RNSDF - Renault: Time To Buy More

2023-11-20 02:35:24 ET

Summary

- Positive price mix, 2.5 months order books, and higher FCF make Renault a Buy.

- Without the positive HORSE carve-out effect, Renault expects a Group operating margin in H2 above H1.

- With ongoing competition from Tesla and Chinese OEMs, Renault's electric vehicle sales increased by 22% in Q3, representing 11% of total sales.

- Ampere IPO could unlock additional shareholder value, and we positively view the new Capital Market Day targets.

Here at the Lab, we very much like the automotive segment, especially when volumes are still down (from the pre-COVID-19 level), and fundamentals are here to stay. As our readers know, we upgraded Renault (RNSDF)(RNLSY) to a buy with a publication called ' Turnaround In Progress With Solid Fundamentals ,' and in the last month, the company released its Q3 update, providing supportive news to the investor community as well as a Capital Market Day presented two days ago on Ampere strategic targets . This year, we moved Renault's rating from neutral to buy due to 1) Business Transformation At Full Speed, 2) being Back To Profitable Growth , and 3) Ampere IPO as a positive catalyst to price in.

Q3 results (brief update)

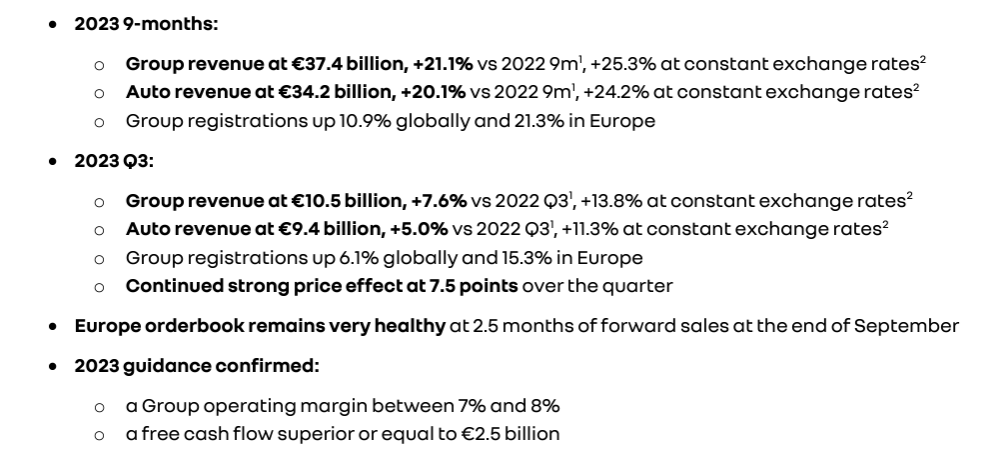

The French Group saw its turnover increase in Q3 after four years of consecutive declines, and looking at the below results, the company confirmed the 2023 outlook and reached positive results in all P&L lines.

Renault Q3 and 9M results in a Snap

{kind=link}

Source: Renault Q3 press release

Our internal team believes that Wall Street and buy-side analysts were pricing higher expectations for the Q3 quarter. However, this year, Renault has already raised twice its guidance. Therefore, our expectations were already set, and we were pricing a cautious forecast. In our last report, we explained that:

We anticipate a flattish H2 volume in line with H1 results. However, we are more optimistic about input costs that should benefit from approximately €500 million relief thanks to an easing of raw material inflationary pressure.

On the positive side, we were forecasting a better price/MIX level with a mid-to-high-single-digit growth, excluding the positive one-off effect recorded in Q2 with the HORSE carveout. In addition, on a negative note, we reported higher ramp-up costs for the company's new models and higher working capital and CAPEX requirements in H2. For the above reason, we forecasted an unchanged automotive FCF of €2.5 billion. This is precisely what has happened, and we are not surprised to be very well aligned with the company's internal estimates.

