SPNT - Revisiting SiriusPoint Common And Preferred

2024-01-22 00:30:05 ET

Summary

- SiriusPoint's preferred units have shot up nicely in recent months, generating strong returns for shareholders.

- SPNT's financial health has improved, with increased profits and a decline in some activities.

- The common units are still rated a 'buy' due to increased profitability, but the limited upside that remains necessitates a downgrade for the preferred units.

Every investor has their own approach to investing and their own preferences. As an example, I almost always prefer common shares of a business over preferred units. Yes, preferred units do often bring with them fairly attractive distributions. They are also technically safer than common shares and are less volatile. For many investors, particularly those in retirement or nearing retirement, these types of opportunities can be considered superior to calm in the units.

Despite my general preference for common shares, I do sometimes come across an opportunity in the preferred space that just makes sense. A fantastic example of this can be seen by looking at SiriusPoint ( SPNT ) ( SPNT.PR.B ), a global underwriter of insurance and reinsurance products. Back in May of 2023, I wrote an article covering both the common units and the preferred units, with a special focus on the preferred ones. I ended up rating the common units a 'buy' while rating the preferred units a 'strong buy'. Improved financial health for the company, combined with a discount that preferred units were trading relative to their liquidation preference, led me to this conclusion.

Since then, things have gone quite well. While the S&P 500 has jumped 14.9%, the common units have seen upside of 22.1%. The preferred units have underperformed slightly, with a total increase, including distributions, of 13.9%. But considering how uncommon it is for preferred shares to see significant upside or downside, I consider this a win. With this move higher, I have decided to reevaluate the picture. Based on my assessment of the company as a whole, I still believe that SiriusPoint makes for a solid 'buy' prospect. But because of the truly limited upside now associated with the preferred units, I am downgrading them from a 'strong buy' to a 'buy'.

SiriusPoint continues to look strong

Looking at the picture purely through a fundamental lens, it's not difficult to see why shares of SiriusPoint have appreciated. We have seen a decline in some of its activities. But at the same time, profits have increased nicely. As an example, during the third quarter of the 2023 fiscal year , the company had gross premiums written of $758.8 million. That's down from the $843.8 million reported one year earlier. This $117.8 million drop was intentional as the company focused less on international reinsurance operations, especially when it comes to property lines.

