RNMBF - Rheinmetall: Fiscal Constraints May Get In The Way Of War Premium

Summary

- It is generally accepted as an unassailable fact that the Ukraine conflict will lead to a sales bonanza for certain weapons producers.

- With the news that Leopard tanks are on their way to Ukraine, it might be argued that the maker of the tank, Rheinmetall, will greatly benefit.

- Rheinmetall's stock price has doubled since the Ukraine war started. There are widespread expectations of European countries ramping up military hardware spending, which is what the market is bullish about.

- The other side of the equation seems to be ignored, namely the fact that Europe has suffered permanent economic damage as a result of the conflict, therefore, fiscal resources are likely to be strained.

- EU countries are feeling increasingly fiscally stretched, with rising borrowing costs, and social spending needs, in the face of a severe energy crisis, as well as other economic support measures. Defense spending is likely to be cut, not increased in the long term.

Investment thesis: Rheinmetall AG (RNMBY) stock has been on a tear since the start of the war in Ukraine. It more than doubled in price, on expectations that the war will lead to a rush in Europe to stock up on military hardware, in response to a higher level of perceived threats, as well as in order to replace large volumes of hardware that have been sent to Ukraine since the start of the war, as well as before that. The other side of the equation tends to be ignored, namely the economic damage that the conflict has done to the European continent, as well as bleak economic prospects, going forward, as Europe's energy security has been badly compromised. While European governments may be making plans to increase military spending, fiscal constraints are likely to scupper many of those plans, and as that will start to happen, Rheinmetall's stock price, which is currently priced for a best-case outcome is likely to take a major hit.

