REVG - REV Group: Speeding Up Amidst The Wagon War

Summary

- REV Group, Inc. had a fruitful FY 2022 with its impeccable performance.

- Its impeccable financial positioning may help it withstand a potential market slowdown.

- Market prospects this year are less robust, but opportunities are still present.

- Dividend payments have been unchanged over the years, but yields are decent.

- The stock price remains in a downtrend, making it cheaper.

REV Group, Inc. (REVG) remains a solid company amidst macroeconomic headwinds. Sustained revenue growth and stable margins highlighted its 4Q 2022 performance. Despite the lower shipments and supply chain disruptions, REVG outperformed the market. Even better, it maintains decent liquidity with its increasing cash and stable borrowings. It also earns enough to cover its operating capacity and borrowings without raising financial leverage. I last covered REVG stock in June 2022.

Moreover, dividend payments are consistent and well-covered. The values have been unchanged over the past decade, but yields are reasonable. Also, the stock price appears undervalued and offers an entry point for interested investors.

Company Performance

Macroeconomic headwinds intensified in 2022 as inflation peaked and set a new all-time high of 9.1% . It matched the ongoing geopolitical tension in Europe and supply chain disruptions across industries. All these factors drove the increase in prices of energy commodities. And even if many vehicles have gone electric, budget constraints and relative efficiency were some concerns. Thankfully, REV Group, Inc. remained unfazed in the face of these challenges.

