REVG - REV Group Fiscal Q4 Earnings Preview: Expect A Double Beat

2023-12-11 12:57:55 ET

Summary

- REV Group, Inc. is expected to report fiscal Q4 results with a 20% YoY EPS growth and 11% revenue growth.

- The company has a history of beating EPS and revenue estimates in previous quarters.

- REV Group is attractively valued with a forward PEG ratio of 0.73 and a price-to-sales multiple of 0.40.

- The company has three almost equally contributing segments that form the core of our society.

REV Group, Inc. (REVG) is expected to report its fiscal Q4 results pre-market on Wednesday, December 13th. Analysts expect the company to report GAAP EPS of 30 cents/share on the back of $666 million in revenue. Should REV Group meet these numbers, it'd represent a YoY EPS growth of 20% and revenue growth of 11%. Will REV Group stock continue its strong YTD performance (30%), or will things turn south after the Q4 report? Let's find out in this earnings preview. But before that, a quick introduction to the company.

REVG Q4 Preview (Seekingalpha.com)

What Does The Company Do?

REV Group is a manufacturer of specialty segment vehicles like ambulances, buses, firefighting vehicles, and recreational vehicles under 24 different brands. The company also deals with aftermarket parts and services for its brand of vehicles. REV Group was founded in 2010, went public in 2017 at an IPO price of $22 and has more than 200,000 vehicles in service today .

REVG Segments (investors.revgroup.com)

With that background out of the way, let's now preview REV Group's upcoming Q4 report on these parameters:

- Expectations heading into earnings

- Historical surprise

- Key things to look for

- Valuation

- Technical setup.

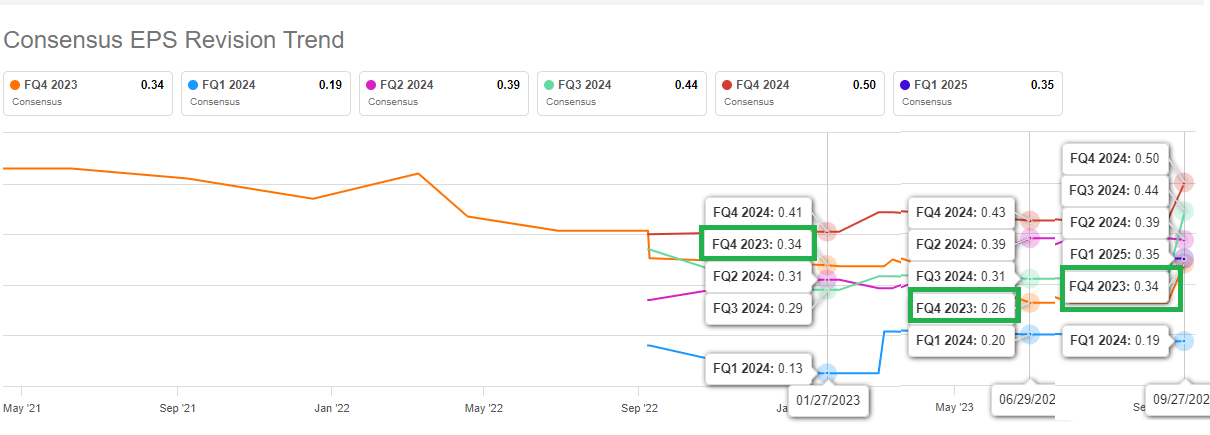

Seesawing Expectations

REV Group's Q4 EPS target has seesawed since the beginning of the year, starting at 34 cents per share to being projected at 26 cents per share in June to back being at 34 cents heading into the report. In addition, all 3 EPS and revenue revisions have been to the upside. Hence, it is not surprising that SA quant ratings gives the stock's earnings revisions an A- grade, but let's be mindful that 3 is not a large enough sample size to rely on.

{kind=link}

{kind=link}

Beat or Miss?

REV Group has beaten both EPS and revenue estimates 6 out of the last 8 quarters, which augurs well heading into Q4. In the most recent quarter, EPS beat by nearly 50% and revenue beat by about 8%. What does that tell us about Q4 being a beat or miss? Nothing, to be quite honest. Predictions are tough, especially about small caps and especially when the company called out inflationary pressure across all 3 segments (Fire & Emergency, Commercial, and Recreation) when reporting its most recent numbers.

But, what's a preview article with the author's prediction? I am going out on a limb and saying that REV Group will beat on both EPS and revenue by double-digit percentages, for the reasons covered below.

{kind=link}

Things To Look For

- As mentioned above, REV Group called out inflationary pressure in all three quarters this FY. However, the fact that all three segments contribute meaningfully to the revenue stream is an enviable position to be in for a small cap. For example, in Q1 , Fire & Emergency segment reported YoY decline but Commercial and Recreation made up for it with YoY increases. Similarly, in Q3 , Recreation segment showed YoY decline in revenue, but the other two segments made up for it. In both Q1 and Q3 (as well as Q2), REV Group handily beat revenue expectations, while beating EPS expectations in 2 and meeting in the other. I expect the three segments to balance each other's weaknesses (if any) in Q4 as well.

- In Q2, the company authorized a new buyback program for $175 million to be used within 24 months. The Q3 report did not highlight any repurchases, and it will be interesting to see whether the upcoming Q4 report highlights this. 24 months means just 8 quarters, and it may be quite a bit to catch up if the company goes two full quarters without repurchasing. There has not been much of a change in shares outstanding since the new buyback program was announced in Q2.

- REV Group has been working on debt reduction over the last few years, and its current net debt of $206 million is its lowest dating back to at least January 2021. Any further reduction in debt level would be welcome news in the current high interest rate environment.

- Q4 being the last quarter of the FY also means REV Group is likely to provide its guidance for FY 2024. Based on Seeking Alpha data , analysts expect the company to generate an EPS of $1.53 in FY 2024 on the back of $2.63 billion in revenue. It will be interesting to see if and how the company guides.

Valuation

- REVG is heading into the Q4 report with a forward multiple of 14, which is rare for a small cap. The valuation gets even more attractive when you consider that earnings are expected to grow at 19%/yr for the next five years. That gives the stock a forward price-earnings/growth [PEG] of .73, which is a GARP (Growth At Reasonable Price) investor's dream.

- If REV Group meets its Q4 revenue estimates, that would bring the company's FY 2023 annual revenue to $2.6 billion. That means the stock is trading at a price-to-sales multiple of about 0.40.

- The stock has only 3 analysts covering it, which is not surprising given the size of the company, but the median price target is $20, a good 22% from the current market price.

- Overall, the stock appears attractively valued heading into the Q4 report.

Technical Indicators

REV Group stock is going into its Q4 report in a technical sweet spot. The stock is trading above all the commonly used moving averages while not being overbought based on Relative Strength Index [RSI]. The RSI is hovering between 50 and 70 depending on the day's interval chosen, but is nonetheless in the sweet spot when you consider that the stock is trading above the 100-Day and 200-Day moving averages.

REV Moving Avgs (Barchart.com) REVG RSI (Barchart.com)

Conclusion

Although the stock has gone up nearly 30% YTD and is trading at its 52-week-high, if I were to play this earnings report, I'd play it on the long side. From a long-term perspective, too, the stock appears valued reasonably and has three, almost equally contributing segments that form the core of our society: commercial, recreation, and emergency. The company has also been paying the same, small dividend of 5 cents/qtr. since its IPO and that adds a bit of a cushion for investors. I rate the stock a "Buy" based on all the above factors.

{kind=link}

For further details see:

REV Group Fiscal Q4 Earnings Preview: Expect A Double Beat