AFCG - REITs Rip As Fed Blinks

2023-12-17 09:00:00 ET

Summary

- U.S. equity markets advanced for a seventh-straight week while benchmark interest rates plunged after the Federal Reserve effectively confirmed that it's concluded its historically aggressive rate hiking cycle.

- Extending its weekly winning streak to the longest since 2017 and lifting the benchmark to within 2% of record highs, the S&P 500 posted gains of 2.0% on the week.

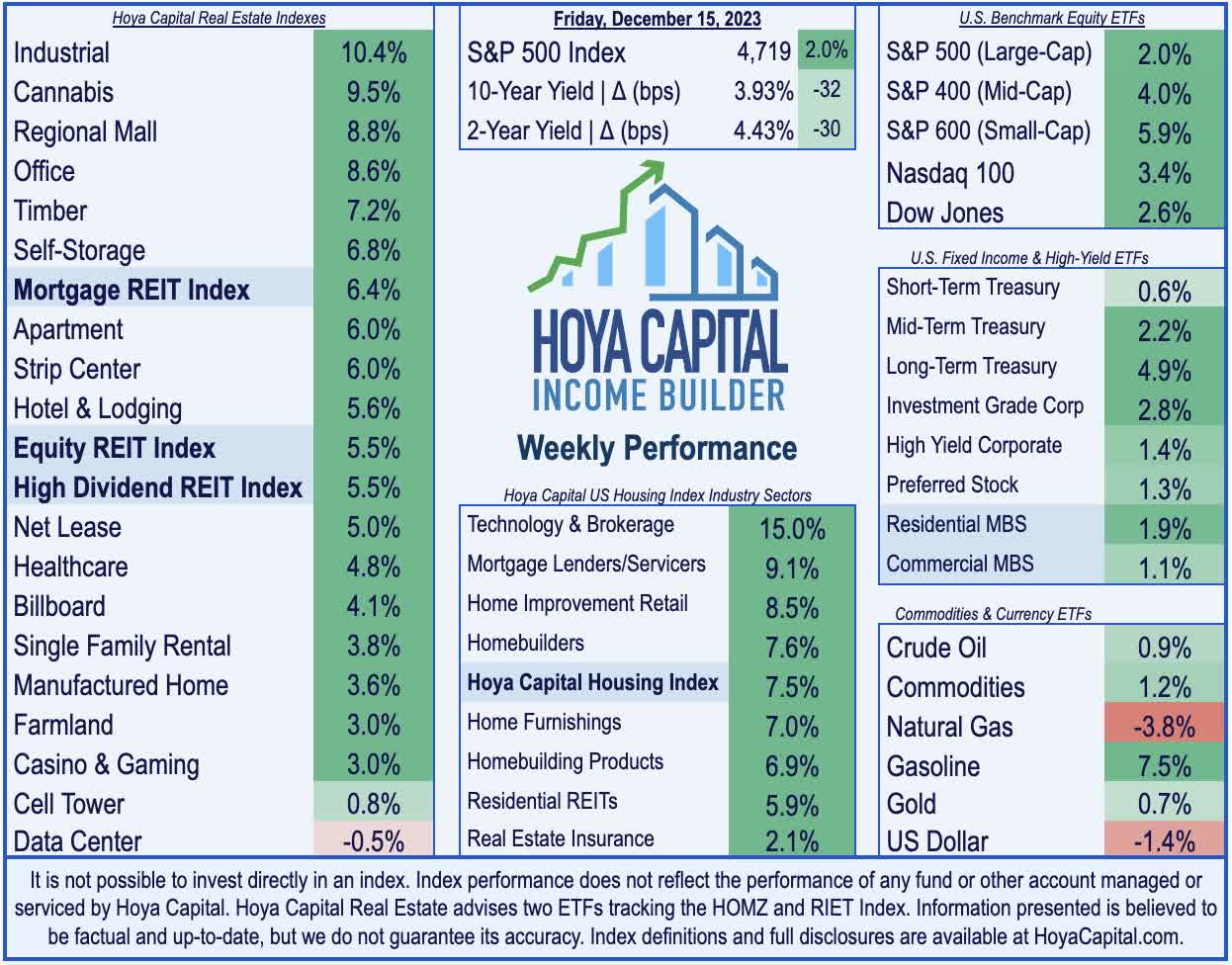

- Real estate equities - the sector that bore the brunt of the Fed's aggressive tightening over the past eighteen months - extended their resurgence this week. The Equity REIT Index gained 5.5%.

- Not to be overlooked amid the focus on the Fed, a critical slate of inflation data this week showed a continued easing of inflationary pressures, as two closely-watched inflation metrics - CPI ex-Shelter and Core PPI - each dipped below the central bank's 2% inflation objective.

- Another week, another wave of REIT dividend hikes and special dividends. Seven REITs hiked their dividend this week - lifting the full-year total above 80 - while three REITs declared special dividends.

Real Estate Weekly Outlook

U.S. equity markets advanced for a seventh-straight week while benchmark interest rates plunged after the Federal Reserve effectively confirmed that it's concluded its historically aggressive rate hiking cycle - yielding to the recent market rebound - and signaled a pivot towards rate cuts by mid-2024. Certainly not to be overlooked amid the focus on the Fed, a critical slate of inflation data this week showed a continued easing of inflationary pressures, as two closely-watched inflation metrics - CPI ex-Shelter and Core PPI - each dipped below the central bank's 2% inflation objective.

{kind=link}

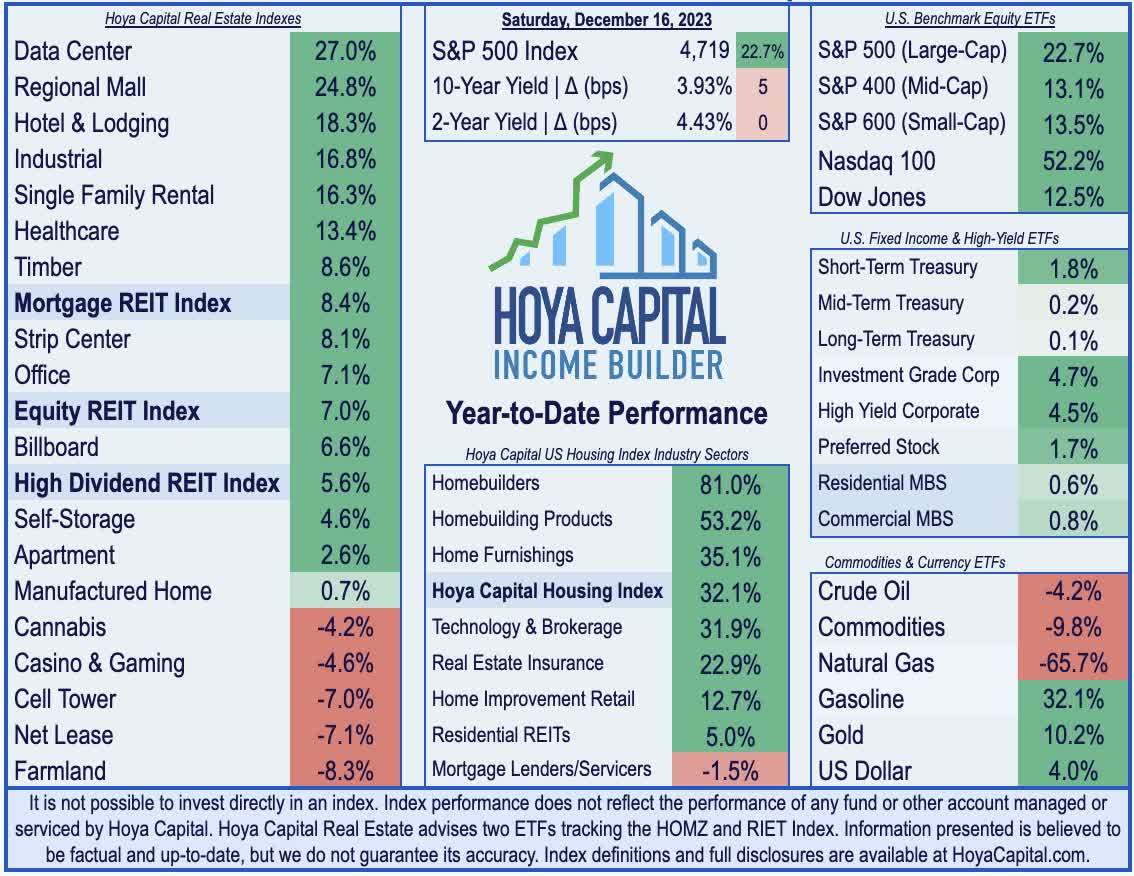

Extending its weekly winning streak to the longest since 2017 and lifting the benchmark to within 2% of record highs, the S&P 500 posted gains of 2.0% on the week while the Dow Jones Industrial Average and Nasdaq 100 each closed the week at fresh record-highs with gains of roughly 3% each. The Mid-Cap 400 and Small-Cap 600 - which lagged their large-cap peers throughout the rate-hiking cycle - led the gains again this week with gains of 4% and 6%, respectively. Real estate equities - the sector that bore the brunt of the Fed's aggressive tightening over the past eighteen months - extended their resurgence this week. Extending their seven-week rebound to nearly 25%, the Equity REIT Index rallied 5.5% this week, with 17-of-18 property sectors in positive territory, while the Mortgage REIT Index gained 6.4%. Homebuilders and the broader Hoya Capital Housing Index rallied more than 7.5% this week as mortgage rates continued to moderate from three-decade highs, dipping below 7% for the first time since August.