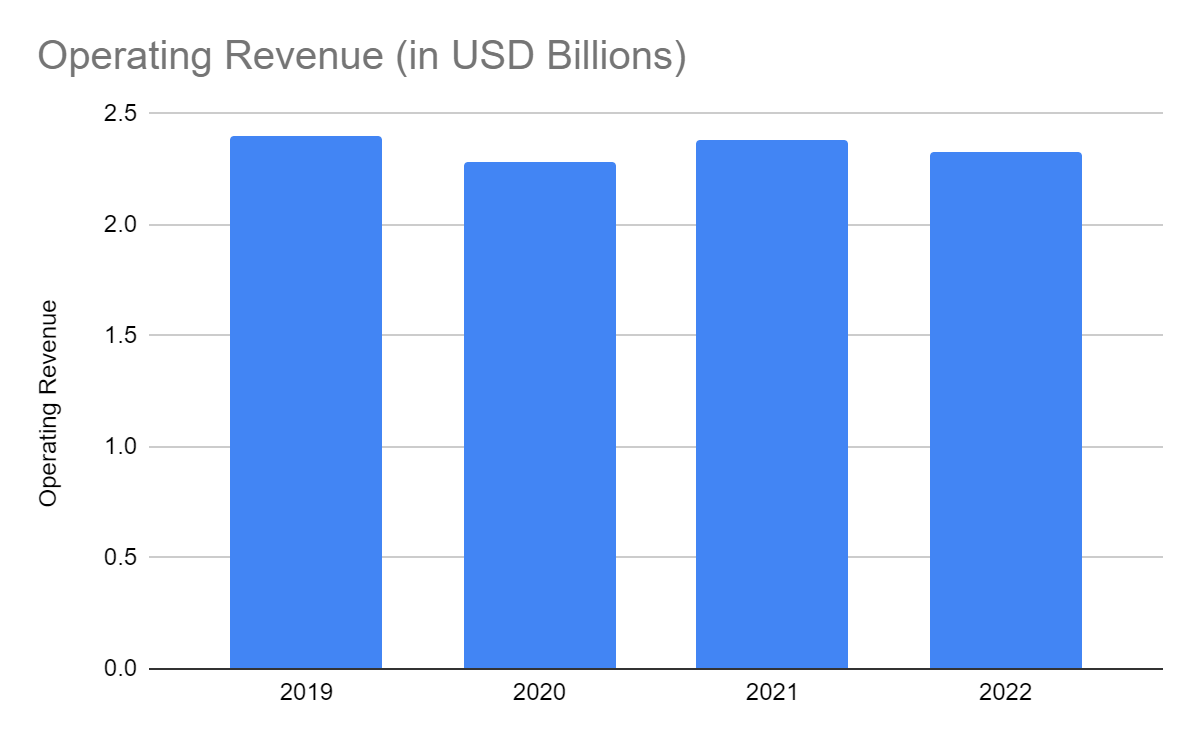

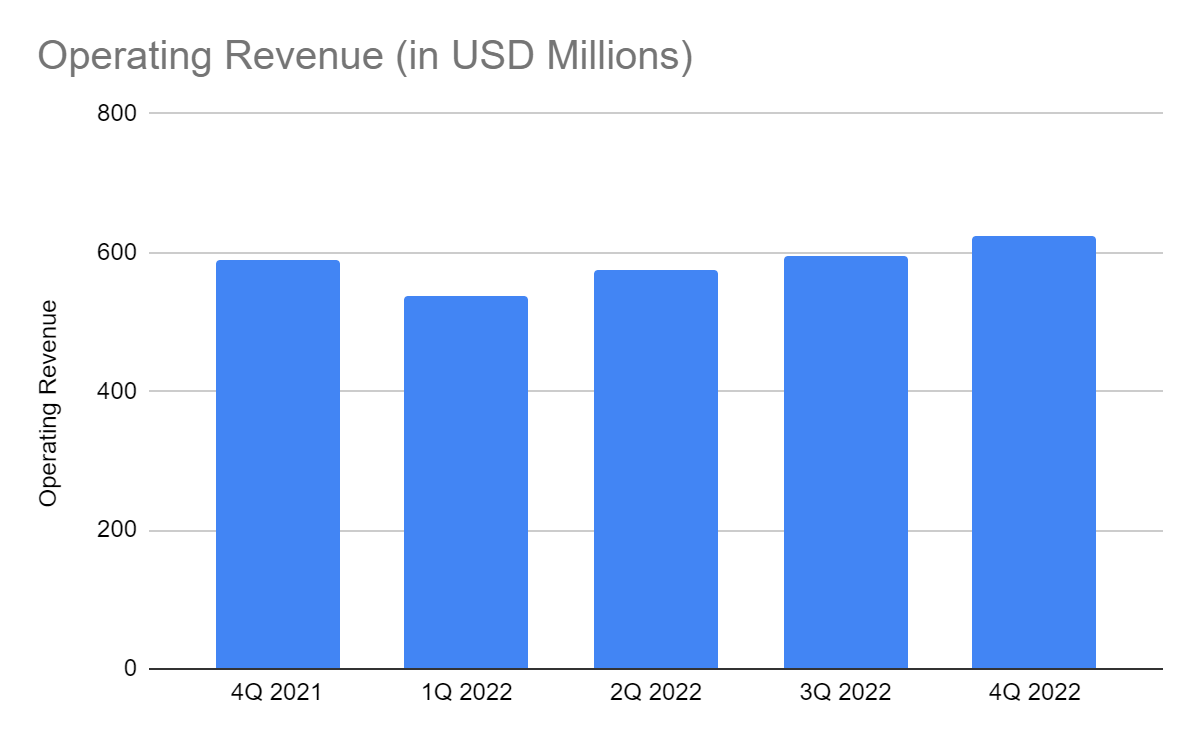

The operating revenue for FY 2022 amounted to $2.33 billion , a 2.1% year-over-year decrease. It was also 3% lower than 2019 levels. Some primary contributors were lower unit shipments, supply chain disruptions, labor constraints, and delays. Again, we can attribute this to inflationary headwinds and production inefficiencies. So it was logical to see lower revenues during the first half of its FY. But in the second half, a noticeable revenue rebound took place. Although insufficient to offset the weaker performance in 1Q and 2Q FY 2022, REVG remained promising. Its 4Q revenue was $624 million , a 6% year-over-year growth. We can see a consistent increase in the last four quarters. Thanks to REV’s flexibility to market changes. Its pricing strategy proved fruitful, offsetting the impact of inflation and normalization of inbound orders. Also, supply chain bottlenecks have started to ease. So it was easier to adjust its inventory levels compared to the first three quarters. But the increase was mainly driven by the commercial and recreational segments. In fact, recreational segment backlogs only amounted to $1.12 billion versus $1.24 billion in 4Q 2021.

Operating Revenue (MarketWatch)

{kind=link}

Operating Margin (MarketWatch)