{kind=link}

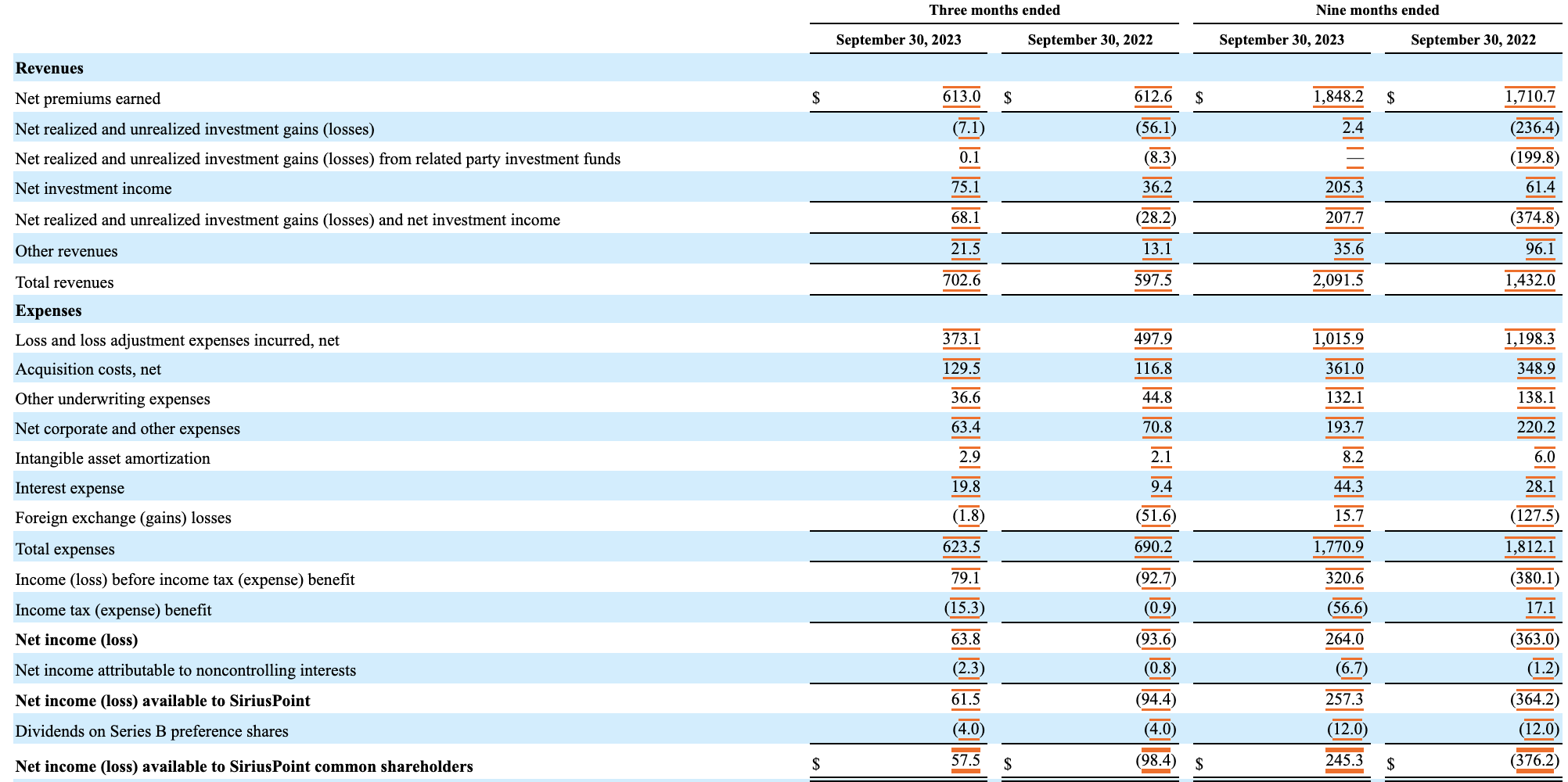

The restructuring initiatives that the company launched in November of 2022 focused on reducing the locations from which the company underwrites property catastrophe reinsurance policies. This led it to announce Closings in Hamburg, Miami, and Singapore. The firm is also reducing its physical footprint in both Liege and Toronto. The ultimate goal is to shrink its entire property catastrophe underwriting business to a single location. And that would be Bermuda. The company has also been making other moves such as de-risking its investment portfolio so that it looks more in line with what the rest of the industry does. Add on top of this the fact that the company is benefiting nicely from a rise in interest rates, and it should be no surprise that even as net premiums earned remained almost flat in the third quarter compared to the same time one year earlier, that net profits of $61.5 million dwarfed the $94.4 million loss reported the same time one year earlier.

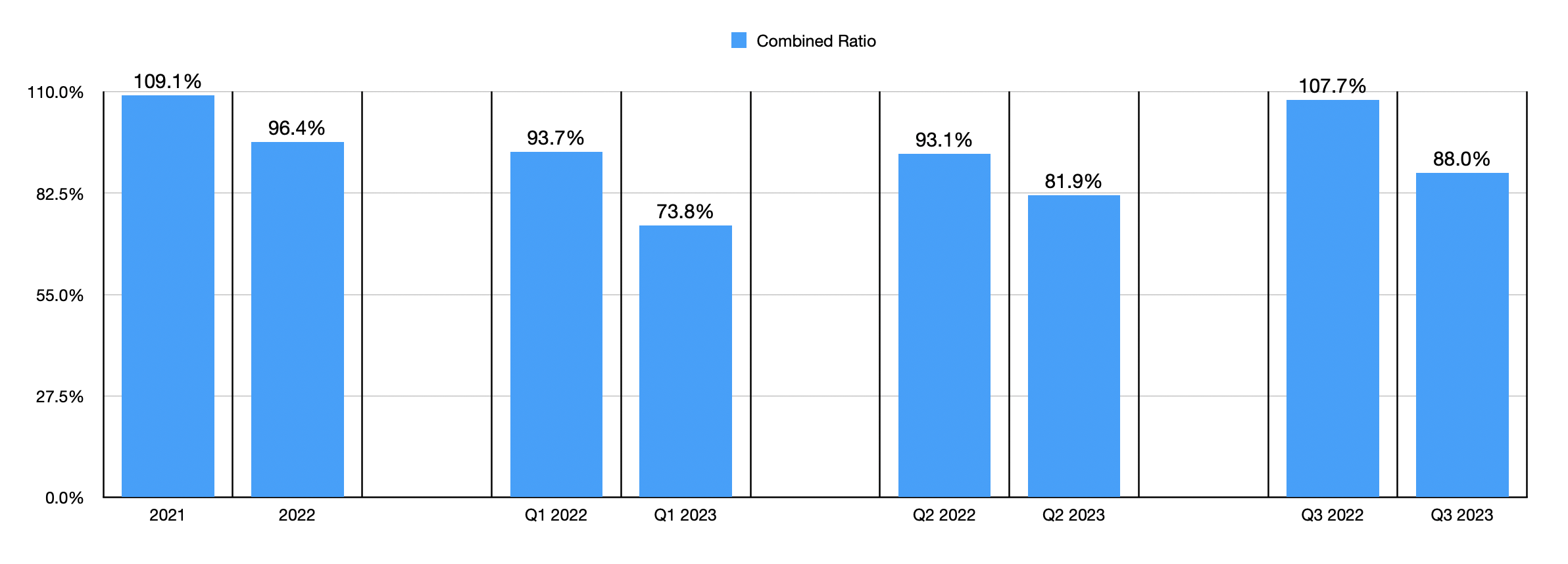

The interest rate picture will not be here in the long run. So investors shouldn't get used to that. Instead, the primary focus should be on the health of the underlying insurance business. The best way to do this is to look at the picture through the lens of the combined ratio. This is a measure of whether the insurance company is successfully earning more in revenue from the premiums it collects than it is ultimately paying out. As you can see in the table below, the combined ratio for the company has consistently shown improvements on a year over year basis. As of the third quarter, this number was 88%. That's down from the 107.7% seen at the same time last year.