{kind=link}

Bonds markets continued their rebound as benchmark interest rates remained in free-fall, taking a fresh leg lower this week after the release of updated FOMC "dot plots," showing a decisive pivot towards rate cuts in 2024. Subsequent remarks from Fed Chair Powell were also distinctly more 'dovish' than recent commentary, conceding that rate cuts are beginning to "come into view" and are “clearly a topic of discussion." Swaps market now imply a 70% probability that the Federal Reserve will cut rates for the first time in March - up from 45% in the prior week - and imply six quarter-point rate cuts by the end of 2024 to a 4.0% upper bound. The 10-Year Treasury Yield dipped 32 basis points this week to 3.93% - the lowest level since July - while the policy-sensitive 2-Year Treasury Yield also dipped 30 basis points to 4.43%. Narrowly snapping an eight-week skid, WTI Crude Oil prices finished higher by about 1% this week but remain 25% below their recent highs in late September. Natural Gas prices dipped another 4% this week, however, extending their year-to-date decline to over 65%. All eleven GICS equity sectors finished higher on the week, led on the upside by Real Estate ( XLRE ) stocks.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

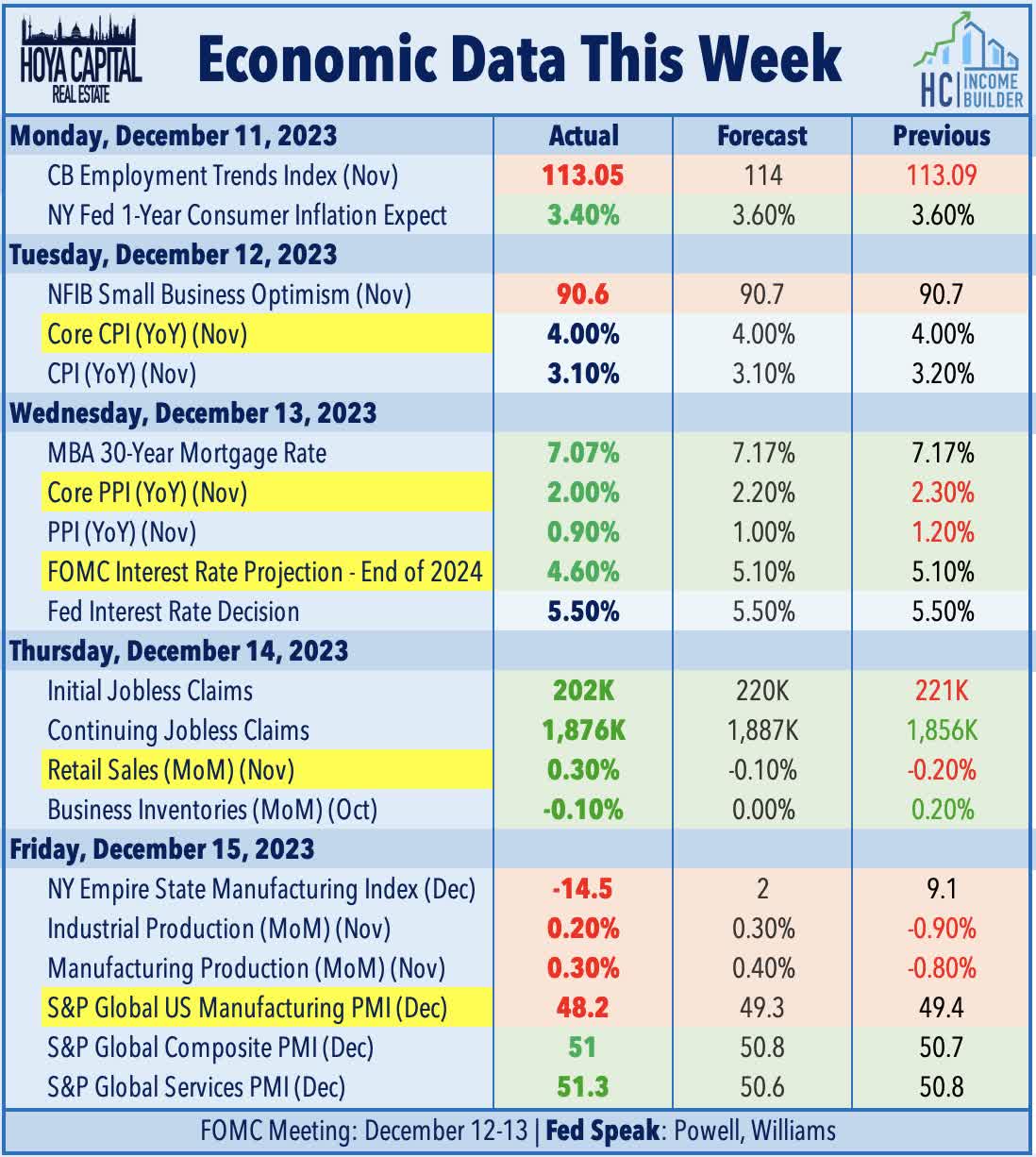

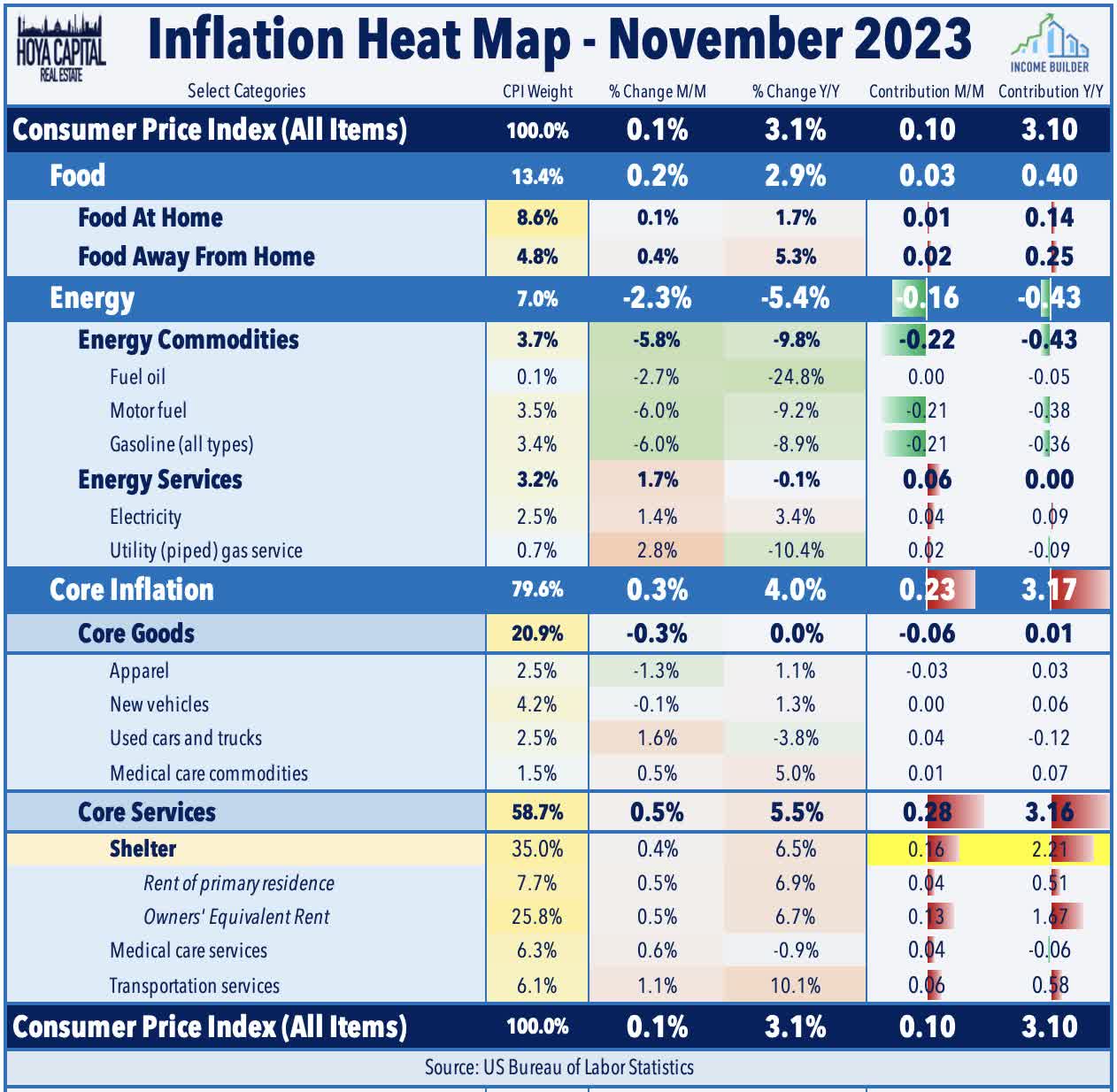

All eyes were on the Consumer Price Index report this week, which showed a continued cooldown of inflationary pressures in November following a three-month reacceleration from June through September driven primarily by resurgent energy prices - the key "swing" inflation input. Headline CPI increased 0.1% month-over-month and increased by 3.14% from a year ago - marginally above consensus estimates of 0.0% and 3.1%, respectively. Core CPI - which excludes food and energy - rose 0.3% on the month and 4.0% on the year, which was exactly in line with expectations. The CPI-ex-Shelter Index - the metric we watch most closely given the substantial lags in the BLS' shelter inflation metrics - declined 0.5% during the month to pull its year-over-year increase back down to 1.4% - remaining below the Fed's stated 2% inflation objective. The BLS continues to show a 6.5% year-over-year increase in shelter inflation - down from the 8.2% peak in March - but still substantially overstating the "real-time" shelter inflation, which we estimate at 1-2%.

