SWX - RGC Resources: Disappointing Market Performance But Thesis Is Intact

2023-11-08 10:39:34 ET

Summary

- RGC Resources, Inc. is a small regulated natural gas utility serving Roanoke, Virginia, with a 4.65% yield.

- The company's stock price has fallen by 30.23% since March, possibly due to being underfollowed by market participants.

- RGC Resources has a stable customer base and has shown resistance to economic fluctuations, making it a reliable investment option.

- The company's forward growth is likely to be somewhat limited compared to other companies in the sector, but the valuation is very reasonable.

- The biggest concern here is that earnings growth will be slow, which makes this company somewhat like a bond with an annual coupon increase.

RGC Resources, Inc. ( RGCO ) is a relatively small regulated natural gas utility that serves the city of Roanoke, Virginia. As this company only serves a single midsized city, it is much smaller than most of the utilities that we discuss in this column. However, that does not mean that it has nothing to offer to investors. After all, the company still benefits from the same overall financial stability that most of its peers experience. It also has a very attractive 4.65% yield at the current price. That is, in fact, comparable or higher than many other pure-play natural gas utilities:

| Company |

| Current Yield |

| RGC Resources, Inc. |

| 4.65% |

| Northwest Natural Holding Company ( NWN ) |

| 5.17% |

| Southwest Gas Holdings, Inc. ( SWX ) |

| 4.14% |

| New Jersey Resources Corporation ( NJR ) |

| 3.97% |

| Atmos Energy Corporation ( ATO ) |

| 2.67% |

| Spire Inc. ( SR ) |

| 4.97% |

Admittedly, most of these companies are substantially larger than RGC Resources. The size of a company has nothing to do with its ability to earn money and provide dividends to its investors, however. Thus, the high yield could still prove useful for anyone who is seeking to generate a high level of income from the assets in its portfolio.

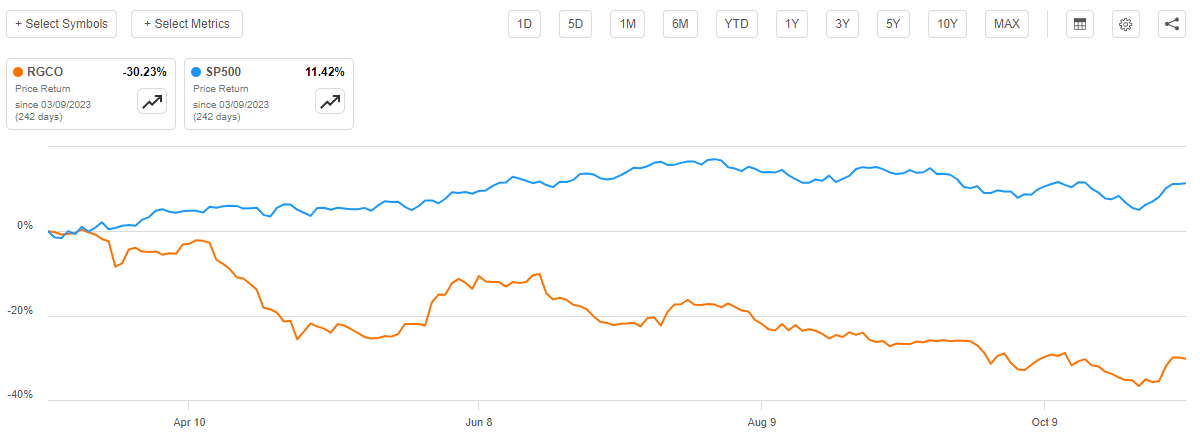

As regular readers may recall, we last discussed RGC Resources back in March. The company's stock price performance since that time has been incredibly disappointing. As we can see here, the stock has fallen by 30.23% since the date that my previous article was published:

{kind=link}

That performance will almost certainly remove this company from consideration in the minds of many readers. However, that alone should not really be the sole factor in a decision to avoid. After all, the company's fundamentals have not really changed and it did not cut its dividend, which would be the normal cause of a decline of this magnitude. Rather, it appears that the company may have just been the victim of being substantially underfollowed by most market participants, so it did not have the liquidity to support it as rates rose over the period. After all, only about 27,000 shares of RGC Resources trade every day so it will generally be more volatile than a larger company.

