RFM - RFM: Better Valuation But Not Great Prospects

Summary

- RFM is at a much better valuation, but the fund also has a lot of negatives.

- They've changed their managed distribution plan so that the hit to the payout this year was lower.

- Expect further pressure as long as interest rates are being hiked by the Fed.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 7th, 2023.

We've covered several of the RiverNorth municipal bond-related funds at one time or another. Today, we are looking at RiverNorth Flexible Municipal Income Fund ( RFM ) for an update.

The discount for this fund has opened up to touching double digits, a big drop from where it was before. Additionally, it could be a more interesting place to consider investing now that municipal bonds got hit hard in 2022 by rising interest rates.

However, remember that this fund is highly leveraged and holds other closed-end funds within its portfolio. That means we are getting leverage on leverage and fees on fees - but also discounts on discounts potentially. It ends up trading as volatile as a high-yield bond fund.

Since our last update , shares have dropped further than the S&P 500. On a total return basis, it did manage to reduce those losses. A good portion of this was simply from discount widening as well. While the S&P 500 isn't an appropriate benchmark, it can give us some context on how this fund has been performing.

RFM Performance Since Prior Update (Seeking Alpha)

Another important note before getting into this fund is that they've recently filed an N-2 . This form is filed when they want to issue new shares. This can come in several ways, allowing for a dividend reinvestment plan or an at-the-market offering. However, it's sometimes more disruptive to the funds through a secondary or rights offering.

When those are announced, shares are often sent lower by a significant amount. At such a large discount already, a rights offering wouldn't make sense, but rights offerings aren't generally in the best interest of shareholders anyway. It is only beneficial if it is done so at a premium to their NAV. Though, some could try to argue that it increases the fund's size, which should lead to greater trading volume. Either way, it benefits the managers in the end as AUM increases. Rights offerings for this fund sponsor aren't unusual.

On the other hand, one way that investors may benefit from more shares coming is if it is preferred shares. The fund could get fixed-rate financing and replace that with its floating-rate credit facility by issuing preferred shares. Ideally, this would have been done a year ago when rates were much lower. RiverNorth has other CEFs that implement preferred shares as leverage, so it isn't unusual for this sponsor.

The Basics

- 1-Year Z-score: -1.40

- Discount: 10.08%

- Distribution Yield: 7..41%

- Expense Ratio: 2.17%

- Leverage: 44.82%

- Managed Assets: $196.7 million

- Structure: Term (anticipated liquidation date on March 26th, 2035)

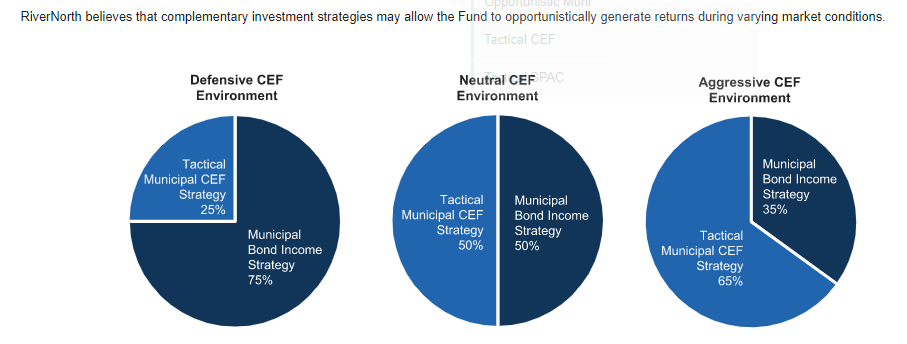

RFM's objective is to "provide current income exempt from regular U.S. federal income taxes with a secondary objective of total return." They do this by investing in a hybrid approach with MacKay. They divide the portfolio into individual muni and muni CEFs. RiverNorth managers are investing in the CEF sleeve and MacKay in the individual sleeve. They then take an active approach to the weightings depending on the current environment for CEFs.

RFM Hybrid Approach (RiverNorth)

{kind=link}

The fund is relatively small, with less than $200 million in assets. That's with a high amount of leverage being employed on top of it. This can cause issues for larger investors if they want to get out of the fund quickly. However, the leverage itself isn't unexpected as they invest in what should be some of the safest assets. We have to consider that when they are holding other CEFs, they are also leveraged. So it's doubled-up leverage as other muni CEFs ramp up their leverage significantly, too.

That also means doubled-up fees on an expense ratio that's already quite elevated at 2.17%. Pushing it to these above-average expenses is the hefty 1.40% management fee.