{kind=link}

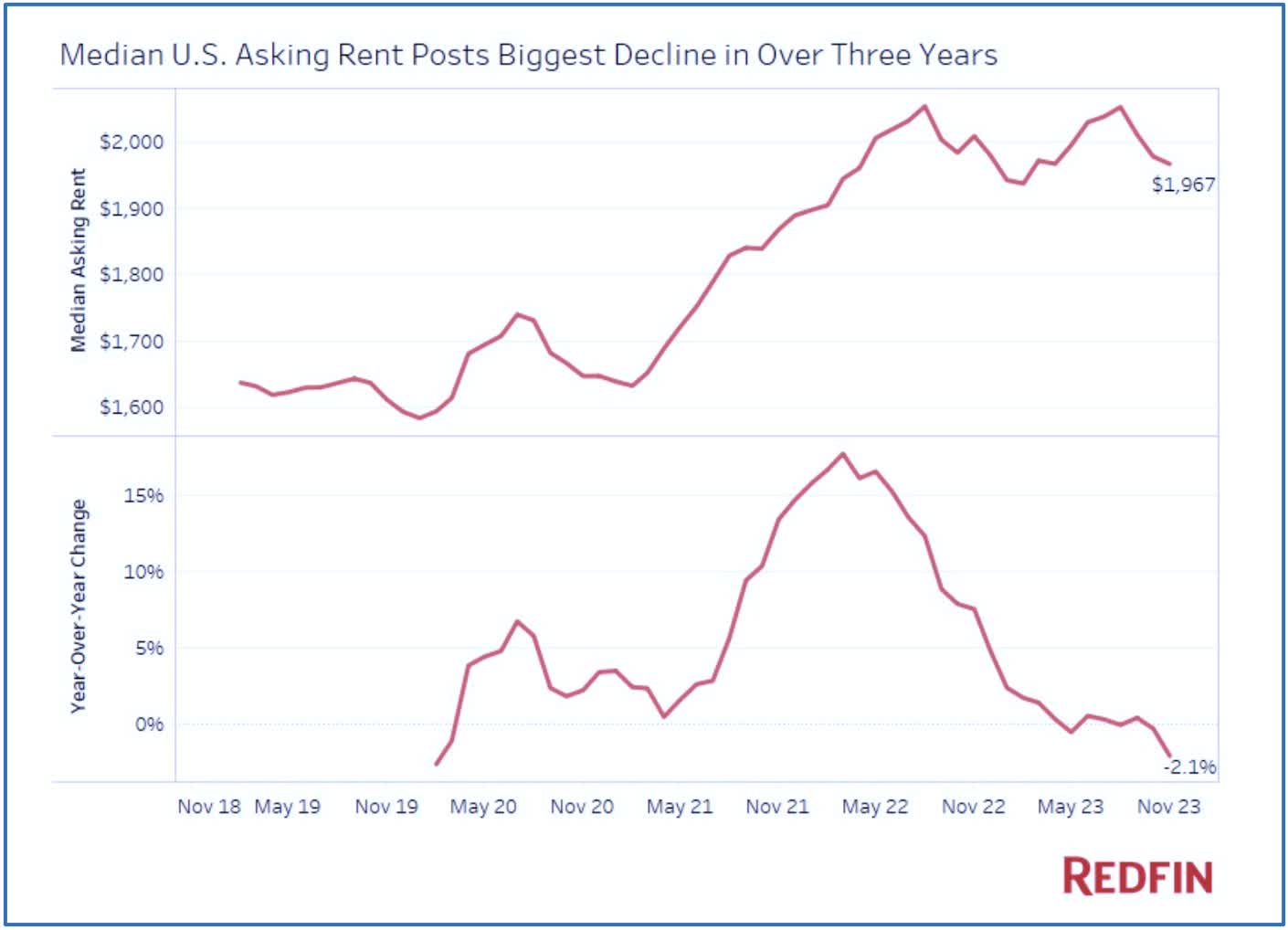

Notably, this overstated shelter component accounted for nearly 70% of the Core CPI increase this month. As we've discussed at length, the multitude of non-government data sources have shown a far more modest - or negative - pace of shelter inflation over the past year, which will trickle into the CPI data in 2024. Residential brokerage firm Redfin ( RDFN ) released its November rent report this week, showing that median U.S. asking rent declined 2.1% year over year in November. RealPage published its monthly Apartment Report last week, which noted that effective asking rents were essentially flat on a year-over-year basis in November, continuing a trend of moderation from the record-setting double-digit increases seen at the peak in early 2022. Apartment List reported that rent growth was -1.1% lower year-over-year in December, which was the fifth-straight month of negative rent growth but slightly above the bottom of -1.5% in October. Realtor reported that annual rent growth was down -0.5% last month - the sixth month of negative growth. Zillow data - which includes single-family rentals as well - shows slightly more buoyant trends, with rent growth of 3.5% in October.

{kind=link}

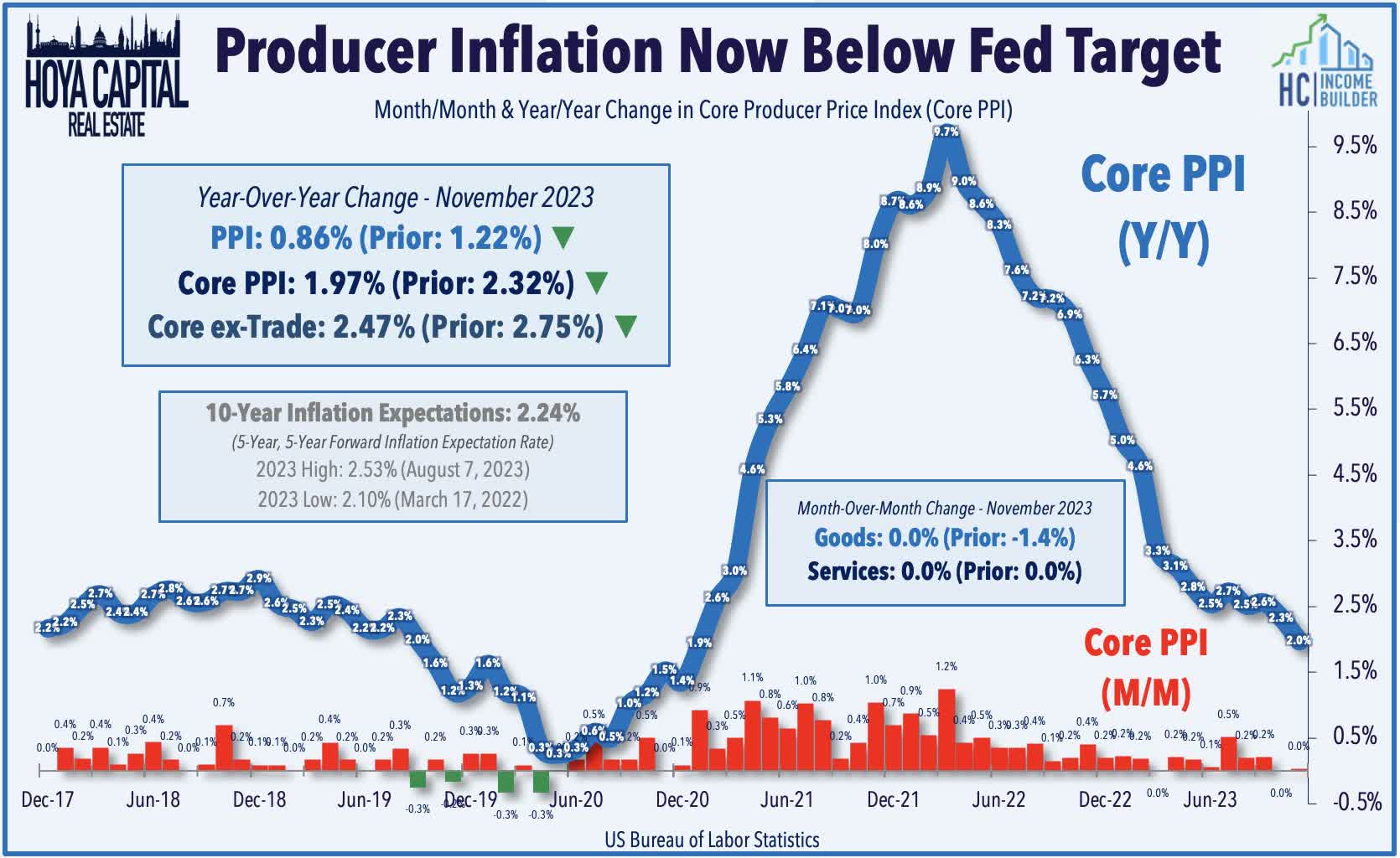

Following the cooler-than-expected Consumer Price Index report, the Producer Price Index data later in the week showed an even sharper moderation of price pressures. The Headline PPI was flat in November - below the 0.1% increase expected - which, combined with revisions to prior months, dragged the annual increase to just 0.86%. Core PPI - which excludes food and energy - was also flat on the month, which dragged its year-over-year increase to below 2% for the first time since February 2021. As with the CPI report, lower oil and natural gas prices are driving the disinflation. Of note, the Services index - which had been an area of "sticky" inflationary trends - was flat for a second straight month, pulling the annual increase down to 2.1%, down sharply from the peak of 5.3% at the start of this year. Survey data over the past two weeks has also shown a sharp decline in consumer inflation expectations. The New York Fed's Consumer Expectation survey released this week showed that short-term inflation expectations fell to two-year lows, while the University of Michigan's Consumer Confidence survey last week showed an even sharper decline in consumer inflation expectations.

