FATBB - Red Robin Gourmet Burgers' Meteoric Rise Isn't Over Yet

2023-03-30 13:47:57 ET

Summary

- Red Robin Gourmet Burgers has done incredibly well over the past couple of months, with shares nearly doubling.

- This is in spite of mixed but mostly weak financial results reported last month and was driven by strong guidance for the future.

- Uncertainty and risks both exist, but shares are still cheap enough to warrant upside from here.

Most people probably wouldn't be surprised by the fact that the food service industry is one of the largest parts of the economy in the US. Employing millions of people and meeting the biological necessity to eat, often as people go about their busy days, is big business, with the market estimated to be worth nearly $1 trillion this year. You would think that such a large market would allow many companies to thrive. But in all actuality, it has created a tremendous amount of competition where countless players end up losing, and only the best survive. One company that has been on the losing end for a long while, but that is now showing significant signs of returning to health, is Red Robin Gourmet Burgers ( RRGB ). This year alone, shares have skyrocketed, defying a weakening on the company's bottom line and on the back of optimism about the future. Even after seeing shares rise materially, the company is trading on the cheap. The company does have some problems, including those related to recent profits and cash flow figures. But given how cheap the stock is and the path that management has the business set on, I do still believe that it warrants a ‘buy’ rating, even if that rating is a soft one.

A massive market

There are very few industries in the US that can hold a candle to the food service industry when it comes to size. According to one study, the market is expected to add around 500,000 jobs this year alone, taking total employment by the end of 2023 to 15.5 million. This growth has been driven by a recovery following the pandemic and is made possible by the fact that 84% of consumers have claimed that going out to a restaurant with family and friends is a better use of their leisure time than cooking food at home themselves and cleaning.

Another way to understand this market is to look at the economic impact of it all. For 2023, it's estimated that the food service industry will be worth around $997 billion. That's $60 billion, or roughly 6.4%, above the $937 billion that the industry was worth in 2022. It's also worth noting that this comes off the back of rapid growth seen in 2022. Industry experts had claimed that the market would only be worth $898 billion last year.

Red Robin Gourmet Burgers has done well

When I last wrote about Red Robin Gourmet Burgers back on January 10th of this year, I talked about how the company had faced a lot of pain over the prior few years, with financial results across the board suffering. Even throughout the 2022 fiscal year, results had been anything but great, but it was encouraging to see management admitting to the company's problems and focusing on a solution. This took the form of a five-point plan that the company was dedicated to following so that it could get its operations back on track. Though it's important to note that the plan in question was severely lacking in detail. Despite these shortcomings, I found myself encouraged by the changes the company had been making, and I was drawn in by just how cheap the stock was. These factors led me to rate the business a ‘buy’, a rating that reflected my view that shares should outperform the broader market moving forward. Little did I know just how much this outperformance would be. In such a short time since the publication of the article, the stock has skyrocketed 93.4%. That compares to the 3.6% upside experienced by the S&P 500.

