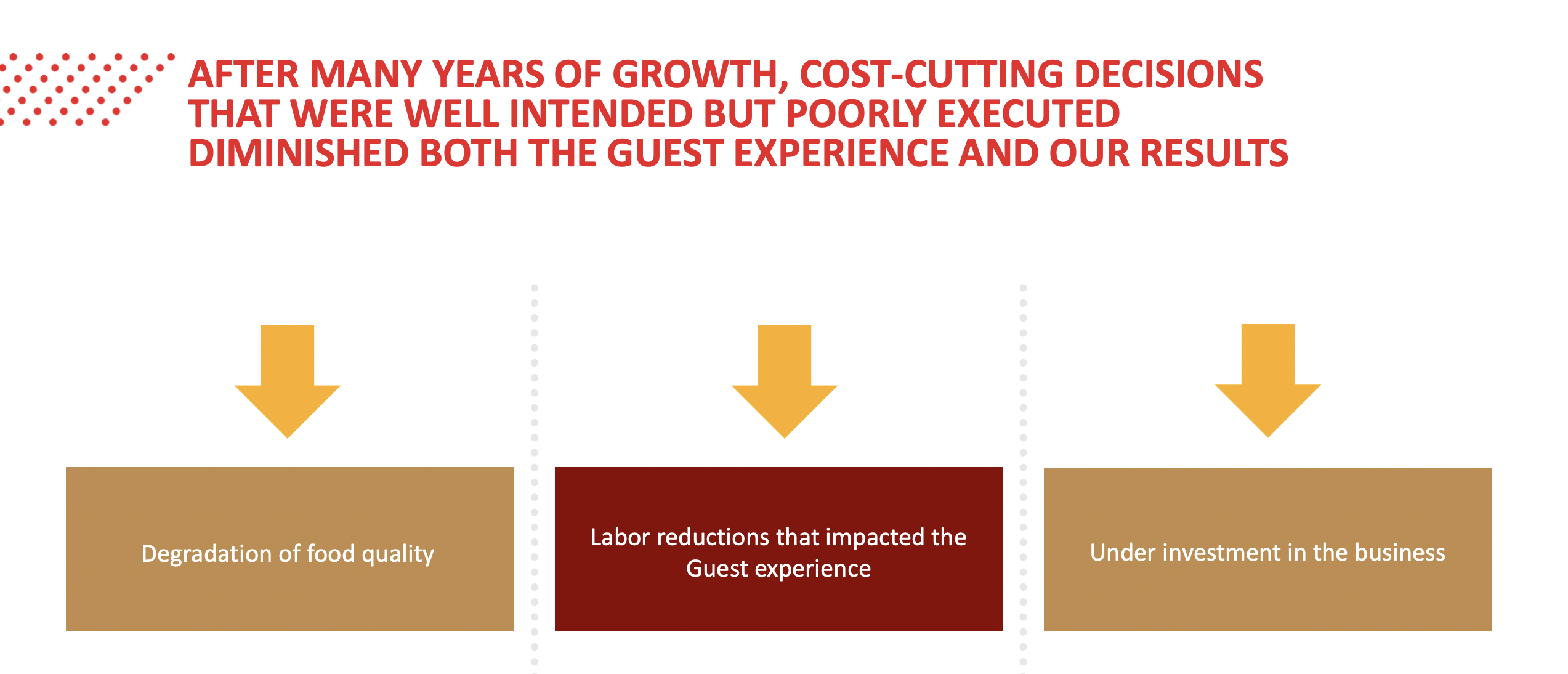

For as long as uncertain economic conditions exist, it's likely that the company will have mixed results. But it is important to note that management seems to have finally come to terms with some serious problems. In its own investor presentation, the company even announced that, ‘after many years of growth, cost-cutting decisions that were well intended but poorly executed Diminished both the guest experience and… results’. The company provided further details on this, acknowledging a degradation of food quality, labor reductions that impacted the guest experience, and underinvestment in his business. It's rare from my experience that companies are this blunt about their shortcomings. That's the good side of the case being made now.