{kind=link}

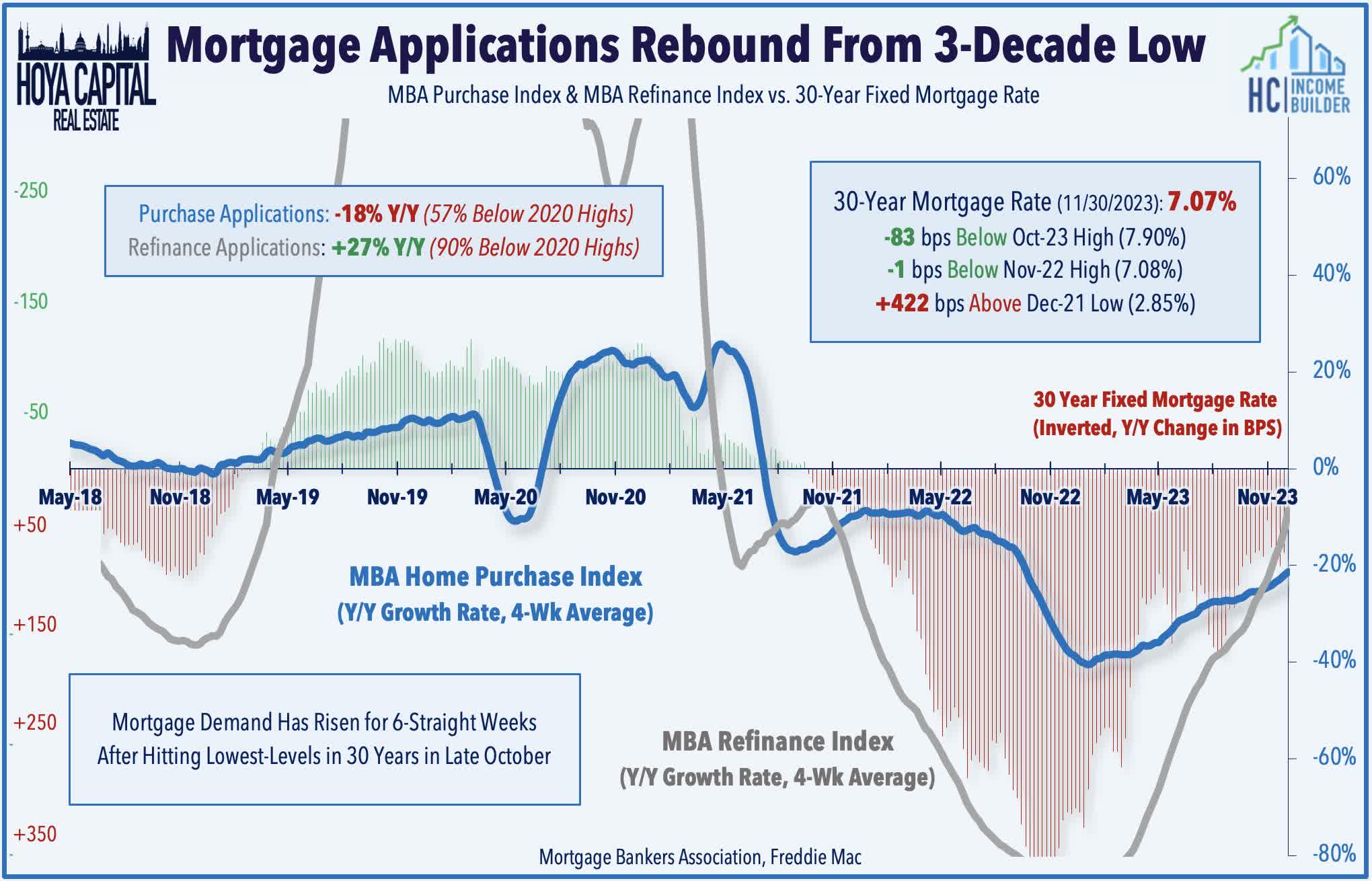

Elsewhere on the economic data front, the Mortgage Bankers Association reported this week that mortgage application volumes - a forward indicator of home sales and broader housing market activity - rose for a sixth-straight week since hitting three-decade lows in October. MBA’s Chief Economist noted, “Borrowers who had seen rates near 8% earlier this fall are now seeing some lenders quote rates below 7%. Refinance volume picked up in response to this drop in rates, but Purchase volume was running about 18% below last year as prospective homebuyers are still challenged by a lack of inventory, even if rates have decreased.” Led by the resurgent single-family homebuilders, the Hoya Capital Housing Index has now gained more than 30% from the lows in late October. Toll Brothers ( TOL ) - which we own in the Dividend Growth Portfolio - soared over 10% this week after it announced a new 20M share buyback program. TOL has already repurchased 13.3M shares - 12% of shares outstanding - over the preceding eighteen months at an average purchase price of $60.15 - a bargain relative to its current price above $105/share.

{kind=link}

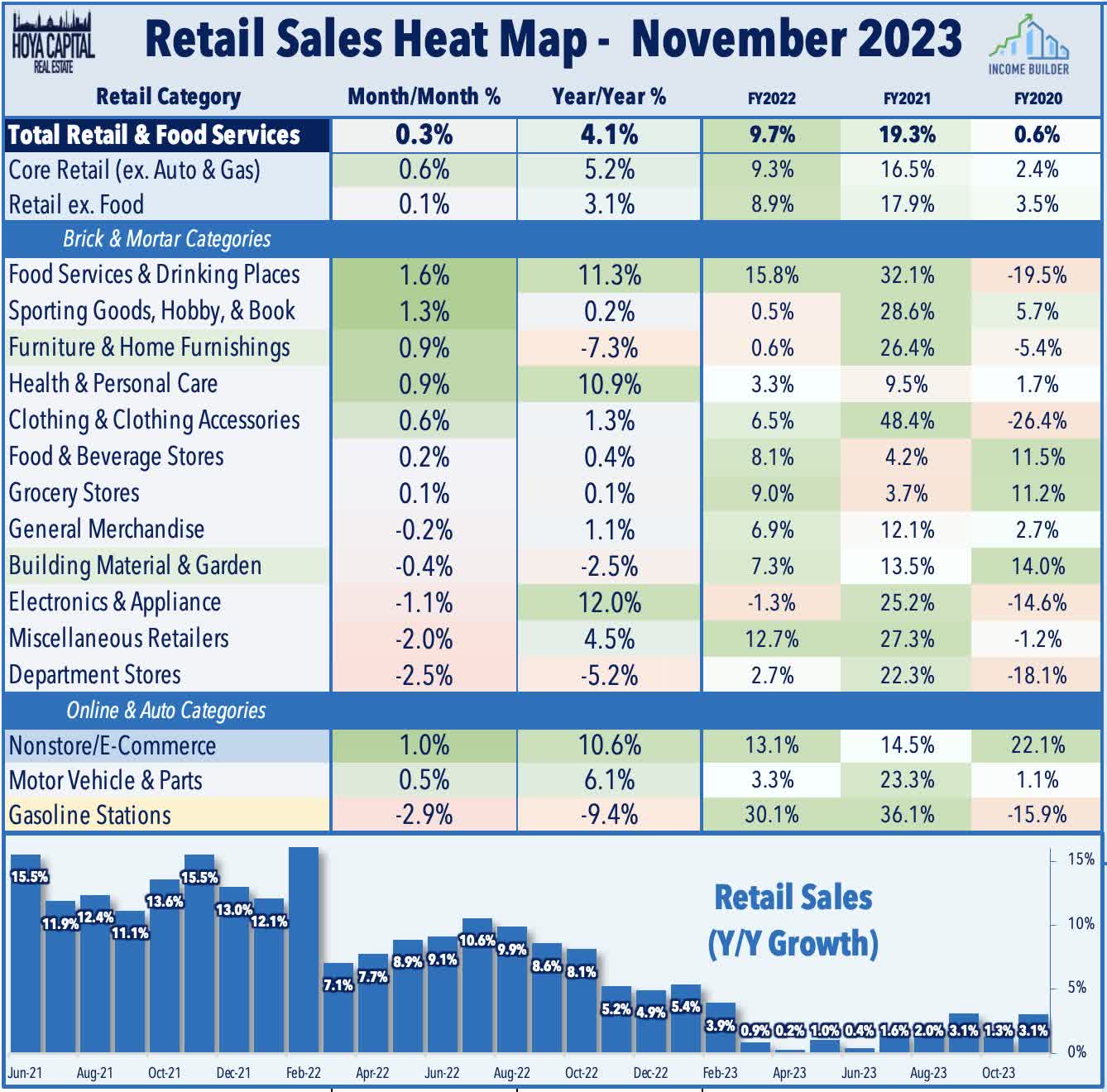

A key look into the health and sentiment of the U.S. consumer, retail sales data this week showed an encouraging start to the critical holiday season for retailers. Total retail sales increased 0.3% in November compared to the prior month and 4.1% from last year - well above the 0.1% forecasted month-over-month decline - but October data was revised marginally lower. Excluding gasoline stations - in which the retreat in gas prices resulted in a 2.9% dip in November - Core Retail sales were even stronger, rising 0.6% during the month and 5.2% from last year. Spending strength was relatively broad-based, with 8 of 13 categories posting sequential monthly increases, led by restaurants and bars, as well as sporting goods stores and online retailers. Furniture retailers also reported a rebound in sales in November amid an otherwise challenging year for housing-related retailers. There were pockets of weakness, however, as department-store sales declined 2.5% - the most since March.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

