RNSDF - Renault: Turnaround In Progress With Solid Fundamentals

2023-10-03 10:34:28 ET

Summary

- Final agreement with Nissan that will participate in Ampere IPO, providing a capital of €600 million.

- The company's profitability has shown significant progress, with a group operating margin of 7.6% and an automotive operating margin of 6.2%.

- Guidance increased and higher EV shares vs. traditional internal combustion engine vehicles. Our buy is then confirmed.

After analyzing Nissan , we decided to comment on Renault's ( RNSDF ) ( RNLSY ) latest development. Nissan and Renault are two correlated investment stories, and a new era is starting for the Alliance. The French group will transfer 28.4% of its Nissan shares into a trust, where the entrusted shares will be voted neutrally. Group Renault would continue to fully benefit from the economic rights (dividends and proceeds from shares' disposal), and this transfer would not lead to any write-down in Renault's balance sheets. This new collaboration alliance focuses on three areas: India, Latin America, and Europe. In addition, as already reported in our publication called ' Ampere IPO Is A Key Catalyst , ' the Japanese company " will invest up to €600 million in the spin-off of Renault's electric car Ampere, securing a place on the board ." Even if this development seems negative on Renault, we believe this alliance rebalance is a positive sign given the necessary CAPEX investment in the EV transition. The two companies had initially sought to reach a final agreement by March 2023 end. However, progress in the negotiations was delayed due to Nissan's concerns over the strategic plan terms, including the handling of intellectual property related to electric vehicles. Despite that, this investment strengthens Ampere's cap table and accelerates Nissan & Renault's EV strategy in Europe.

{kind=link}

Source: Renault Q2 results presentation

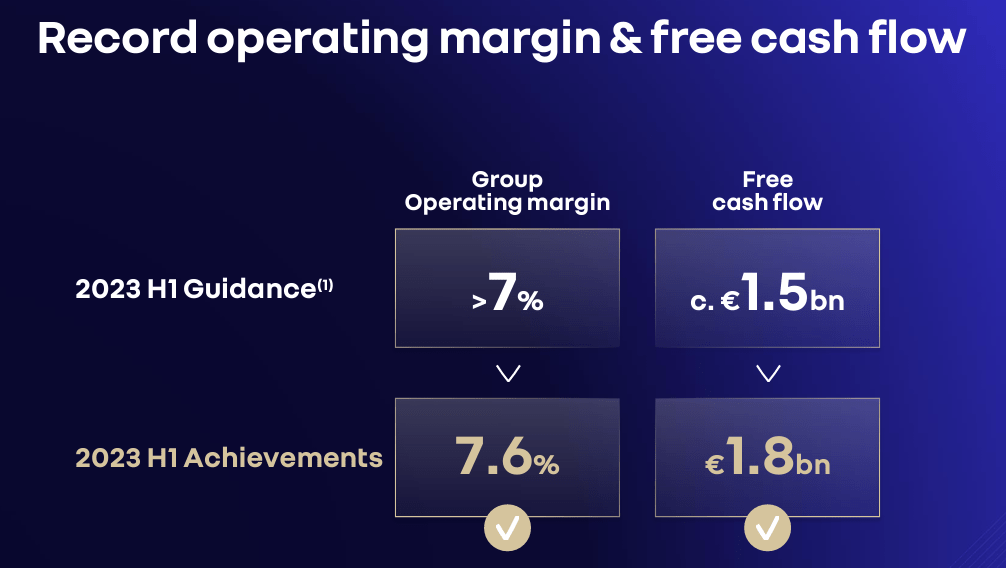

H1 financial review

Here at the Lab, we mentioned that Renault is ' Back To Profitable Growth; ' however, in H1, we should note that the company's operating margin reached 7.6% but was boosted by a carve-out impact. For this reason, the French group's results were slightly above Wall Street estimates. The company achieved stronger than expected top-line sales (€26.8 billion compared to a consensus at €25.6 billion), thanks to pricing activities, up by approximately +9 vs. last year's results. As mentioned, the company's EBIT margin reached 7.6%, but we should include a €275 million positive one-off effect related to D&A cessation on HORSE. According to our analysis, if we had the powertrain D&A, the group margin should have been at 6.6%, which is a remarkable result vs. Renault's recent historical average but lower numbers than the one presented below.

