REVG - REV Group: Might Be Rewarding In The Coming Times

2023-09-21 06:53:33 ET

Summary

- REV Group recently announced solid Q3 FY23 results, with a rise in net sales of 14.3% compared to the previous year.

- The company's fire & emergency and commercial segments saw significant increases in sales, driven by improved supply chain and higher shipments.

- Despite strong financial performance, REVG is trading at a lower multiple, indicating it is undervalued and presenting a buying opportunity.

REV Group (REVG) manufactures specialty vehicles and aftermarket parts worldwide. REVG recently announced solid Q3 FY23 results. Even after performing well financially, the company is trading at a multiple, which shows that it is undervalued. I will analyze its Q3 FY23 results in this report. I think it can be a great buying opportunity due to strong financials, low valuation, and bullish price action. Hence, I assign a buy rating on REVG.

Financial Analysis

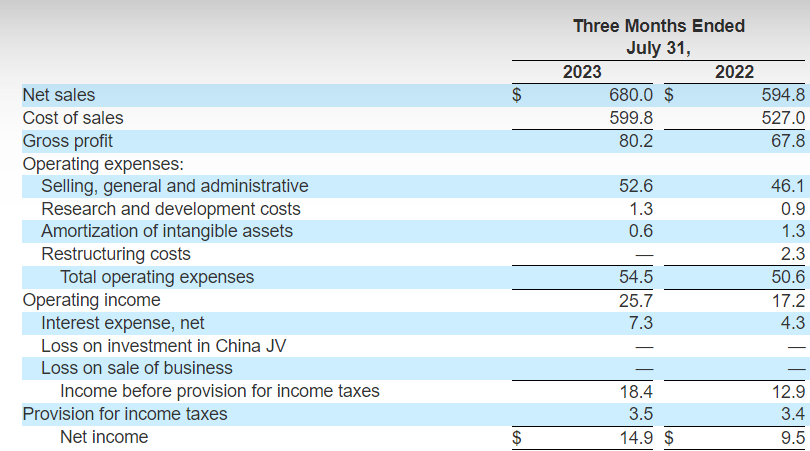

REVG recently posted its Q3 FY23 results . The net sales for Q3 FY23 were $680 million, a rise of 14.3% compared to Q3 FY22. Higher sales in its fire & emergency and commercial segments led to a significant increase in the company's sales. I believe an improved supply chain was the main factor behind the success of both these segments. The revenue from the fire & emergency segment grew by 40.3% in Q3 FY23 compared to Q3 FY22. The higher shipments of ambulance units were the main reason behind the increased sales. The revenue from the commercial segment grew by 29.1% in Q3 FY23 compared to Q3 FY22. The increased shipments of municipal transit buses and street sweepers benefitted the commercial segment. The adjusted EBITDA in Q3 FY23 increased by 33.5% compared to Q3 FY22. I think better price realization, along with increased sales in both segments, was the major reason behind the increase.

{kind=link}

Its net income grew by 56.8% in Q3 FY23 compared to Q3 FY22. The strong rise in sales and net income was impressive, and the management has increased its FY23 revenue guidance to around $2.6 billion from $2.5 billion. The sales guidance for FY23 is around 11.5% higher than FY22. I believe the company might achieve its sales targets for FY23, and we might see solid annual results. The reason I think they might achieve the sales target is because of the strong demand they are experiencing in their fire & emergency segment. The backlog in this segment by the end of Q3 FY23 was $3.2 billion, a significant rise of 48.8% compared to Q3 FY22, and what is more impressive is that the significant rise isn't because of production or management's inefficiency. In fact, the supply chain issues that the industry faced in FY22 weren't there in FY23; it shows that the increase in backlog was mainly due to strong demand. So, looking at the strong demand in its fire & emergency segment, increased backlog, and efficient supply chain, I think they will reach the sales target for FY23, resulting in the highest revenue in the company's history. So, considering all these factors, I am bullish on REVG.

