RLTY - Retirement Planning: The Income Compounder Portfolio 2024 Update

2024-01-08 13:16:54 ET

Summary

- The number of retirees in the U.S. is growing rapidly, with as many as 10,000 new retirees a day.

- Retirees with income from employment, pensions, or investments are generally better off than those relying solely on Social Security.

- By investing in an Income Compounder portfolio strategy, it is possible to grow your river of cash to support your future retirement needs.

A recent report from The Federal Reserve on the economic health and well-being of U.S. households in 2022 caught my attention. Retirees represent a sizable percentage of the adult population, and that number is growing rapidly - by as many as 10,000 new retirees a day according to AARP . According to the report, 27% of adults considered themselves retired, although some of those are still working (I fall into that category). Those who are currently retired consider themselves generally well off, but those who are approaching retirement are getting concerned that they are not saving enough money to live on when they do retire.

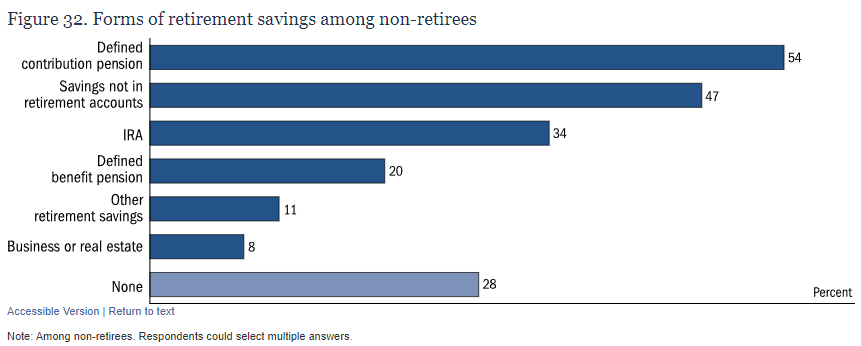

Retirees generally report high levels of financial well-being, but those with income from employment, pensions, or investments were doing better than those who relied solely on Social Security or other public income sources. Among non-retirees, a lower share said they felt like their retirement savings were on track compared with 2021.

Note that in the report, those who have other sources of income besides Social Security consider themselves doing better than those who do not. Income from a pension, 401k, or other defined contribution plans (e.g. 403b, 457b), IRA (Traditional or Roth), or rental income for example can help one to feel better about their retirement when Social Security alone is not enough.

And while almost 75% of non-retirees have some form of retirement savings, about 28% did not have any. For those who do not have enough saved and wish to learn how to save more to generate wealth in retirement, consider creating a passive income retirement account using an Income Compounder approach, like the one that I have created and discussed here .

{kind=link}

In my opinion, many retirees or those who are nearing retirement age concern themselves too much with the value of their retirement portfolio. Yes, net worth is important to measure and understand, however, the real issue that needs to be addressed is how much you will spend in retirement.

As investors (or savers) transition from growth to decumulation, the concern is whether the funds will run out over time. While most people are working from their 20s until their 60s (generally speaking), they are earning some income and (hopefully) saving some. During those earning years, growth of the asset base is of paramount importance.

But once you retire and no longer have a steady paycheck coming in, the income that you have coming in from your investments needs to support your lifestyle. Whether you have $500k, $1 million, or $5 million saved does not matter as much as whether the amount of income that you have coming into your bank account each month exceeds or at least equals how much is going out. This is what financial planners refer to as the Decumulation phase because you are spending down those assets that you worked your whole life to save. I explained my approach to that transition in this article , where I also describe my Income Compounder portfolio.

Unfortunately, many individuals are not comfortable managing their own self-directed investments and would prefer to rely on a financial planner or investment adviser.

Self-directed retirement accounts frequently rely on individuals to have the skills and knowledge required to manage their own investments. Non-retirees with self-directed retirement savings varied in their comfort with making investment decisions for their accounts. Sixty-one percent of non-retirees with self-directed retirement savings expressed low levels of comfort in making investment decisions with their accounts.