When including leverage expenses, it comes to 2.58%. That can make it quite difficult for the fund to generate returns when considering the underlying CEFs. Some of the capital is operating with expenses at around 4% or higher. It could even be up to 7 or 8% when considering the underlying leverage expenses since leverage costs have exploded higher. Therefore, it is a bit about relying on the managers to be quite successful in their strategy by investing in income-producing munis and realizing gains.

With interest rates rising, their leverage expenses are also rising. They borrow at the overnight bank funding rate plus 90 basis points. At the end of June 30th, 2022, their interest rate was 2.37%. With rates only going higher since leverage expenses have only gone higher. The OBFR at the last look was 4.32%, so their leverage would now cost them 5.22%.

Fortunately, to offset some of those higher expenses were the future contracts that they went short on U.S. Treasuries.

RFM Realized/Unrealized Gains (RiverNorth)

Performance - Attractive Discount, Not Attractive Results

The fund isn't all that old, with its inception in 2020. Interestingly, RiverNorth puts out one of these funds that are investing highly similarly almost annually now. Here are the results for RMM.

RFM Annualized Returns (RiverNorth)

{kind=link}

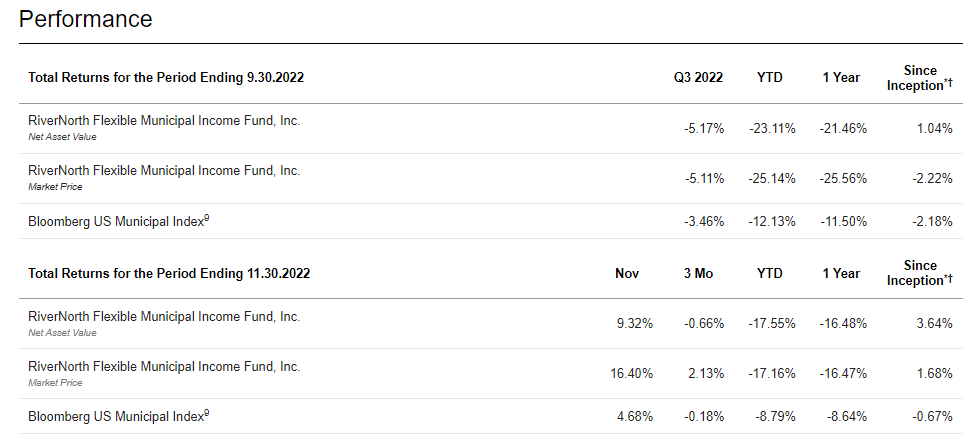

The fund has shown that since its inception, they've been able to top out the Bloomberg US Municipal Index. However, the latest results have the fund falling far short in the one-year period. This wasn't just on a market price basis but also on a NAV basis.

One of the reasons for this is that CEFs had their discounts widened out substantially through 2022's volatile year. So that put added pressure on the underlying portfolio of RMM - even if the underlying portfolio of those positions was holding up better.

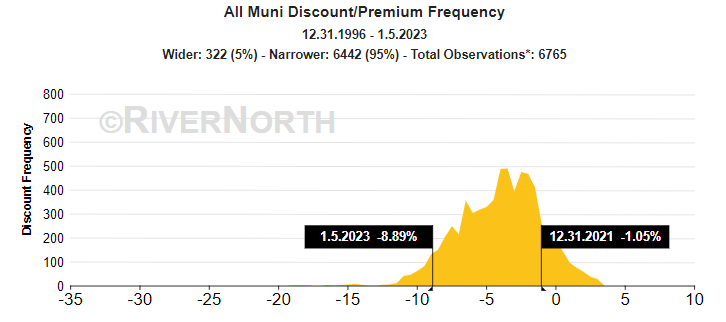

As of the latest figure, muni CEFs have an average discount of nearly 9%. That's from starting 2021 at an incredibly shallow ~1% discount.

CEF Muni Discount/Premium (RiverNorth)

{kind=link}

With an estimated hedged duration of 7.42 years, that is certainly going to take a hit when interest rates rise too. That means that for every 1% increase in interest rates, RFM's underlying portfolio should fall 7.42%. Thankfully, it didn't end up happening that way in practice, or the results would have been even direr.

So the overall results of RFM haven't been pretty. And again, going forward, it could be difficult now that leverage costs are out of control, and that's on top of their elevated management expenses.

However, the fund has a glimmer of attractiveness, even if ever so small. It is taking the combination of those highly discounted muni CEFs and their in RMM's portfolio, which is also highly discounted at the moment.

Besides the COVID crash, we have the fund trading near the bottom end of its discount range since its launch.