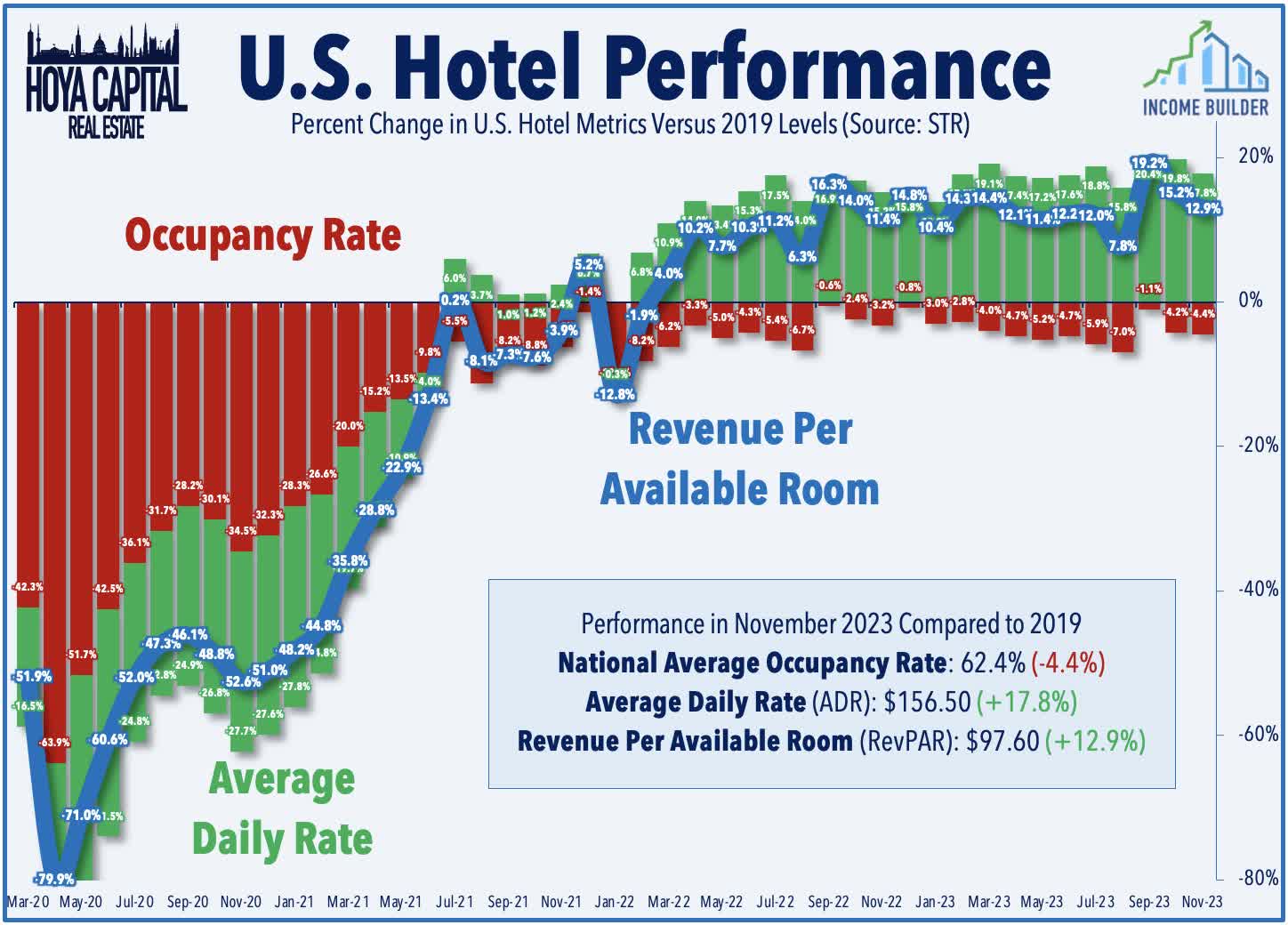

Hotels : Another week, another wave of REIT dividend hikes and special dividends. Host Hotels ( HST ) - which we own in the Dividend Growth Portfolio - rallied 6% this week after it hiked its quarterly dividend for the fourth time this year to $0.20/share (4.1% dividend yield) - an 11% increase from last quarter and up 70% from last year. Host Hotels becomes the first hotel REIT to fully restore its dividend to pre-pandemic 2019 levels. HST also declared a special dividend of $0.25/share, becoming the fifth REIT to declare a supplemental dividend this week. Host also received a credit rating upgrade from Fitch, which upped its rating to “BBB” from “BBB-“ with a stable outlook. The TSA announced earlier this month that the U.S. saw the busiest day for air travel ever during the Thanksgiving weekend, with more than 2.9 million people screened at checkpoints. Recent checkpoint data shows that throughput climbed to over 105% of 2019 levels during November - the highest since the pandemic - but has moderated a bit in early December to 101% of 2019-levels. Hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was 13% above 2019 levels in November, as a roughly 18% relative increase in Average Daily Room Rates ("ADR") offset a roughly 4% relative drag in average occupancy rates.

{kind=link}

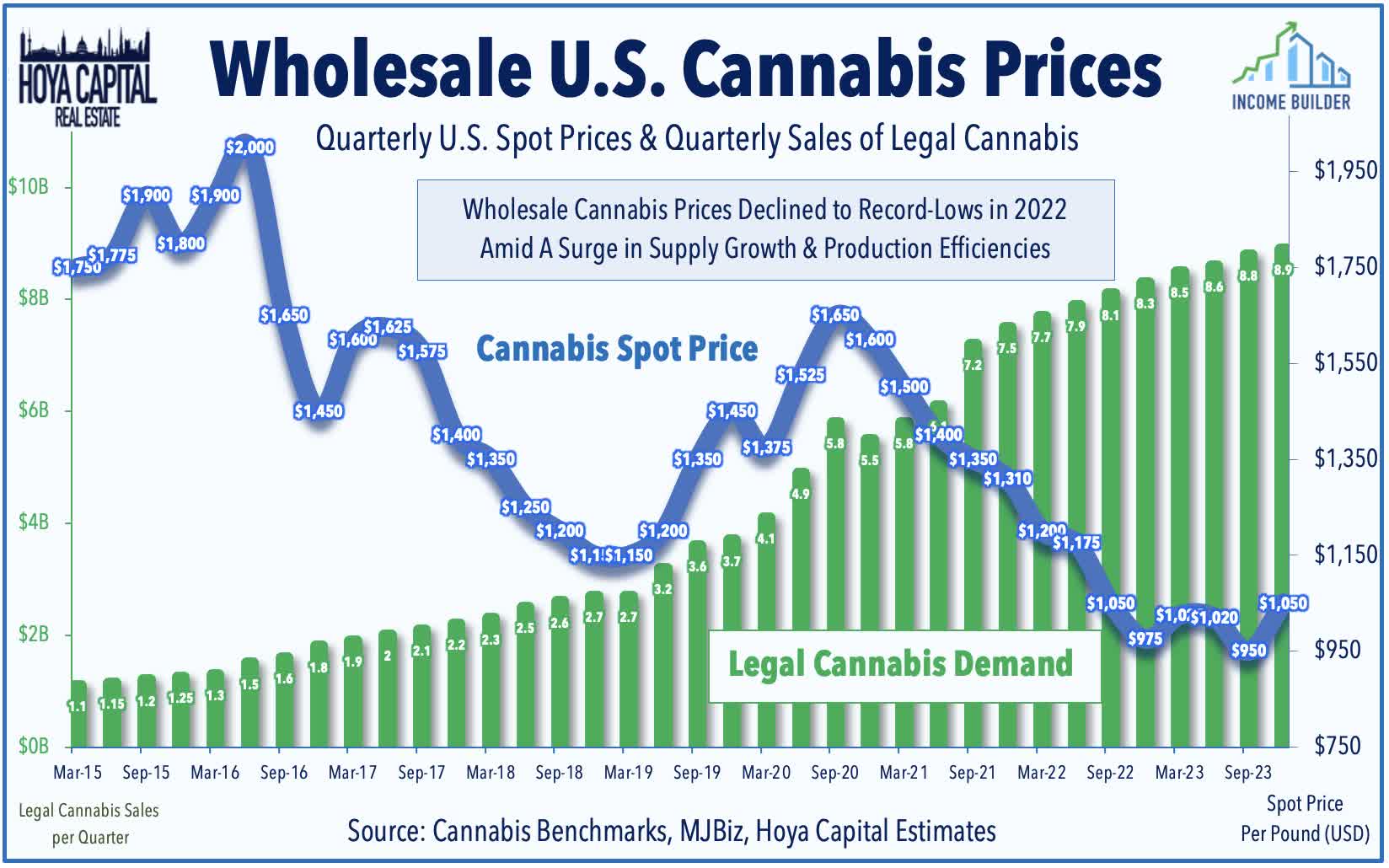

Cannabis : We also saw a pair of dividend hikes from cannabis REITs - which have been the second-best performing property sector during this seven-week rally behind the suddenly resurgent office REIT sector. Innovative Industrial ( IIPR ) - the largest cannabis REIT - surged 12% this week after it raised its quarterly dividend by 1% to $1.82/share (7.4% dividend yield). IIPR has now rebounded by over 40% since late October. NewLake Capital ( OTCQX:NLCP ) - the second-largest cannabis REIT - gained 4% this week after it hiked its quarterly dividend by 3% to $0.40/share (10.9% dividend yield). AFC Gamma ( AFCG ) - the largest cannabis mortgage REIT - held its dividend steady at $0.48/share (15.8% dividend yield) after having reduced it earlier this year. Cannabis REITs have been under pressure since mid-2022 amid concern over defaults from their cannabis cultivator tenants, which have been smoked by plunging wholesale cannabis prices and setbacks on federal legalization. Concerns over rent collection and loan performance have been mounting over the past two years as publicly traded tenants of these cannabis REITs posted share price declines between 60-90% before the recent rebound.