To that I would say, get over it! What is more important than your financial future? Take some time to read, learn, save, and invest. Make some mistakes, learn from them, and keep learning and saving even if only a little bit each month. That is what I did, and if I had more time, I would relate my entire life story. But suffice to say that I am a self-taught investor, having fired my financial advisor in 2009 after I lost about 30% of my retirement savings at the time to the GFC. I started reading, learning, and investing whatever I could into a self-directed IRA and contributed at least 3% (the amount that my employer matched) of my paycheck to the company 401k while I was working.

In the remainder of this article, I would like to offer some suggestions for a few different high yield income investments that offer a substantial return on your investment if you are willing to accept some risk. In my case, I am one of the fortunate ones who have all the different sources of income to support my retirement including a pension, income from working part-time for myself, investment income from my Income Compounder or IC portfolio, and eventually Social Security once I decide to start taking it.

Energy Revival

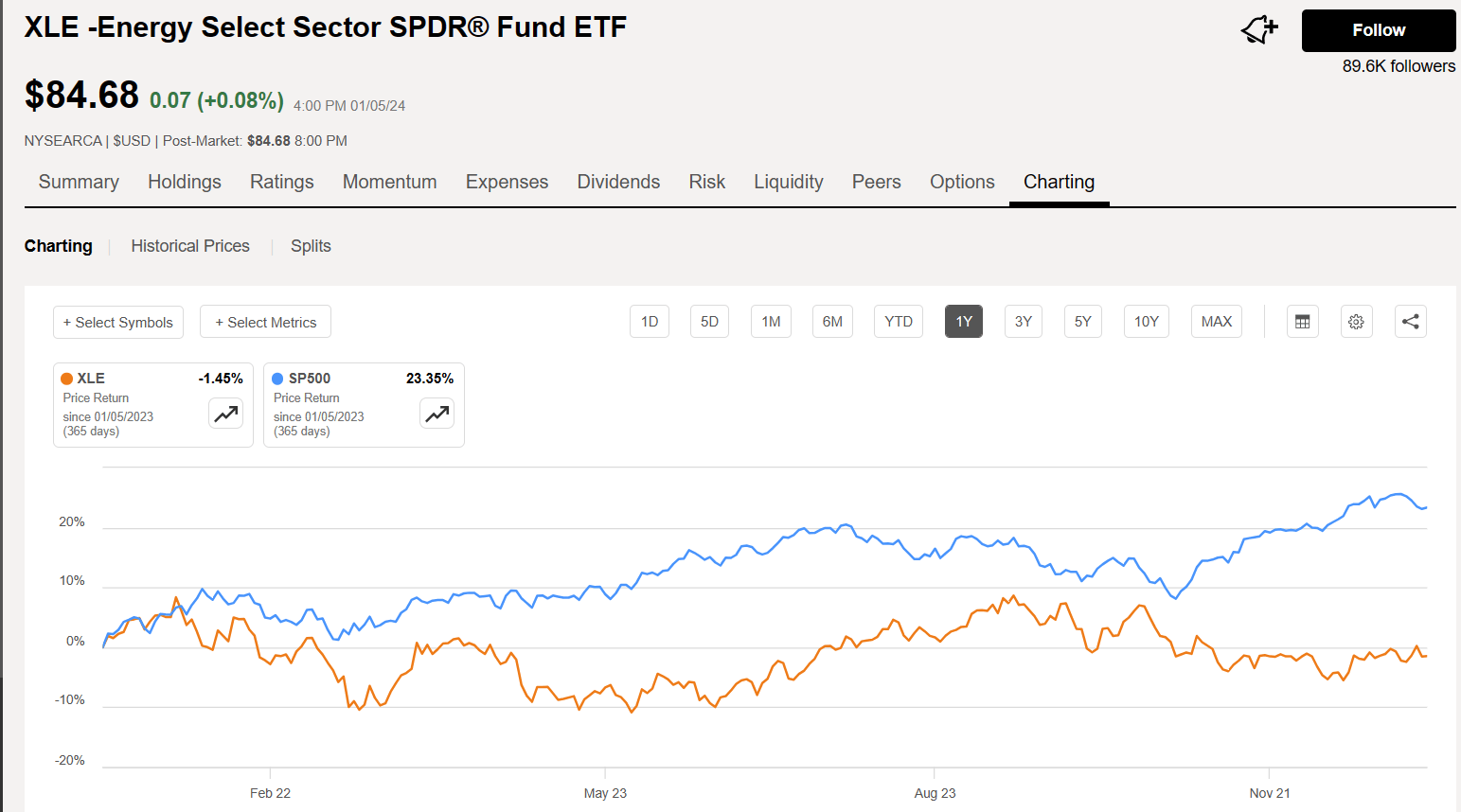

Because I have other sources of income, my IC portfolio takes on a bit more risk than some conservative investors might feel comfortable with. I do not consider a dividend growth stock that pays 3% to 4% annual yields an income investment. That is more of a growth investment, which is fine if you have another 20 years to grow your portfolio. And I do hold a few of those stocks myself, including Chevron (CVX). My first employer out of college in my first real career job was with Chevron and they were and still are an excellent company. I bought my first shares of CVX (for about $142 cost basis) just last year and I intend to hold them for at least 20 years assuming I live that long. I feel that the energy sector ( XLE ) is due for a revival now in 2024 after a lackluster year in 2023.

{kind=link}

I also recommend CVR Energy ( CVI ) if you are willing to take on a little more risk and are interested in a high-yield income investment in the energy sector. I recently published an article about the CVI stock if you wish to learn more.

Technology Impact on the Future

Like the energy sector, technology is not going away and is very much molding the future of society with the rapid growth of AI, blockchain technology, the rise of quantum computing , electric vehicles (much to the disdain of ICE lovers), renewable energy, etc. Therefore, any long-term investments should have at least some moderate degree of exposure to technology. In her recent book, Broken Money , about the history of money and what the future of global finance looks like, Lyn Alden explains how technology has had more of an impact on money than politics or anything else:

Politics can affect things temporarily and locally, but technology is what drives things forward permanently and globally. From shells to gold, from papyrus bills of exchange to central banks, and from the invention of the telegraph to the creation of Bitcoin, this is just as true for money as it is for anything else.