{kind=link}

Source: Renault Q3 results presentation

Looking at the numbers, in the third quarter, the French car manufacturer increased its top-line sales by 7.6% compared to the same period in 2022. Since the beginning of the year, the company's consolidated revenue growth stands at a plus 21%. The Group sold 511 thousand vehicles (+6.1%), of which almost 357k Renault branded and 148k Dacia branded, with a consolidated turnover of €10.5 billion. Also, Alpine confirmed its positive unit volume trajectories.

Why are we still positive?

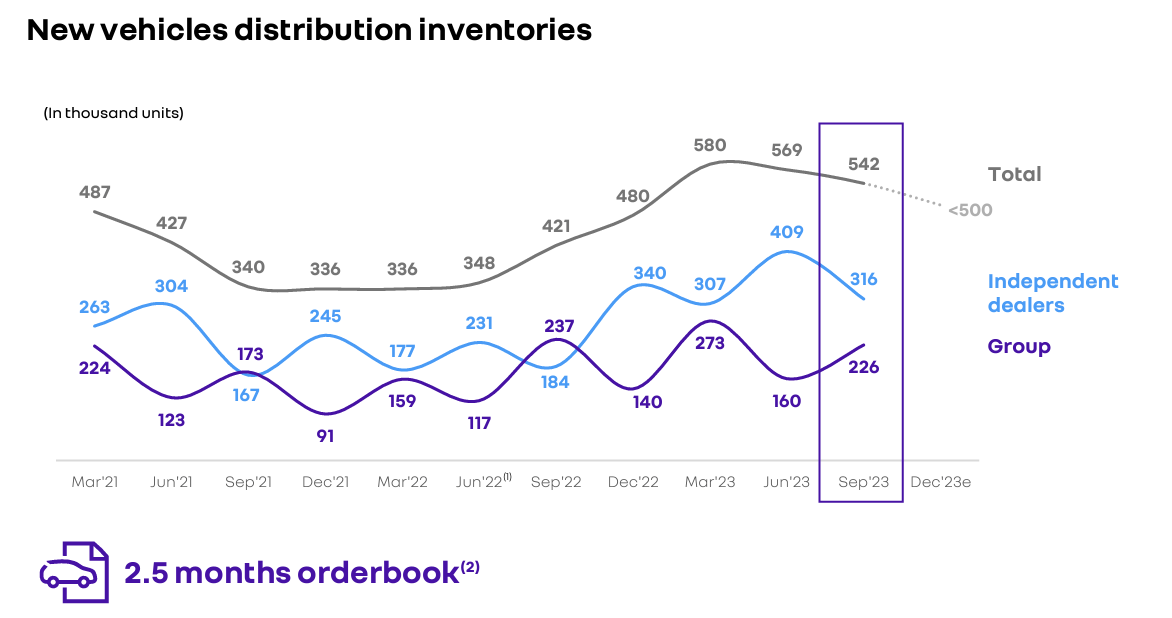

- Renault's orderbook is very healthy, with 2.5 months of forward turnover in September-end. In light of these, the automaker was able to increase its 2023 targets on operating margin, now closer to 8% vs. previous estimates between 7% and 8%;