{kind=link}

Elsewhere, net lease REIT Realty Income ( O ) rallied over 6% this week after it hiked its monthly dividend for the fourth time this year to $0.2565/share (5.7% dividend yield). Cell tower REIT American Tower ( AMT ) gained 3% this week after it hiked its quarterly dividend for the third time this year to $1.70/share (3.2% dividend yield) - a 5% increase from last quarter and a 9% increase from last year. Diversified REIT Alexander & Baldwin ( ALEX ) - which focuses exclusively on the Hawai'i market - rallied over 5% this week after it hiked its quarterly dividend by 1% to $0.2225/share (5.1% dividend yield). ALEX owns 3.9 million square feet of commercial space in Hawai'i, including 22 retail centers, 13 industrial assets, and four office properties. Two REITs declared special dividends this week as well. Farmland Partners ( FPI ) declared a special supplemental dividend of $0.21/share (in addition to its $0.06/share quarterly dividend). Strip center REIT SITE Centers ( SITC ) declared a supplemental cash special dividend of $0.16/resulting from 2023 transaction activity. We've now seen 80 REITs raise their dividend this year (including the handful of special dividends), while 30 REITs have lowered their payouts. In our State of the REIT Nation report last week, we noted that FFO growth has significantly outpaced dividend growth since the start of the pandemic, which has resulted in a REIT dividend payout ratio of just 66% in Q3 - below the 20-year average of 80%.

{kind=link}

Apartment : Sunbelt-focused Mid-America Apartment ( MAA ) - which we own in the Dividend Growth Portfolio - rallied nearly 6% this week after it hiked its quarterly dividend by 5% to $1.47/share - the 14th consecutive year MAA has increased its dividend. Expanding on the discussion above, residential brokerage firm Redfin ( RDFN ) released its November rent this week, which showed that median U.S. asking rent declined 2.1% year over year in November to $1,967—the biggest annual drop since February 2020. While rents are dropping, they’re still 22.1% higher than they were in November 2019 before the pandemic. Redfin also noted that the number of completed apartments in the U.S. rose 7% year over year in the third quarter to a seasonally adjusted annual rate of 1.2 million - one of the highest levels of the last three decades - and because renters have an increasing number of buildings to choose from, vacancies are climbing. The rental vacancy rate rose to 6.6% in the third quarter, the highest level since the first quarter of 2021. Redfin notes that "while there are a lot of apartments hitting the market, there aren’t as many single-family homes for rent" and predicts that SF rents will rise in 2024 because they’re "particularly attractive to millennials, many of whom desire homes large enough for their growing families."

{kind=link}

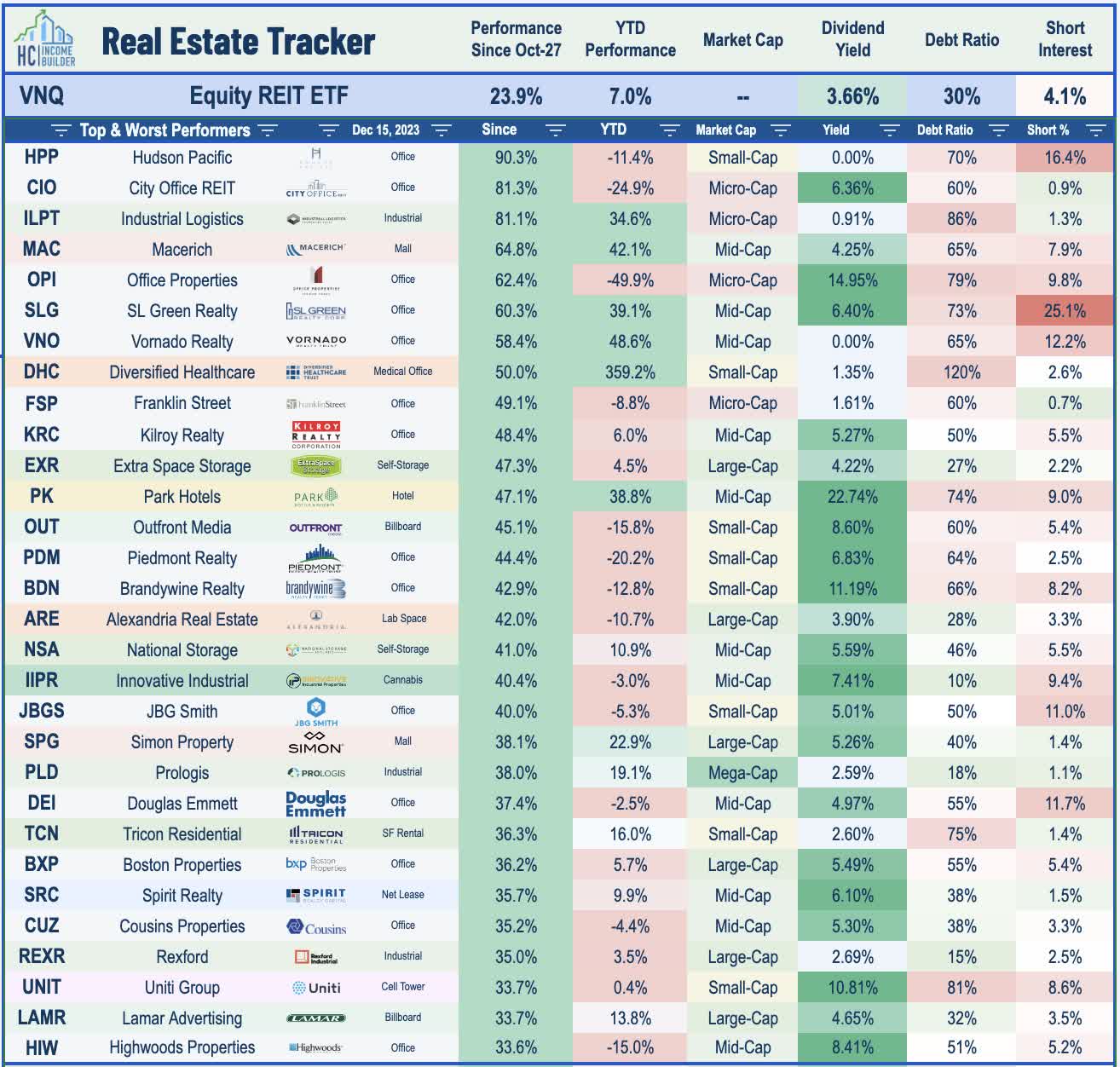

Office : The battered office sector has been the top-performing property sector during the powerful REIT rebound since late October with average gains of roughly 40%, and was again among the leaders this week on further indication that office leasing demand has picked up some momentum in recent months. Among the most notable moves since the lows on October 27, West Coast-focused Hudson Pacific ( HPP ) has surged over 90%, while Sunbelt-focused City Office ( CIO ) has surged more than 80%. Following similar leasing announcements from a handful of office REITs over the past two weeks, lab space owner Alexandria Real Estate ( ARE ) rallied another 9% this week to push its seven-week gains to over 40% after announcing a pair of large lease signings. ARE signed a 165k square foot lease to Novo Nordisk at its under-development Boston campus which is expected to deliver in 2025. ARE also signed a 100k square foot lease to CARGO Therapeutics at its San Carlos mega campus in the San Francisco Bay Area. Elsewhere, Kilroy Realty ( KRC ) advanced 7% after it hired a new CEO following the retirement of its current CEO John Kilroy. The current CFO of strip center REIT Brixmor Property ( BRX ) - Angela Aman - will take the reigns beginning in 2024.

{kind=link}

Office : JBG SMITH ( JBGS ) - a diversified REIT focused on the Washington DC metro market - soared more than 15% this week after it announced that it plans to partner with Monumental Sports & Entertainment - owner of the Washington Wizards and Washington Capitals - to develop the Potomac Yard section of National Landing site in Alexandria, Virginia into a mixed-use development including a new 20,000 seat arena for the two DC sports franchises, a surprising relocation that comes after failed negotiation between Monumental and the DC government to keep the teams at their current home in Downtown DC. The preliminary development plan calls for the arena to be constructed on a currently unoccupied 12-acre site situated between the Metro entrance and the first phase of the Virginia Tech Innovation Campus. The site is owned by JBG Smith and its joint venture partner and will be sold to a proposed Virginia Authority. JBG Smith will serve as the developer for the corporate MSE headquarters, arena, media studio, performing arts venue, and esports facility. The planned project also calls for significant joint infrastructure investment by the Commonwealth, the City, Monumental, and JBGS. JBGS serves as the master developer of approximately 55 acres surrounding the project, with a total potential density of approximately 8.1 million square feet, of which JBG SMITH owns approximately 1.5 million square feet of density. JBGS is already developing 2.1 million square feet of space for Amazon in the development and has 1,583 multifamily units under construction

{kind=link}

Mall : Small-cap mall owner Pennsylvania REIT ( OTC:PRET ) - which owns 23 mall properties across eight states - filed for Chapter 11 bankruptcy proceedings for the second time in three years this week, as its portfolio of Class B and C mall properties struggles to remain relevant in the changing retail landscape. PREIT was one of three small-cap mall REITs that filed for bankruptcy early in the pandemic - effectively wiping out existing common stockholders - but was one of two that re-emerged as a public company by early 2021 with a restructured balance sheet that, unfortunately, was comprised heavily of shorter-term variable rate debt which again pushed the firm into default as interest rates soared over the past eighteen months. Despite the strongest fundamental conditions for retail real estate in at least a decade, PREIT's common stockholders will be wiped out once again in a pre-packaged restructuring plan supported by 100% of its first and second lien lenders. PREIT has received commitments for new money debtor-in-possession and exit-revolver financing in an aggregate amount of roughly $135 million from a diverse group of investors led by Redwood Capital Management and Nut Tree Capital Management which plan will "reduce its total indebtedness by approximately $880 million."