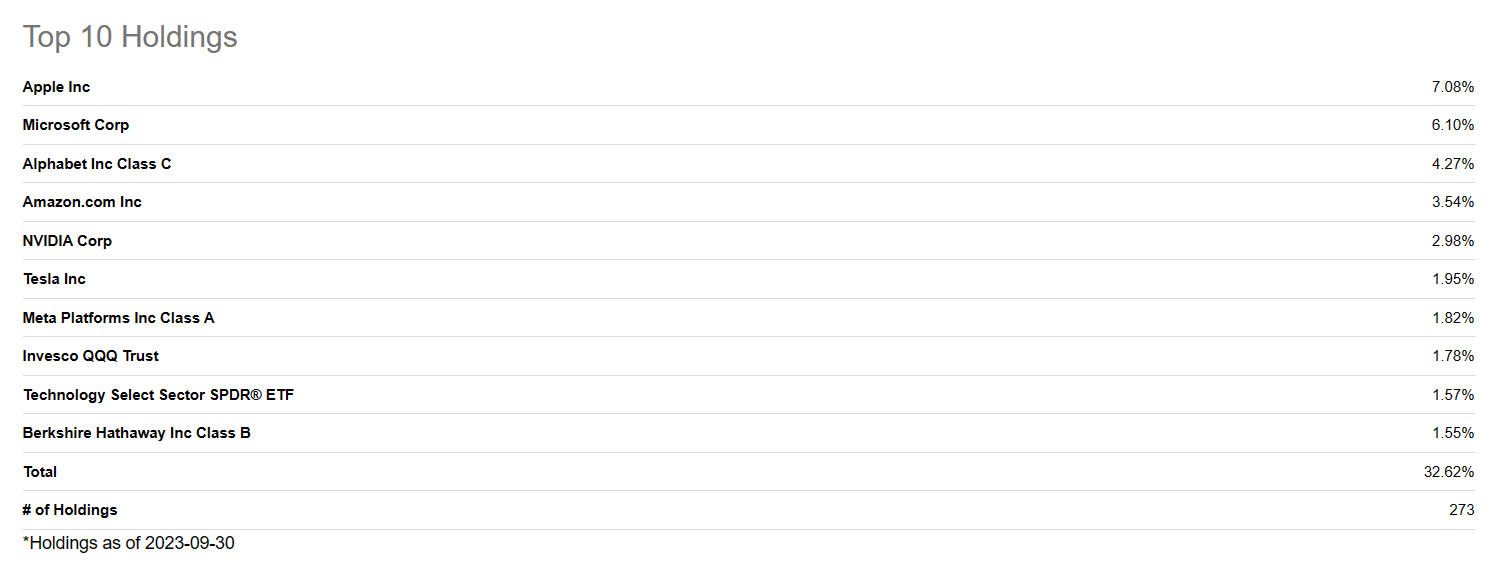

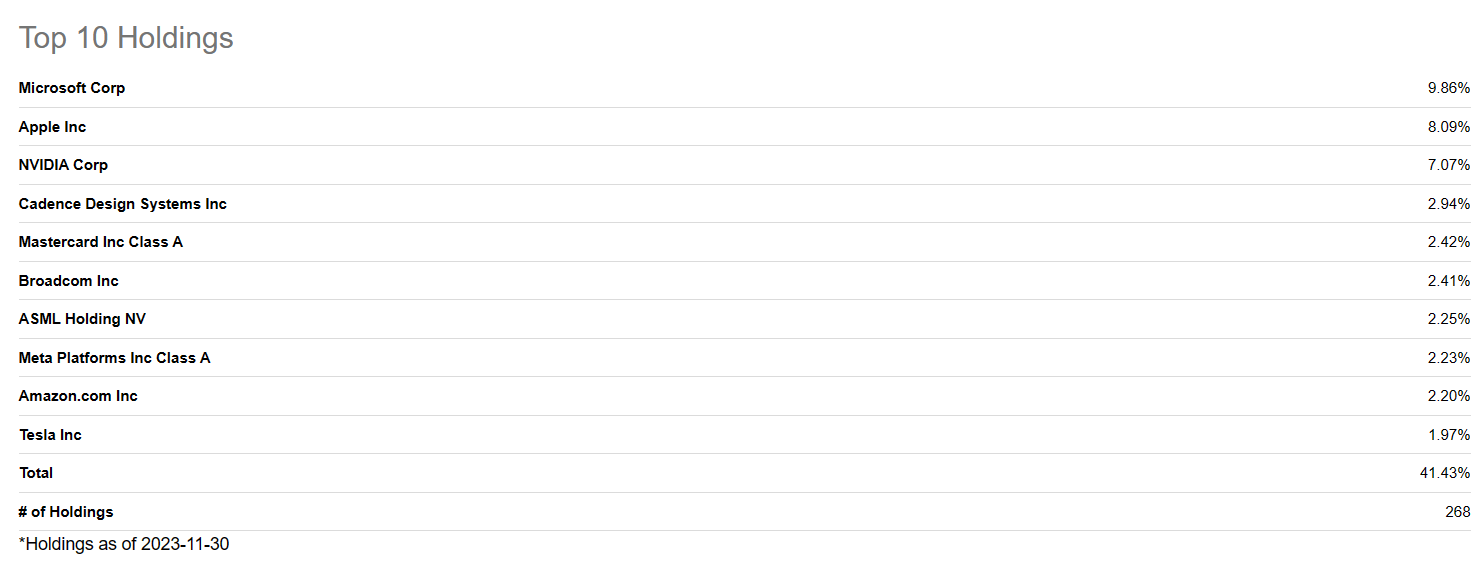

Many tech stocks were the darlings of 2023 including those in the so-called Magnificent Seven. The companies considered to be the "Magnificent Seven" include Alphabet (GOOGL), Amazon (AMZN), Apple, Meta Platforms, Microsoft, Nvidia (NVDA), and Tesla. Someone who wanted to own many or all those stocks in an IC portfolio can buy them individually, or they can buy a closed end fund that holds those stocks in its portfolio.

That is what I chose to do, and I recommend that you consider the Cornerstone funds, Cornerstone Strategic Value Fund ( CLM ) and Cornerstone Total Return Fund ( CRF ) for your own IC portfolio. Both CLM and CRF pay a very high yield distribution that currently amounts to an annual yield of about 18% and trade at a premium to NAV. The top 10 holdings in CLM (as of 9/30/23) include all 7 of the Mag 7 stocks.