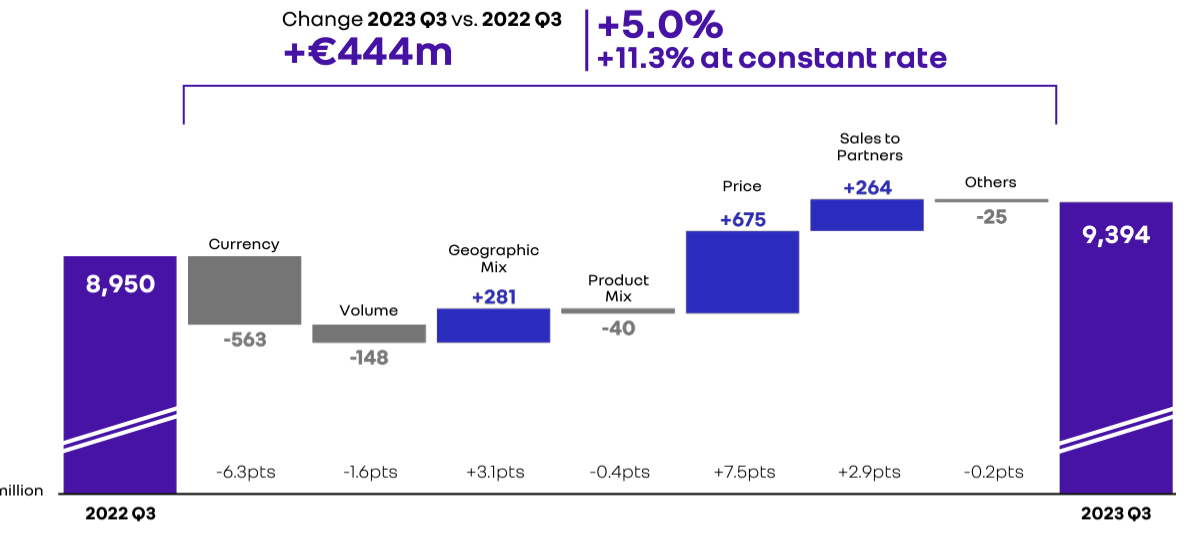

- The company continued to benefit from a higher unit price effect of 7.5 points over the previous quarter. This result aligns with our PRICE/MIX evolution (Fig 1). In numbers, the better price was a plus €675 million in the sales waterfall and was able to offset raw materials inflationary pressure fully;

- The total inventory development (including the independent network) is positive. Inventories decreased to 542,000 units from the 569,000 vehicles at June-end. The company aims to achieve a target below 500,000 units by year-end (Fig 2);

- Renault brand in the EV segment signed a solid overperformance with a plus 22% more EV sold vs Q2 2022. Electric, hybrid, and plug-ins represent 43% of the brand's European sales. In particular, fully electric cars accounted for 11% of the total in the third quarter. This year's increase in sales comes at a time of fierce competition in the EV race, with Tesla and Chinese manufacturers offering increasingly cheaper models. This is a remarkable result from Renault, and as already mentioned, the Espace E-Tech Hybrid was a positive catalyst waiting for the New Clio. This is just the beginning; starting in 2024, Renault will increase its EV offering with the Scenic and Renault 5.