{kind=link}

{kind=link}

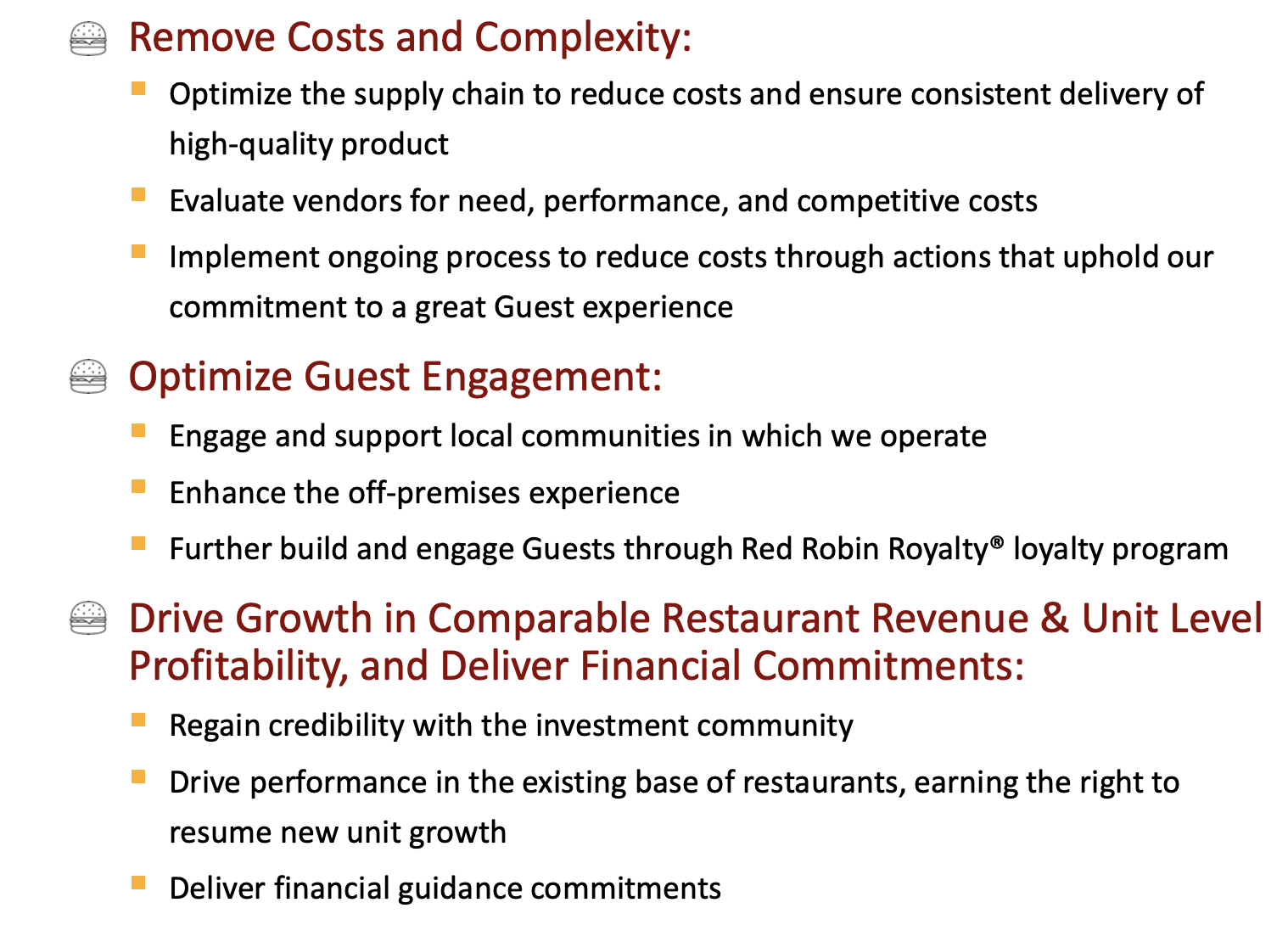

In an attempt to rectify these problems, management has initiated a five-point plan that centers around transforming into an operations-focused restaurant company, improving the guest experience, reducing costs and complexity, optimizing guest engagement, and driving growth and profitability. The full extent known publicly about this plan can be seen in the image below. And this is where the bad side comes in. When investors want and need to see at a time like this are concrete steps that have dollar amounts attached to them. How much in cost savings can the company achieve? What assets need to be divested of or shut down? How will the supply chain change? The list goes on. But the firm offers none of this. They have already fallen on their sword by admitting some harsh truths. But they have offered up no substantive changes except their goal to double the EBITDA margin of the company over the next three years and to initiate a review process that could see them engage in a sale-leaseback transaction between now and the end of the second quarter of this year.

For those not familiar with a sale-leaseback transaction, it is an arrangement where a company that currently owns assets sells those assets off to a new owner and then leases them back, often for an extended period of time. In the long run, the company may end up paying more to operate. But the hope is that the proceeds can be put to better use today in order to create long-term value for shareholders. One option here might be for the company to pay down its debt, while another might be for it to invest in the aforementioned plan. The company does have net debt right now of $133.2 million. So reducing that in order to lower leverage and cut interest expense could push the company closer to a good cash flow position.

The plan in question may result in up to 35 of its restaurants being sold and leased back. I felt as though this number was quite small considering the company has 511 locations in operation. 81% of these locations are company owned compared to 19% that are franchise owned. But at the end of the day, the devil is in the details. Although most of its locations are company-owned, almost all of them are actually leased properties. When the company refers to something being owned by itself, it really means the restaurant is operated by management. In fact, as of the end of its 2021 fiscal year, only 37 of its restaurants were fully owned by the company. That means that all or substantially all the assets associated with its truly owned locations will be sold off and leased back to the company if this plan goes through as expected.

This is not to say that the company is making a bad move here. If they do have actionable steps aimed at improving operations and/or they can get enough capital to pay down debt materially, this may be the best move to make. But it doesn't mean that the company has some magic pill to raise tremendous amounts of cash. Even with this fact taken into consideration though, shares might still make sense for investors to buy into. For the 2022 fiscal year in its entirety, management is forecasting EBITDA of between $53 million and $58 million. If we annualize results experienced so far for adjusted operating cash flow, then we might expect a reading there of $33.6 million.