{kind=link}

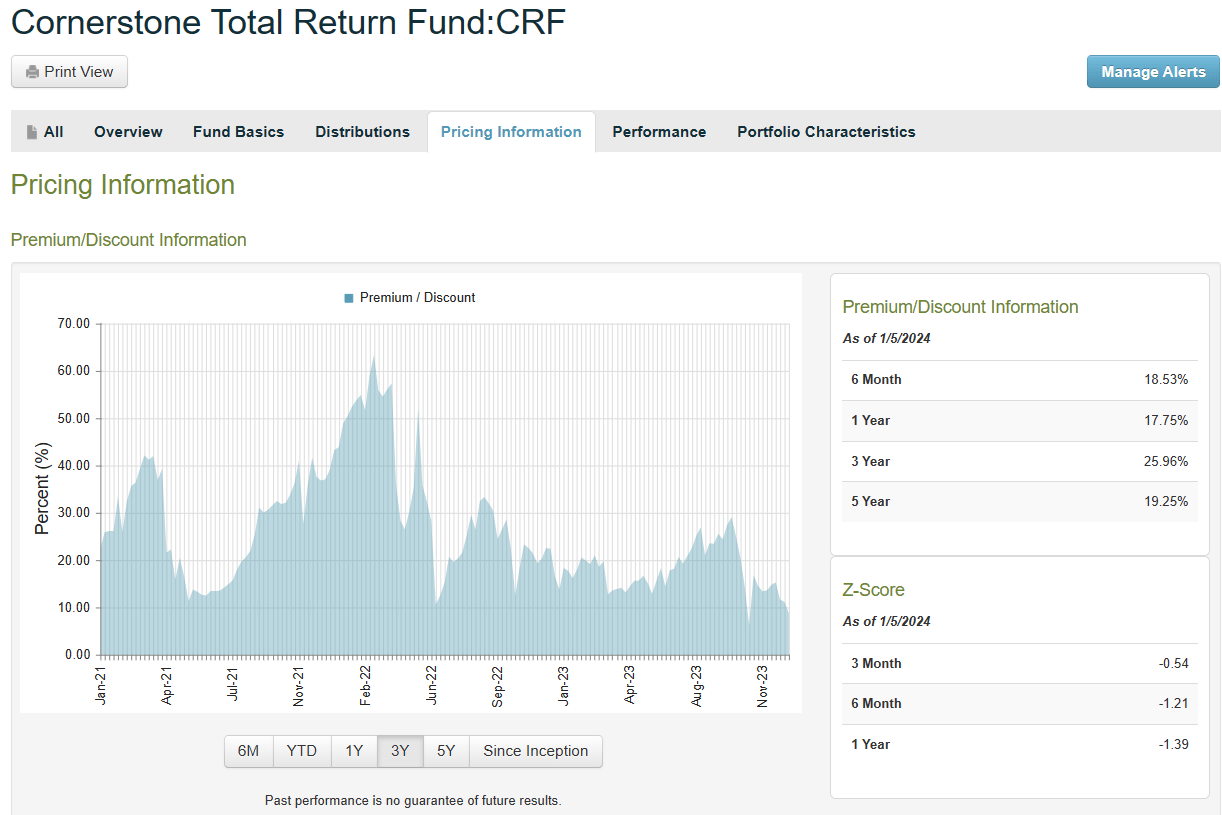

One aspect of the funds that is appealing to income investors who like to compound their monthly income like I do, is that both funds allow reinvestment at NAV, which at times can offer a discount of -20% or more depending on the premium at the time of reinvestment. Currently, the two funds trade at a premium of 6.6% for CLM and 9.4% for CRF, however, the 3-year average premium is about 25% as shown on CEFconnect.

{kind=link}

If your risk tolerance does not allow you to enjoy the high yield monthly income from CRF or CLM, you may wish to consider the BlackRock Science and Technology Trust ( BST ) instead. One advantage to BST is that it uses no leverage while trading at a discount and paying a distribution that currently yields about 9% annually. The top 10 holdings are similar to CLM with only GOOG from the Mag 7 missing from the top 10 as of 11/20/23.