{kind=link}

Fig 1

Renault inventories and order book development

{kind=link}

Fig 2

Ampere CMD update

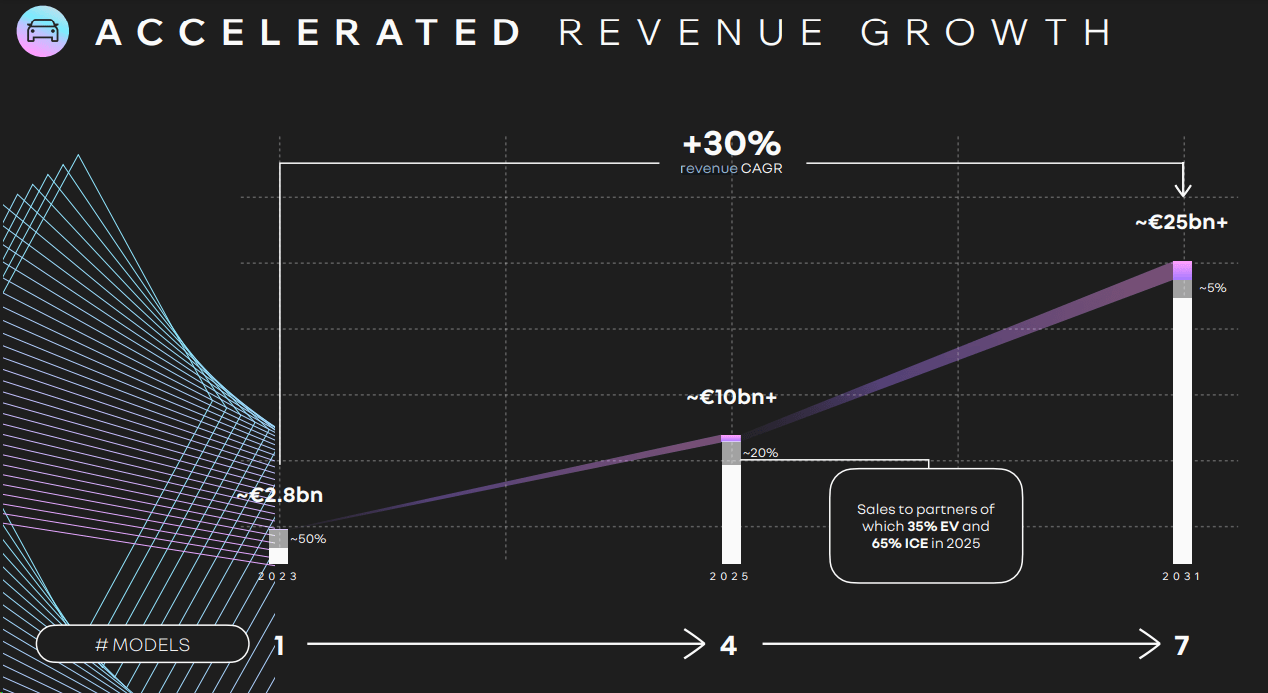

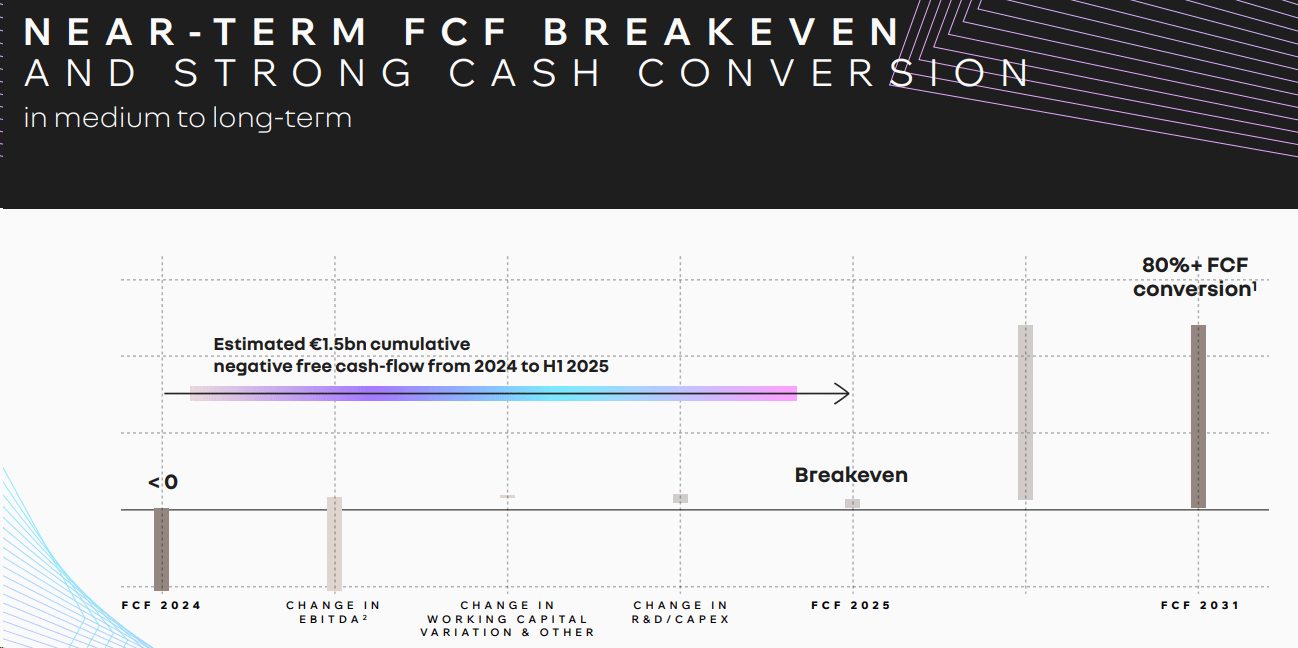

We now have much more details to check. First, we suggest listening to the 2.5-hour presentation on Ampere and looking at the new online corporate website . To add content, 2023 EV units sold were at 45k, and there are target projections to deliver 300k and 1m units in 2025 and 2031. 2023/2025/2031 top-line sales estimates are €2.8/€10/€31 billion (Fig 3), with breakeven forecasted in 2025 on both operating margin and cash flow with a 10% operating margin from 2030 onwards (Fig 4). The compound annual growth rate is estimated to be above 30% between the current year and 2031, with a double-digit market share penetration. These are Ampere's ambitions to win against the competition in the EV era. As a reminder, the company was founded as an electric vehicle and software company that designs, develops, produces, and markets electric vehicles for Renault. The aim is for technological excellence with battery-powered cars democratization, which at the moment are anything but democratic, given the prices on average 30% more expensive than ICE cars.

Renault presents the Ampere project and is waiting for favorable market conditions for a possible IPO in the first half 2024.

Among the most important innovations is a new model called Legend . This is a model which should arrive on the market in 2026. It is an urban vehicle with class-leading efficiency: just 10 kWh/100 km, CO? emissions 75% lower than the average European internal combustion engine car sold in 2023, zero CO? emissions, and lower fuel consumption. This car will be " Made in Europe, with an entry price lower than €20k. " Legend will compete directly with Chinese manufacturers' EV offers and Tesla's Model 2 and Citroen ë-C3.

We see this move as part of Renault's efforts to reassure investors and push ahead with the Ampere IPO. In the CMD release, we understood that the company has 11 thousand employees, of which 35% are engineers. Most investments have already been made for electric vehicles and its industrial ecosystem. They are located in the ElectriCity, an area in northern France where Renault intends to verticalize the supply chain, also thanks to two gigafactories for batteries.