{kind=link}

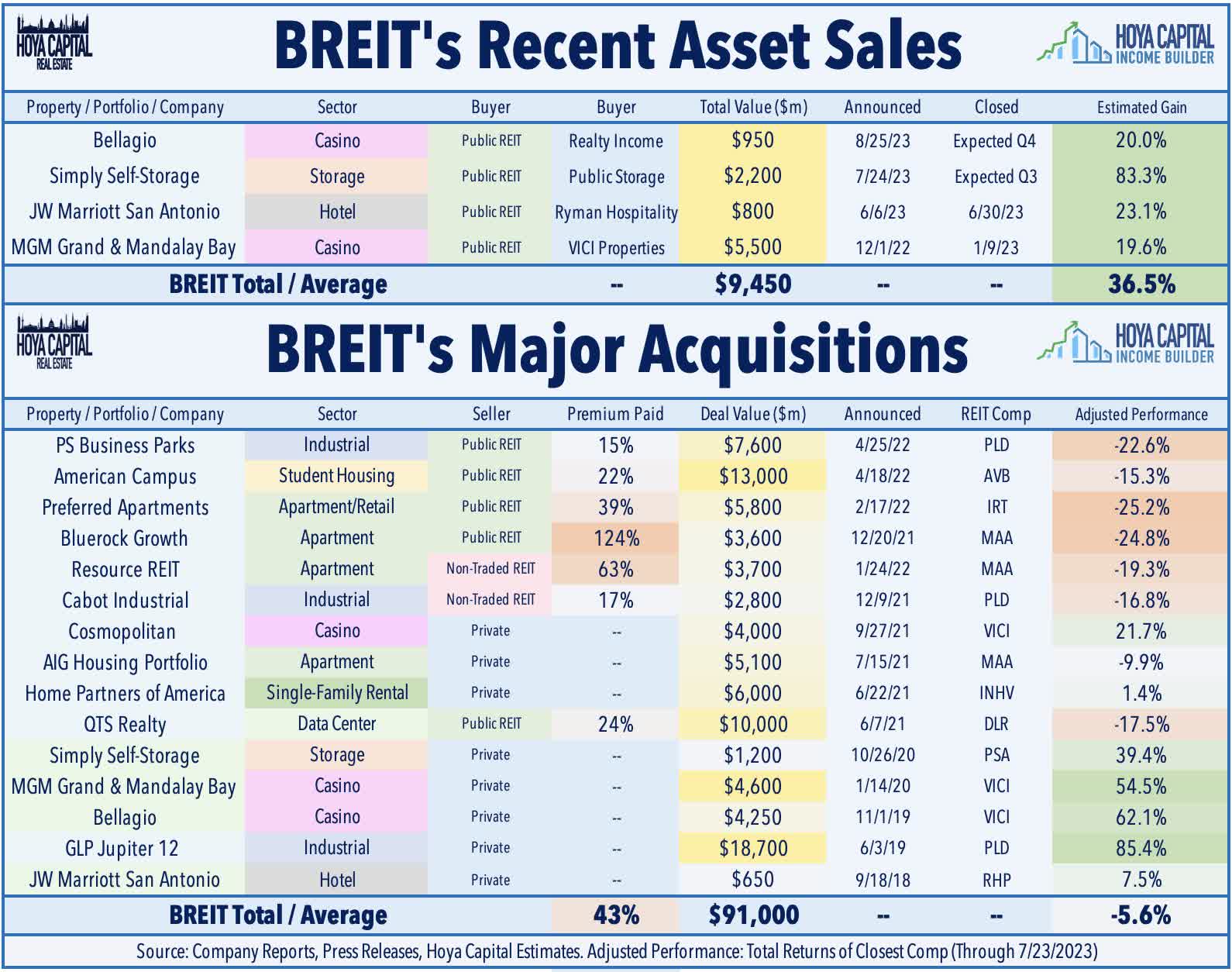

On a related note, asset manager Blackstone ( BX ) was in focus again this week after it announced that two of its funds - Real Estate Debt Strategies and its Real Estate Income Trust ("BREIT") - paid $1.2 billion to acquire a 20% stake in a portfolio of commercial property loans from Signature Bank - which abruptly collapsed earlier this year - alongside two other joint venture partners. The funds will invest alongside two other JV partners - Canada Pension Plan Investment Board and Rialto Capital - while the FDIC will control the remaining 80% share. The portfolio consists of roughly 2,600 first-mortgage loans on retail, market-rate multifamily, and office properties located primarily in the New York metropolitan area. Roughly 90 percent of the loans are fixed rate with low in-place coupons and "strong in-place debt service coverage." The FDIC also said it will provide financing equal to 50% of the venture’s value. For BREIT - BX's non-traded REIT platform - the deal comes despite the fund's continuing limit on investor redemptions. BREIT announced earlier this month week it limited redemptions for the 13th straight month in November, exercising its cap at 2% of NAV in any month and 5% of NAV in a calendar quarter. After scooping up over $50B in assets from 2020-2022 - primarily by acquiring public equity REITs - BREIT has sold more than $10B in properties this year back to public equity REITs to raise cash to meet redemption requests.

{kind=link}

Mortgage REIT Week In Review

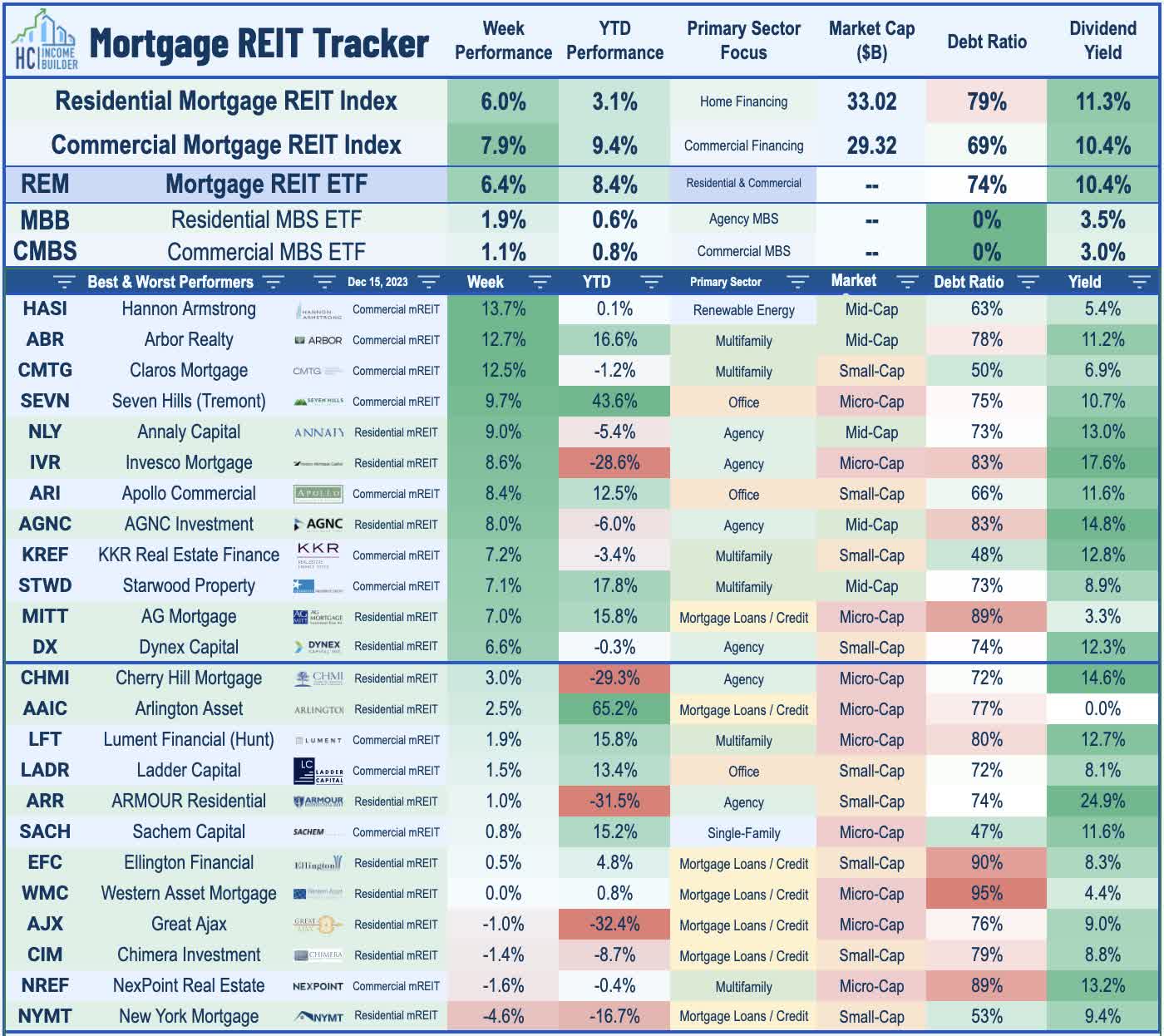

Extending their two-month resurgence amid expectations of a pivot towards less-hawkish monetary policy, Mortgage REITs were again among the leaders this week, with the iShares Mortgage Real Estate Capped ETF ( REM ) surging 6.4% to push their seven-week gains to just shy of 30%. Consistent with the trends seen on the equity REIT side, several of the most heavily shorted REITs posted double-digit gains on the week. Multifamily lender Arbor Realty ( ABR ) - that has been targeted in several short reports over the last year, including one from Viceroy Research last month - surged nearly 13% after it increased its stock buyback program, expanding its authorization to $150M (~5% of its market capitalization). Arbor's stock price has now fully recovered since the publication of a short report in mid-November by Viceroy Research alleging that the company is overvaluing its assets. Renewable energy lender Hannon Armstrong ( HASI ) - which has also been a target of recent short reports - surged nearly 14% after completing $550M in new debt financing last week.