{kind=link}

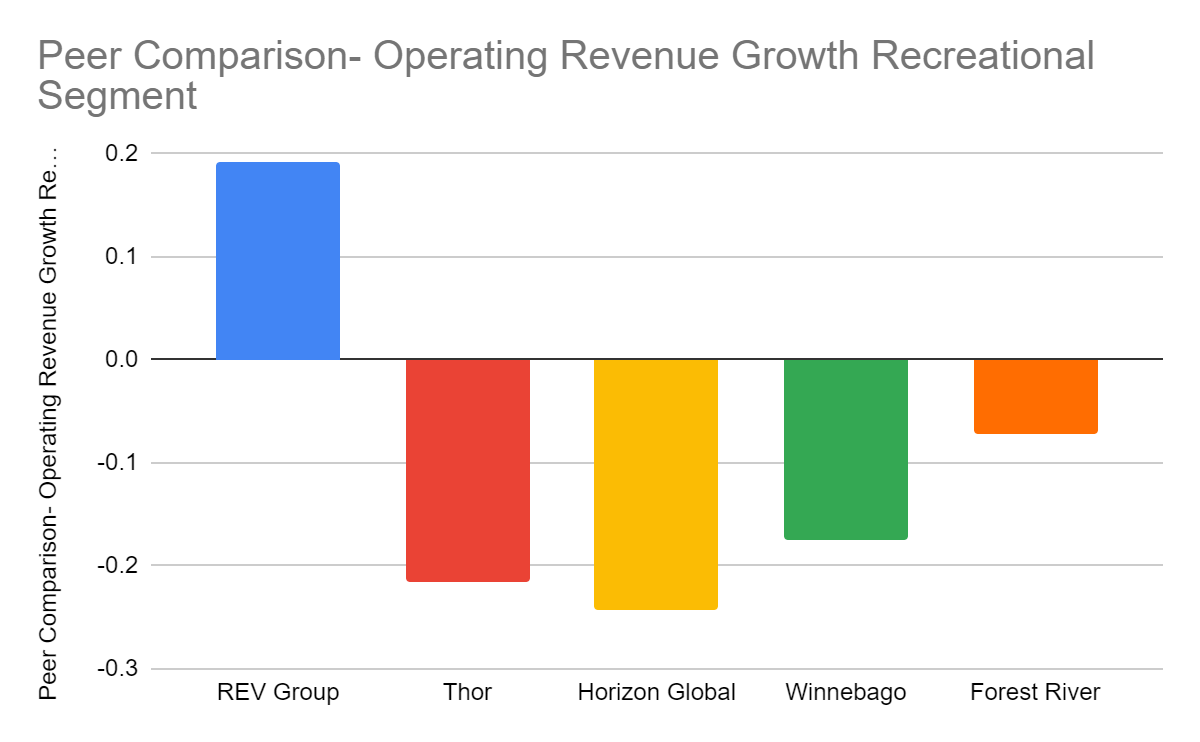

With regards to its peers, REV Group, Inc. proves it can go head-to-head even with larger companies. It still stands its ground, making it a durable RV (recreational vehicles) figure. I will focus on this segment since it shows the most massive increase. Also, it comprised 42% of revenues in 4Q 2022. Among the popular RV producers, THOR ( THO ) and Forest River ( BRK ) remained the most prominent manufacturers and distributors. Winnebago ( WGO ) also remains a massive company. Meanwhile, REVG and Horizon Global ( HZN ) were dwarves amidst the giants. Despite this, REV Group, Inc. has outperformed the market in 4Q. It had the highest recreational segment revenue growth of 19%. It was also the only company that had a higher revenue.

Operating Revenue Growth (MarketWatch)