Ycharts

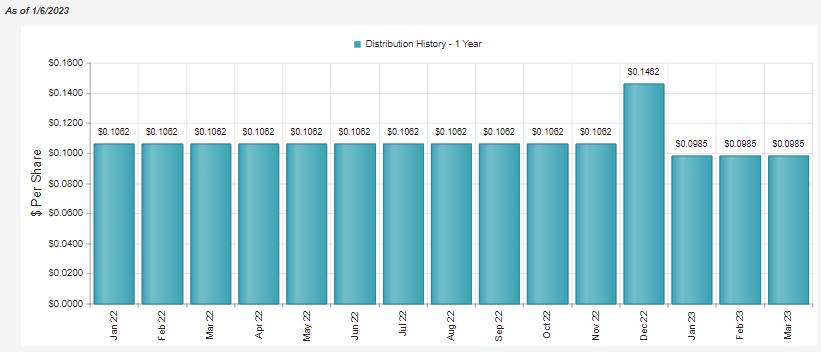

Distribution - Managed Distribution Plan Adjustment

Another factor that could be seeing shares fall to a deeper discount is their latest adjustment to their annual distribution. It resets annually, so if NAV falls, its payout goes lower and vice versa.

However, what these sly managers did was take their managed distribution plan from 5.5% to now 6.75%, so the cut wouldn't be as drastic.

This was the previous language in distribution press releases :

In accordance with its level distribution policy, RMM's annual distribution rate has been set equal to 5.50% of the of the Fund's NAV per common share as of the final trading day of the preceding calendar year.

And here is the new language in the latest distribution press release :

In accordance with its level distribution policy, RFM's annual distribution rate has been set equal to 6.75% of the average of the Fund's NAV per share as reported for the final five trading days of the preceding calendar year.

That could be a positive, though, as it meant the cut was much more shallow. It also could reflect the nature that yields have risen after interest rates have been hiked. The longer-term impact of this is that it could erode the fund faster. It also means they are willing to change what is supposed to be a predictable formula at will.

RFM Distribution History (CEFConnect)

{kind=link}

While that might be the case that yields have risen, in the last annual report, it didn't help the fund. Albeit, we are getting quite dated information at this point. We won't get their next semi-annual report until sometime in early March if history is any guide. However, I would suggest that the net investment income should decline further with rising interest rate costs and a long-maturity portfolio.

Here's what we see for NII as of June 30th, 2022.

RFM Annual Report (RiverNorth)

NII declined 7% year-over-year, and NII coverage came in at around 29%. That's some of the lowest I've seen for a fixed-income fund, but that's where the active management part comes in. RiverNorth exploits the discount/premium mechanic in CEFs to realize gains. In this case, it still wasn't enough to cover the distribution in the fiscal year.

However, the futures contracts, as we saw above, did help offset the realized losses they generated on their portfolio. It was enough to bring realized gains to the positive side.

They also announced a year-end long-term capital gain of $0.04001. That would indicate that later in the calendar year, they were able to dig up some gains somewhere.

For tax purposes, we will get more detailed information for 2022 later. Investors in a muni fund might be expecting a lot of tax-free distributions. Well, with RFM, that is a bit hit or miss.

RFM Tax Classifications (RiverNorth)

In 2020 , tax-free or "exempt-interest dividends" was a large portion of the distribution, but then in 2021, the majority of the distribution was classified as non-qualified dividends. We can also see a fair bit in 2022 looks like it'll be ordinary income as well.

RFM Tax Classifications (RiverNorth)

{kind=link}

RFM's Portfolio

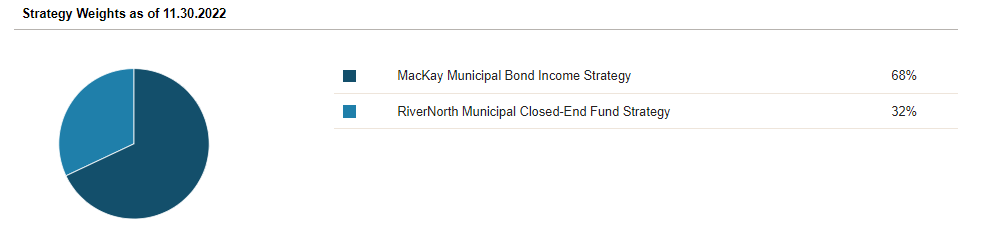

The latest portfolio allocation would align more closely with the "neutral CEF environment" they laid out above. This was similar to almost a year ago, so Mackay manages the bulk of the portfolio.