About RGC Resources

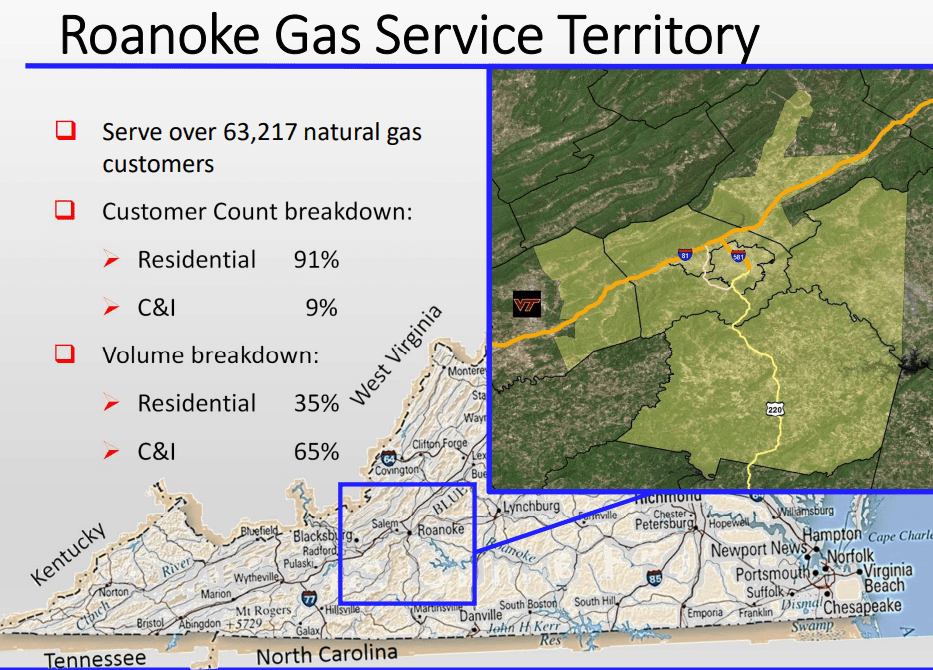

As mentioned in the introduction, RGC Resources is a regulated natural gas utility that serves the city of Roanoke, Virginia. According to the 2020 Census, Roanoke has a population of 100,011 people residing in 44,411 households. As most households would be on one utility bill, this somewhat limits RGC Resources' customer base. The company states that it serves 63,217 customers, which includes both residential and business customers. However, the company's business is heavily weighted to residential customers:

{kind=link}

That by itself is certainly not a bad thing. In fact, residential customers can be much more reliable utility customers than businesses. This is partly because residential customers are less affected by economic cycles. During a recession, for example, a commercial or industrial customer may opt to close down completely or take other steps that greatly reduce their consumption of natural gas. However, a residential customer will likely do everything in their power to ensure that the utility bill gets paid. After all, nobody wants to be without heat in the winter. This provides the company with a certain amount of financial stability through any economic climate.

As I pointed out in my previous article on RGC Resources:

The reason for this stability over time is that natural gas service to a home is generally considered to be a necessity. After all, heating during the winter months is actually protected by habitation laws and the government even provides assistance to help people pay their heating bills during the coldest months of the year. As such, people generally prioritize paying their natural gas bills ahead of other expenses during times when money gets tight.

Unfortunately, though, we can see that the vast majority of the company's revenue actually comes from commercial and industrial customers, as these entities consume far more natural gas than residential customers. This does expose the company to the business cycle somewhat, for reasons that have already been mentioned. In short, its revenue may certainly fluctuate with the economy, but its residential base does provide the company with more resistance to the business cycle than a company that is entirely dependent on consumer discretionary spending.