{kind=link}

With interest rates expected to start coming down this year, technology funds like BST should perform well with some potential for capital appreciation along with the 9% yield. This recent article from my fellow SA analyst describes BST in more detail and explains the Buy thesis.

Firstly, it means these companies can borrow money more easily and at a lower cost. This is essentially giving them a discount on loans, making it easier for them to grow and invest in new initiatives, products, and research developments.

Also, when interest rates go down, people and businesses tend to spend and invest more money. This is good for tech companies because it means more people want to buy their products and services.

Of course, the same logic applies to the Cornerstone funds, so pick your poison (so to speak), depending on your risk tolerance and investment objectives.

Utilities and Infrastructure

Another industry sector that benefits from lower interest rates and inflation coming down is the utilities and infrastructure sector. Also, with the passing of the Biden administration bills supporting infrastructure spending those impacts are just starting to be realized with as many as 40,000 new projects worth $400B coming online or in progress according to the White House. It will take from 3 to 5 years to complete all the projects and most of the revenues from those projects will be recognized in 2024 and 2025. There are several ways to take advantage of that spending blitz and I offer two suggestions, one with less risk and lower returns and one that is more global with higher risk and greater potential returns.

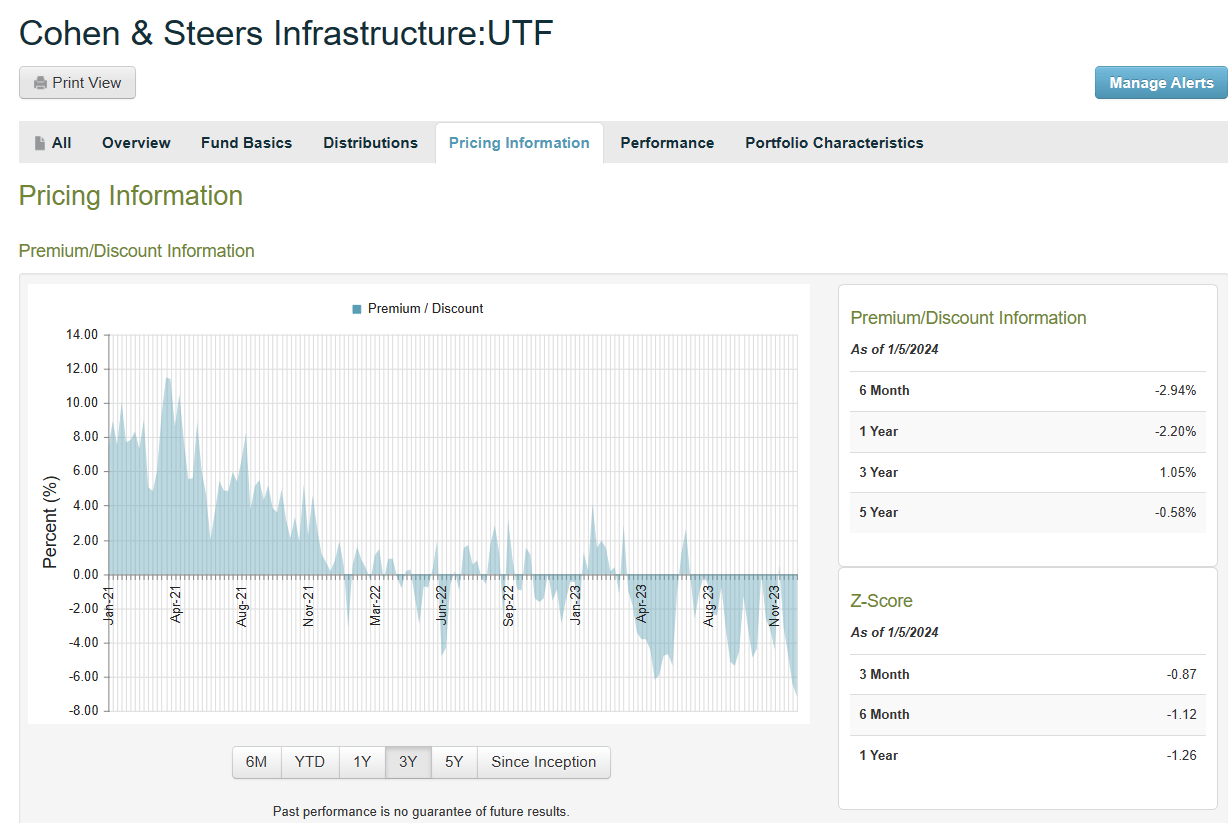

The less risky, more conservative option is the Cohen & Steers Infrastructure Fund ( UTF ) which currently yields about 8.5% based on a monthly distribution of $0.155 that has been paid steadily for the past 5 years. Several of the top holdings took a big hit in 2023, including NextEra Energy which lost about -25% in the past year. However, many of those names are now starting to recover. This recent article from another SA analyst covers the Buy thesis for UTF if you want to learn more about that fund.

{kind=link}

And according to CEFconnect, UTF is now trading at about the widest discount that it has traded for in quite some time. The one-year Z-score of -1.26 is another strong buy signal.

{kind=link}

For a little more risk but a higher reward you may wish to consider the MainStay CBRE Global Infrastructure Megatrends Term Fund (MEGI). With a long name but a short history, the MEGI CEF offers investors a yield of 11% (also paid monthly) with an increase in the distribution in August 2023 from $.1083 to $.1250. The fund was incepted in 2021 and was one of a dozen CEFs that were launched that year.