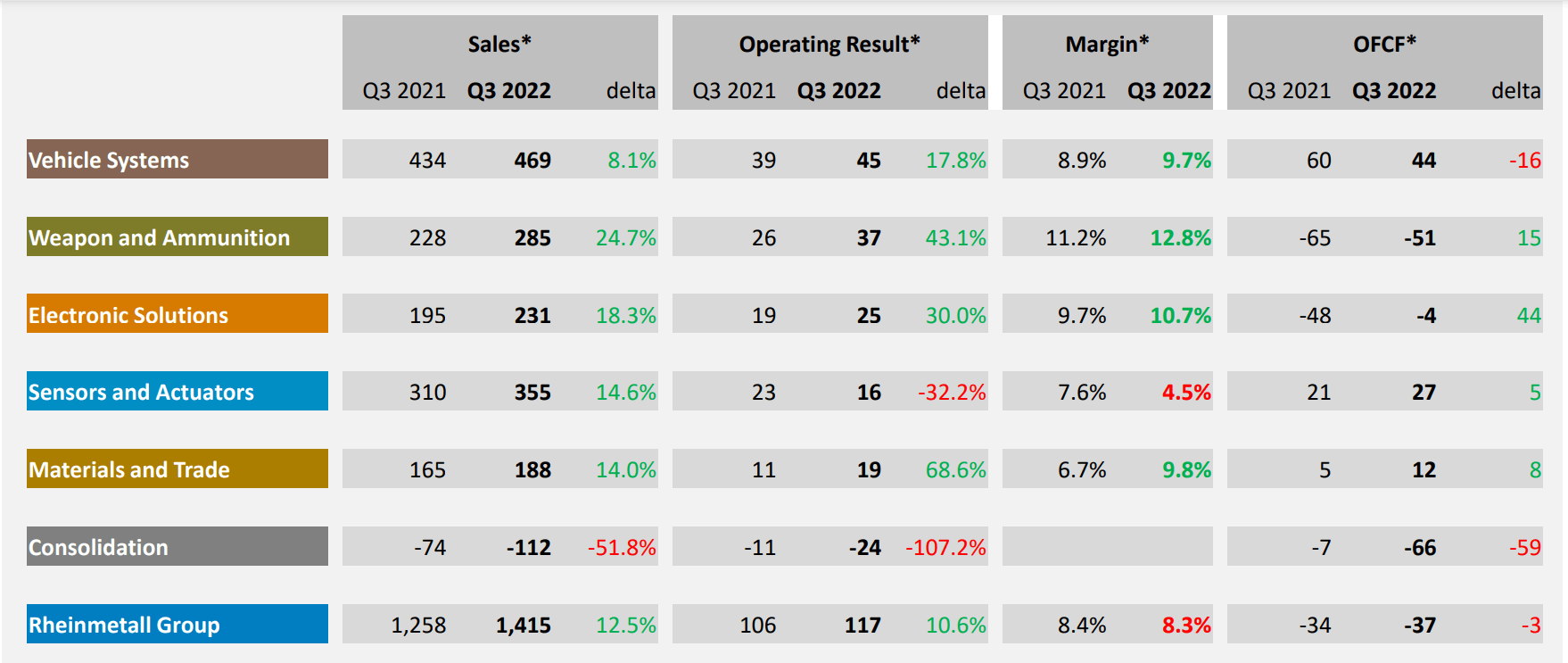

Rheinmetall's financial results improved in 2022, in contrast to the mostly gloomy overall economic situation in Europe.

{kind=link}

Even as the EU economy had about $800 billion shaved off of its GDP in USD terms, based on IMF estimates, Rheinmetall saw an increase in sales & operating results, with the military hardware segment leading the way, as may be expected. It should be noted that the segment is overall not dominant in terms of the company's business and product profile by any means.

{kind=link}

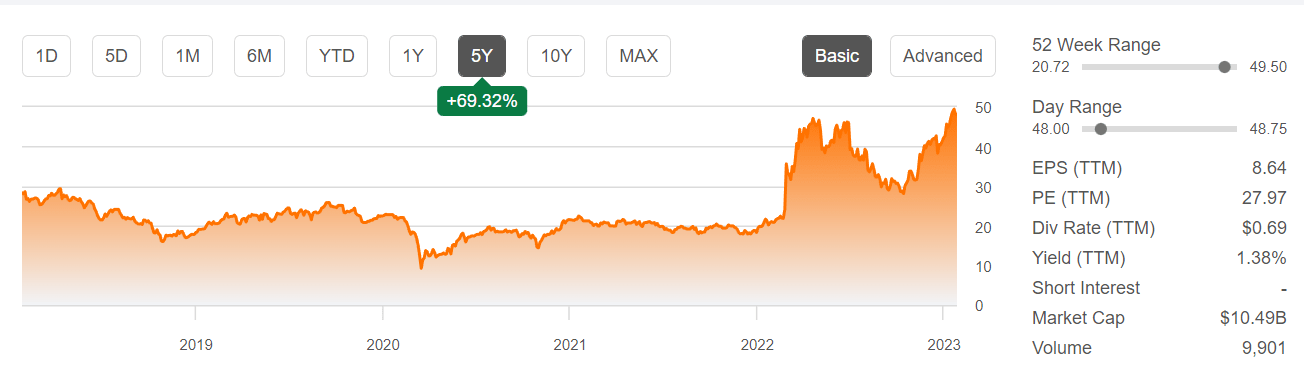

As we can see from Rheinmetall's five-year stock price profile, it took a great leap, that coincided with Russia's invasion of Ukraine. The obvious bet is that Rheinmetall is set to see a surge in military hardware sales, ranging from ammunition to the Leopard tanks that are seen as being among the best in the world in terms of price/value for the world's militaries.

It should be noted that while its stock price more than doubled in the past year in USD terms, its revenues as well as its operating returns performed rather poorly in USD terms, once we factor in the USD to euro conversion. The euro currency lost about 12% versus the US dollar from the end of the third quarter of 2021, until the end of the third quarter of 2022, which is the timeline represented in the financial results I referenced above. This means that, in USD terms, revenues as well as operating returns were about flat. The euro has been firming in the past few months, which should help the company's financial performance when measured in USD terms for the next few quarters, but it is questionable whether it will help a great deal in bringing that P/E ratio of about 28 back down to fundamental reality.

Europe's economy is in rough shape, and the outlook is not at all bright, meaning that defense spending may be cut in the long term.