RFM Portfolio Positioning (RiverNorth)

{kind=link}

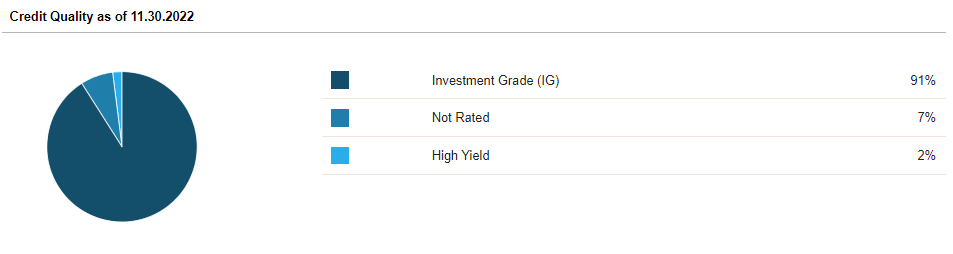

Being municipal bonds, a large portion of their portfolio is listed as investment-grade. That could be another benefit through 2023 if a recession happens, as most suggest having a good chance of occurring.

RFM Credit Quality (RiverNorth)

{kind=link}

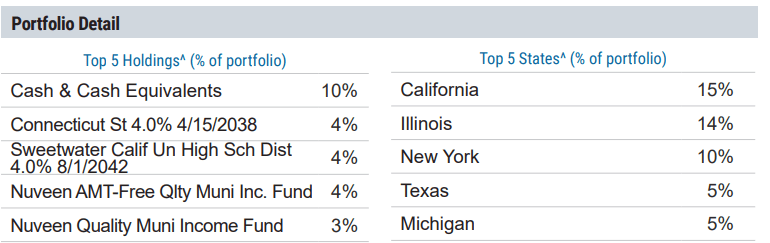

At the end of September 30th, 2022 , their fact sheet lists these as their top five holdings and top five state exposure.

{kind=link}

What might be interesting to note is that MacKay is investing the bulk of their portfolio, but there is an even split of 2 and 2 between individual and CEF holdings in the top spot. Cash takes up the largest allocation at the end of this reporting period.

The good news is that cash does earn something these days; the bad news is they hold their cash in the BlackRock Liquidity Funds MuniCash. At least, that is where they had it held at the end of June 2022.

It isn't good because MCSXX is an institutional money market fund that earns less than individual investors can get at Fidelity, interestingly enough. The 7-day yield listed was 2.57% compared to SPAXX at Fidelity, coming in at 3.87%.

Cash is only supposed to be a temporary parking place until they put it elsewhere. So I'm not sure if we should be too critical on this point or not.

When we look at Nuveen AMT-Free Quality Municipal Income Fund ( NEA ) and Nuveen Quality Municipal Income Fund ( NAD ), we can see more of the fund's appeal. That's the discount on discounts that a fund of funds can offer. In the last year, we can see that NEA and NAD had their discounts widened significantly. There was a very recent spike higher, but that's come back down quickly.

Ycharts

The income these two have been paying out has been trending lower and lower. That goes back to the higher interest expenses these funds now have to fork over. NEA has an effective leverage level of 40.17%, and NAD is at 40.26%. As long as interest rates are heading higher, this is likely to continue as interest expenses hit their total investment income, reducing their NII.

Ycharts

That's why we can also continue to expect RFM's income to decline too, but doubly as it is hit by its underlying holdings and on the fund level.

Conclusion

RFM is a bit of an unusual muni bond fund. There are a couple of bright spots, but it gets quite overshadowed by the bad. The fund's discount is large, and they invest some of their portfolios in other CEFs with similarly large discounts.

However, the continually increasing interest rates that the Fed has been doing will continue to hurt this fund. Admittedly, we should be nearer the end of this cycle than the beginning. Most of the negative impacts should be over. It hurts the fund directly by raising its interest rate expenses, and it also hurts its underlying holdings by raising its interest rate expenses too. That is on top of being highly interest rate-sensitive investments. The fund's high expense ratio makes it all an uphill battle too.

Additionally, this isn't a great choice if you are looking for tax-free income. A relatively limited amount is classified as tax-free despite their portfolio invested in munis.

Investing in this fund, one should expect a slow liquidation over time. The only time that would reverse - and it'd probably be temporary - is with strong bull markets combined with decreasing interest rates. In that scenario, bonds would rally, and CEF discounts would narrow. That's something we saw in 2020 and the beginning of 2021, where the fund worked quite well.

RFM Share And NAV Price (CEFConnect)

As soon as interest rates started to get hiked and CEF discounts widened, the fund tumbled. This was all exacerbated by the high utilization of leverage on the fund and the underlying holdings.

Personally, I'd avoid this fund, but I know some readers feel the other way strongly.

For further details see:

RFM: Better Valuation, But Not Great Prospects