MEGI also trades at a discount of about -15% currently (which has been the 1-year average discount) and has started to recover from a big price drop in 2023, following the broader utility sector as shown by this total return chart with XLU representing the broader sector return.

{kind=link}

My fellow analyst, Nick Ackerman, first introduced me to the MEGI fund, and he recently reviewed it here .

Real Estate

Another market sector that has struggled mightily in 2023 due to inflation and rising interest rates is the real estate sector. However, like utilities and infrastructure, real estate is looking at making a strong comeback in 2024 with talk of the Fed starting to reduce, or at least stop raising interest rates. Traditionally, many income investors have enjoyed the benefits of REITs with their incentive to return 90% of taxable income to shareholders each year. There are many reasons to invest in REITs as explained by NAREIT :

REITs historically have delivered competitive total returns, based on high, steady dividend income and long-term capital appreciation. Their comparatively low correlation with other assets also makes them an excellent portfolio diversifier that can help reduce overall portfolio risk and increase returns.

But the after-effects of the Covid-19 pandemic with the ensuing “work from home” movement harmed commercial real estate, and now rising interest rates due to inflation have led to much higher mortgage rates which has in turn negatively impacted residential real estate as well. However, as inflation has stalled and interest rates appear to be coming down, real estate is beginning to look appealing again in 2024 from an investor standpoint.

There are two funds that I recommend considering in the real estate sector for an IC portfolio. The first is a global fund, CBRE Global Real Estate Income Fund (IGR), which I reviewed in November. IGR offers a yield of about 13.5% currently and is trading at a discount to NAV of -11.7%. The price of the fund began to recover shortly after that article was published and they have so far maintained the steady $0.06 monthly distribution. Some people fear that the dividend may be cut this year, so that is one risk to consider with IGR. However, as I explained in my analysis back in November, the fund managers are optimistic about the resiliency of global growth in the real estate sector heading into 2024:

One final point made by the fund managers during the Q3 webinar is that global REIT growth remains resilient and is expected to provide attractive opportunities in 2024 due to contractual rent increases, high occupancy rates, and prior-year leases coming online.