{kind=link}

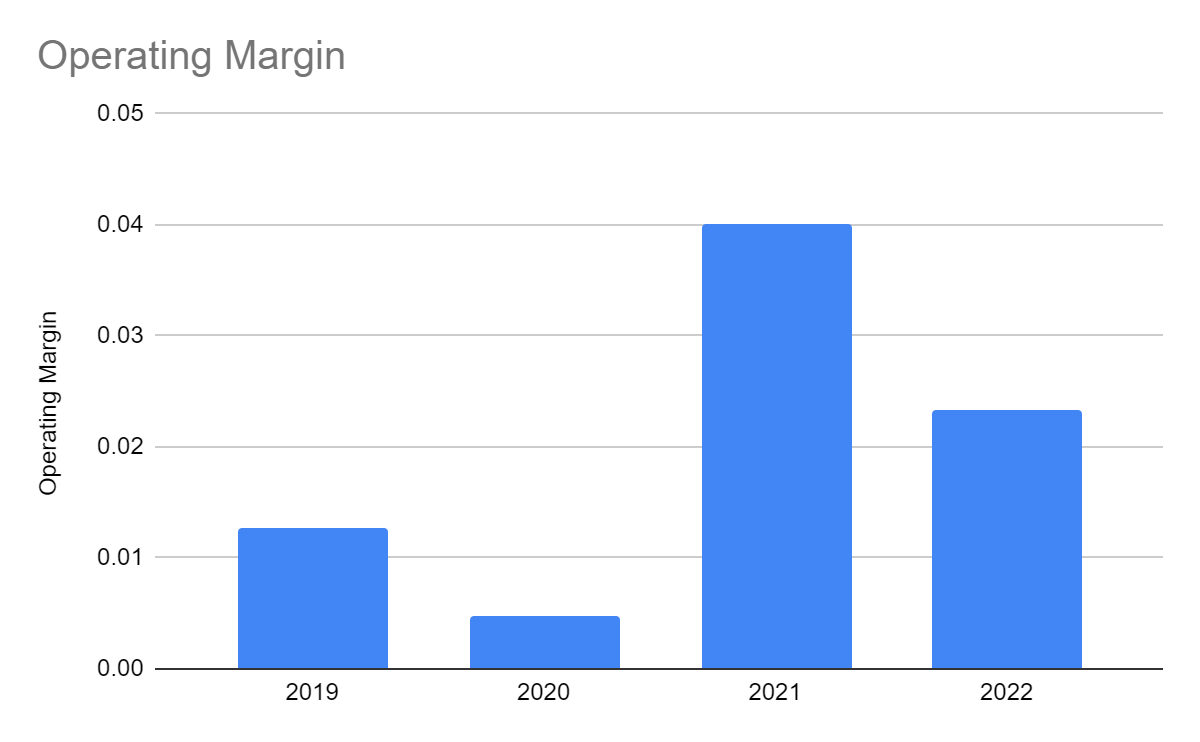

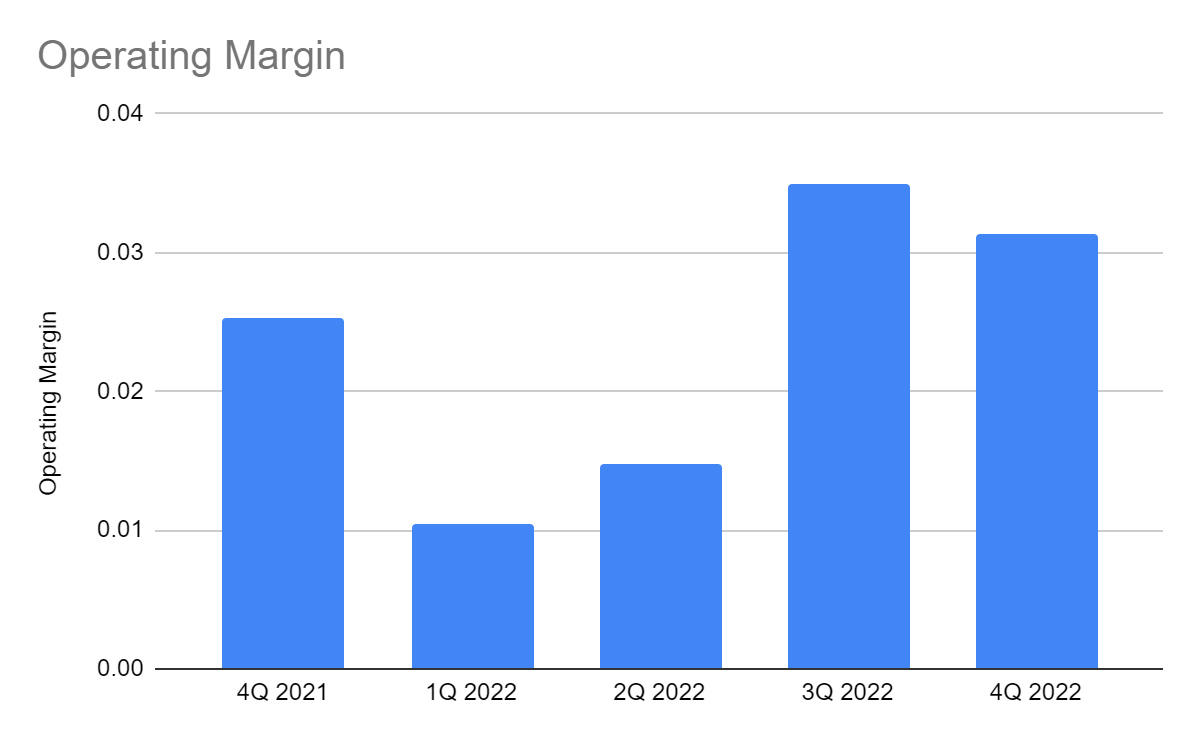

Meanwhile, costs and expenses were stable, which stabilized its viability. Indeed, REVG made up for the lower shipments and supply chain disruptions through operational efficiency. The operating margin in 2022 remained stable at 2.3% versus 1.3% in 2019 and 4% in 2021. Meanwhile, its 4Q operating margin reached 3.2% versus 2.5% in 4Q 2021. It shows that pricing strategies helped sustain revenue growth and offset increased expenses. Also, the lower backlogs in the recreational segment improved its inventory levels. It was able to stabilize costs and expenses. We can also attribute it to the relaxing inflation, which dropped to 7.8% at the end of the fiscal year.

Operating Margin (MarketWatch)

{kind=link}

Operating Margin (MarketWatch)