{kind=link}

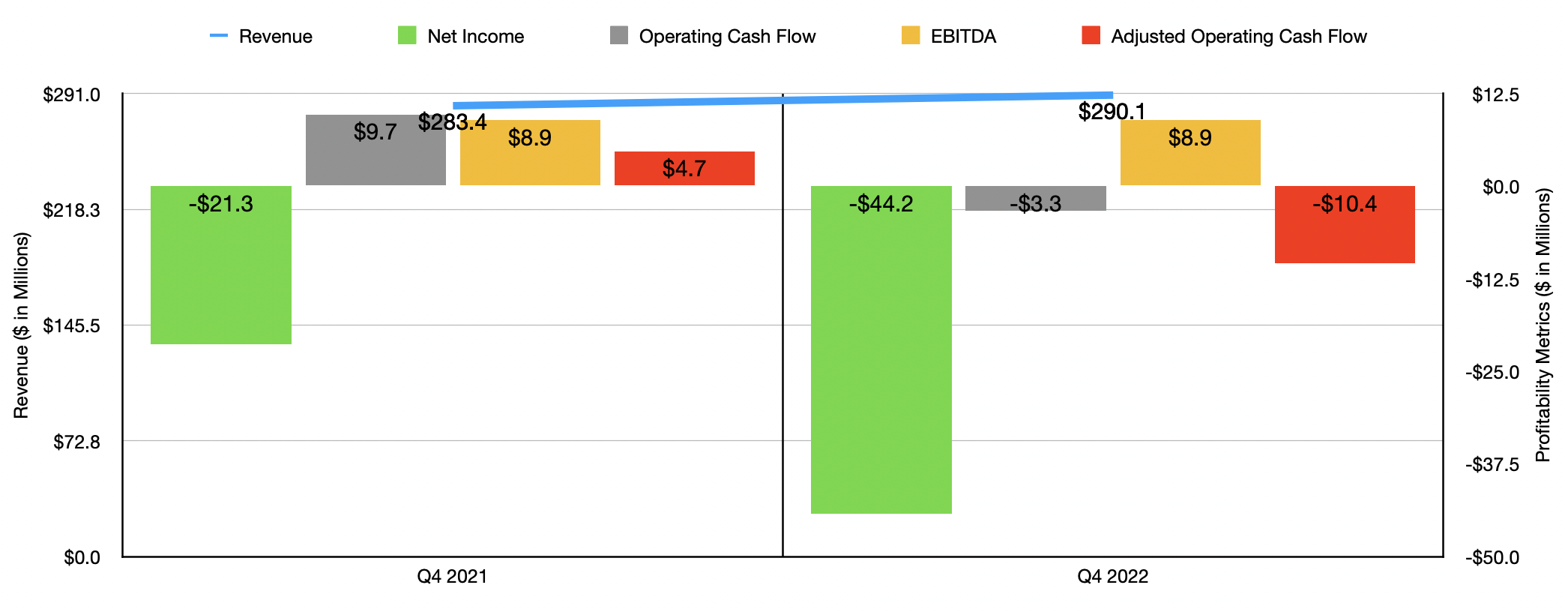

This massive surge largely came in response to the fourth quarter earnings release that management made public on February 28th. Normally, such a move higher would have been driven by a significant outperformance by the business. But the firm actually fell short of expectations during that time. Particularly problematic was the company's bottom line. Its net loss went from $21.3 million in the final quarter of 2021 to $44.2 million in the final quarter of last year. Operating cash flow turned from $9.7 million to negative $3.3 million. If we adjust for changes in working capital, the picture was even worse, with the metric going from $4.7 million to negative $10.4 million. The only metric that held stable was EBITDA, hitting $8.9 million in both quarters.