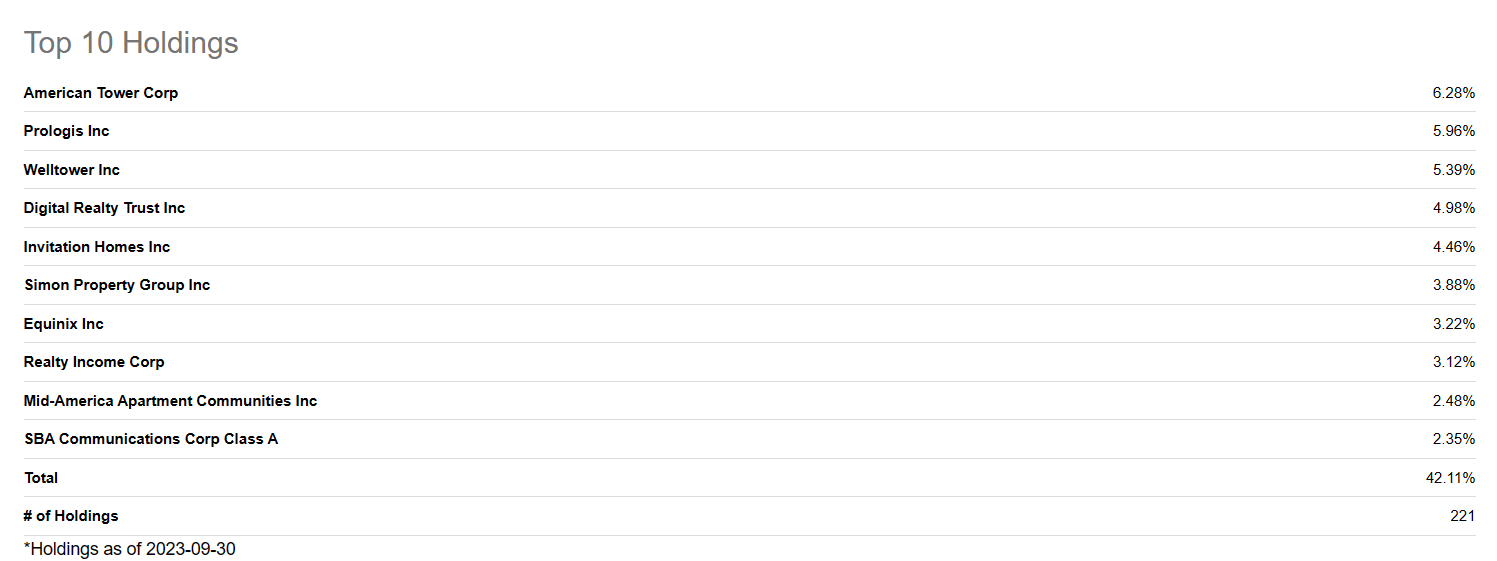

A relative newcomer to the REIT public market is a CEF that was launched in 2022 from Cohen and Steers, the Cohen & Steers Real Estate Opportunities and Income Fund (RLTY). Although the fund has only been around for just under two years now, the distribution was raised in July 2023 from $.1040 to $.1100 monthly. At the current price of about $14, the annual yield is 9.5% and the fund trades at a discount to NAV of -11.7%.

The fund’s top 10 holdings are all strong, well-respected REITs with good growth prospects.

{kind=link}

My colleague and fellow analyst, Nick Ackerman , recently provided an excellent update on the RLTY fund where he suggests the many reasons why it is a Buy for income investors who wish to take advantage of the recovery in real estate in 2024:

RLTY is poised to perform strongly as the REIT space continues on its recovery. With the Fed acknowledging that inflation is coming down, rate cuts are now nearer than originally forecasted. That can help propel the space higher, and with RLTY trading at a deep discount, that's an additional catalyst for upside. At the same time, the fund pays out a healthy distribution to investors while waiting for potential capital appreciation.

Summary

As we head into the new year, I wanted to provide my followers (and new followers) some ideas on where I am looking to invest for income. I currently hold over 50 individual positions in my IC portfolio and have only suggested a few ideas in this writeup to keep from overwhelming new investors or those who do not have the risk appetite that I have. Many of my other income holdings include BDCs, CEFs, preferred shares, and some alternative ETFs that generate yields well in excess of 10% annually. I typically reinvest all those monthly distributions (and some quarterly payers) into more shares of whatever security looks like a good buy at the time. I do take some distributions as cash and will eventually live off those distributions but still intend to reinvest at least 50% of them into more shares to continue growing the income generated by the portfolio holdings. That is the beauty of the Income Compounder approach to investing for retirement. The income stream keeps growing creating an ever-increasing river of cash.

For further details see:

Retirement Planning: The Income Compounder Portfolio 2024 Update