{kind=link}

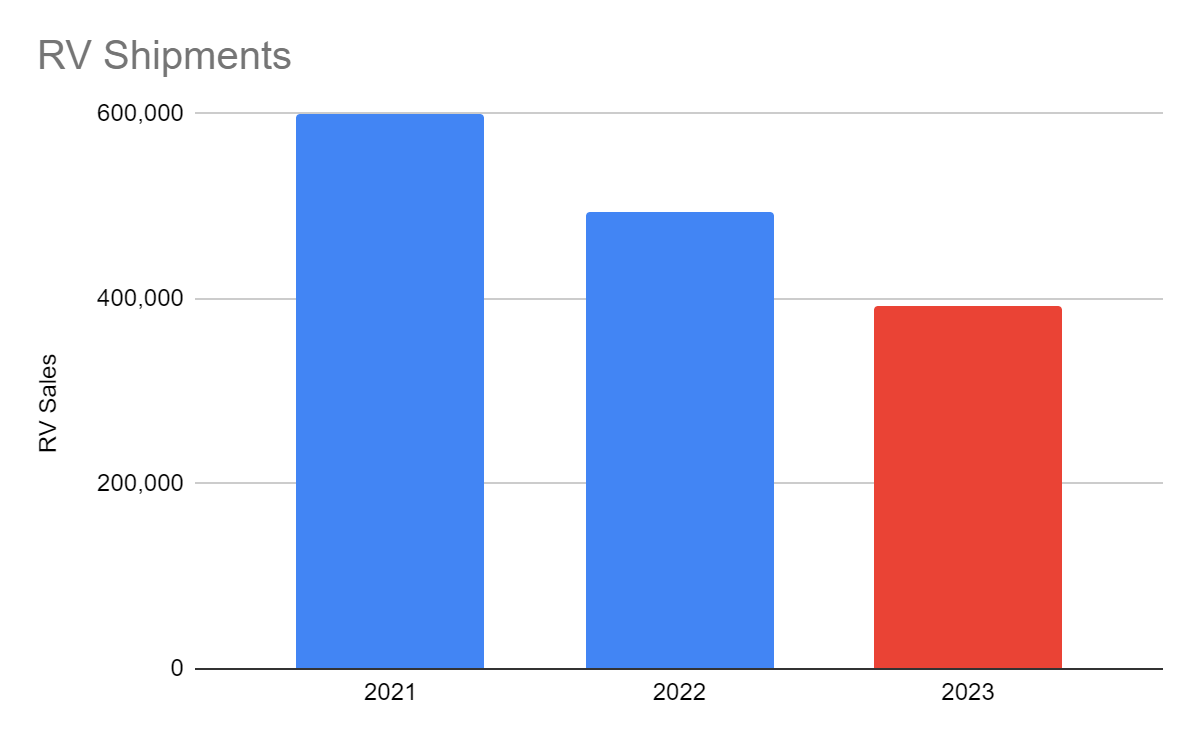

This year, we anticipate more challenges as market demand softens. Shipments continue to decrease, which may lower the operating revenue. In 2022, the number of RV shipments reached 493,268 . Although it was the third-best year on record, the 18% decrease must be considered. But the current trend is logical since it conveys the normalization of demand. According to the Recreational Vehicle Industry Association, shipments may decrease further to 379,000-404,000 units. Despite this, I am optimistic about REV Group’s performance this year. It may not be as robust as in 2022, but I expect it to fare well.

{kind=link}

How REV Group, Inc. May Still Fare Well This Year

We saw how REV Group, Inc. coped with macroeconomic headwinds in 2022. It was successful at stabilizing revenues and margins. Despite the decreasing shipments, it can work on improving efficiency. After all, inflation is now only 6.4% and may continue to decrease as the Fed remains conservative. Gasoline prices are now only $3.501 per gallon versus the 2022 peak at $5.032 per gallon. These external factors may cause a slight uptrend in shipments or allow the companies to set more favorable prices.

