M - REIT Opportunities Remain Abundant: 3 Top Picks

2024-01-06 09:00:00 ET

Summary

- REITs crashed due to rising interest rates.

- But they are now set to rally as interest rates are cut in 2024.

- The window of opportunity is closing fast, but opportunities remain abundant.

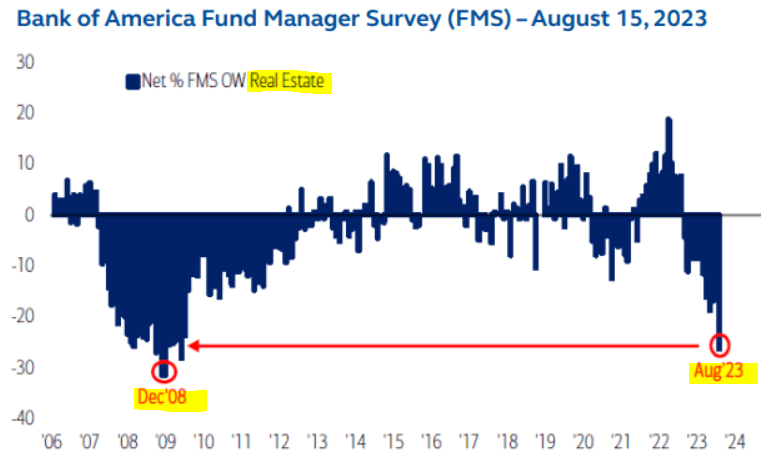

For most of 2022 and 2023, investors avoided REITs due to rising interest rates. As a result, allocations to REITs dropped to their lowest levels since the great financial crisis and with that, valuations also became heavily discounted:

Bank of America REIT valuations are historically low (Principal Asset Management)

{kind=link}

But here's my important warning for you: this is all about to reverse in 2024 and REITs could recover just as fast as they crashed.

Inflation has normalized, the economy is weakening, and interest rates have already begun to decline...

Most major banks ( JPM , BAC , GS , DB , etc.) are now predicting significant rate cuts already by mid-2024, and the Fed just recently indicated at least 3 rate cuts in the next 12 months.

This is very important news for REITs because the only reason why they are shunned by the market is about to disappear.

If REITs crashed due to rising interest rates, then declining interest rates should have the opposite effect. Studies also prove this point: REITs are strong outperformers in the periods after rates reach their peak and start to decline.

Cohen & Steers

That's today!

Right now, investors are still comfortably hiding in money market funds and short-term treasuries, thinking that they will earn a ~5% yield.

These short-term fixed-income instruments have amassed $10s of billions of capital over the past two years, and a lot of it came from income vehicles like REITs.

But this 5% yield is nothing more than an illusion.

As rates are cut, and the expectation for declining rates kicks in, investors will realize that the "5% yield" was just a mirage and I predict that a lot of that capital will come right back into the REIT market.

The 5% seemed very compelling when the expectations were that we would stay in a "higher for longer" environment with more rate hikes to come.

But after rates are cut by ~100 basis points, and the market begins to expect even more rate cuts, then money market funds will suddenly become very unattractive relative to alternatives like REITs.

That's because you will end with a 3-4% nominal yield, which is only 1-2% in real terms, and you will risk further yield erosion as rates are cut further. Moreover, you won't participate in any upside or growth so you will be exposed to significant reinvestment risk.

So suddenly, securing a ~6% dividend yield from a REIT that's growing, coupled with some upside as rates are cut, will become far more attractive in the eyes of investors and this could lead to an epic recovery in 2024.

In fact, this recovery has already started and rates have not even been cut yet so that gives you a good preview of what's to come in 2024:

Opportunities Remain Abundant

Even after this recent rally, REIT valuations are still historically low relative to other stocks. The S&P 500 ( SPY ) is now back near its all-time-highs, but REITs are still down nearly 30% on average because all that extra capital is hiding in money market funds:

Moreover, that's just the average of the REIT sector, which is dominated by mega-cap investment-grade rated companies. If you look at smaller and lesser-known REITs that aren't included in major indexes, many of them are down by close to 50%.

Here are a few examples that we expect to enjoy significant upside in 2024:

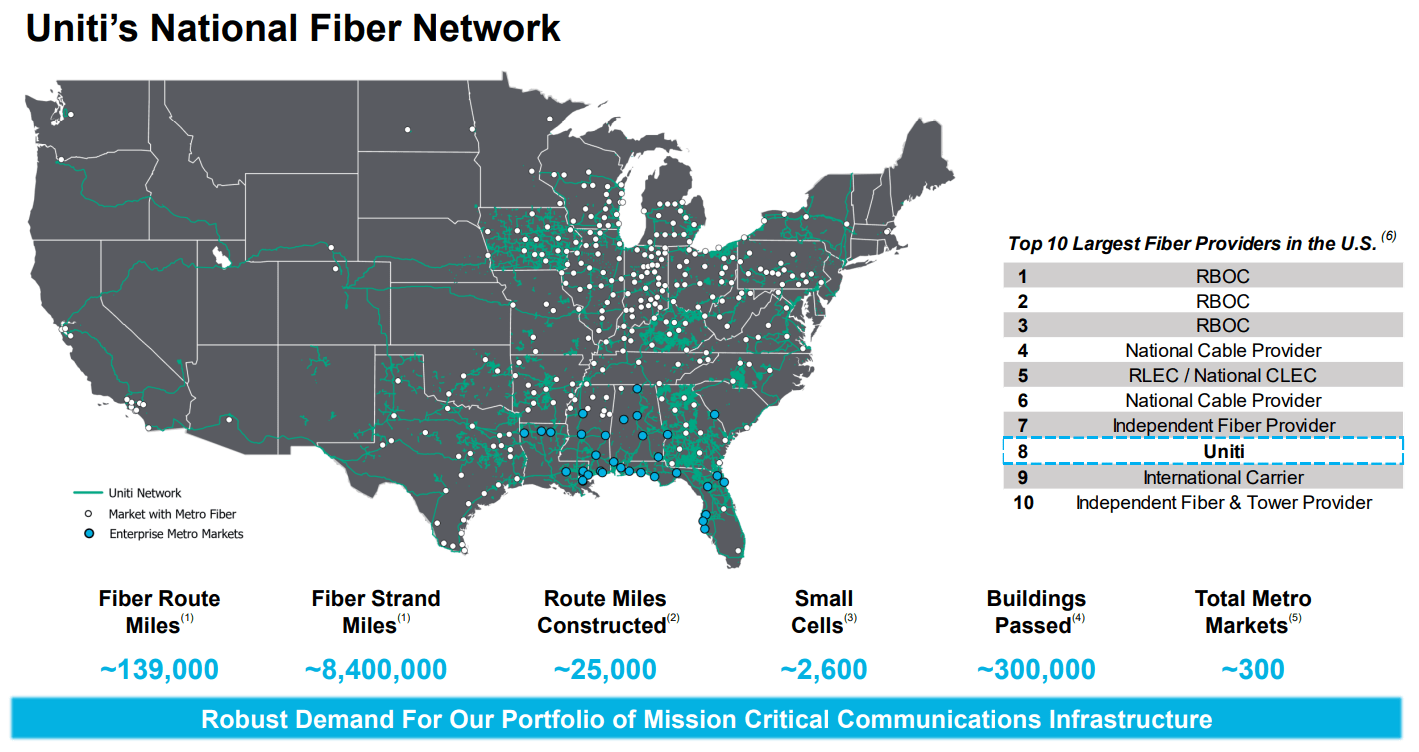

Uniti Group ( UNIT ): UNIT is a small-cap infrastructure REIT that owns a vast portfolio of fiber networks. It enjoys long leases and earns steady and predictable cash flow. But despite that, it is down 50% over the past 3 years and currently trades at just 4x its cash flow, an estimated 50% discount to its net asset value, and offers a 10.4% dividend yield. The CEO of the company recently also bought over $1 million worth of stock after repetitively saying in 2023 that their stock was deeply undervalued. But there are risks. UNIT has dropped more than most other REITs because it is heavily leveraged and its biggest tenant is a private company with shacky financials. But this also means that a drop in interest rates should have a bigger positive impact on UNIT in 2024, potentially leading to significant upside. While you wait, you earn a high dividend yield and the company is also deleveraging its balance sheet to create value for shareholders.

{kind=link}

Clipper Realty ( CLPR ): CLPR is one of the smallest REITs that specializes in apartment communities. It is down over 50% off its highs and as a result, it is today priced at a big 50% discount to its net asset value and offers a 7% dividend yield. It uses more leverage than the bigger apartment REITs and this is a cause of concern for investors, but the leverage remains reasonable and importantly, the company has no major debt maturities until 2028. It owns mainly properties in Manhattan and Brooklyn, which enjoy significant barriers to entry due to the unavailability of land for new developments. The management is also the biggest shareholder of the company so the value of their equity is far greater than their salaries. In a future recovery, the stock could easily rise by 50%+ as it returns closer to its net asset value.

Clipper Realty

Armada Hoffler ( AHH ): AHH is a diversified small-cap REIT that focuses on rapidly growing sunbelt markets and generates most of its revenue from defensive properties such as new-built apartment communities and service-oriented mixed-use retail properties. Its rents have been growing steadily, but its stock is still down 30%, and as a result, the management recently began buying back shares to take advantage of this disconnect between its share price and its fundamentals. The stock is currently priced at 10x cash flow and they pay a 6.3% dividend yield, which leaves plenty of cash flow to reinvest in growth and buybacks. We estimate that the share price is about 30% below its net asset value, offering significant upside potential in a future recovery.

Armada Hoffler

Closing Note

REITs were shunned for most of 2022/2023 due to rising interest rates and a lot of that capital ended up going into money market funds.

But all of that is about to reverse in 2024.

Right now, valuations are still discounted and opportunities are abundant in the REIT sector, but the window of opportunity is closing rapidly.

For further details see:

REIT Opportunities Remain Abundant: 3 Top Picks