{kind=link}

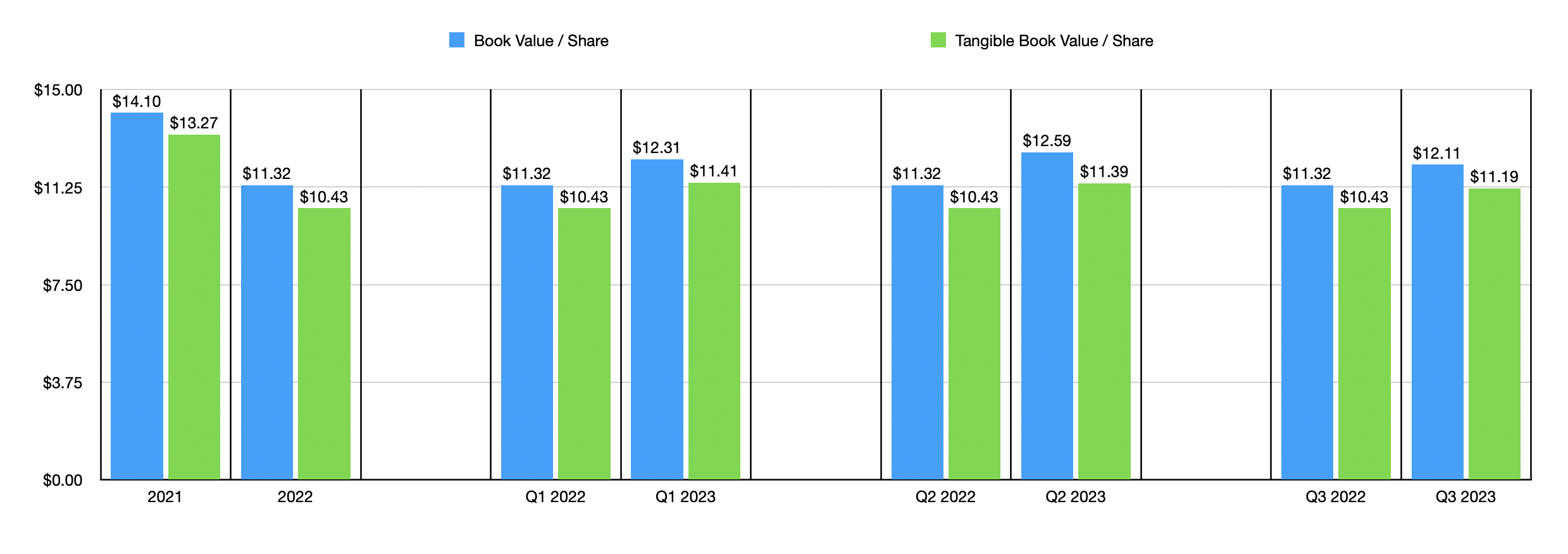

The data shown for the third quarter of the year is not all that we have to go off of. In the second quarter, the combined ratio was 81.9%. That's a drop from a 93.1% seen one year earlier. And from the first quarter, we saw a drop as well. Outside of the combined ratio, there's also the topic of the book value per share. Although this number did drop from $12.59 in the second quarter of this year to $12.11 in the third quarter, and even though tangible book value per share followed a similar trajectory from $11.39 per share to $11.19 per share, the fact that these are all up year over year is promising.

This is exactly the kind of progress you want to see in a business of this nature. As for what this means for the stock, my belief is that both the common units and the preferred are healthy. For starters, the common units trade at $10.99 as of this writing. That's below both the book value per share and tangible book value per share, as is common in the insurance space. When it comes to the preferred units, the only thing that matters is that the company can cover all of its costs and payments to any securities that might be senior. On this front, the company currently has no problems. Net profits attributable to common shareholders in the latest quarter totaled $57.5 million. That's up from the $98.4 million loss seen one year earlier. For the first nine months of the year, profits of $245.3 million significantly beat out the $376.2 million loss reported one year earlier.

{kind=link}

Takeaway

At the end of the day, I have decided to downgrade the preferred units of SiriusPoint. This is because, even in spite of attractive fundamental performance, they likely don't have any significant upside from here. As of this writing, they can be purchased for $25.12. They were at $22.94 when I wrote about the company last year. Add on top of this the fact that they only have a liquidation preference of $25, and we now have a company that should be trading a bit lower and that has an effective yield of 7.96% compared to the 8% based on the liquidation preference. This is still hefty, but without a high likelihood of rising much further, a 'buy' rating now makes sense. As for common units, the increases in profitability are definitely reason enough to be optimistic. So for that, I am keeping the company rated a 'buy'.

For further details see:

Revisiting SiriusPoint Common And Preferred