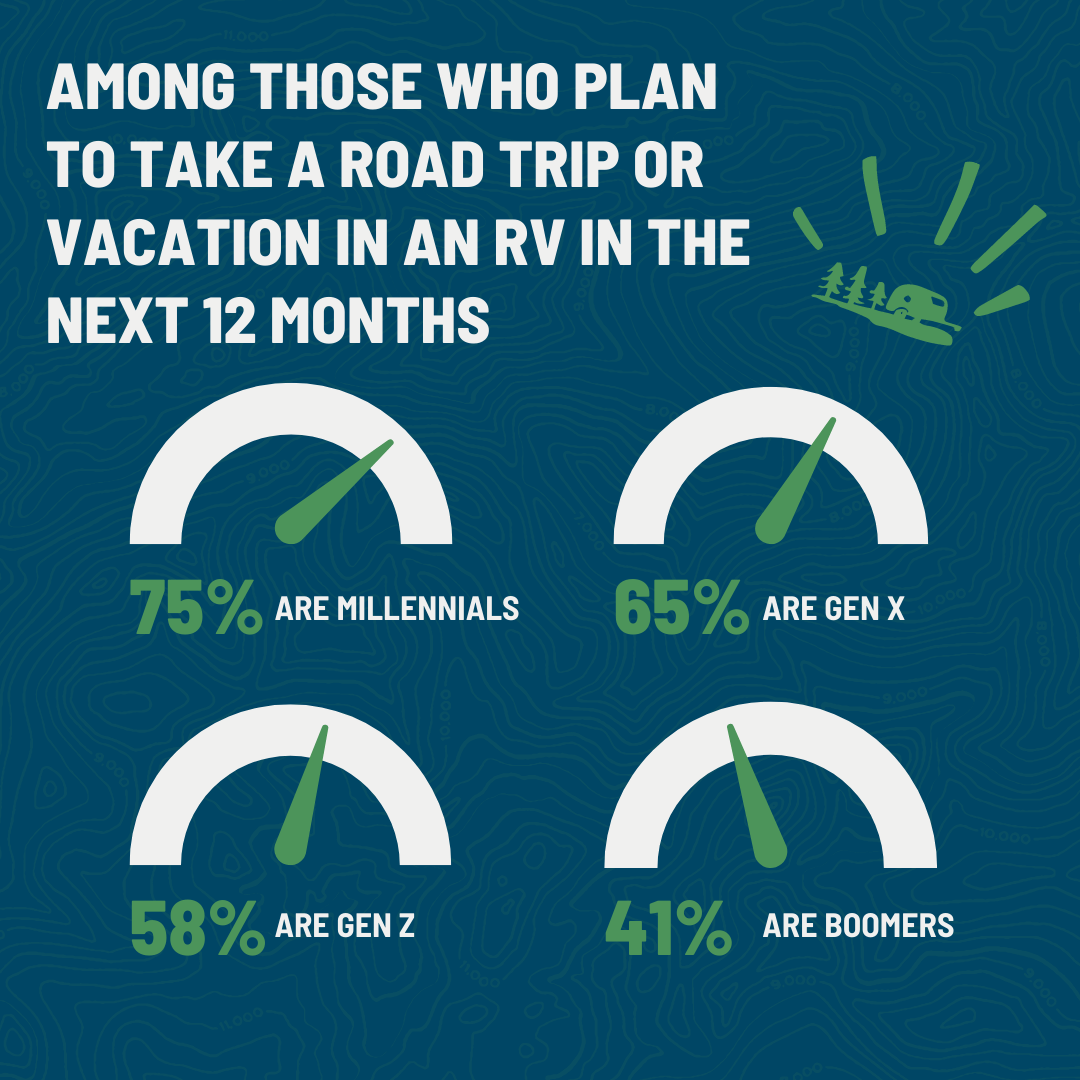

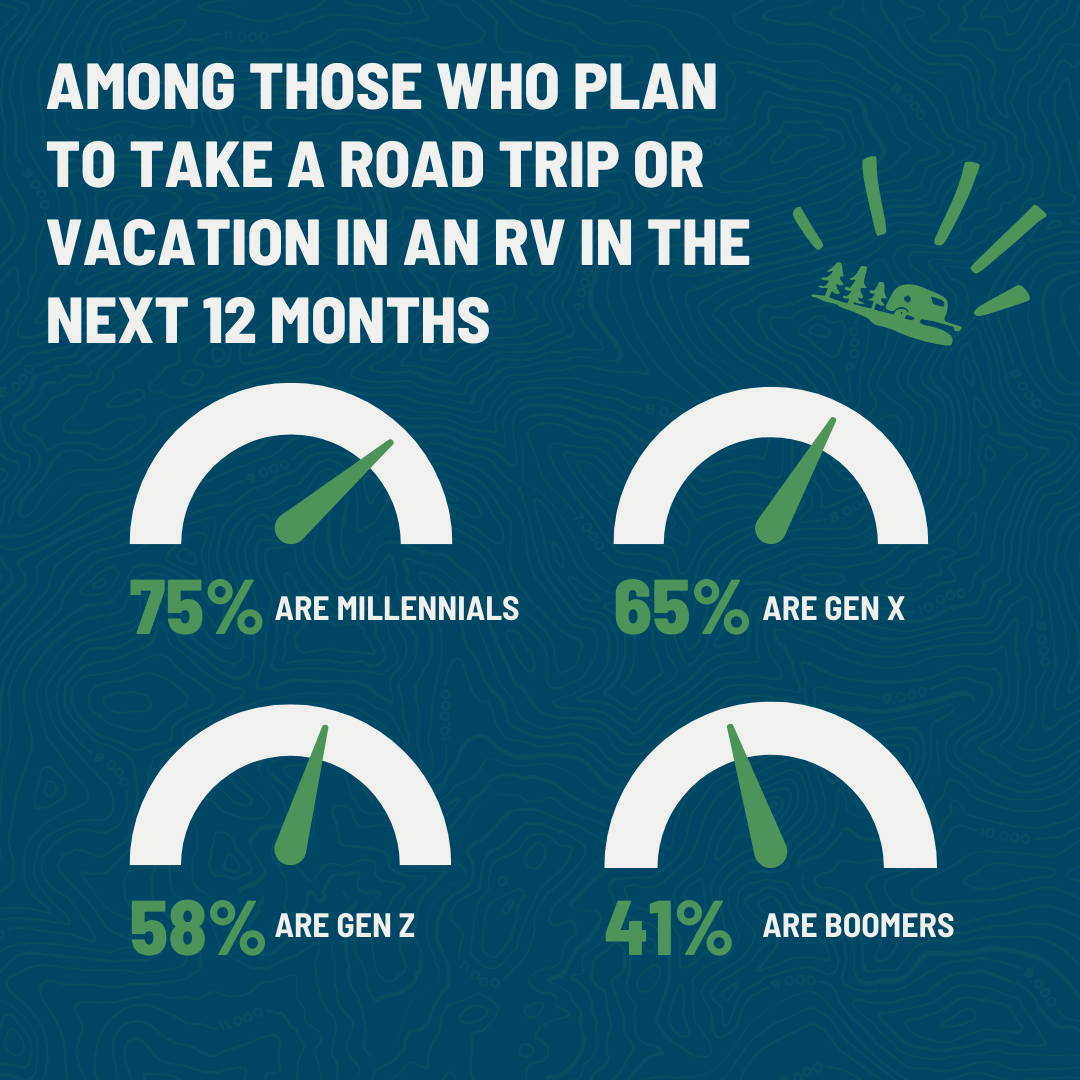

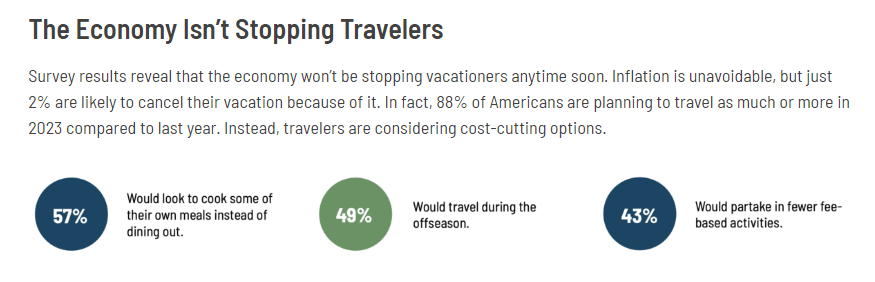

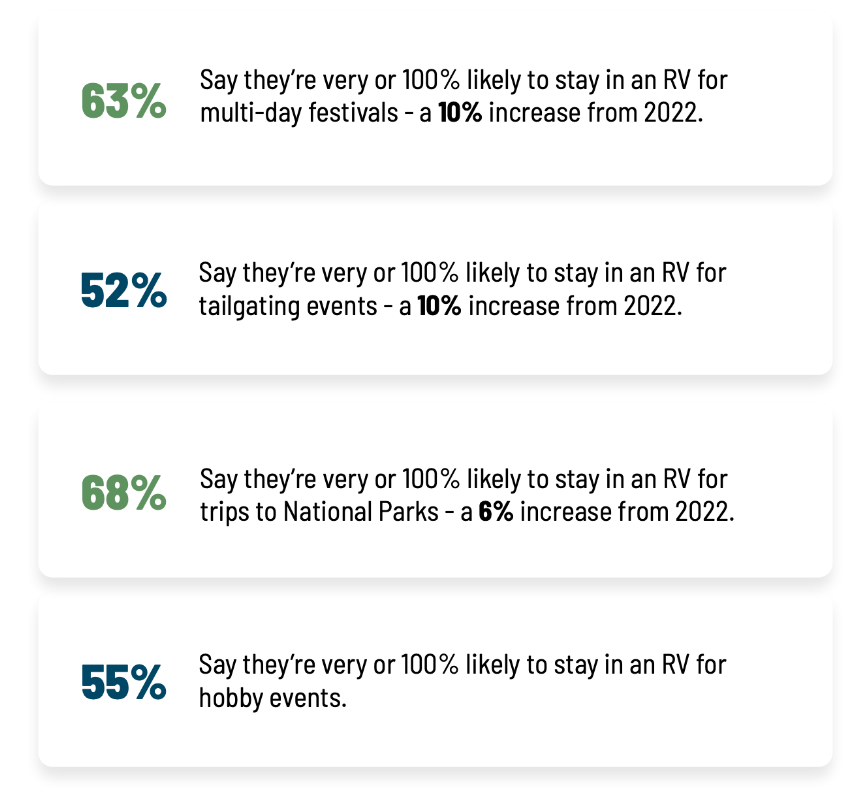

Moreover, travel budget constraints are changing the itineraries of many travelers. Although there is an increased interest in international travel, many Americans are eyeing RVs. It may be higher between spring and summer. A recent survey shows that 37% of American travelers plan to go on an RV trip this year. Work flexibility due to hybrid and remote setups remains their top reason. The percentage is higher for those who already have RVs. Others opt to rent or borrow RVs. Among the popular leisure travel destinations, the National Park tops the list with RVs as the best option. More interestingly, Millennials have the highest preference for RVs. The thing is, RVs are still one of the go-to options for travelers across all age groups. In the infographics below, we will see other important trends we can expect for RVs.

Travel Trend (RVshare) RV Trip Demographics (RVshare) Economy And Travelers (RVshare) RV Travel Plans 2023 (RVshare)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