{kind=link}

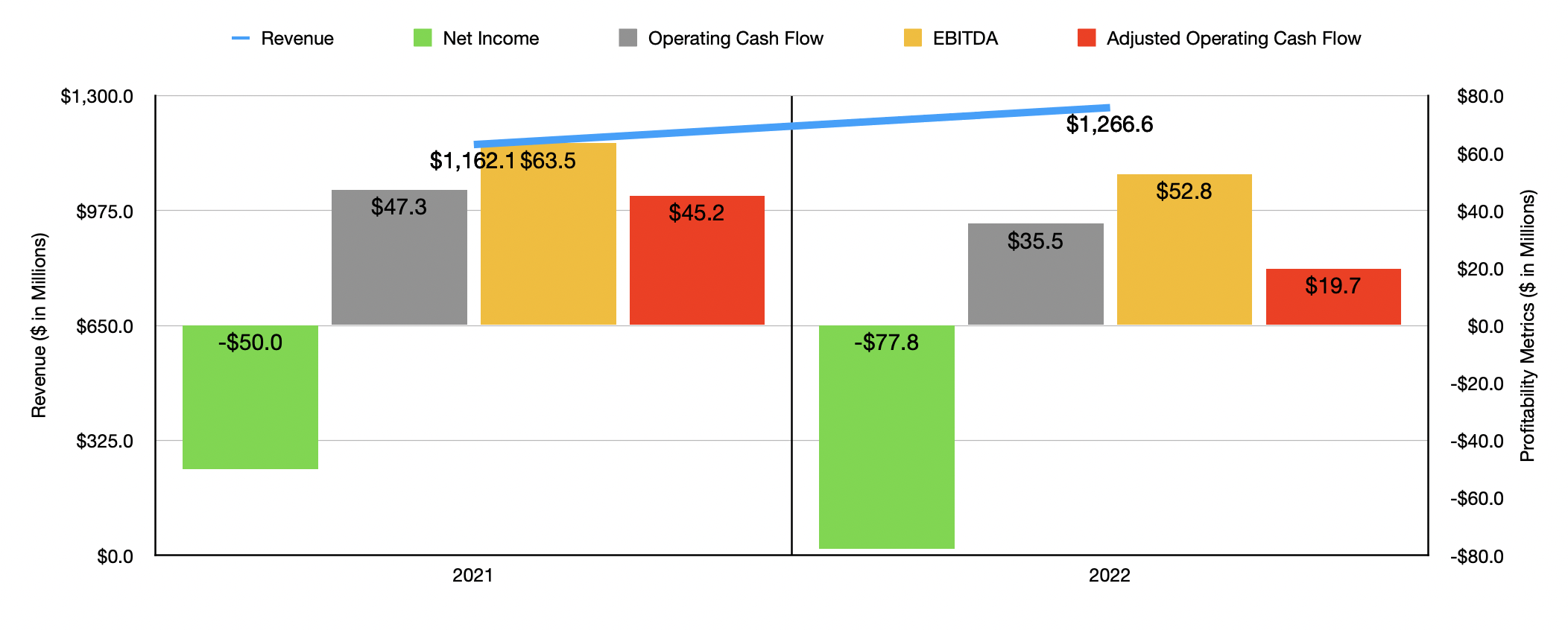

Not everything was awful though. Revenue, for instance, managed to hit $290.1 million. That's 2.4% higher than the $283.4 million generated in the final quarter of 2021. This increase, management said, was attributable to a 2.5% rise in comparable restaurant sales. On an adjusted basis, the growth was a more modest 1.5%. The rise came about even in spite of a 6.3% decline in guest traffic. Menu price increases added 7.3% to the company's top line, while a change in menu mix added 2.2%. This all follows a trend that developed throughout the 2022 fiscal year in its entirety. As you can see in the chart above, bottom line results for 2022 were worse than they were in 2021. However, revenue for the company rose nicely year over year, even as guest traffic declined by 0.9%. This was more than offset by a 6.4% increase in menu prices and a 3.8% contribution coming from menu mix. Overall, this resulted in comparable restaurant revenue for the company growing 9.2% year over year.

Much of the optimism centered around Red Robin Gourmet Burgers seems to involve management's outlook moving forward. Revenue for 2023, for instance, should come in at around $1.3 billion. That's 2.6% higher than the $1.27 billion reported one year earlier. Though it is worth noting that this increase is being aided in part by an extra week of operations that will be under the firm's belt this year compared to last. At the same time, profits as measured by EBITDA are forecasted to come in stronger, totaling between $62.5 million and $72.5 million. At the midpoint, that would be 27.8% above the $52.8 million reported for 2022. It would also imply adjusted operating cash flow of around $46.9 million compared to the $19.7 million seen in 2022.

Aiding the company will be a continued focus on cost-cutting initiatives. Management has not provided that much in the way of detail on this front. But they did say that they see certain opportunities in the supply chain to reduce expenses, with some examples including the increase of pack size for the same products that it buys today, as well as consolidating vendors in order to take advantage of its scale. The firm is also looking to right-size Some of its vendor contracts as well. Outside of the cost-cutting side of things, the firm is also dedicated to expanding its Donatos partnership. At present, around 250 of its restaurants are outfitted with this capability. The firm plans to add another 25 installations this year. These factors, combined with attempts at improving guest engagement, as well as other initiatives, will push the company, management says, toward doubling its EBITDA margin by 2025 compared to what the company generated in 2022. Even if sales were to remain flat relative to what was seen in 2022, this would push the metric up to $105.6 million.