{kind=link}

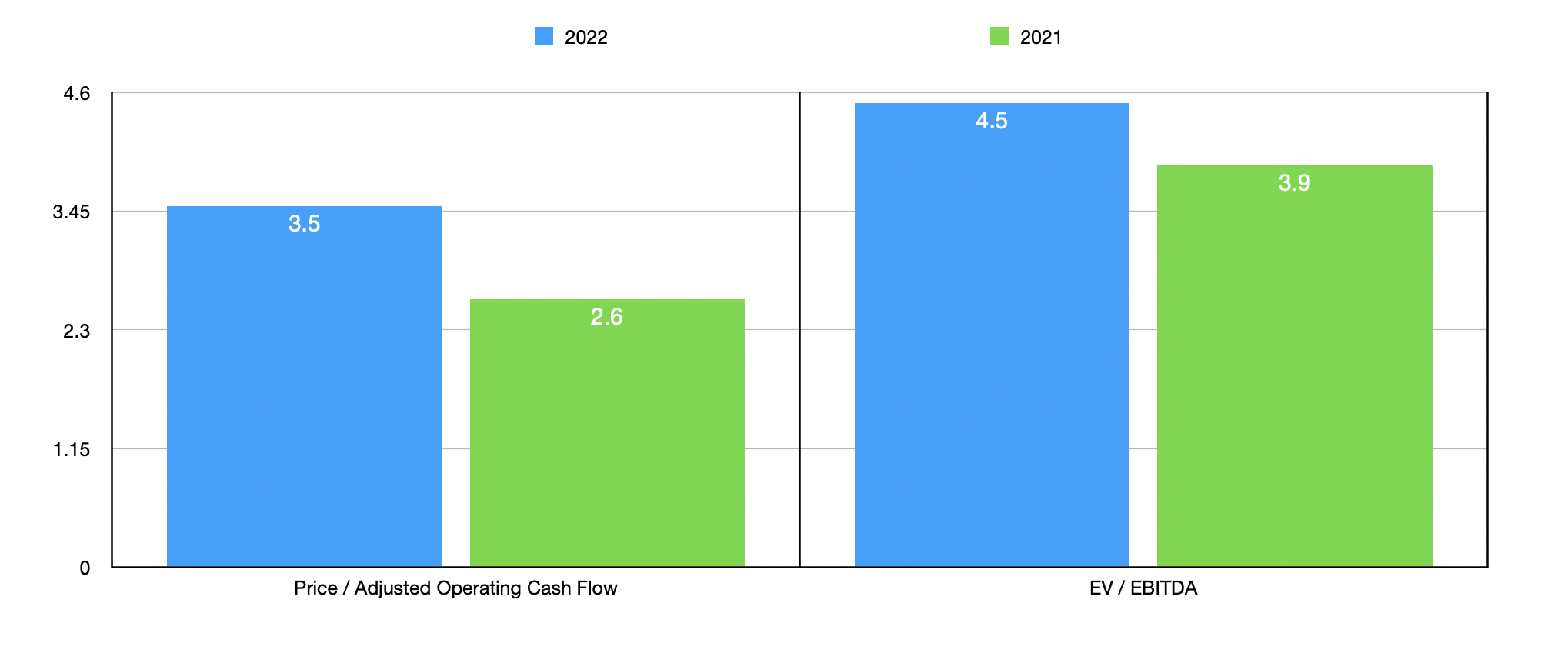

Based on these numbers, the company is trading at a forward price to adjusted operating cash flow multiple of 3.5 and at a forward EV to EBITDA multiple of 4.5. By comparison, using the data from 2021, these multiples would be 2.6 and 3.9, respectively. These are incredibly low on an absolute basis. As you can see in the table below, they are also cheap relative to similar firms. On a price to operating cash flow basis, five companies that I looked at that are similar in nature to Red Robin Gourmet Burgers are trading at multiples of between 4.4 and 153.9. Using the EV to EBITDA approach, the range is between 4.6 and 45.2. In both cases, our prospect is the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Red Robin Gourmet Burgers |

| 3.5 |

| 4.5 |

| FAT Brands ( FAT ) |

| 153.9 |

| 24.5 |

| Carrols Restaurant Group ( TAST ) |

| 4.4 |

| 27.9 |

| Potbelly Corp. ( PBPB ) |

| 51.9 |

| 11.6 |

| Fiesta Restaurant Group ( FRGI ) |

| 17.1 |

| 45.2 |

| Noodles & Co. ( NDLS ) |

| 18.5 |

| 18.6 |

Takeaway

Given everything that's going on at the moment, I would make the case that Red Robin Gourmet Burgers is most certainly an interesting prospect that investors should consider. I by no means think that the company is some easy money or a home run. But I do think it could offer a tremendous amount of upside for those who are bullish about the firm if that bullish call ends up being right. Simply because of how cheap shares are, combined with the fact that management is looking at a sale-leaseback transaction and the fact that cash flow is still positive despite current inflationary pressures, I have decided to rate the company a soft ‘buy’. But I would be a fool to say that the company should not be monitored very closely to see what kind of actionable steps are taken, if any, to solve its current woes. In the event that something doesn't come out of the woodwork, rather quickly, investors would be wise to reconsider a stake in the business.

For further details see:

Red Robin Gourmet Burgers: A Risky, But Potentially Stellar Turnaround Prospect