We can see some of this resistance to economic problems by looking at the company's revenues over time. Here are RGC Resources' revenues during each of the past eleven twelve-month periods:

{kind=link}

This period includes the effects of the widespread economic lockdowns throughout much of 2020 as well as the highly inflationary post-pandemic period. Yet, RGC Resources appears to have been largely unaffected by these changes in economic conditions.

We see the same thing if we look at the company's operating income over the same period:

{kind=link}

Once again, we can see that the company seems to be immune from anything that is going on in the broader economy. This is very comforting considering that the current direction of the economy is very uncertain.

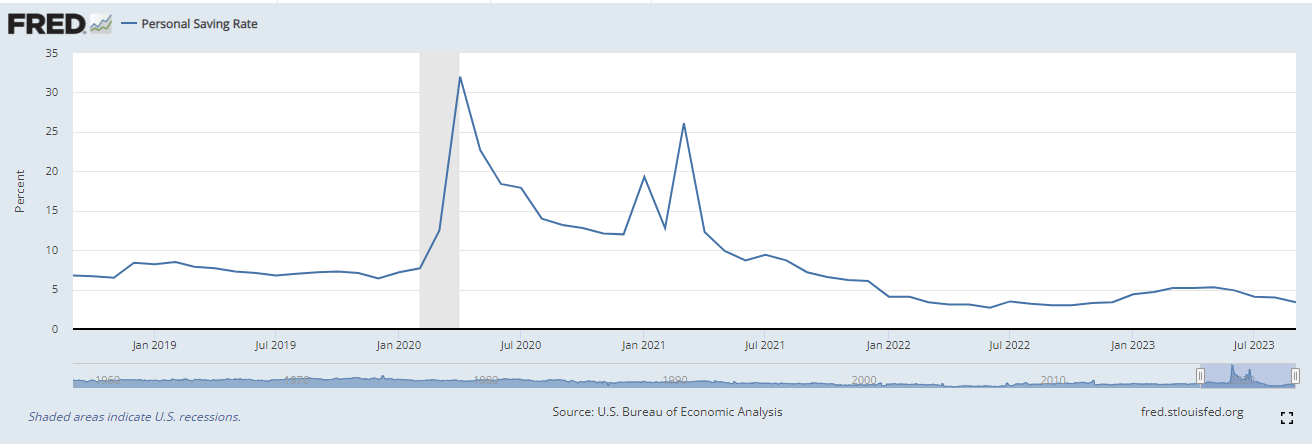

Consumption is generally stated to be about 70% of all economic activity that occurs in the United States. Naturally, this would require American consumers to be financially healthy. However, there are some signs that this is not the case. First, we have the fact that the personal savings rate has been declining. In September, the personal savings rate was 3.4%, which was the lowest level since December of 2022:

Federal Reserve Bank of St. Louis

{kind=link}

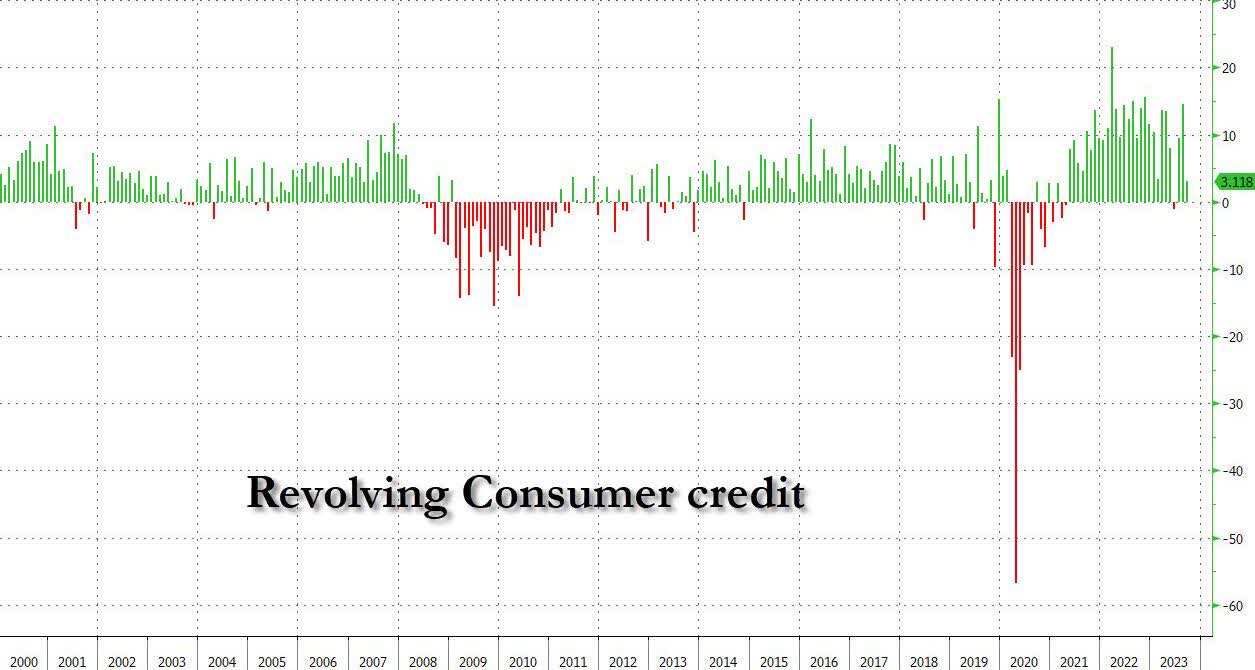

This is a sign that the U.S. consumer may be starting to get tapped out, especially when we consider that the increase in revolving credit card debt was only $3.1 billion in September, which was the lowest level since the pandemic (except for June 2023):

{kind=link}

These are both signs that the consumer is starting to seriously hurt financially. It appears they are reluctant to increase spending but at the same time, they are unable to save. The only explanation that I can think of is that inflation has driven non-discretionary spending to levels that are such a high percentage of incomes that consumers are unable to spend on gadgets, travel, and other things. As consumer spending on such things is an enormous percentage of gross domestic product, this is a sign that we could be entering a recession.

Fortunately, RGC Resources should prove to be resistant to consumer weakness since people will still pay their natural gas bills to keep their homes heated. That positions the company pretty well for whatever might be coming over the next few months.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. We would like to see growth from any company that we include in our portfolios. Fortunately, RGC Resources is well-positioned to deliver some growth going forward. The primary way through which the company will accomplish that goal is by increasing its rate base. I explained the concept of rate base in my last article on the company:

"The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows the company to increase or adjust its prices in order to achieve that specified rate of return. This is usually accomplished by spending money on upgrading, modernizing, or possibly expanding a company's utility-grade infrastructure."