{kind=link}

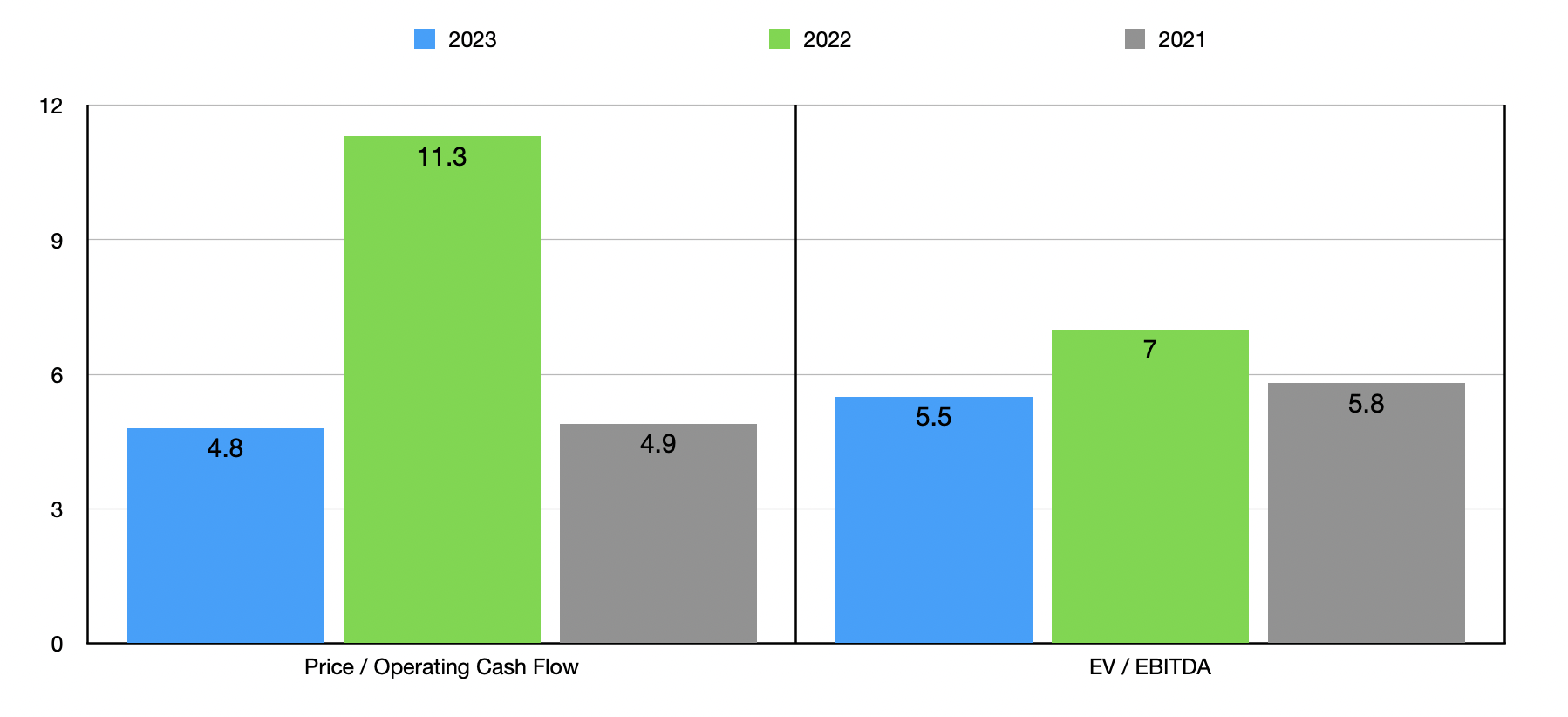

In terms of valuation, shares of the company do still look cheap, even after rising materially. As you can see in the chart above, I priced the company using estimates for 2023, as well as using actual results from both 2021 and 2022. And in the table below, I compared the business to five similar firms. On a price-to-operating cash flow basis, the trading multiple of 11.3 meant that only one of the five competitors was cheaper than it. And when it comes to the EV to EBITDA multiple of 7, Red Robin Gourmet Burgers is still the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Red Robin Gourmet Burgers |

| 11.3 |

| 7.0 |

| FAT Brands ( FAT ) |

| 153.9 |

| 66.6 |

| Carrols Restaurant Group ( TAST ) |

| 5.5 |

| 17.9 |

| Potbelly Corporation ( PBPB ) |

| 17.9 |

| 11.7 |

| Fiesta Restaurant Group ( FRGI ) |

| 13.0 |

| 31.3 |

| Noodles & Company ( NDLS ) |

| 22.6 |

| 11.5 |

Takeaway

Based on the data that I can see, Red Robin Gourmet Burgers is in an interesting position at this point in time. The most recent data provided by management was mixed and largely negative. But current guidance for 2023 is positive and management remains confident that their plans will drastically improve operations moving forward. I am always skeptical of what management forecasts for any business. This is especially true of a company that has struggled in recent years. But that's why buying stock at low trading multiples is important. In this case, for instance, I do think that the risk is largely priced into the picture, meaning that downside from here is likely minimal. As such, I have decided to keep the company as a ‘buy’ candidate for now.

For further details see:

Red Robin Gourmet Burgers' Meteoric Rise Isn't Over Yet