Technical Analysis

{kind=link}

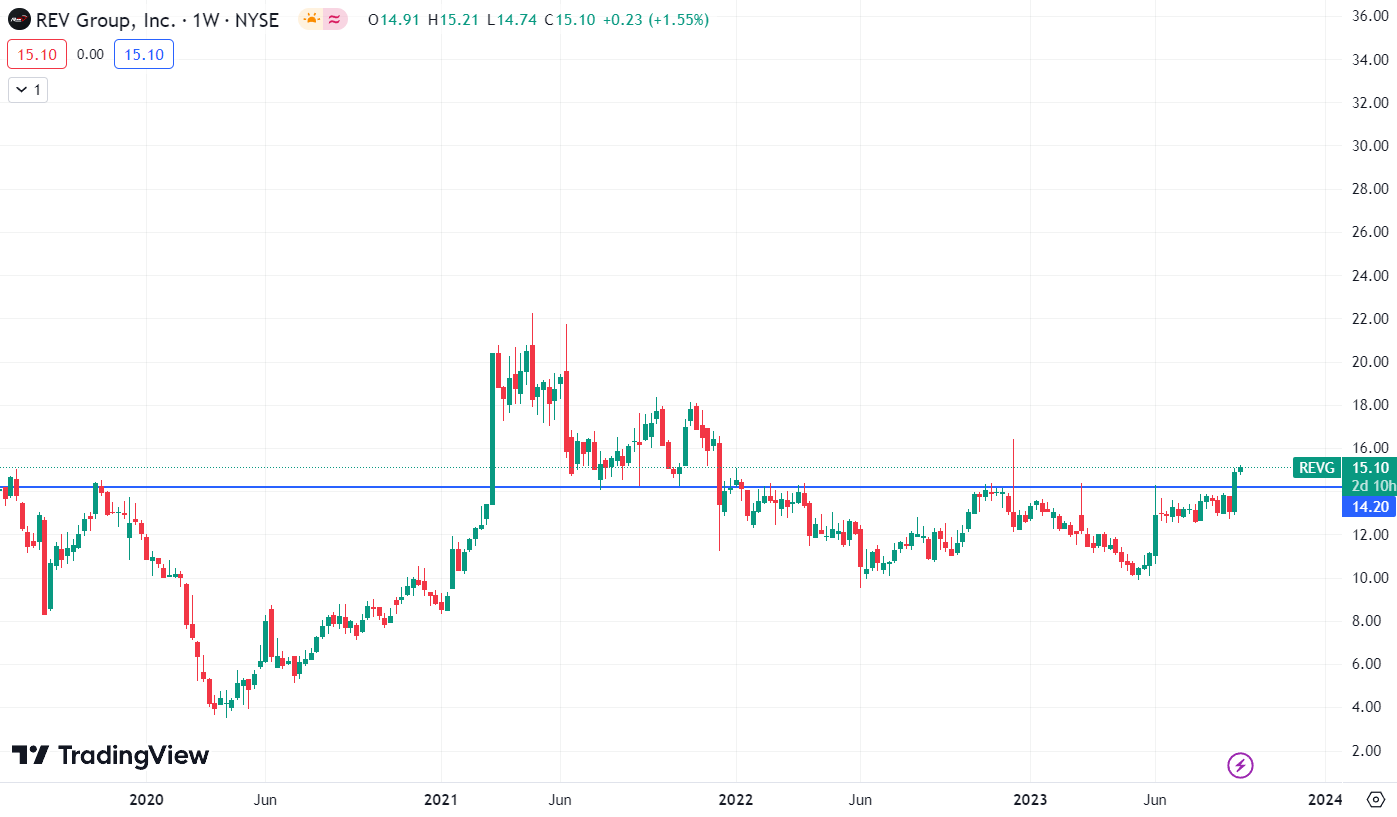

REVG is trading at $15.1. The chart of REVG looks quite solid, with a strong upside potential. There are two reasons why I think we might see an upward rally in the stock. First, the stock has given a range breakout, and second, there is a pattern change in the stock. Talking about the range breakout, it has broken an important resistance zone of $14, which the stock has tried to break five times since December 2021. The breakout is quite strong, and the chances of its success are quite high because if you look at the chart before giving a breakout, the stock consolidated for about four months near the $14 level. So, the chances of a successful breakout are high whenever there is a consolidation before a breakout. Now, talking about the pattern change, the stock went into a downtrend after giving a solid upward rally from 2020 to 2021 and started to form lower highs and lower lows. But recently, the stock failed to create a lower low, which indicates a potential trend reversal. So, considering these two factors, I am bullish on REVG.

Should One Invest In REVG?

The company reported solid quarterly results on 13 September, and the stock price gave a breakout in that week. It shows the market liked the results. Now, it is time to get smart and utilize this opportunity because I mentioned earlier that the company is on its way to reporting record annual sales. So, the outlook is quite positive, and looking at the price chart, I think the institutions and the smart investors have already started to take positions. This will be the right approach because I think the stock has great potential in the next three months. In addition, its valuation also looks attractive. When a company is performing well financially and its outlook is positive, the company generally trades at a higher valuation. But this is not the case in REVG. REVG is trading at a P/E [FWD] ratio of 12.87x, which is lower than its five average ratio of 19.58x and the sector ratio of 17.4x. REVG is trading at an EV / Sales [FWD] ratio of 0.42x compared to the sector median of 1.67x. So, even after performing well financially and with a positive outlook, it is trading at a lower multiple. I guess that's what being undervalued means, so that's why I think it can be a great, rewarding opportunity. Hence, I assign a buy rating on REVG.

Risk

They use a lot of raw materials in their production operations, and the prices of those resources depend on global supply and demand dynamics and other exogenous factors like ongoing inflation. Price changes for raw materials could have a negative impact on the outcomes. A substantial amount of aluminum, plastics, and other resins, fiberglass products, and a variety of other commodity-sensitive raw materials are bought by them each year, both directly and indirectly through component purchases. In particular, prices for steel and aluminum have fluctuated in the past with unanticipated and unexpected results. Furthermore, the U.S. government's planned or implemented tariffs and retaliatory tariffs could drive up the cost of components imported from foreign suppliers and certain commodities generally, independent of their country of origin. Although the company occasionally buys steel, aluminum, and other raw materials up to 24 months in advance in order to provide certainty regarding portions of their pricing and supply, they rarely enter into fixed-price contracts for the majority of their raw material purchases and may not be able to accurately predict future raw material prices for those inputs, including the effects of inflation. Over the last few years, commodity prices have changed a lot, and they might also do so in the future. Such changes might materially affect their cash flow balance sheets, and it might affect the comparability of their results across financial periods.

Bottom Line

I have a buy rating on REVG due to its strong financial results, bullish price action, and low valuation. The company is experiencing strong demand, and its fire & emergency segment backlog has increased significantly. So, I think this is the right time to enter the stock because I expect the company to report strong annual results.

For further details see:

REV Group: Might Be Rewarding In The Coming Times