As is the case with Rheinmetall's financial results, Europe's economic results last year have been a bit of a distortion. In euro terms, the EU economy expanded at a moderate pace. In USD terms, however, based on IMF estimates Germany's economy shrank by about $250 billion in USD terms, France's by about $180 billion, and Italy's by about $100 billion. Overall, the EU economy shrank by about $800 billion in nominal USD terms last year, if the early IMF estimates are correct. Other measures, such as real consumer purchasing power, and industrial production volumes, ranging from steel to fertilizers were in retreat.

This year, the EU economy is expected to grow by .3% in real euro terms, while a recovery is expected next year, although it remains to be seen if that will materialize and in what shape & form it will happen, if indeed it will happen. In my view, at this point, it all depends on the weather. Another mild winter next year could pave the way for an economic recovery, while a colder-than-average winter might prolong the current stagnant situation. A colder-than-average winter in both Europe and North America would most likely trigger a very deep economic crisis in the EU, as demand for gas will surge, even as the US, which is now Europe's biggest LNG supplier will cut supplies.

In the meantime, the EC is expecting deficits to remain over the crucial 3% threshold this year and next. In other words, fiscal pressures are set to remain. This may have not been a major issue of concern in the past decade as many EU governments experienced free borrowing. With government bond yields on the rise, however, this may no longer be the case going forward.

Those rising government debt yields may turn out to be Rheinmetall's greatest threat in terms of meeting the already very high expectations of increased business volumes, stemming from higher weapons sales expectations. By far its largest customers are within the EU, and many EU states may simply not be able to afford to splurge on military hardware spending. Yields on euro-denominated bonds have risen about 2.5 points in the past year, while the debt/GDP ratio in the eurozone is just under 100%. What this means is that in the next five years or so, with everything held at current levels, in other words, the debt/GDP as well as bond yields, we are looking at an increase in debt-servicing costs of about $300 billion in the next five years or so, as lower-yielding bonds mature and new bonds have to be issued in order to service the debt.

In addition to the presumably higher debt-servicing costs that EU nations will have to cope with going forward, it is also very likely that social welfare spending will have to be ramped up. The real buying power of Europeans has been shrinking this decade and I expect the trend will continue. The intensity of real buying power loss may depend on the weather. The weather may also end up affecting how much corporate welfare EU states will have to engage in. These things may add up to hundreds of billions of euros per year in extra spending needs. It may therefore be the case that European defense spending will not rise as much as it is currently predicted or expected.

Ukraine may end up receiving perhaps as many as 1,000 Leopard tanks if all expectations of a prolonged conflict will pan out. It is currently also assumed that European countries will want to expand their existing fleet of about 2,000 Leopard tanks. In theory this all adds up to perhaps increased demand for 2,000 or more Leopard tanks in the next few years, which is probably what the market is betting on when assuming that a doubling of the stock price in the past year was justified. In a worst-case scenario, most of those Leopard tanks that will be sent to Ukraine will come from current arsenals, which will not be replenished any time soon, which would only lead to a relatively modest increase in Rheinmetall's arms sales.

Investment implications:

Even if the best-case scenario were to come to fruition and Rheinmetall will see an influx of orders for thousands more tanks and other equipment this decade, it is still hard to justify the rally in its stock in my view. Not all of its products are meant for military purposes. Its automotive parts sector for instance, which based on its latest results makes up about one-third of its total sales could be particularly badly hit if the EU economy fails to recover. By some estimates, as much as 40% of the EU auto industry could disappear within the next few years. Persistently high energy prices can end up squeezing its profit margins, given that its manufacturing is mostly EU-based, so even if it will see a boom in orders, the profit margins might not be all that spectacular.

As things stand right now, the best-case scenario in terms of increased weapons sales is not at all guaranteed to happen. There are too many macro-economic headwinds in Europe at the moment, with too few prospects of improvement, which can lead to currently ambitious military spending programs being scaled back significantly once currently ambitious military spending plans will meet the harsh fiscal realities that many EU governments increasingly face.

For further details see:

Rheinmetall: Fiscal Constraints May Get In The Way Of War Premium