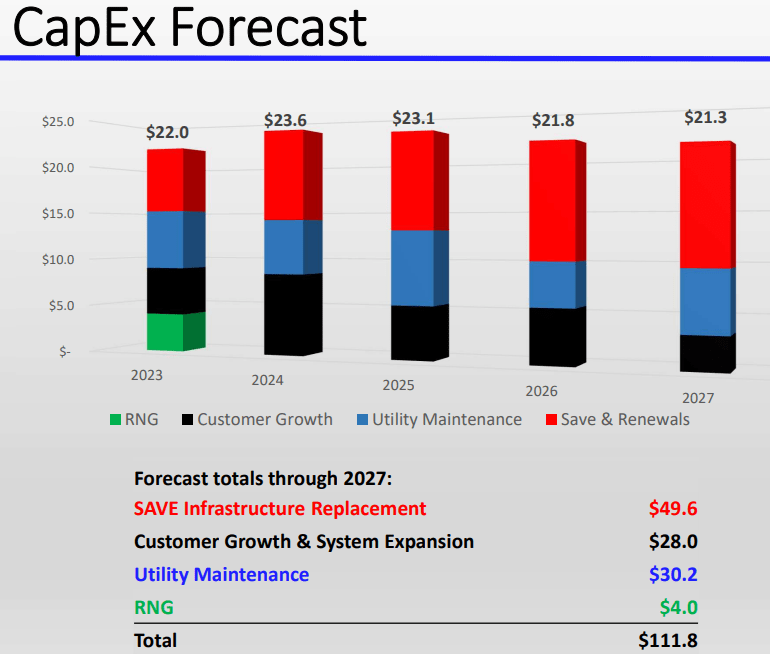

RGC Resources intends to engage in capital spending with just that goal in mind. The company recently put forward a five-year plan to invest a total of $111.8 million into its infrastructure over the 2023 to 2027 period:

{kind=link}

This is actually better than we have seen in the past. As I pointed out in my previous article on RGC Resources, this company has historically been somewhat more opaque about its capital spending plans than some of its peers.

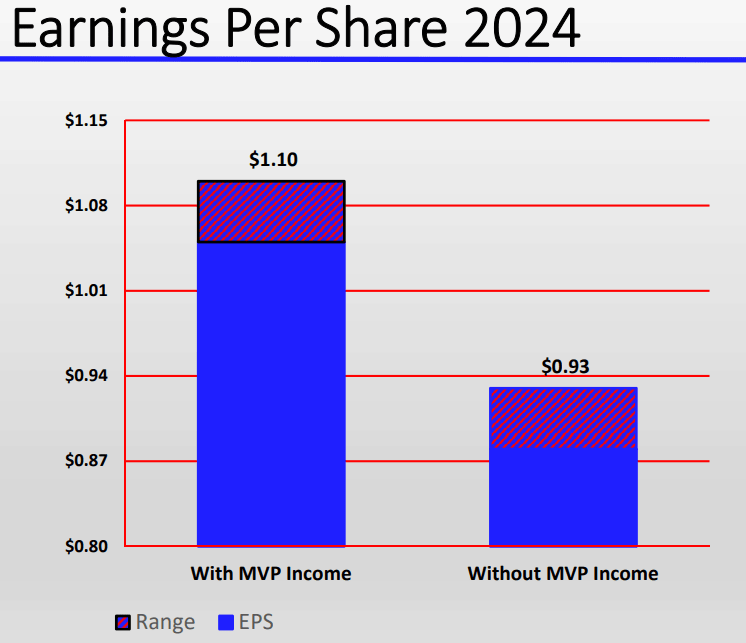

The company has not provided investors with any guidance regarding how much this rate base growth program will grow its earnings. The only thing that we have been provided with is preliminary guidance for 2024:

{kind=link}

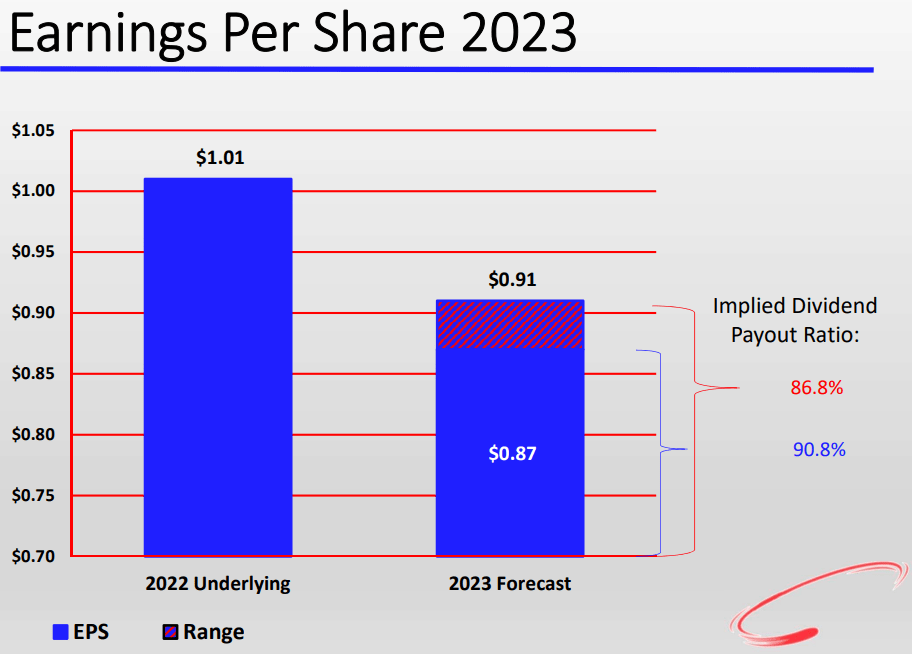

The 2024 midpoint guidance is $1.10 per share, $0.93 per share which will be from the natural gas utility itself. That is a 2.2% increase over the $0.91 per share midpoint guidance level for the full-year 2023 period:

{kind=link}

That is obviously not a very impressive growth rate, although the company should do better once we include the Mountain Valley Pipeline (which is proceeding to completion due to an act of Congress) into the mix.

The growth from the Mountain Valley Pipeline will mostly only be a one-time boost before the company falls back down to the much lower growth rate that we see in its guidance that excludes the pipeline income. If we assume that the company only manages to deliver 2.2% annual earnings per share growth, investors can only expect to receive a total average annual return of 6.85% including the dividend. That is far less than the company's peers are likely to deliver over the same period.

Zacks Investment Research does not appear to be especially optimistic about the company's growth either:

Zacks Investment Research

Overall, the company should prove to be better than a bond investment over the next five years but it does not appear that we should expect anything remarkable besides the earnings growth from the Mountain Valley Pipeline.

Financial Considerations

As I explained in my last article on this company:

It is always important that we review the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt, which can cause a company's interest expenses to increase under certain market conditions. This is something that may be a big concern today considering that the Federal Reserve has been actively raising interest rates over the past twenty months or so, causing newly issued debt to be more expensive than it once was.

As I have pointed out in a few recent articles on other utilities, many of these companies have been seeing rising interest expenses recently. RGC Resources is no exception to this, as can clearly be seen here:

{kind=link}

During the twelve-month period that ended on June 30, 2023, RGC Resources paid $5.4 million in interest related to its debt. That represents a 35% increase over the amount that the company paid during the full-year 2020 period. That is a pretty remarkable increase in just a short period of time. It may seem that a $1.4 million increase is not much, and it certainly would not be for a much larger company, but percentages are the most important thing and clearly, this company's debt is becoming an increasingly big burden for it. That is a problem because the more money that the company has to pay on debt servicing expenses, the less is available to make its way down to investors as either earnings growth or dividends.

Let us see if RGC Resources is overly reliant on debt to finance its operations. The usual way in which we do that is to compare the company's net debt-to-equity ratio to its peers.

As of June 30, 2023 (the most recent date for which data has been provided by the company), RGC Resources has a net debt of $130.7 million compared to a shareholders' equity of $100.9 million. This gives the company a net debt-to-equity ratio of 1.30 today. Here is how that compares to the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| RGC Resources, Inc. |

| 1.30 |

| Northwest Natural Holding Company |

| 1.22 |

| Southwest Gas Holdings, Inc. |

| 1.50 |

| New Jersey Resources Corporation |

| 1.59 |

| Atmos Energy Corporation |

| 0.61 |

| Spire Inc. |

| 1.54 |

(All figures as of June 30, 2023, to provide an appropriate comparison.)

This is very nice to see, as RGC Resources does not appear to be particularly heavily leveraged compared to its peers. That is a good sign, as it suggests that the company is not overly reliant on debt. It should, in fact, be a bit less risky overall than some of the other companies on this list. Thus, we should not have to worry too much about this company.