{kind=link}

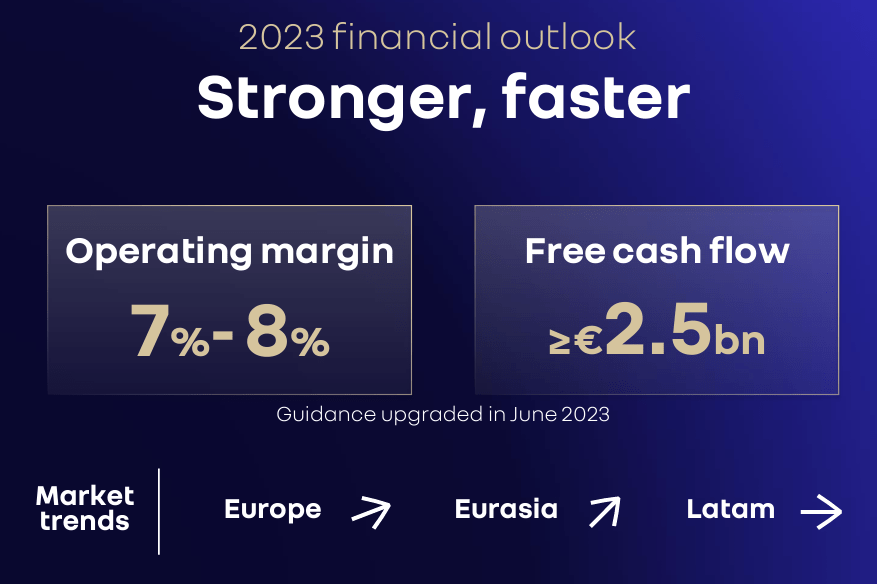

Renault's automotive cash flow reached €3.3 billion in the semester and was inflated by €600 million from a dividend coming from the financial services. Despite that, the Group confirmed its 2023 operating EBIT guidance in the range between 7-8% compared to a consensus estimate of 7.1%. This implied that the operating margin could be at the outlook top-end. The net cash financial position reached €2.2 billion at June-end, up by €1.6 billion compared to December.

{kind=link}

Why are we optimistic about Renault?

- On the EV front, the Renault brand recorded an 18% volume increase in electrified passenger car sales compared to H1 2022, equivalent to 37% of the brand's passenger car sales in Europe. Fully EV accounted for 11% of the brand's passenger car sales. The first hybrid version of the Dacia range was launched in January 2023. Despite component constraints, the Dacia Jogger Hybrid already represents over 25% of its order. Dacia Spring (100% electric) recorded over 27,000 European sales in H1 and was on the EU retail sales podium. This supportive phase will continue in H2 thanks to the Espace E-Tech Hybrid and the New Clio. In addition, from 2024 onwards, Renault's electric range will accelerate further with Scenic and Renault 5. Meanwhile, the EV orders group level remains high. Positive for the brand is the new compact SUV Austral, which continues a positive sales trajectory in the business;

- On a cautious estimate, we anticipate a flattish H2 volume in line with H1 results. However, we are more optimistic about input costs that should benefit from approximately €500 million relief thanks to an easing of raw material inflationary pressure;

- On the price/MIX level, we believe that Renault will record a mid-to-high-single-digit growth with the HORSE carveout effects neutral in H2. On a negative note, given the ramp-up of new models, working capital and the CAPEX will increase. For this reason, we should remain more cautious on the automotive FCF, which we forecast at €2.5 billion for FY23;

- Alpine, which has just changed leadership with the arrival of CEO Philippe Krief , continued to improve its sales with almost 1,900 units, up 9% compared to the first half of 2022;

- We should report that Ampere IPO might be planned in 2024 first months and according to rumors, the first meetings with investors have been positive.

Conclusion and Valuation

Here at the Lab, we expect financial performance to remain solid over the medium term, with even some scope for further earnings surprises. Therefore, we confirmed our buy rating of €41.5 per share ($11.5 in ADR). Our valuation is based on a P/E of 4.5x in the next visible period, compared to a current valuation of 3.5x. Even valuing Ampere with a 50% discount on the potential valuation, we think that Renault brands, supported by its EV transition and additional margin-accretive SUV launches, are more than enough to justify a buy. On the downside risk, BYD might represent a significant EU market share loss; however, the recent EU investigation on Chinese cars might limit this concern. In addition, we should report that Ampere aims for an EBIT margin at a double-digit rate by 2030. This creates a visibility issue and a valuation that might be impacted by exogenous factors such as battery costs, execution risks, competitive landscape, and production costs. As already reported, the holding complexity is another critical risk in Renault's investment thesis. As a reminder, the French Group is " creating five independent and autonomous companies."

For further details see:

Renault: Turnaround In Progress With Solid Fundamentals