{kind=link}

Elsewhere, Ellington Financial ( EFC ) announced that it completed its acquisition of Arlington Asset and reiterated that the deal is expected to be accretive to earnings in 2024. The deal provides EFC more exposure to the mortgage servicing rights ("MSR") business - an inversely-rate sensitive segment which has been the steadiest area in the mortgage space over the past two years. The agency-backed segment of the mortgage market - which is the most sensitive to interest rates - has been the laggard this year. On the topic of M&A, commercial mREIT Ready Capital ( RC ) - which acquired fellow mREIT Broadmark Realty earlier this year - announced this week that it will "temporarily" reduce its quarterly dividend to 17% to $0.30/share (10.5% dividend yield) - its second reduction this year. Ready Capital commented that the “current dividend is a temporary, short-term reflection of our merger with Broadmark... we remain confident that the merger will start to deliver long-term earnings accretion as we move through next year and beyond.”

{kind=link}

Two additional mREITs also reduced their dividends this week. ARMOUR Residential ( ARR ) confirmed that it plans to reduce its monthly dividend by 40% to $0.24/share (14.8% dividend yield) beginning in January. ARR also noted that its estimated that book value per common share was $21.88 as of December 12th, up about 1% from the end of Q3. New York Mortgage Trust ( NYMT ) reduced its quarterly dividend by 33% to $0.20/share (8.4% dividend yield). As noted in our Earnings Recap, we noted that NYMT alluded to a likely dividend reduction in its earnings call last month. Each of the other dozen mREITs that declared dividends held their payouts steady at current levels, including the two largest commercial mREITs - Blackstone Mortgage ( BXMT ) and Starwood Property Trust ( STWD ) - and two of the largest residential mREITs - AGNC Investment ( AGNC ), and Rithm Capital ( RITM ). The average residential mREIT now pays a dividend yield of 11.8%, while the average commercial mREIT yields 11.0%.

{kind=link}

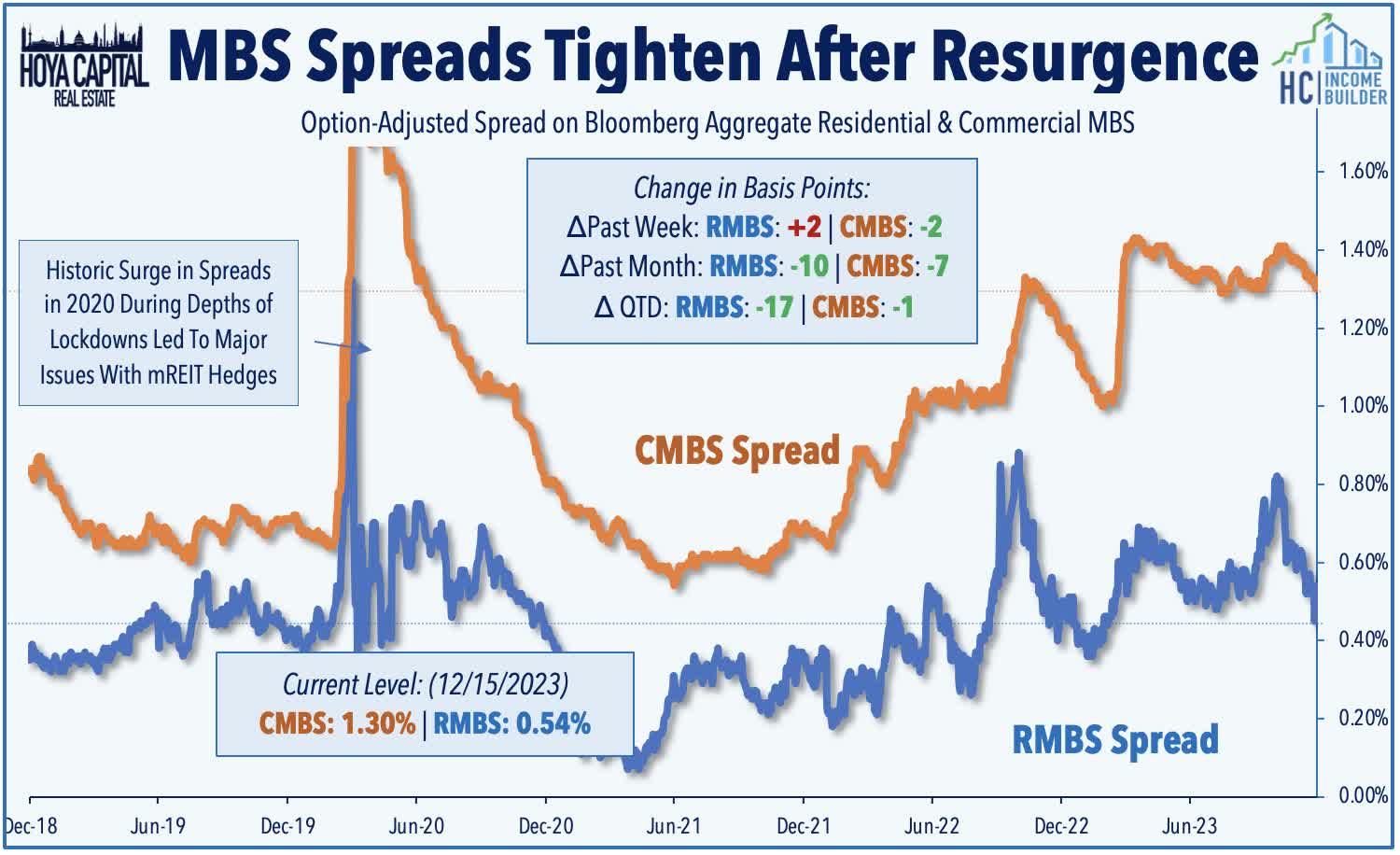

Firming valuations across the battered mortgage-backed security ("MBS") market have certainly helped brighten the outlook for mortgage REITs. The iShares MBS ETF ( MBB ) - an unlevered index tracking residential MBS values - has surged nearly 10% over the past two months, implying a book value increase of between 20-30% for the average residential mREIT during this time. The iShares CMBS ETF ( CMBS ) - which tracks commercial MBS values - has gained about 5% during this time. Before this rebound, both indexes were on pace to post back-to-back years of record-setting declines amid the Fed's historically aggressive interest rate hiking cycle. The retreat in benchmark interest rates has come alongside a modest tightening of credit spreads as well. Since the end of the third quarter, RMBS spreads have tightened by 17 basis points, while CMBS spreads have tightened by 1 basis point. While RMBS spreads have returned to pre-pandemic levels, CMBS spreads have remained considerably above 2019 levels since the start of the Fed's tightening cycle in mid-2022, driven primarily by concern over office defaults.

{kind=link}

2023 Performance Recap & 2022 Review

With just two weeks left in 2023, the Equity REIT Index is now higher by 7.0% on a price return basis for the year (10.5% on a total return basis), while the Mortgage REIT Index is higher by 8.4% (+17.4% on a total return basis). This compares with the 22.7% gain on the S&P 500 and the 13.1% gain for the S&P Mid-Cap 400 . Within the real estate sector, thirteen property sectors are now in positive territory on the year, led by Data Center, Regional Malls, and Hotel REITs, while Net Lease and Farmland REITs have lagged on the downside. At 3.93%, the 10-Year Treasury Yield has climbed 5 basis points since the start of the year - up from its 2023 intra-day lows of 3.26% in April - but down sharply from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is higher this year, producing total returns of 4.9% thus far. WTI Crude Oil - perhaps the most important "swing" inflation input - is now lower by 4.2% this year, while Natural Gas is lower by over 65% this year.

{kind=link}

Economic Calendar In The Week Ahead

The state of the U.S. housing market will be in focus in the week ahead - the segment that bore the brunt of the Fed's rate hiking cycle. This slate of data could very well represent the "bottom" of the rate-driven downturn, as the housing industry appears poised to finally rebound in 2024 following two years of stagnation. On Monday, we'll see NAHB Homebuilder Sentiment data for December, which is expected to show a rebound in builder optimism following four straight months of declines. On Tuesday, we'll see Housing Starts and Building Permits data for November, which is expected to show a continued moderation in construction activity amid a still-challenging financing environment for both single-family and multi-family development. On Wednesday, we'll see Existing Home Sales data, which is expected to show a slowdown in sales velocity in November to a 3.78M annualized rate, which would be the second slowest month for home sales since 1995. New Home Sales data on Friday is expected to accelerate to a 695k annualized rate, however, as the largest builders have been able to cope with multi-decade-high mortgage rates by leveraging their relatively healthy balance sheet to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market. We'll also be closely watching the PCE Price Index on Friday - the Fed's preferred gauge of inflation - which is expected to show an annual increase of 2.8% - down sharply from the 7.0% rate seen a year ago.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

For further details see:

REITs Rip As Fed Blinks