Dividend Analysis

One of the biggest reasons why investors purchase shares of utility companies is because of the high yields that these companies typically possess. RGC Resources is certainly no exception to this, as the company's 4.65% yield is considerably higher than the S&P 500 Index ( SP500 ) and compares quite well to its peers. We discussed this already.

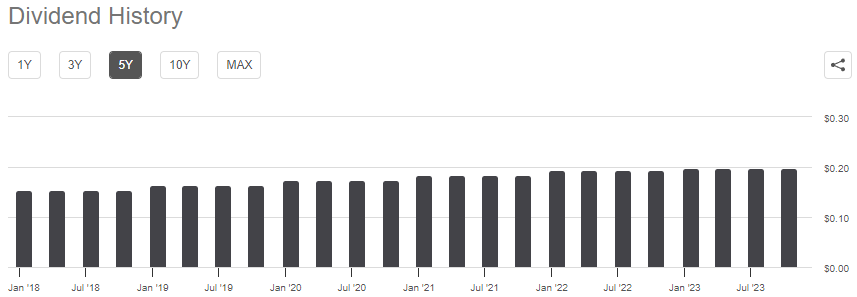

RGC Resources has a very long history of raising its dividend on an annual basis:

{kind=link}

This is something that we very much like to see, particularly during periods of inflation. After all, the inflation that we have seen over the past two years has been robbing investors of their purchasing power. The dividend naturally does not buy as much as it used to, which is a problem for anyone who depends on it to provide the money that they need to cover their bills or other lifestyle expenses. The fact that the company increases its dividend annually helps to offset this and helps to maintain the purchasing power of the dividend.

However, it is important that we ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our income and almost certainly causes the company's share price to decline.

The usual way that we judge a company's ability to afford its dividend is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, RGC Resources reported a negative leveraged free cash flow of $12.3 million. This is obviously not enough to pay any dividends, but the company still paid out $7.7 million in dividends to its shareholders over the period. At first glance, this is quite likely to be concerning as the company is clearly failing to generate enough cash internally to cover its regular expenses, capital expenditures, and dividends.

However, it is quite common for utilities to finance their capital expenditures through the issuance of debt and equity. They will then pay their dividends out of operating cash flow. This is done because of the incredibly high costs involved with constructing and maintaining utility-grade infrastructure over a wide geographic area. During the trailing twelve-month period, RGC Resources reported an operating cash flow of $19.4 million. That was more than sufficient to cover the $7.7 million that was paid out in dividends and leave the company with a respectable amount of money for other tasks.

Overall, the dividend is probably sustainable at the current level.

Valuation

According to Zacks Investment Research , RGC Resources is currently trading with a forward price-to-earnings ratio of 15.88. Here is how that compares to other pureplay natural gas utilities:

| Company |

| Forward P/E Ratio |

| RGC Resources, Inc. |

| 15.88 |

| Northwest Natural Holding Company |

| 14.09 |

| Southwest Gas Holdings, Inc. |

| 17.16 |

| New Jersey Resources Corporation |

| 15.03 |

| Atmos Energy Corporation |

| 17.14 |

| Spire Inc. |

| 13.56 |

This is a rather pleasant surprise. As we can see here, RGC Resources is reasonably in line with its peers in terms of current price. It is not overly expensive, but it is also not the cheapest company on the list. Thus, it may make sense to buy right now but it is not really offering a "must-buy" proposition right now.

Conclusion

In conclusion, RGC Resources is a small natural gas utility that does not get very much attention in the market. It has performed horribly this year, but it seems likely that its limited liquidity is one big reason for that. After all, the low volume of this stock means that it does not take very much money to move the share price substantially. Despite this relatively poor performance, though, the company's financials look fine as it is continuing to deliver the stability and high yield that we have come to expect from it. The company's valuation is acceptable as well.

For further details see:

RGC Resources: Disappointing Market Performance But Thesis Is Intact