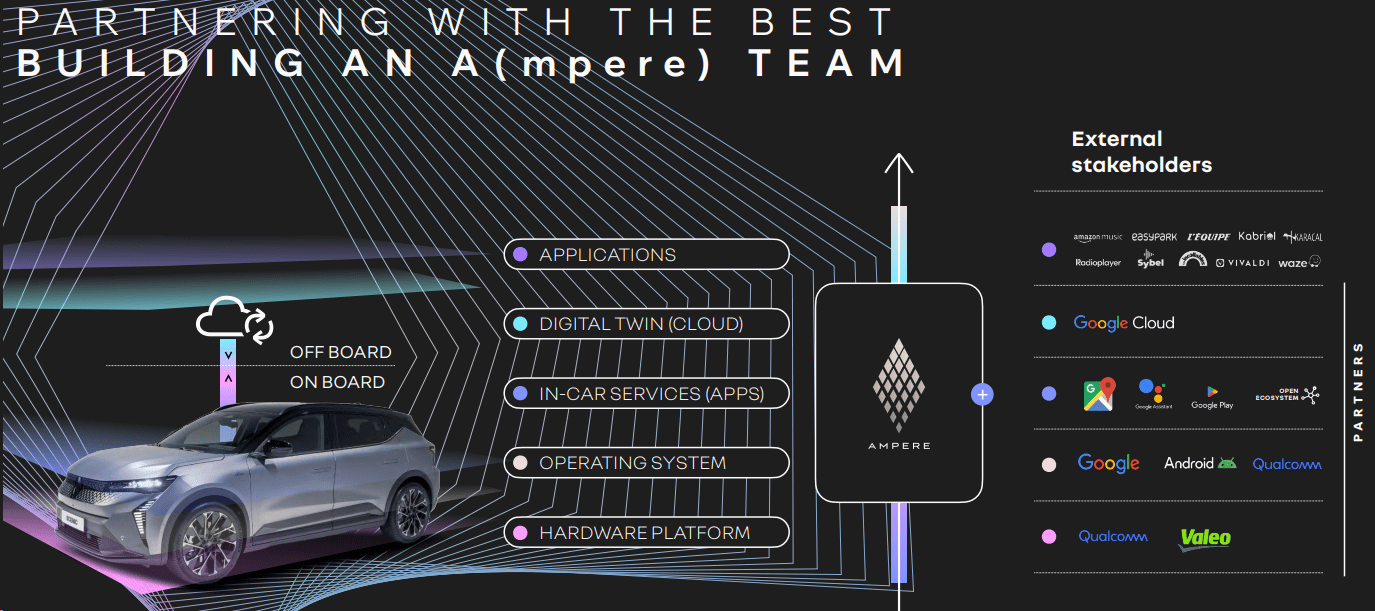

The EV product range is already planned, with seven vehicles by 2031 in the heart of the European market: Megane E-Tech, Scenic E-Tech, Renault 5, Renault 4, Legend, and two other vehicles. Further projects are planned (both on cars and for software) with different brands and partners such as Alpine, Nissan, and Mitsubishi. Among other things, Nissan will be among the primary investors, " injecting up to €0.7/€0.8 billion ". Qualcomm is also " evaluating the possibility of investing " with the giant Google, which decided to start a tech partnership with Ampere (Fig 5). Renault (once again) made it clear that it will still maintain a substantial majority of equity shares in Ampere.

{kind=link}

Source: Ampere CMD presentation - Fig 3

Ampere FCF and EBITDA evolution

{kind=link}

Fig 4

{kind=link}

Fig 5

Here at the Lab, we appreciated the idea of separating the activities relating to electric motors from those about internal combustion engines. An IPO could unlock shareholders' value. In addition, distributing Ampere shares to existing shareholders would minimize dilution, achieve the benefits of separating Ampere, and minimize the risk of capital loss. No value has yet been assigned to Ampere; however, rumours exist for a €10 billion valuation .

Conclusion and Valuation

Today, we are not forecasting a Renault sum-of-the-part valuation with Ampere estimate. However, if the IPO continues and Renault retains majority control, we could imply a value of at least €5 billion vs. a current Renault market cap of €10.45 billion. Back to basics, looking at the Q3 results, we expected ‘ financial performance to remain solid over the medium term, with even some scope for further earnings surprises .’ In our internal estimates, Renault profits surprised to the upside; however, this was not very well reflected by market expectations. In our supporting buy rating thesis, Renault will likely have a holding complexity, but we believe this 3x P/E valuation does not fully reflect the company’s fundamentals. Our valuation is based on an unchanged 4.5x P/E with a value of €41.5 per share ($11.5 in ADR). Therefore, we maintain our overweight target. As a reminder, we positively value de Meo and believe he is one of the best CEOs in the sector. As a cross-coverage, we suggest our readers check our publication on Nissan . Renault owns about 43% of the Japanese company (including c28% owned via a French trust) and fully benefits from an ongoing dividend distribution. Downside risks include intensifying competition from Tesla and Chinese OEMs and higher European exposure, with approximately 70% of unit sales coming from the Old Continent. Therefore, the company might be impacted by a local consumer slowdown. Additional risks include lower FCF evolution, Ampere higher targets, which might equal a large discount post-IPO, and higher holding complexity.

For further details see:

Renault: Time To Buy More