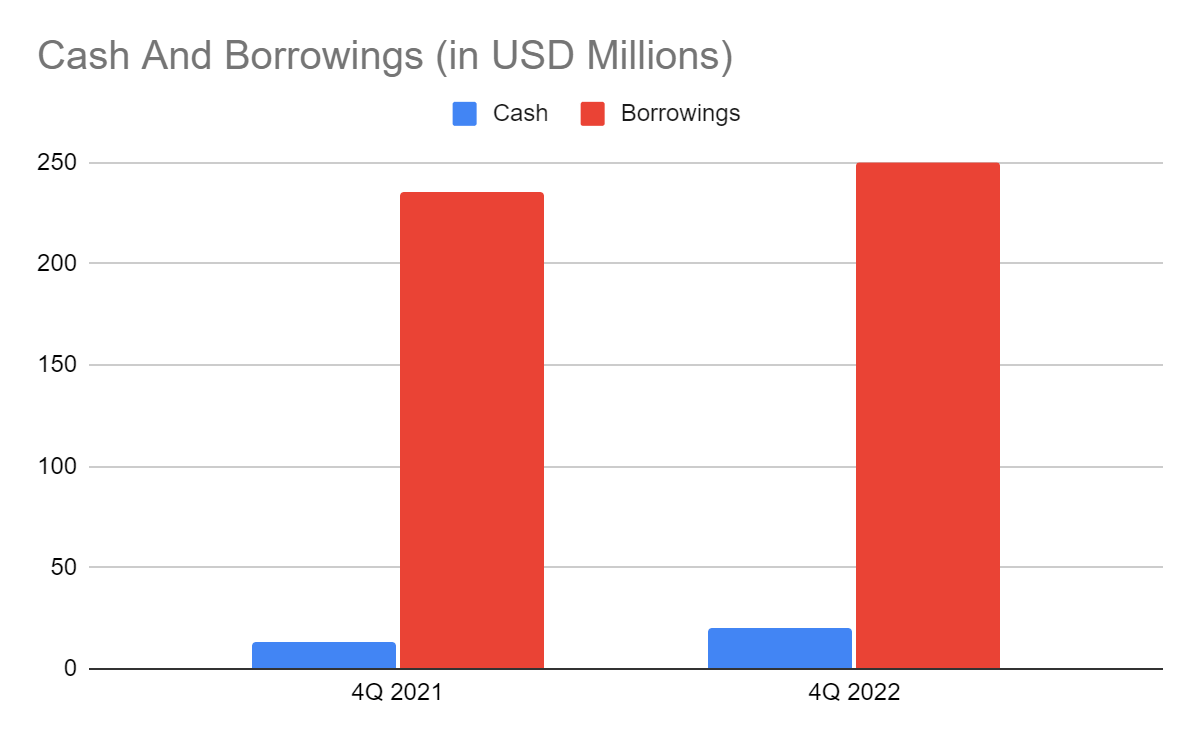

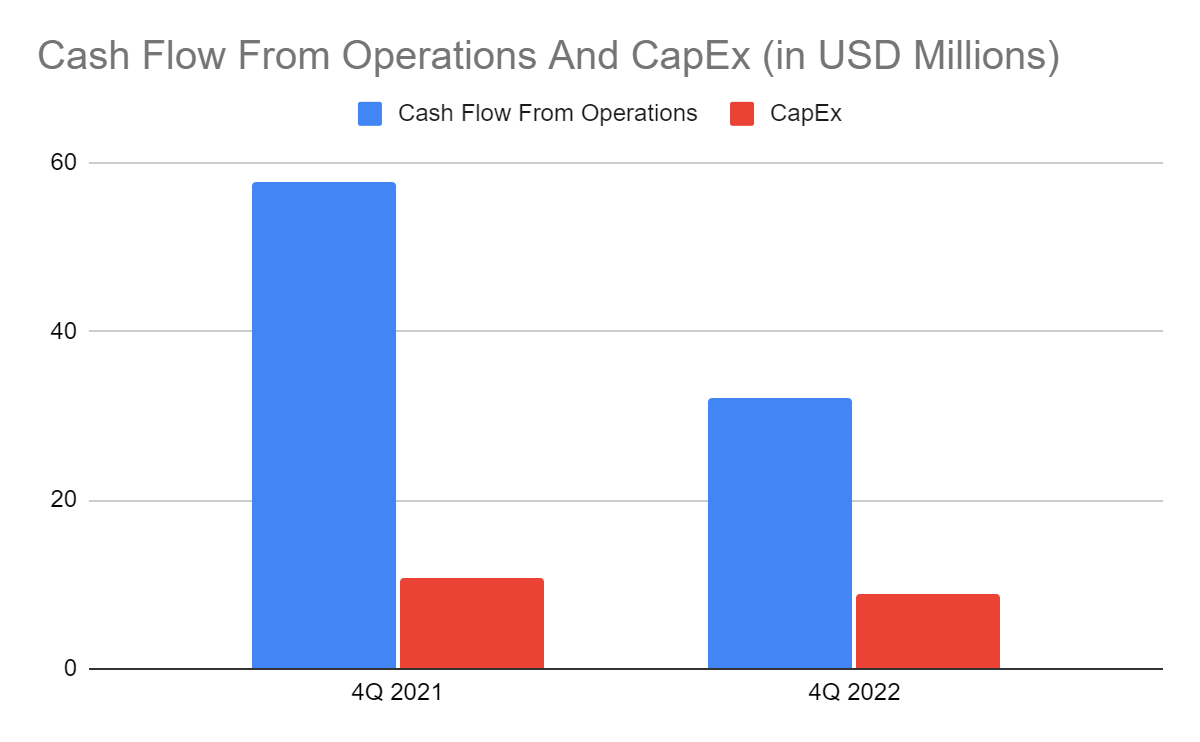

What makes REV a solid company is its decent liquidity position. Cash and borrowings are both increasing at stable levels. Even better, its Net Debt/EBITDA Ratio is only 2.7x, suitable for a capital-intensive company. Indeed, it earns enough to cover its borrowings. It may not have to raise its financial leverage to sustain its operating capacity. We can confirm it using the cash flow from operations that is more than thrice its CapEx. Its cash inflows are more than enough to cover its operations, repay borrowings, and distribute dividends.

Cash And Equivalents And Borrowings (MarketWatch)

{kind=link}

Cash Flow From Operations And CapEx (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of REV Group, Inc. has been in a continued downtrend for more than a year. It may be logical, given the less robust view of the RV industry. At $11.64, the stock price has already been cut by 13% from last year’s value. But this shows an opportunity to buy the stock at a discount. The PB Ratio shows potential undervaluation. The current stock price and BVPS of 7.69 gives a PB Ratio of 1.51x, lower than the average of 1.7x. If we use the current BVPS and the average PB Ratio, the target price will be $13.08.

Meanwhile, dividend payments have been consistent over the years. It has a dividend yield of 1.57%, higher than the S&P 600 average of 1.24%. It may not be high, but still decent if we compare it to larger companies like THO with 1.98% and WGO with 1.7%. To assess the stock price better, we will use the DCF Model.

FCFF $76,400,000

Cash $20,400,000

Borrowings $250,300,000

Perpetual Growth Rate 4.2%

WACC 9.2%

Common Shares Outstanding 59,324,000

Stock Price $11.64

Derived Value $15.09

The derived value adheres to our supposition of potential undervaluation. There may be a 30% upside in the next 12-18 months. So, investors may consider the current stock price a potential entry point to buy shares.

Bottomline

REV Group, Inc. remains successful at stabilizing revenues and margins with its pricing strategy and popularity amidst market headwinds. Although lower shipments may affect sales volumes, the relaxing inflation and fuel prices may provide more room for price adjustments. Its solid Balance Sheet, matched with stable cash inflows, makes it sustainable. Moreover, it continues to pay dividends with decent yields. Also, the potential undervaluation is seen in both price metrics. It may be an ideal entry point for interested investors. The recommendation is that REV Group, Inc. is a buy.

For further details see:

REV Group: Speeding Up Amidst The Wagon War